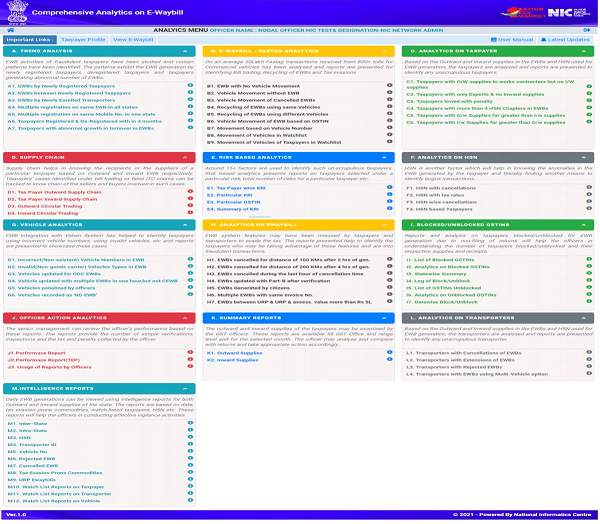

The Comprehensive Analytics on E-Way Bill provides all the analytics and reports provided under one umbrella. The reports are spread out on the screen in one glance. This will help the officer in quickly identifying the reports and making use of it. The reports are numbered so that they may be referred quickly for correspondence.

