What is House Rent Allowance (HRA): HRA Exemption, Tax Deduction, Rules & Regulations in the Indian Context

Abstract

House Rent Allowance (HRA) is a critical component of an individual’s salary structure in India. It is provided by employers to employees to help them meet rental housing expenses. HRA offers dual benefits: it aids employees in managing their housing costs and provides a potential tax-saving opportunity under the Income Tax Act, 1961. This blog delves into the nuances of HRA, its exemptions, tax deductions, and the rules governing it, specifically within the Indian context.

What is House Rent Allowance?

House Rent Allowance (HRA) is a monetary benefit provided by employers to employees as part of their salary. It is intended to help employees cover the cost of renting a house. HRA is particularly significant in urban and metropolitan areas where housing costs are high. The allowance varies depending on factors such as the employee’s salary, city of residence, and company policy.While HRA forms a part of the salary package, it is not entirely taxable. Employees can claim exemptions on HRA, provided they meet certain conditions laid down by the Income Tax Act.

FLOWCHART

Is HRA part of salary? → NO → No tax benefit

↓ YES

Are you paying rent? → NO → No tax benefit

↓ YES

Calculate tax-exempt HRA

↓

Submit rent receipts & landlord PAN (if applicable)

↓

Declare HRA details while filing ITR

↓

HRA Tax Deduction Applied!

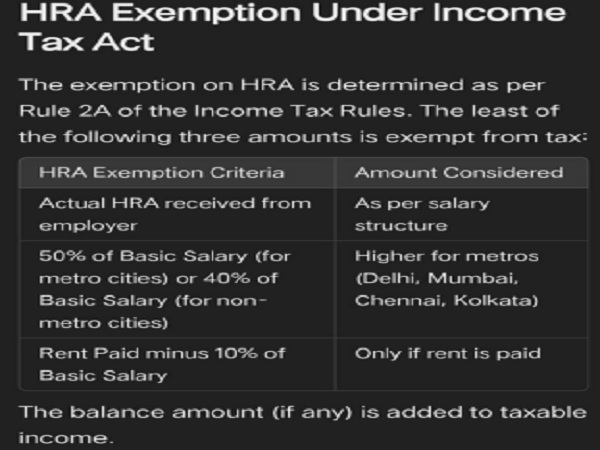

HRA Exemption Under the Income Tax Act

Section 10(13A) of the Income Tax Act, 1961, and Rule 2A of the Income Tax Rules govern the exemption of HRA. The exemption is calculated as the least of the following three amounts:

1. Actual HRA Received: The total HRA received from the employer during the financial year.

2. Rent Paid Minus 10% of Salary: Rent paid in excess of 10% of the employee’s basic salary.

3. 50% or 40% of Salary: 50% of the basic salary for employees living in metro cities (Delhi, Mumbai, Kolkata, and Chennai), and 40% for those residing in non-metro cities.

Salary here includes basic salary, dearness allowance (if it forms part of retirement benefits), and commission (if calculated as a percentage of turnover).

For instance:

- If your basic salary is ₹50,000 per month, and you pay ₹30,000 as monthly rent in a metro city, the HRA exemption will be the least of the following:

1. Actual HRA received (say ₹20,000/month = ₹2,40,000 annually).

2. Rent paid minus 10% of salary: ₹30,000 – ₹5,000 = ₹25,000/month (₹3,00,000 annually).

3. 50% of salary: ₹50,000 × 50% = ₹25,000/month (₹3,00,000 annually).

Thus, the exemption will be the least, i.e., ₹2,40,000 annually.

The remaining portion of HRA, if any, is taxable as part of your income.

Conditions to Claim HRA Exemption

To claim HRA exemption, certain conditions must be met:

1. Employee Must Pay Rent: The employee must pay rent for residential accommodation. The exemption cannot be claimed if the employee resides in their own house.

2. Rent Receipts Are Essential: Employees must submit rent receipts or a rental agreement to their employer as proof of rent payment.

3. PAN of Landlord: If the annual rent exceeds ₹1,00,000, employees must provide the landlord’s PAN to the employer. In the absence of a PAN, a declaration from the landlord is required.

4. Exemption for Only One Property: HRA exemption can be claimed for only one rented property, even if the employee has multiple rented accommodations.

HRA Exemption for Self-Employed Individuals

Self-employed individuals are not eligible for HRA under Section 10(13A). However, they can claim a deduction under Section 80GG of the Income Tax Act. To do so:

- The individual must not receive HRA.

- They should not own a house in the same city where they reside.

- The deduction is capped at the least of the following:

1. ₹5,000 per month.

2. 25% of total income (excluding capital gains).

3. Rent paid minus 10% of total income.

Tax Benefits of HRA

HRA offers significant tax benefits by reducing the taxable portion of an employee’s income. These benefits, however, are contingent upon proper documentation and adherence to the rules. Here’s why HRA is advantageous:

1. Reduces Taxable Income: A substantial portion of HRA can be exempted, lowering the employee’s overall tax liability.

2. Ease of Claim: The exemption is straightforward to claim, provided the employee maintains proper records, such as rent receipts and rental agreements.

3. Encourages Savings: By lowering the taxable income, HRA indirectly encourages savings, allowing employees to allocate funds to other financial goals.

Rules and Regulations Governing HRA

To ensure compliance with tax laws, the following rules govern HRA:

1. Separate HRA from Basic Salary: HRA is calculated separately from the basic salary and is listed as a distinct component of the salary slip.

2. Mandatory Documentation: Employees must submit rent receipts, agreements, and the landlord’s PAN (if required) to claim exemption.

3. HRA for Joint Renters: If multiple individuals share a rented property, each can claim HRA exemption proportionate to their contribution to the rent. Adequate documentation and rent-sharing agreements are necessary.

4. HRA and Home Loans: Employees with a home loan can simultaneously claim HRA exemption and deductions for home loan interest and principal repayment. However, they must reside in a rented house and justify why their own house is not being used.

Common Misconceptions About HRA

1. Owning a House and Claiming HRA: Many believe owning a house disqualifies an individual from claiming HRA. However, HRA can be claimed if the employee lives in a rented house in a different city from their owned property.

2. HRA Covers All Rent: HRA exemption is calculated based on specific rules and may not cover the entire rent paid.

3. No Rent Agreement Required: A valid rent agreement is essential for claiming HRA exemptions, especially in case of disputes or audits by the Income Tax Department.

Conclusion

House Rent Allowance (HRA) plays a pivotal role in the financial planning of salaried individuals in India. By understanding the exemption rules, maintaining proper documentation, and adhering to tax laws, employees can leverage HRA to reduce their tax burden significantly. Employers, too, benefit by structuring salaries to include HRA, ensuring compliance and enhancing employee satisfaction.

With housing costs on the rise, especially in urban centres, HRA remains a vital component of salary structures. Whether you’re a salaried employee or self-employed, understanding the intricacies of HRA can help you optimize your financial planning and make the most of the tax-saving opportunities available in India.

****

BY: ANSHU CHAUDHARY | 4TH YEAR STUDENT , BA LLB. HONS. | LOVELY PROFESSIONAL UNIVERSITY