Securities and Exchange Board of India (SEBI), as a regulatory body, consistently amends its regulations to adapt to the changing financial landscape. This article sheds light on the Master Circular (No. SEBI/HO/DDHS/PoD1/P/CIR/2023/119) updated as on July 07, 2023, which encompasses the issue and listing guidelines for various non-convertible securities, municipal debt securities, commercial papers, and more.

The Master Circular incorporates regulations that were enacted as a consequence of merging SEBI (Issue and Listing of Debt Securities) Regulations, 2008, and SEBI (Issue and Listing of Non-Convertible Redeemable Preference Shares) Regulations, 2013, into the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021. It supersedes multiple circulars covering procedural and operational aspects, providing a consolidated reference for issuers and other market stakeholders.

This circular not only covers instruments under the NCS Regulations but also provisions applicable to the issue of securities under the SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008 and SEBI (Issue and Listing of Municipal Debt Securities) Regulations, 2015. It directs all stakeholders to comply with its provisions, update necessary systems and infrastructure, make consequential changes to their respective bye-laws, rules and regulations, and ensure effective communication and awareness among other stakeholders.

Securities and Exchange Board of India

Master Circular No. SEBI/HO/DDHS/PoD1/P/CIR/2023/119 Dated: August 10, 2021

(updated as on July 07, 2023)

To,

Issuers who have listed and / or propose to list Non-convertible Securities, Securitised Debt Instruments, Security Receipts, Municipal Debt Securities or Commercial Paper1,;

Recognised Stock Exchanges;

Registered Depositories;

Registered Credit Rating Agencies, Debenture Trustees, Depository Participants, Stock Brokers, Merchant Bankers, Registrars to an Issue and Share Transfer Agents, Bankers to an Issue;

Sponsor Banks;

Self-Certified Syndicate Banks; and

National Payments Corporation of India

Madam/ Sir,

Sub: Master Circular2 for issue and listing of Non-convertible Securities, Securitised Debt Instruments, Security Receipts, Municipal Debt Securities and Commercial Paper

1. Vide notification no. SEBI/LAD-NRO/GN/2021/39 dated August 09, 2021, SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021 (hereinafter referred to as the SEBI NCS Regulations, 2021) were notified, pursuant to merger and repeal of the SEBI (Issue and Listing of Debt Securities) Regulations, 2008 (hereinafter referred to as the SEBI ILDS Regulations, 2008) and SEBI (Issue and Listing of Non-Convertible Redeemable Preference Shares) Regulations, 2013 (hereinafter referred to as the SEBI NCRPS Regulations, 2013).

2. Since the notification of the SEBI ILDS Regulations, 2008 and the SEBI NCRPS Regulations, 2013 and subsequent notification of SEBI NCS Regulations, 2021, SEBI has issued multiple circulars covering procedural and operational aspects thereof.

3. For effective regulation of the corporate bond market and to enable the issuers and other market stakeholders to get access to all the applicable circulars at one place, this Master Circular has been prepared.

4. The process of merging these regulations into the SEBI NCS Regulations, 2021 also entailed consolidation of related existing circulars (Annex – 1) into a single operational circular, with consequent changes. The stipulations contained in such circulars have been detailed chapter-wise in this Master circular. Accordingly, the circulars listed at Annex – 1 of this Master Circular stand superseded by this Master

5. While this circular covers instruments under the NCS Regulations, certain chapters contain provisions applicable to issue of securities under the SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008 (hereinafter referred to as the SEBI SDI Regulations, 2008) and SEBI (Issue and Listing of Municipal Debt Securities) Regulations, 2015 (hereinafter referred to as the SEBI ILDM Regulations, 2015). This has been accordingly indicated in the chapters.

6. Notwithstanding the supersession as mentioned in Clause 3 of this circular3, –

6.1. anything done or any action taken or purported to have been done or taken under the rescinded circulars, prior to such rescission, shall be deemed to have been done or taken under the corresponding provisions of this Master Circular;

6.2. any application made to the Board under the rescinded circulars, prior to such rescission, and pending before it shall be deemed to have been made under the corresponding provisions of these regulations;

7. Recognized Stock Exchanges, Depositories, other SEBI registered intermediaries, Issuers and other stakeholders are directed to:

7.1. Disseminate the provisions of this circular on their website4;

7.2. comply with the conditions laid down in this circular;

7.3. put in place necessary systems and infrastructure for implementation of this circular;

7.4. make consequential changes, if any, to their respective bye-laws, rules and regulations and bidding portal; and

7.5. Communicate and create awareness amongst stakeholders.

7.6. Monitor the compliance of this circular by issuer companies, as applicable5

8. This Circular is issued in exercise of powers conferred under: 1. Section 11(1) of Securities and Exchange Board of India Act, 1992;

8.2. Regulation 55 of SEBI NCS Regulations, 2021; 8.3. Regulation 29 of SEBI ILDM Regulations 2015; 8.4. Regulations 48 of SEBI SDI Regulations, 2008.

9. This circular shall come into force with effect from August 16, 2021, unless specifically mentioned otherwise in this circular.6

10. This Circular is available on SEBI website at www.sebi.gov.in under the “Legal Framework”.

Yours faithfully,

Pradeep Ramakrishnan

General Manager

Department of Debt and Hybrid Securities

+91 – 022 2644 9246

pradeepr@sebi.gov.in

Page Contents

- Chapter I – Application process in case of public issues of securities and timelines for listing7

- Chapter II – Application form and Abridged Prospectus12

- Chapter III – Day count convention, disclosure of cash flows and other disclosures in the offer document14

- Chapter IV – Additional Disclosures by Non-Banking Finance Company or Housing Finance Company or Public Financial Institution15

- Chapter V – Denomination of issuance and trading of Non-convertible Securities

- Chapter VI – Electronic Book Provider platform18

- Chapter VII – Standardization of timelines for listing of securities issued on a private placement basis19

- Chapter VIII – Specifications related to ISIN for debt securities20

- Chapter IX – Green Debt Securities22

- Chapter IX-A – Dos and don’ts relating to green debt securities to avoid occurrences of greenwashing23

- Chapter IX-B – Additional Requirements for the issuers of Transition Bonds24

- Chapter X – Structured or market linked debt securities25

- Chapter XI – Operational framework for transactions in defaulted debt securities post maturity date/ redemption date26

- Chapter XII – Fund raising by issuance of debt securities by large corporate28

Chapter I – Application process in case of public issues of securities and timelines for listing7

[See Regulations 34, 35 and Clause 2.2.28 of Schedule I of SEBI NCS Regulations, 2021, Regulation 10 and Clause 7(h) of Schedule I of SEBI ILDM Regulations, 2015 and Regulation 31 of SEBI SDI Regulations, 2008]

Applicability:

The provisions under this chapter shall be applicable for public issues of securities under SEBI NCS Regulations, 2021, SEBI ILDM Regulations, 2015 and SEBI SDI Regulations, 2008.

Procedure for making application through ASBA mechanism:

1. Investors applying in a public issue shall use ASBA facility for making payment:

1.1. by either writing their bank account numbers and authorising the banks to make payment in case of allotment by signing the application forms; or

1.2. mentioning UPI ID in order to block the funds. The investor may utilize the UPI mechanism to block the funds for application value up to Rs. 5 lakh8 per application.

2. Modes of application in public issue of securities: An investor may apply for public issue of securities through any of the following modes:

2.1. Through SCSBs or intermediaries (viz. syndicate members, registered stock brokers, registrar and transfer agent and depository participants):

a) An investor may submit the bid-cum-application form, with ASBA as the sole mechanism for making payment, physically at the branch of a SCSB, i.e. investor’s bank. For such applications, the SCSB shall upload the bid on the stock exchange bidding platform and block funds in the investor’s account.

b) An investor may submit the completed bid-cum-application form to intermediaries mentioned above along with details of his/ her bank account for blocking of funds. The intermediary shall upload the bid on the stock exchange bidding platform and forward the application form to a branch of a SCSB for blocking of funds.

c) An investor may submit the bid-cum-application form with a SCSB or the intermediaries mentioned above and use his/ her bank account linked UPI ID for the purpose of blocking of funds, if the application value is Rs. 5 lakh9 or less. The intermediary shall upload the bid on the stock exchange bidding The application amount would be blocked through the UPI mechanism in this case.

2.2. Through stock exchanges (App/ Web interface): An investor may submit the bid-cum-application form through the App or web interface developed by stock exchanges wherein the bid is automatically uploaded onto the stock exchange bidding platform and the amount is blocked using the UPI mechanism.