Comprehensive Analytics On E-Way Bill system

| Table of Contents | Page |

| Introduction | 4 |

| A. Trend Analysis | 5 |

| A1. EWBS BY NEWLY REGISTERED TAXPAYERS | 6 |

| A2. EWBS BETWEEN NEWLY REGISTERED TAXPAYERS | 7 |

| A3. EWBS BY NEWLY ENROLLED TRANSPORTERS | 8 |

| A4. MULTIPLE REGISTRATION ON SAME PAN IN ALL STATES | 9 |

| A5. MULTIPLE REGISTRATION ON SAME MOBILE NUMBER IN ONE STATE | 10 |

| A6. TAXPAYERS REGISTERED & DE-REGISTERED WITHIN 3 MONTHS | 10 |

| A7. TAXPAYERS WITH ABNORMAL GROWTH IN THE TURNOVER IN EWBS | 11 |

| B. E-Waybill Fastag Analytics | 12 |

| B1. E-WAYBILLS WITH NO VEHICLE MOVEMENT | 13 |

| B2. VEHICLE MOVEMENT WITHOUT EWB | 14 |

| B3. VEHICLE MOVEMENT OF CANCELLED EWBS | 15 |

| B6. RFID ANALYSIS ON EWB BASED ON GSTIN | 17 |

| B7. MOVEMENT BASED ON VEHICLE NUMBER | 18 |

| B8. MOVEMENT OF VEHICLES REGISTERED IN STATE/ZONE WATCH LIST | 19 |

| B9. MOVEMENT OF VEHICLES OF TAXPAYERS IN WATCH LIST | 20 |

| C. Analytics On Taxpayer | 21 |

| C1. TAXPAYERS WITH OUTWARD SUPPLIES TO WORKS CONTRACTORS BUT NO INWARD SUPPLIES | 21 |

| C2. TAXPAYERS WITH ONLY EXPORTS & NO INWARD SUPPLIES | 22 |

| C3. TAXPAYERS LEVIED WITH PENALTY | 22 |

| C4.TAX PAYERS WITH MORE THAN 4 HSN CHAPTERS IN EWBS | 23 |

| C5. TAXPAYERS WITH MORE OUTWARD SUPPLIES FAR GREATER THAN INWARD SUPPLIES | 23 |

| C6. TAXPAYERS WITH MORE INWARD SUPPLIES FAR GREATER THAN OUTWARD SUPPLIES | 24 |

| D. Supply Chain | 25 |

| D1.TAX PAYER OUTWARD SUPPLY CHAIN | 25 |

| D2.TAX PAYER INWARD SUPPLY CHAIN | 28 |

| D3. OUTWARD CIRCULAR TRADING | 31 |

| D4. INWARD CIRCULAR TRADING | 32 |

| E. Risk Based Analytics | 33 |

| E1. Taxpayer wise KRIs | 38 |

| E2. Particular Key Risk Indicator | 39 |

| E3. Risk analysis report for GSTIN | 41 |

| E4. Risk Analysis summary | 43 |

| F. Analytics On HSN | 44 |

| F1. HSN WITH CANCELLATIONS | 44 |

| F2. HSN WITH TAX RATES | 45 |

| F3. HSN WISE CANCELLATIONS | 45 |

| F4.HSN BASED TAXPAYERS | 46 |

| G. Vehicle Analytics | 47 |

| G1. INCORRECT (NON-EXISTENT) VEHICLE NUMBERS IN EWB | 47 |

| G2. INVALID (NON-GOODS CARRIER) VEHICLES TYPES IN EWB | 48 |

| G3. VEHICLES UPDATED FOR ODC EWBS | 49 |

| G4. Vehicle Updated with Multiple EWBs in one Hour, but Not CEWB | 50 |

| G5. Vehicles Penalized by Officers | 51 |

| G6. Vehicles Recorded As ‘No EWB’ | 52 |

| H. Analytics on E-waybill | 53 |

| H1. EWBS CANCELLED FOR DISTANCE OF 100 KMS AFTER 2 HOURS OF GENERATION | 53 |

| H2. EWBS CANCELLED FOR DISTANCE OF 200 KMS AFTER 4 HOURS OF GENERATION | 54 |

| H3. EWBS CANCELLED DURING THE LAST HOUR OF CANCELLATION TIME | 54 |

| H4. EWBS UPDATED WITH PART-B AFTER VERIFICATION | 55 |

| H5. EWBS GENERATED BY CITIZENS | 56 |

| H6. MULTIPLE EWBS WITH SAME INVOICE NO. | 56 |

| H7. EWBs between URP and URP of assessable value more than Rs. 5 lakhs | 57 |

| I. Blocked/Unblocked GSTINs | 58 |

| I1. LIST OF BLOCKED GSTINS | 58 |

| I2. ANALYTICS ON BLOCKED GSTINS | 59 |

| I3. STATEWISE SUMMARY | 59 |

| I4. BLOCK/UNBLOCK DETAILS OF GSTIN | 60 |

| I5. LIST OF GSTIN UNBLOCKED | 60 |

| I6. ANALYTICS ON UNBLOCKED GSTINS | 61 |

| I7. DATE WISE BLOCK/UNBLOCK GSTIN LIST | 61 |

| J. Officer Action Analytics | 62 |

| J1. Performance Report | 63 |

| J2. Performance Report Based on Tax Evasion Prone Commodities | 64 |

| J3. Usage of Reports by Officers | 65 |

| K. Summary Reports | 66 |

| K1. Outward Supplies | 66 |

| K2. Inward Supplies | 66 |

| L. Analytics On Transporter | 67 |

| L1. TRANSPORTERS WITH CANCELLATIONS OF EWBS | 67 |

| L2. TRANSPORTERS WITH EXTENSIONS OF EWBS | 68 |

| L3. TRANSPORTERS WITH REJECTED EWBS | 69 |

| L4. TRANSPORTERS WITH EWBS USING MULTI VEHICLE OPTION | 69 |

| M. Intelligence Reports | 70 |

| M1. INTER STATE | 71 |

| M2. INTRA STATE | 72 |

| M3. HSN | 72 |

| M4. TRANSPORTER ID | 73 |

| M5. VEHICLE NUMBER | 73 |

| M6. REJECTED EWB | 74 |

| M7. CANCELLED EWB | 75 |

| M8. TAX EVASION PRONE COMMODITY | 75 |

| M10.WATCH LIST REPORTS ON TAXPAYERS | 76 |

| M11.WATCH LIST REPORTS ON TRANSPORTERS | 77 |

Introduction

The Comprehensive Analytics on E-Way Bill provides all the analytics and reports provided under one umbrella. The reports are spread out on the screen in one glance. This will help the officer in quickly identifying the reports and making use of it. The reports are numbered so that they may be referred quickly for correspondence.

The E-Waybill system is integrated with Fastag and Vahan System. The vehicle movement details from 800+ tolls are being consumed by the e-waybill system. On a daily average, around 30 Lakh transactions are sent by NPCI system to e-waybill system. Analytics on Fastag integration will help in identifying the taxpayers who are into fake invoicing, tax evasion, recycling of EWBs etc.