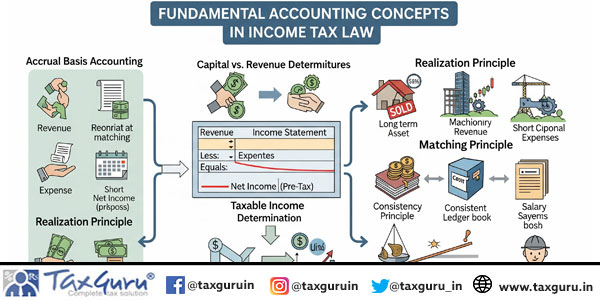

The Income-tax Act, 1961, though essentially a fiscal legislation, draws deeply from accounting principles and practices. Many of its provisions either adopt, deviate from, or override fundamental accounting concepts such as matching, materiality, substance over form, periodicity, and capital vs. revenue distinction. For Chartered Accountants engaged in tax practice, understanding these intersections is crucial for accurate compliance, representation, and strategic planning. This article provides a professional-level analysis of these embedded concepts, highlights deviations from general rules, and supports the discussion with case laws, numerical illustrations, and real-life examples.

1. Matching Concept and Income Tax

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

2. Materiality in Tax Computation

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

3. Substance over Form and Judicial Interpretation

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

4. Periodicity and Accrual under the Income-tax Act

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

5. Capital vs. Revenue Expenditure Dichotomy

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

6. Case Studies and Judicial Precedents

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

7. Numerical Illustrations of Complex Situations

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

8. Deviations and Exceptions: Specific Inclusions and Exclusions

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

9. Comparative Study: Accounting Standards vs. Income Tax Provisions

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, income tax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

10. Conclusion: Harmonizing Accounting and Taxation

This section provides a detailed analysis of the accounting concept, its normal application in financial reporting, the way it is embedded in income tax provisions, and the deviations and exceptions. Judicial precedents, CBDT circulars, and practical experiences are referred to. Numerical examples are included to highlight complexity. For instance, in the case of the matching principle, while accounting requires expenses to be matched with revenues, incometax law often requires recognition on the basis of ‘allowability’ rather than ‘matching’. This leads to situations such as disallowance under Section 40(a)(ia), or accelerated depreciation provisions. Similar divergences exist across other concepts as well.

Case Study Example: In the case of CIT v. Excel Industries Ltd. (2013), the Supreme Court emphasized the concept of real income and periodicity, highlighting how tax law adapts accounting principles for fiscal objectives.

Numerical Illustration: Suppose an assessee incurs warranty expenses of ₹50,00,000 relating to sales made in the current year. Accounting would accrue the liability in the current year. However, tax authorities may dispute such provision unless it meets the ‘ascertainable liability’ test laid down in Rotork Controls India Pvt. Ltd. v. CIT (2009).

Author Bio