3. Role of SCSBs and intermediaries:

3.1. The SCSBs or the above-mentioned intermediaries shall, at the time of receipt of the application, provide an acknowledgement to the investor, by giving the counter foil or specifying the application number to the investor, as proof of having accepted the application form, in physical or electronic mode, respectively.

3.2. For applications submitted by investors to SCSBs: After accepting the form, the SCSB shall capture and upload details in the electronic bidding system as specified by the stock exchange(s) and may begin blocking of funds available in the bank account specified in the form, to the extent of the application money specified.

3.3. For applications submitted by investors to other intermediaries: After accepting the application form, the respective intermediary shall capture and upload details in the electronic bidding system as specified by the stock exchange(s).

3.4. SCSBs shall carry out further action for ASBA forms such as signature verification, blocking of funds etc. and forward these forms to the registrar to the issue.

3.5. The SCSBs or intermediaries shall guide investors in making applications in public issues and are advised to take necessary steps to ensure compliance in this regard.

3.6. SCSBs are advised to ensure that they shall block the application amount only against/ in a funded deposit account and ensure that clear demarcated funds are available.

3.7. SCSBs are also advised to ensure that for making applications on own account using ASBA facility, they should have a separate account in own name with any other SEBI registered SCSBs. Such account shall be used solely for the purpose of applying in public issues and clear demarcated funds should be available in such account for ASBA applications.

4. Role of the stock exchanges:

4.1. Stock exchange(s) shall allow modification of selected fields viz. DP ID/ Client ID or PAN (Either DP ID/ Client ID or PAN can be modified but not both), bank code and location code in the bid details already uploaded, on a daily basis within the timeline as specified.

4.2. Stock exchanges shall have systems to facilitate investors to view the status of their public issue applications on their websites; and to send the details of applications and allotments through SMS and e-mail alerts to the investors.

5. Role of entities/ mechanisms part of the public issue process using UPI:

5.1. NPCI, a RBI initiative, is an umbrella organization for all retail payments in India. It has been set up with the guidance and support of the RBI and IBA;

5.2. UPI is an instant payment system developed by NPCI. It enables merging several banking features, seamless fund routing & merchant payments into one hood. UPI allows instant transfer of money between any two persons’ bank accounts using a payment address which uniquely identifies a person’s bank account.

5.3. Sponsor Bank means a Banker to the Issue registered with SEBI which is appointed by the Issuer to act as a conduit between the stock exchanges and the NPCI in order to push the mandate collect requests and/ or payment instructions of investors10 into the UPI.

6. Validation by stock exchanges and depositories:

6.1. The details of investor viz. PAN, DP ID/ Client ID, entered on the stock exchange platform at the time of bidding, shall be validated by the stock exchange(s) with the Depositories on real time basis.

6.2. Stock exchanges and Depositories shall put in place necessary infrastructure for this purpose.

7. Other requirements:

7.1. Stock exchanges shall update demand data on working days on their websites which shall include all the UPI (accepted/ pending) and ASBA bids.

7.2. The details of commission and processing fees payable to each intermediary and the timelines for payment shall be disclosed in the offer document.

7.3. The intermediaries shall provide necessary guidance to their investors in use of UPI while making applications in public issues.

7.4. Stock exchanges shall formulate and disclose the operational procedure for applying through the app/ web based interface developed by them in order to apply in public issue on their websites.

7.5. The merchant banker shall ensure that the process of applying through the App/ web interface developed by the stock exchanges as well as the additional payment mechanism through UPI is disclosed in the offer document.

7.6. All entities involved in the process are advised to take necessary steps to ensure compliance with this circular.

8. The character length for each of fields of the schedule to be forwarded by the intermediaries along with each application form to the designated branches of the respective SCSBs for blocking of funds shall be uniformly prescribed by the stock exchange(s) and the format of the schedule shall be as under:

Table 1: Format of the character length of the fields of the schedule

| Field number | Details |

| 1 | Symbol |

| 2 | Bid Date |

| 3 | Intermediary Code |

| 4 | Intermediary name |

| 5 | Bank code |

| 6 | Bank name |

| 7 | Location Code |

| 8 | Application No. |

| 9 | Category |

| 10 | PAN |

| 11 | DP ID |

| 12 | Client ID |

| 13 | Quantity |

| 14 | Series |

| 15 | Amount |

| 16 | Stock exchange |

9. Further modalities in relation to UPI Process:

9.1. Bidding and validation process:

a) Before submission of the application with the intermediary, the investor would be required to have/ create a UPI ID, with a maximum length of 45 characters including the handle (example: investorid@bankname).

b) An investor shall fill in the bid details in the application form along with his/ her bank account linked UPI ID and submit the application with any of the intermediaries or through the stock exchanges App/ Web interface.

c) The intermediary, upon receipt of form, shall upload the bid details along with the UPI ID on the stock exchange bidding platform using appropriate

d) Once the bid has been entered on the bidding platform, the stock exchange shall undertake validation of the PAN and demat account combination details of investor with the depository.

e) The depository shall validate the aforesaid PAN and demat account details on a near real time basis and send response to stock exchange which would be shared by stock exchange with intermediary through its platform, for corrections, if any.

f) Once the bid details are uploaded on the stock exchange platform, the stock exchange shall send a SMS to the investor regarding submission of his/ her application, at the end of day, during the bidding period. For the last day of bidding, the SMS may be sent the next working day.

9.2. The Block process:

a) Post undertaking validation with the depository, the stock exchange shall, on a continuous basis, electronically share the bid details along with investors UPI ID, with the sponsor bank appointed by the issuer.

b) The Sponsor Bank shall initiate a mandate request on the investor i.e. request the investor to authorize blocking of funds equivalent to application amount and subsequent debit of funds in case of allotment.

c) The request raised by the sponsor bank, would be electronically received by the investor as a SMS/ intimation on his/ her mobile number/ mobile app, associated with the UPI ID linked bank account.

d) The investor shall be able to view the amount to be blocked as per his/ her bid in such intimation. The investor shall be able to view an attachment wherein the public issue bid details submitted by investor will be visible. After reviewing the details properly, the investor shall be required to proceed to authorize the mandate. Such mandate raised by the sponsor bank would be a one-time mandate for each application in the public issue.

e) An investor is required to accept the UPI mandate latest by 5 pm on the third working day from the day of bidding on the stock exchange platform except for the last day of the issue period or any other modified closure date of the issue period in which case, he/ she is required to accept the UPI mandate latest by 5 pm the next working day.

f) An investor shall not be allowed to add or modify the bid(s) of the application except for modification of either DP ID or Client ID or PAN but not both. However, the investor can withdraw the bid(s) and reapply.

g) For mismatch bids, on successful validation of PAN and DP ID or Client ID combination during T+1 modification session, such bids will be sent to sponsor bank for further processing by the Exchange on T+1 day till 1pm.

h) The facility of re-initiation/ resending the UPI mandate shall be available only till 5 pm on the day of bidding.

i) Upon successful validation of block request by the investor, as above, the said information would be electronically received by the investors’ bank, where the funds, equivalent to application amount, would get blocked in investors account. Intimation regarding confirmation of such block of funds in investors account would also be received by the investor.

j) The information containing status of block request (e.g. accepted/ decline/ pending) would also be shared with the sponsor bank, which in turn would be shared with the stock exchange. The block request status would also be displayed on the stock exchange platform for information of the

k) The information received from the sponsor bank, would be shared by the stock exchange with the RTA in the form of a file for the purpose of reconciliation.

10. Post issue closure:

10.1. Post closure of the offer, the stock exchange shall share the bid details with RTA. Further, the stock exchange shall also provide the RTA, the final file received from the sponsor bank, containing status of blocked funds or otherwise, along with the bank account details with respect to applications made using UPI ID.

10.2. The allotment of securities shall be done within five working days of the issue closure as detailed in the table above.

10.3. The RTA, based on information of bidding and blocking received from the stock exchange, shall undertake reconciliation of the bid data and block confirmation corresponding to the bids by all investor category applications (with and without the use of UPI) and prepare the basis of allotment.

10.4. Upon approval of the basis of allotment, the RTA shall share the ‘debit’ file with sponsor bank (through stock exchange) and SCSBs, as applicable, for credit of funds in the public issue account and unblocking of excess funds in the investor’s account. The sponsor bank, based on the mandate approved by the investor at the time of blocking of funds, shall raise the debit/ collect request from the investor’s bank account, whereup n funds wil be transferred from investors account to the public issue account and remaining funds, if any, will be unblocked without any manual intervention by investor or their bank.

10.5. Upon confirmation of receipt of funds in the public issue account, the securities would be credited to the investor’s account. The investor will be notified for full/ partial allotment. For partial allotment, the remaining funds would be unblocked. For no allotment, mandate would be revoked and application amount would be unblocked for the investor.

10.6. Thereafter, stock exchanges will issue the listing and trading approval.

11. Role of issuer, registrar, stock exchange, intermediaries and collecting bank:

11.1. Issuer:

a) Issuer shall use an on-line app based/ web based platform provided by stock exchange(s) for receiving applications in public issue of debt securities.

b) For this purpose, the issuer and the stock exchange shall enter into an arrangement which shall contain the inter se rights, duties, responsibilities and obligations of the issuer and stock exchange(s) and provide for a dispute resolution mechanism between the issuer and the stock exchange(s).

c) Issuer shall maintain a single escrow account for collecting application money through all the methods. The sponsor bank appointed by the issuer may be the same bank with whom the public issue account has been

d) Issuer shall appoint one of the SCSBs as sponsor bank to act as conduit between the stock exchanges and NPCI in order to push mandate, collect requests and/ or payment instructions of the investors in the UPI.

11.2. Registrar:

a) The registrar shall have an online or system driven interface with the stock exchange platform to get updated information/ data/ files pertaining to issue.

b) The registrar shall collect aggregate applications details from the stock exchanges platform to decide the eligible applications and process the allotment as per applicable SEBI Regulations.

c) An application without valid application amount shall be treated as invalid application by the Registrar.

d) The registrar shall credit securities to all valid allottees.

e) The registrar shall ensure refund of application amount or excess application amount in the bank account of the applicant as stated in its demat account.

11.3. Stock exchanges:

a) Stock exchanges shall provide a platform for making applications through:

i. Intermediaries; and

ii. App based/ web interface applications from investors with UPI mode for blocking the mode for application value up to Rs. 5 lakh11.

b) The stock exchanges shall be responsible for:

i. accurate, timely and secured transmission of the electronic application file uploaded by all participants on the online platform, to the Registrar; and

ii. disseminating the issue information on the stock exchange website on a periodic basis across all categories.

c)Notwithstanding the responsibility of the intermediaries as laid down in SEBI Regulations, the stock exchange shall be responsible for addressing investor grievances arising from applications submitted online through the App based/ web interface platform of stock exchange or through their Trading Members.

d) Intermediaries:

i. The intermediaries shall be responsible for addressing any investor grievances arising from the applications uploaded by them in respect of quantity, price or any other data entry or other errors made by them.

ii. If the intermediary has not entered any details correctly on the stock exchanges platform and it results on the mismatch with the data obtained by the registrar from the Intermediary shall be responsible for rejection of such applications.

e) Collecting Bank:

The Collecting Bank shall be responsible for addressing any investor grievances arising from non-confirmation of funds to the Registrar despite successful realization of the payment instrument in favour of the issuer’s Escrow Account, or any delay or operational lapse by the Collecting Bank in sending the forms to the Registrar.

Timelines:

12. The SCSBs, stock exchanges, depositories, intermediaries, NPCI and Sponsor Bank shall co-ordinate to ensure completion of listing (through public issue) and commencement of trading of non-convertible securities, municipal debt securities and securitised debt instrument, within T+6 working days from the date of closure of issue as under:

Table 2: Timelines from issue closure till listing

|

Sl. No. |

Details of activities | Due date (working day) |

| 1 | Issue closes | T (Issue closing date) |

| 2 | a) Stock exchange(s) shall allow modification of selected fields (till 01:00 PM) in the bid details already uploaded.

b) Registrar to get the electronic bid details from the stock exchanges by end of the day. c) SCSBs to continue blocking of funds. d) Designated branches of SCSBs may not accept e) Registrar to give bid file received from stock exchanges containing the application number and amount to all the SCSBs who may use this file for validation/ reconciliation at their end. |

T+1 |

| 3 | a) Issuer, merchant banker and registrar to submit relevant documents to the stock exchange(s) except listing application, allotment details and demat credit and refund details for the purpose of listing permission.

b) SCSBs to send confirmation of funds blocked (final certificate) to the registrar by end of the day. c) Registrar shall reconcile the compiled data received from the stock exchange(s) and all SCSBs (hereinafter referred to as the “reconciled data”). d) Registrar to undertake “Technical Rejection” test based on electronic bid details and prepare list of technical rejection cases. |

1+2 |

| 4 | a) Finalization of technical rejection and minutes of the meeting between issuer, lead manager, registrar.

b) 1he allotment in the public issue of securities should be made on the basis of date of upload of each application into the electronic book of the stock exchange. However, on the date of oversubscription and thereafter, the allotments should be made to the applicants on proportionate basis. c) Registrar shall finalise the basis of allotment and submit it to the designated stock exchange for approval. d) Designated stock exchange to approve the basis of allotment. e) Registrar to prepare funds transfer schedule based on approved basis of allotment. f) Registrar and merchant banker to issue funds transfer instructions to SCSBs. |

1+3 |

| 5 | a) SCSBs to credit the funds in public issue account of the issuer and confirm the same.

b) Issuer shall make the allotment. c) Registrar/ issuer to initiate corporate action for credit of debt securities, NCRPS, municipal debt securities and SDIs to successful allottees. d) Issuer and registrar to file allotment details with designated stock exchange(s) and confirm all formalities are complete except demat credit. e) Registrar to send bank-wise data of allottees, amount due on debt securities, municipal debt securities, NCRPS and SDIs allotted, if any, and balance amount to be unblocked to SCSBs. |

1+4 |

| 6 | a) Registrar to receive confirmation of demat credit from depositories.

b) Issuer and registrar to file confirmation of demat credit and issuance of instructions to unblock ASBA funds, as applicable, with stock exchange(s). c) The lead manager(s) shall ensure that the allotment, credit of dematerialised debt securities, municipal debt securities, NCRPS, SDIs and refund or unblocking of application monies, as may be applicable, are done electronically. d) Issuer to make a listing application to stock exchange(s) and stock exchange(s) to give listing and trading permission. e) Stock exchange(s) to issue commencement of trading notice. |

1+5 |

| 7 | Trading commences | T+6 |

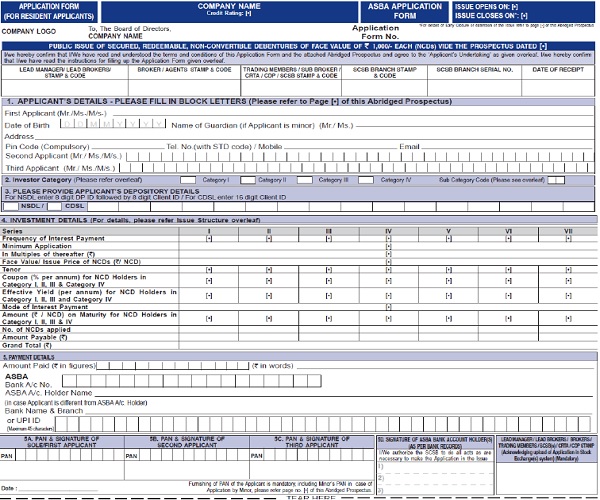

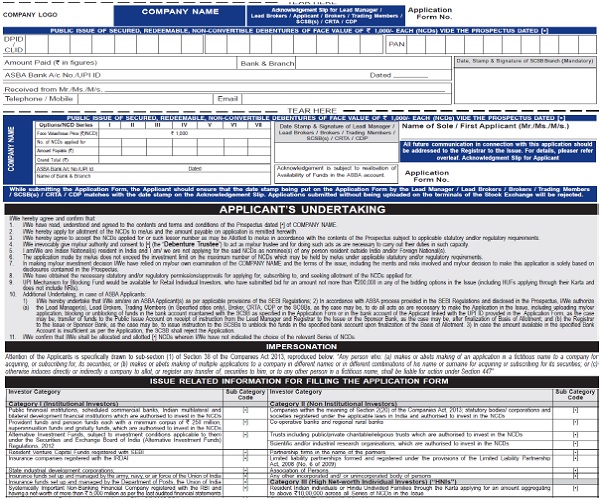

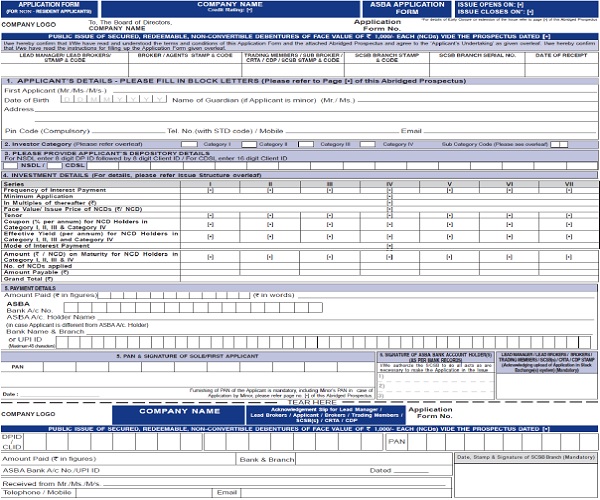

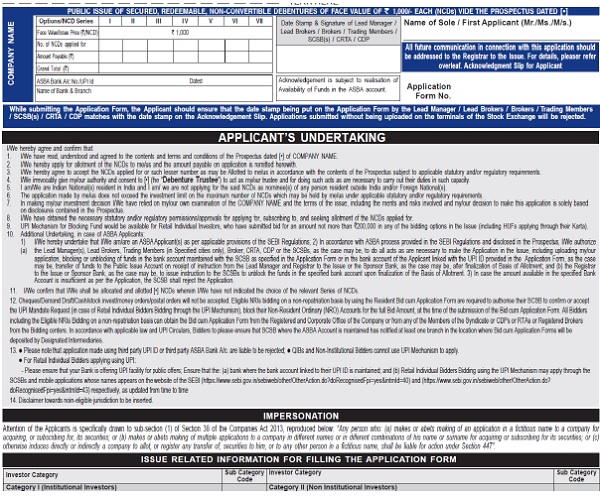

Chapter II – Application form and Abridged Prospectus12

[See Regulation 32 and Part B of Schedule I of the SEBI NCS Regulations, 2021]

Application Form:

1. The following shall be applicable with respect to the application form to be filled up by the investor in case of public issue:

1.1. Application form shall be printed on A4 size sheets. The illustrative format of the application forms to be filled by Resident and NRI, are placed at Annex – IIA and Annex – IIB, respectively. Certain sections in the forms are pre-filled for illustrative purpose.

1.2. No change shall be carried out in spacing, placement or in data fields in the application form except for the following:

a) The number of columns for providing different series details is illustrative and may vary depending upon the terms of the issue;

b) Investor Categories and sub-categories, depending upon the type of issue.

c) Details to be provided under issue structure may vary depending upon the terms of the issue;

2. The payment details in the application-cum-bidding-form including the acknowledgement slip shall include UPI ID with maximum length of 45 characters.

3. The overleaf of the application form shall include the following:

3.1. UPI mechanism for blocking funds would be available for application value upto Rs. 5 lakh13;

3.2. Bidders undertaking and confirmation to include blocking of funds through UPI mode; and

3.3. Instructions with respect to payment/ payment instrument to include instructions for blocking of funds through UPI mode.

Abridged Prospectus:

4. The abridged prospectus shall be in the format as specified in Part B of Schedule I of the SEBI NCS Regulations, 2021. The following shall be ensured with respect to the abridged prospectus annexed to the application form:

4.1. The abridged prospectus shall be printed:

a) on A4 size sheets;

b) in Times New Roman font with font size of not less than 11; and

c) with a line spacing not less than 1.00 lines and normal character spacing with 100% scale without condensing.

4.2. A larger font size may be used, if required, for different heads of information. All major heads shall be in uppercase and bold and in boxes. The first level subheads shall be in bold and in boxes. The other levels of sub-heads shall be bold and underlined.

4.3. The order of the contents in the abridged prospectus shall not be changed. The numbering shall be either continuous or with different types of numbering for different heads/ sub-heads.

4.4. The abridged prospectus shall be so positioned that on the tearing-off of the application form, no part of the nformation given in the abridged prospectus is mutilated.

4.5. Tabular formats and pointers may be used wherever possible for efficient understanding. Instructions for filling up the form, payment instructions and risk factors shall be in pointers and every pointer shall be in a new line.

4.6. Any information which is important for the investor but has not been included in any of the heads, may be included under the section, ‘any other information’.

4.7. Risk factors shall be so provided that they convey the risks associated with the issue in brief.

4.8. A reference may be made to the offer document wherever necessary.

Annex – IIA: Application form for Resident Applicant

–

–

Annex – IIB: Application form for NRI Applicant

–

–

Chapter III – Day count convention, disclosure of cash flows and other disclosures in the offer document14

[See Regulation 14, Clause 2.2.27 of Schedule I and Clause 2.3.22 of Schedule II of SEBI NCS Regulations, 2021]

1. The cash flows emanating from the non-convertible securities according to the day count convention (Actual! Actual) shall be mentioned in the offer document, by way of an illustration.

2. For the purpose of standardization, if the coupon! dividend payment date of the non- convertible securities falls on a Sunday or a holiday, the coupon payment shall be made on the next working day. However, the dates of the future payments would continue to be as per the schedule originally stipulated in the offer document.

3. If the maturity date of the debt securities, falls on a Sunday or a holiday, the redemption proceeds shall be paid on the previous working day.

4. In order to ensure consistency, a uniform methodology shall be followed for calculation of interest! dividend payments in the case of leap year. If a leap year (i.e. February 29) falls during the tenor of a security, then the number of days shall be reckoned as 366 days (Actual! Actual day count convention) for the entire year, irrespective of whether the interest! dividend is payable annually, half yearly, quarterly or monthly.

5. A sample illustration is given below:

Table 1: Illustration depicting computation of days regarding coupon and redemption

| Name of the issuer | XYZ Limited |

| Face Value (per security) | 10,00,000 |

| Tranche Issue date! Date of allotment | Monday, December 14, 2020 |

| Date of redemption | Sunday, December 14, 2025 |

| Tenure and coupon rate | 5 years; 8.95% p.a. |

| Frequency of the interest! dividend payment (with specified dates) | Annually; First interest/ dividend shall become payable on December 14, 2021 and subsequently on 14th December every year, till maturity/redemption. |

| Day Count Convention | Actual/Actual |

–

| Cash Flows | Day and date for coupon/ redemption becoming due | Number of days for denominator | Amount (in Rupees) |

| 1st Coupon | Tuesday, December 14, 2021 | 365 | 89,500 |

| 2nd Coupon | Wednesday, December 14, 2022 | 365 | 89,500 |

| 3rd Coupon | Thursday, December 14, 2023 | 365 | 89,500 |

| 4th Coupon | Monday, December 16, 2024 | 366 | 89,500 |

| 5th Coupon | Friday, December 12, 2025 | 365 | 89,500 |

| Principal | Friday, December 12, 2025 | – | 10,00,000 |

| Total | – | 14,47,500 | |

In the above illustration, the year 2024 being a leap year has 29 days in February 2024. This implies that 366 days would be reckoned as the denominator (Actual/ Actual), for payment of interest/ dividend. Further, December 14, 2024 falls on a Saturday which being the second Saturday will be a banking holiday. Hence, the 4th coupon payment shall be made on the next working day i.e. December 16, 2024. However, the calculation for payment of interest shall be only till December 13, 2024, which would have been the case if December 14, 2024 was not a holiday. This shall not affect the subsequent coupon payment and it shall continue to fall due on December 14, 2025, i.e. original coupon payment schedule. However, since December 14, 2025 falls on a Sunday, the redemption (i.e. principal and the 5th/ last coupon payment) shall be made on the previous working day i.e. on December 12, 2025.

6. Other disclosures: The issuer shall make the following additional disclosures in the offer document in case of public issue:

6.1. Provisions relating to fictitious applications;

6.2. Declaration by board of directors that the underwriters, if any, have sufficient resources to discharge their respective obligations;

6.3. Reservation in the issue, if any;

6.4. Utilization details regarding the previous issues of the issuer as well as its group companies, for the past 3 years;

6.5. Benefit/ interest accruing to promoters/ directors out of the object of the issue; and

6.6. Details regarding material contracts other than the contracts entered in the ordinary course of business and the material contracts entered within the previous two years.

Chapter IV – Additional Disclosures by Non-Banking Finance Company or Housing Finance Company or Public Financial Institution15

[See Regulation 25(4), Clause 2.2.9 of Schedule I and Clause 2.3.15 of Schedule II of SEBI NCS Regulations, 2021]

A. Disclosures by NBFC or HFC or PFI, in a public issue:

1. In case the issuer is a NBFC or HFC or PFI and the objects of the public issue entail loan to any entity which is a ‘Group Company’, then disclosures shall be made in the following format:

Table 1: Disclosure by NBFC or HFC or PFI with respect to “Group Company”

| Sl. No. | Name of borrower | Amount of advances/ exposures to such borrower (group company) (Rs. crore) (A) | Percentage of exposure = (A)/ Total AUM |

B. Disclosures by NBFC or HFC, in a public issue or private placement:

2. Details with regard to the lending done by the issuer out of the issue proceeds of debt securities in last three years, including details regarding the following:

2.1. Lending policy: Should contain overview of origination, risk management, monitoring and collections;

2.2. Classification of loans/ advances given to associates, entities/ person relating to board, senior management, promoters, others, etc.;

2.3. Classification of loans/ advances given, according to type of loans, denomination of loan outstanding by loan to value, sectors, denomination of loans outstanding by ticket size, geographical classification of borrowers, maturity profile etc.;

2.4. Aggregated exposure to the top 20 borrowers with respect to the concentration of advances, exposures to be disclosed in the manner as prescribed by RBI in its stipulations on Corporate Governance for NBFCs or HFCs, from time to time;

2.5. Details of loans, overdue and classified as non-performing in accordance with RBI stipulations;

3. In order to allow investors to better assess the debt securities issued by the NBFC/ HFC, the following disclosures shall also be made by such issuers in their offer documents:

3.1 . A portfolio summary with regard to industries/ sectors to which borrowings have been made;

3.2. NPA exposures of the issuer for the last three financial years (both gross and net exposures) and provisioning made for the same as per the last audited financial statements of the issuer;

3.3. Quantum and percentage of secured vis-à-vis unsecured borrowings made; and

3.4. Any change in promoters’ holdings during the last financial year beyond the threshold, as prescribed by RBI.

C. NBFCs shall provide disclosures on the basis of the following draft template:

4. Classification of loans/ advances given according to:

4.1. Type of loans:

Table 2: Details of types of loans

| Sl. No. | Type of loans | Rs. crore |

| 1 | Secured | |

| 2 | Unsecured | |

| Total assets under management (AUM)*^ |

*Information required at borrower level (and not by loan account as customer may have multiple loan accounts); ^Issuer is also required to disclose off balance sheet items;

4.2. Denomination of loans outstanding by loan-to-value:

Table 3: Details of LTV

| Sl. No. | LTV (at the time of origination) | Percentage of AUM |

| 1 | Upto 40% | |

| 2 | 40-50% | |

| 3 | 50-60% | |

| 4 | 60-70% | |

| 5 | 70-80% | |

| 6 | 80-90% | |

| 7 | >90% | |

| Total |

4.3. Sectoral exposure:

Table 4: Details of sectoral exposure

|

Sl. No. |

Segment-wise break-up of AUM | Percentage of AUM | |

| 1 | Retail | ||

| A | Mortgages (home loans and loans against property) | ||

| B | Gold loans | ||

| C | Vehicle finance | ||

| D | MFI | ||

| E | MSME | ||

| F | Capital market funding (loans against shares, margin funding) | ||

| G | Others | ||

| 2 | Wholesale | ||

| A | Infrastructure | ||

| B | Real estate (including builder loans) | ||

| C | Promoter funding | ||

| D | Any other sector (as applicable) | ||

| E | Others | ||

| Total | |||

4.4. Denomination of loans outstanding by ticket size*:

Table 5: Details of outstanding loans category wise

| Sl. No. | Ticket size (at the time of origination) | Percentage of AUM |

| 1 | Upto Rs. 2 lakh | |

| 2 | Rs. 2-5 lakh | |

| 3 | Rs. 5 – 10 lakh | |

| 4 | Rs. 10 – 25 lakh | |

| 5 | Rs. 25 – 50 lakh | |

| 6 | Rs. 50 lakh – 1 crore | |

| 7 | Rs. 1 – 5 crore | |

| 8 | Rs. 5 – 25 crore | |

| 9 | Rs. 25 – 100 crore | |

| 10 | >Rs. 100 crore | |

| Total |

* Information required at the borrower level (and not by loan account as a customer may have multiple loan accounts);

4.5. Geographical classification of borrowers:

Table 6: Top 5 states borrower wise

| Sl. No. | Top 5 states | Percentage of AUM |

| 1 | ||

| 2 | ||

| 3 | ||

| 4 | ||

| 5 | ||

| Total |

4.6. Details of loans overdue and classified as non-performing in accordance with RBI’s stipulations:

4.7. Segment-wise gross NPA:

Table 9: Segment wise gross NPA

|

Sl. No. |

Segment-wise gross NPA | Gross NPA (%) | |

| 1 | Retail | ||

| A | Mortgages (home loans and loans against property) | ||

| B | Gold loans | ||

| C | Vehicle finance | ||

| D | MFI | ||

| E | MSME | ||

| F | Capital market funding (loans against shares, margin funding) | ||

| G | Others | ||

| 2 | Wholesale | ||

| A | Infrastructure | ||

| B | Real estate (including builder loans) | ||

| C | Promoter funding | ||

| D | Any other sector (as applicable) | ||

| E | Others | ||

| Total | |||

4.8. Residual maturity profile of assets and liabilities (in line with the RBI format):

Table 10: Residual maturity profile of assets and liabilities

| Category | Up to 30/31 days | >1 month

– 2 |

>2 months – 3 months |

>3 months – 6 months |

>6 months – 1 year | >1

years – 3 years |

>3

years – 5 years |

>5 years | Total |

| Deposit | |||||||||

| Advances | |||||||||

| Investment s | |||||||||

| Borrowing s | |||||||||

| FCA* | |||||||||

| FCL* |

*FCA – Foreign Currency Assets; FCL – Foreign Currency Liabilities;

Chapter V – Denomination of issuance and trading of Non-convertible Securities

[See Regulation 50(4) and Clause 2.2.e of Schedule II SEBI NCS Regulations, 2021]

1. Issuance of non-convertible securities:

1.1 . The face value of each debt security or non-convertible redeemable preference share issued on private placement basis shall be Rs. One lakh16.

Provided that with respect to a shelf placement memorandum which is valid as on January 1, 2023, the issuer thereof shall have the option while raising funds through tranche placement memorandum, to keep the face value at Rs. Ten lakhs or Rs. One Lakh. Necessary addendum shall be issued by such issuer to the shelf placement memorandum.

1.2. The face value of each security mentioned under Chapter V of SEBI NCS Regulations, 2021 and Chapter XIII of this Master circular shall be Rs. One crore.

2. Trading of non-convertible securities:

2.1. The face value of a listed debt security or non-convertible redeemable preference share issued on private placement basis traded on a stock exchange or OTC basis shall be Rs. One lakh17.

2.2. The face value of a listed security mentioned under Chapter V of SEBI NCS Regulations, 2021 and Chapter 13 of this operational circular traded on a stock exchange or OTC basis shall be Rs. One crore.

2.3. The trading lot shall always be equal to face value.

3. This chapter is not applicable for debt securities and non-convertible redeemable preference shares issued on a public issue basis.

Chapter VI – Electronic Book Provider platform18

[See Regulation 12 of SEBI NCS Regulations, 2021 and Regulation 16 of SEBI ILDM Regulations, 2015]

Primary issuances through EBP platform shall comply with the stipulations provided in this chapter.

The following are the eligible participants (i.e. bidders) on the EBP Platform:

1.1. QIBs as defined under Regulation 2 (ss) of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 (hereinafter referred to SEBI ICDR Regulations, 2018).

1.2. Any non-QIB, who/ which has been authorized by the issuer, to participate in a particular issue on the EBP Platform.

2. The following issues of securities shall be made through the EBP platform:

2.1. A private placement of debt securities and NCRPS as per the provisions of SEBI NCS Regulations, 2021, if it is:

i. a single issue, inclusive of green shoe option, if any, of Rs. 50 crore or more;

ii. a shelf issue, consisting of multiple tranches, which cumulatively amounts to Rs. 50 crore or more, in a financial year; and

iii. a subsequent issue, where aggregate of all previous issues by an issuer in a financial year equals or exceeds Rs. 50 crore.

2.2. Issues of debt securities and NCRPS on private placement basis, irrespective of issue size, by issuers who are in existence for less than three years, in accordance with Clause 2.3.8 c. of Schedule II to the SEBI NCS Regulations, 2021.

2.3. The issuance of PDIs, PNCPS, PCPS, RNCPS, and instruments of similar nature which are essentially non-equity regulatory instruments, forming part of a bank’s or NBFC’s capitalissued as per RBI stipulat ons and listed under Chapter V of the SEBI NCS Regulations, 2021, irrespective of the issue size.

3. An issuer, if desirous, may choose to access EBP platform for private placement of municipal debt securities or CPs or CDs also.

4. Issuers of debt securities and NCRPS on private placement basis of issue size less than Rs.50 crore may also choose to access the EBP platform for such issuances.

5. The obligations of issuers are as under:

5.1. The issuer shall ensure compliance with all requisite laws, rules, regulations, etc. with respect to private placement of securities including ensuring compliance with Section 42 of the Companies Act, 2013.

Provided that, the issuer, shall include the number of non-QIB eligible participants, on whose behalf arranger(s) is making bids in a particular issue, for the purposes of compliance with the provisions of Section 42 of the Companies Act, 2013 and other relevant statutes.

5.2. The Issuer shall provide the Placement Memorandum and term sheet (i.e. summary of important terms and conditions related to an issue) to the EBP at least two working days prior to the issue opening date.

However, the issuer issuing the securities for the first time through EBP platform shall provide the above information at least five working days prior to the issue to the opening date.

5.3. The Placement Memorandum and the term sheet, inter-alia, discloses the following:

5.3.1. Details of size of the issue and green shoe portion, if any.

Provided that the green shoe portion shall not exceed five times the base issue size.

5.3.2. Interest rate parameter – Zero coupon, fixed coupon or floating coupon.

5.3.3. Bid opening and closing date.

5.3.4. Minimum Bid Lot.

5.3.5. Manner of bidding in the issue i.e. open bidding or closed bidding.

5.3.6. Manner of allotment in the issue i.e. uniform yield allotment or multiple yield allotment.

5.3.7. Manner of settlement in the issue i.e. through clearing corporation or through escrow bank account of issuer.

5.3.8. Settlement cycle i.e. T+1 or T+2 day.

5.4. The issuer may choose to disclose estimated cut-off yield to the EBP, however the same has to be disclosed at least one hour prior to opening of the bidding for the issue.

5.5. Subsequent to closure of the issue, the issuer shall ensure following details of the issue are provided on the EBP platform:

Table 1: Details of allotment in private placement

| Details of Investors to whom allotment has been made | |||

| Name | QIB/ Non-QIB |

Category i.e. Scheduled Commercial Banks, MF, Insurance Company, Pension Fund, Provident Fund, FPI, PFI, Corporate, Others |

Amount invested in Rs. crore |

6. Participants:

6.1. Participants, prior to entering into the bidding process shall be required to enroll with EBP. Such enrollment of a participant on an EBP will be onetime exercise and shall be valid till the time such enrolment is annulled or rescinded.

6.2. The KYC verification and enrolment of the eligible participants on the EBP platform shall be done in the following manner:

6.2.1. KYC verification shall be undertaken by obtaining/ utilizing existing KYCs of clients from KYC Registration Agencies (KRAs) registered with SEBI or on the basis of the guidelines as prescribed by SEBI from time to time.

6.2.2. For QIB investors bidding directly or through arranger(s), KYCs and enrolment shall be done by the EBP.

6.2.3. For non-QIB investors bidding directly, KYCs shall be done by the issuer and enrolment shall be done by the EBP.

6.2.4. For non-QIB investors, which are bidding through arranger(s), KYC and enrolment on EBP shall be ensured by arranger(s).

6.3. EBPs shall ensure that all eligible participants have access to the Placement Memorandum (PM), term sheet and other issue specific information available with them.

6.4. Each eligible participant shall provide confirmation to the EBP that it is not using any software, algorithm, Bots or other automation tools, which would give unfair access for placing bids on the EBP platform.

6.5. Each EBP shall ensure that it does not provide any preferential access to any bidder on a selective basis.

6.6. An eligible participant cannot bid for an amount more than Rs.100 crore or 5% of the base issue size, whichever is lower, through arranger(s) on the EBP platform.

Provided that Foreign Portfolio Investors may bid through their custodians.

6.7. An arranger can bid, on behalf of multiple participants, subject to the limits for each participant, as mentioned above.

6.8. For bids made by an arranger for any particular issue, such arranger shall disclose the following to the EBP at the time of bidding:

6.8.1. Specify that whether the bid is:

a. a proprietary bid; or

b. a client bid i.e. entered on behalf of an eligible participant; or

c. a consolidated bid i.e. an aggregate bid consisting of proprietary bid and Client bids.

6.8.2. For consolidated bid, arranger shall disclose breakup between proprietary bid and client bid(s). Further, for client bids, the following shall be disclosed:

a. Names of such eligible participants;

b. Category (i.e. QIB or non-QIB); and

c. Quantum of bid of each eligible participant.

7. Bidding, allotment and settlement process:

7.1. Bidding timings and period:

7.1.1. In order to ensure operational uniformity across various EBP platforms, the bidding on the EBP platform shall take place between 9 a.m. to 5 p.m. only, on the working days of the recognized stock exchanges.

7.1.2. The bidding window shall be open for the period as specified by the issuer in the bidding announcement; however, the same shall be open for at least one hour.

7.1.3. An issuer can provide details of the eligible participant(s) for a particular issue, to the EBP, not later than one hour before the bidding start time.

7.2. Bidding announcement:

7.2.1. Issuer shall make the bidding announcement on EBP at least one working day before initiating the bidding process.

7.2.2. Bidding announcement shall be accompanied with details of bid opening and closing time, and any other details as required by the EBP from time to time.

7.2.3. Any change in bidding time and/ or date by the issuer shall be intimated to the EBP, ensuring that such announcement is made within the operating hours of the EBP, at least a day before the bidding date.

Provided that such changes in bidding date or time shall be allowed for a maximum of two times.

7.3. The bidding process on EBP platform shall be on an anonymous order driven system.

7.4. Bid shall be made by way of entering bid in:

7.4.1. Price; or

7.4.2. Coupon (in %), up to four decimal places; or 7.4.3. Spread in basis points (bps).

Further, the bid amount shall be specified in Rupees (INR).

7.5. Bidding process shall be based on the following:

7.5.1. Coupon specified by issuer: The face value and coupon remaining constant, bids/ quotes shall be placed by the bidders in terms of price.

7.5.2. Coupon/ spread discovered during bidding: The face value remaining constant, bids/ quotes shall be placed by the bidders in terms of coupon/ spread.

7.6. Investors may place multiple bids in an issue.

7.7. Modification or cancellation of the bids shall be allowed i.e. bidder can cancel or modify the bids made in an issue, subject to the following:

7.7.1. such cancellation/ modification in the bids can be made only during the bidding period;

7.7.2. no cancellation of bids shall be permitted in the last 10 minutes of the bidding period; and

7.7.3. in the last 10 minutes of the bidding period, only revision allowed would be for:

a. downward revision of coupon/ spread or upward modification of price; and/ or

b. upward revision in terms of the bid size.

7.8. The bd placed in the system shalhave an audit trail which includes bidders identification details, time stamp and unique order number. Further against such bids, the EBP shall provide an acknowledgement.

7.9. All the bids made in a particular issue shall be disclosed on the EBP platform, in the following format:

Table 2: Details of cumulative demand received on EBP platform

| Coupon/ price/ spread |

Amount demand at that particular coupon/ price/ spread (in Rs. crore) | Cumulative amount demand (in Rs. crore) |

7.10. For issues with open bidding, the aforesaid information shall be disseminated on a real time basis; however, for issues with closed bidding, the information shall be disseminated after closure of bidding.

7.11. Allotment and settlement amount for the bidders shall be based on the following:

7.11.1. Coupon specified by issuer: All bids shall be arranged as per ‘price time priority

a. In case of ‘uniform yield allotment’, allotment and settlement value shall be based on the cut-off price determined in the bidding process.

b. In case of ‘multiple yield allotment’, allotment and settlement value shall be based on the price quoted by each bidder/ allottee in the bidding process.

7.11.2. Coupon discovered during bidding: All bids shall be arranged as per ‘yield time priority’.

a. In case of ‘uniform yield allotment’, allotment and settlement value shall be based on the face value.

b. In case of ‘multiple yield allotment’, allotment and settlement value shall be based on the price adjusted as per the coupon/ spread quoted by each bidder/ allottee in the bidding process.

7.11.3. If two or more bids have the same coupon/ price/ spread and time, then allotment shall be done on ‘pro-rata’ basis.

8. Anchor portion within the base issue size:

8.1. Issuer shall have an option to avail an anchor portion’ within the base issue size, subject to the below mentioned conditions:

8.1.1. Issuer shall have the discretion to select the anchor investor(s) for the anchor portion.

8.1.2. The quantum of allocation(s) to the anchor investor(s) shall be at the discretion of the issuer, subject to total allocation to the anchor(s) not exceeding 30% of the base issue size.

8.1.3. There shall be no bidding for anchor portion on the EBP platform.

8.1.4. If the issuer opts for anchor portion, the same shall be suitably disclosed in the placement memorandum and the term sheet, along with the relevant quantum (maximum 30%).

8.1.5. Issuer shall disclose details of the anchor investor(s) and the corresponding quantum allocated, to the EBP, along with the Placement Memorandum and the term sheet.

8.1.6. The settlement amount for the anchor investor(s) shall be determined on the basis of the following:

a. Coupon specified by the issuer:

Uniform yield allotment: The ‘cut-off’ price determined in the bidd ng process (in case of issues with anchor portion, it will imply total issue size less the anchor portion).

Multiple yield allotment: Face value of the security.

Provided that, in case of re-issuance, the ‘cutloff’ price determined in the bidding process shall be applicable on the anchor investor(s).

b. Coupon/ spread determined in the bidding process: Uniform yield or multiple yield allotment: Face value of the security

8.2. The remaining portion of the issue (i.e. the non-anchor portion within the base issue size and the green shoe portion), shall be open for bidding by the eligible participants at the chosen time slot on the EBP platform. The anchor investor(s) may also participate in the said portion if identified as eligible participant(s) by the issuer.9. Pay-in obligations:

9.1 . Pay-in towards the allotment of securities shall be done from the account of the bidder, to whom allocation is to be made. For bids made by the arranger on behalf of eligible participant(s), pay-in towards allotment of securities shall be made from the account of such eligible participants.

9.2. Pay-in of funds through escrow bank account of issuer: The pay-in of funds towards an issue on EBP shall be permitted either through clearing corporations of stock exchanges or through the escrow bank account of an issuer. An issuer, in its PM, shall disclose the manner of pay-in of funds so chosen and details thereof. The process of pay-in of funds by investors and pay-out to issuer can be done on either T+1 or T+2 day, where T day is the issue day, and the same shall be disclosed by the issuer in the PM.

9.3. In case of non-fulfillment of pay-in obligations by allottees and anchor investor(s), such allottees and anchor investor(s) shall be debarred from accessing the bidding platform across all EBPs for a period of thirty days from the date of such default.

9.4. In case of three instances of non-fulfillment of pay-in obligations, across all EBPs, by client(s) for whom an arranger has bid, then such arranger shall be debarred from accessing the bidding platform on any EBP, for a period of seven days from the date of the such third or subsequent default.

9.5. Pay in shall be done through the clearing corporations of stock exchanges, as per their operating guidelines, or through an escrow bank account of the issuer, as mentioned below.

Provided that where the issuer has selected the escrow bank account as the mechanism for pay-in, EBP, pursuant to successful closure of issue, shall share the allocation details with the Registrar to an Issue, associated with the issue.

9.6. Process flow of settlement, where funds pay-in is to be made to escrow bank account of issuer:

9.6.1. Successful bidders, in an issue, will make pay-in of funds towards the allocation made to them, in the escrow bank account within the timelines, as provided by the issuer in the PM/ IM. The funds pay-in by the successful bidders will be made only from the bank account(s), which have been provided/ updated in the EBP system. Further, pay-in received from any other bank account will lead to cancellation of bid and consequent debarment of the investor from accessing EBP platform for 30 days.

9.6.2. Escrow bank, pursuant to receipt of funds will provide a confirmation to the RTA, associated with the issue, about receipt of funds along with details including name of bank account holder, bank account number and the quantum of funds received.

9.6.3. RTA, will then reconcile the information received from escrow bank with the details as provided by EBP and after reconciliation RTA shall intimate to the issuer about receipt of funds. Subsequently, issuer will initiate the process of corporate action through the RTA to Depository.

9.6.4. RTA, after passing on the instructions for corporate action to the depositories, will issue instruction to the escrow bank to release money to the issuers bank account.

10. Withdrawal of offer by an issuer:

10.1. An issuer, at its discretion, may withdraw from the issue process at any time; however, subsequent to such withdrawal, the issuer shall not be allowed to access any of the EBP platforms for a period of seven days from the date of such withdrawal. A withdrawal from the issue process shall imply withdrawal of the total issue including anchor portion.

10.2. If an issuer withdraws from the issue because of any of the reasons as outlined below, the restrictions mentioned in the above paragraph shall not be applicable:

10.2.1. issuer is unable to receive the bids up to the base issue size; or

10.2.2. bidder has defaulted on payment towards the allotment, within stipulated timeframe, due to which the issuer is unable to fulfill the base issue size; or

10.2.3. cut-off yield (i.e. the highest yield at which a bid is accepted) in the issue is higher than the estimated cut-off yield (i.e. the yield estimated by the issuer, prior to opening of issue) disclosed to the EBP, where the base issue size is fully subscribed.

10.3. Disclosure of estimated cut-off yield on the EBP platform to the eligible participants, pursuant to closure of issue, shall be at the discretion of the issuer.

10.4. In case an issuer withdraws issues on the EBP platform because of the cut-off yield being higher than the estimated cut-off yield, the EBP shall mandatorily disclose the estimated cut-off yield to the eligible participants.

11. Responsibilities of various entities involved in the process:

11.1. Issuer shall:

11.1.1. open an escrow bank account/ have an escrow bank account jointly with a RTA, where the role of the RTA in operating such bank account shall be limited to the responsibilities as provided under this circular;

11.1.2. provide the details of escrow bank account in which pay-in of funds has to be made and the timelines by which such pay-in shall be done by the successful bidders; and

11.1.3. effect corporate action for credit of securities to the successful bidders, after receiving confirmation from the RTA about receipt of funds.

11.2. RTA shall:

11.2.1. undertake reconciliation between information received from the escrow Bank and EBP. Further, after reconciliation, shall intimate the issuer about the receipt of funds and shortfall, if any, and the reasons thereof;

11.2.2. issue instructions to the escrow bank account for the release of funds, after passing on the instructions for corporate action to the depositories; and

11.2.3. intimate to the EBP, upon closure of the issue, the status of the issue i.e. successful or withdrawn, details of defaulting investors etc.

12. Obligations and duties of EBP:

12.1. An EBP shall:

12.1.1. provide an on-line platform for placing bids;

12.1.2. have necessary infrastructure like adequate office space, equipment, risk management capabilities, manpower and other information technology infrastructure to effectively discharge the activities of an EBP;

12.1.3. ensure that the PM, term sheet and other issue related information is available to the eligible participants on its platform immediately on receipt of the same from the issuer;

12.1.4. have adequate backup, disaster management and recovery systems; and

12.1.5. ensure safety, secrecy, integrity and retrievability of data.

12.2. EBPs shall ensure that all details regarding the issuance is updated on its website.

12.3. EBPs shall together ensure that the operational procedure is standardized across all EBP platforms and the details of such operational procedure are disclosed on their websites.

12.4. Where an issuer has disclosed estimated cut-off yield to the EBP, the EBP shall ensure its electronic audit trail and secrecy. However, in case issuers withdraw issues on the EBP because of the cut off yield being higher than the estimated cut off yield, the EBP shall mandatorily disclose the estimated cut off yield in its platform.

12.5. EBPs shall ensure coordination amongst themselves and also with depositories so as to ensure that the cooling off period for issuers and debarment period for investors is adhered to.

12.6. EBPs shall ensure that bidding is done in the manner as specified.

12.7. The EBP shall be responsible for accurate, timely and secured bidding process of the electronic bid by the bidders.

12.8. The EBP shall provide a facility to the eligible participants to define the limits/ range, within which quotes may be placed, from its user interface, to avoid ‘fat finger’ errors.

12.9. The EBP shall be responsible for addressing investor grievances arising from bidding process.

13. CISA Audit of EBP Platform:

The EBP platform so provided by the EBP shall be subject to audit by a CISA at least once a year.

14. Electronic Book Providers are directed to:

14.1. comply with the conditions laid down hereunder;

14.2. put in place necessary systems and infrastructure for implementation and make consequential changes, if any, to their bidding portal and respective exchange bye-laws; and communicate and create awareness about these provisions amongst issuers, arrangers and investors.

Chapter VII – Standardization of timelines for listing of securities issued on a private placement basis19

[See Regulations 6, 44 and 46 of SEB! NCS Regulations, 2021, Regulations 24 and 38D of the SEB! SD! Regulations, 2008 and Regulations 4A, 4E and Clause 7(m) of Schedule ! of SEB! !LDM Regulations, 2015]

1. This chapter shall be applicable for non-convertible securities, securitised debt instruments, security receipts and municipal debt securities (hereinafter referred to as “securities” in this chapter) issued on a private placement basis.

In-principle approval:

2. An issuer desirous of issuing and listing non-convertible securities or municipal debt securities, shall make an application for in-principle approval to the stock Exchange(s), in terms of Regulation 6 of the NCS Regulations or Regulation 4A of the ILDM Regulations, respectively, complete in all respects, including the submissions and disclosures, as may be specified by the stock exchange(s).

Timelines for issuance and listing of securities on private placement basis:

3. The timelines for each of the steps involved, from submission of the application for in-principle approval to the listing of the security on the stock exchange(s), are given below:

Table 1: Timelines for issuance and listing of securities on private placement basis

| Category | Timeline (working day) | Nature of activity | |

| EBP | Non-EBP | ||

| In-principle approval

|

Prior to T-2/ T-5 (EBP);

Prior to T (Non-EBP) |

Issuer shall ensure receipt of in-principle approval from the stock exchange(s) where it wishes to list its proposed debt issuance/ securities, prior to the date of providing the Placement Memorandum and term sheet to the EBP(s), in terms of paragraph 5.2 of Chapter VI of this Master Circular. | Issuer shall ensure receipt of in-principle approval from the stock exchange(s) where it wishes to list its proposed debt issuance/ securities, prior to issue open date. |

| Bidding announcement | On or before T-1 | Issuer shall provide the bidding start time and close time to EBP, on or before T-1. | Issue period (open and close date) is to be disclosed by the Issuer in the Placement memorandum. |

| Day of bidding/ Issue period | T |

|

|

| ISIN allocation/ assignment/ confirmation by Depository | On or before T+1 |

|

|

| Settlement | On or before T+1/ T+2 (as per settlement cycle chosen by the Issuer) (EBP);On or before T+2 (Non-EBP); |

|

|

*For privately placed issues through EBP, T implies bidding date; for privately placed issues outside EBP, T implies issue open date;

Note: In the above table, for privately placed issue outside EBP, for illustration, it is assumed that issue is open for one day only. In case issue is kept open for more than one day, the timelines specified above for activities post the bidding date shall be computed from issue closure date.

4. Stock exchange(s) are advised to inform the listing approval details to the Depositories whenever listing permission is given to securities issued on private placement basis.

5. Depositories shall activate the ISINs of securities issued on private placement basis only after the stock exchange(s) have accorded approval for listing of such

Further, in order to facilitate re-issuances of new debt securities in an existing IS IN, Depositories are advised to allot such new securities under a new temporary ISIN which shall be kept frozen. Upon receipt of listing approval from stock exchange(s) for such new securities, the securities credited in the new temporary ISIN shall be debited and the same shall be credited in the pre-existing ISIN of the existing securities, before they become available for trading.

6. In case of delay in listing of securities issued on privately placement basis beyond the timelines specified above, the issuer shall pay penal interest of 1% p.a. over the coupon/ dividend rate for the period of delay to the investor (i.e. from the date of allotment to the date of listing).

7. The stock exchanges are advised to issue necessary directions regarding:

a. the submissions/ disclosures required to be made by an issuer at the time of making an in-principle approval application and listing application; and

b. the timelines within which such application for in-principle approval and listing, is to be made by an Issuer.

8. The stock exchanges may permit deviation from the above, if found necessary, subject to the outer limit of T+3 days for conclusion of listing process, after recording the reasons in writing.

[See Regulation 17 of SEBI NCS Regulations, 2021]

1. In respect of private placement of debt securities, the following shall be complied with regard to ISINs, utilised to issue debt securities from April 1, 2023:

1.1 A maximum number of fourteen ISINs maturing in any financial year shall be allowed for an issuer of debt securities. In addition, a further six ISINs shall also be available for the issuance of the capital gains tax debt securities by the authorized issuers under section 54EC of the Income Tax Act, 1961 on private placement basis.

1.2 Out of the fourteen ISINs maturing in a financial year, the bifurcation of ISINs shall be as under:

a. A maximum of nine ISINs maturing per financial year shall be allowed for plain vanilla debt securities. Within this limit of nine ISINs, the issuer can issue both secured and unsecured debt securities.

Provided where the total outstanding amount across the nine ISINs, maturing in a given financial year, reaches Rs. 15,000 crore, then three additional ISINs would be permitted to mature in the same financial year. The same should be intimated by the issuer to the stock exchanges and depositories.

b. A maximum of five ISINs maturing per financial year shall be allowed for structured debt securities and market linked debt securities.

1.3 Where an issuer issues only structured/ market linked debt securities, the maximum number of ISINs allowed to mature in a financial year shall be nine.

1.4 Further, with respect to the debt securities issued on or after April 01, 2023, all the ISINs corresponding to these issues (including ISINs issued prior to April 01, 2023), maturing in any financial year, shall adhere to the limits as specified above.

1.5 The above threshold may be reviewed periodically to further reduce fragmentation in the corporate bond market.

2. In respect of private placement of debt securities, the following shall be complied with regard to ISINs,, utilised for issuance of debt securities up to March 31, 2023 and maturing in later years:

2.1 A maximum number of seventeen ISINs maturing in any financial year shall be allowed for an issuer of debt securities. In addition, a further twelve ISINs shall also be available for the issuance of the capital gains tax debt securities by the authorized issuers under section 54EC of the Income Tax Act, 1961 on private placement basis.

2.2 Out of the seventeen ISINs maturing in a financial year, the bifurcation of ISINs shall be as under:

a. A maximum of twelve ISINs maturing per financial year shall be allowed for plain vanilla debt securities. Within this limit of twelve ISINs, the issuer can issue both secured and unsecured debt securities

b. A maximum of five ISINs maturing per financial year shall be allowed for structured debt securities and market linked debt securities.

2.3 Where an issuer issues only structured/ market linked debt securities, the maximum number of ISINs allowed to mature in a financial year shall be twelve.

3. Issuers of certain debt securities like subordinate debt, Tier II bonds issued by Standalone Primary Dealers, bonds issued by banks to raise resources for lending to long term infrastructure sub-sectors and affordable housing were provided dispensations from ISIN restrictions till June 30, 2020.

4. In case of conversion of partly paid debt securities to fully paid debt securities, such conversion shall not be counted as an additional IS IN.

5. In case of debt securities, where call and/ or put option is exercised, the issuer, if it so desires, may issue additional debt securities for the balance period viz. remaining period of maturity of earlier debt securities. For example, if an issuer has issued debt securities in the month of August 2017 having maturity period of three years and callable after one year, then in such a scenario if the call option is exercised in the month of August 2018, then for the balance two years’ period viz. (September 2018 – August 2020) the issuer may issue additional debt securities maturing in August 2020, under the same ISIN.

Provided that the aforesaid additional issue shall be subject to the condition that the aggregate count of outstanding ISINs maturing in the financial year in which the original issue of debt securities (bearing call and/ or put option) is due for expiring, shall not exceed the prescribed limit of ISINs.

6. In case of structured/ market linked debt securities which have embedded options call and/ or put option, the maturity of ISINs shall be reckoned on basis of original maturity date of debt securities.

For e.g. If a structured debt security with a maturity period of five years has an option to be called after three years and every year thereafter till redemption, then such security shall be grouped as per its maturity period i.e. five years and not based upon the option to call.

7. Mechanism for honoring debt obligations arising out of capping of ISINs:

7.1. An issuer may honour its debt obligations/ liabilities, arising out of such ISIN restrictions, in the manner as deemed feasible to them i.e. the issuer can make staggered repayments or bullet maturity repayments or in any other manner deemed so.

7.2. An issuer may offer different type of payment options to different category of investors subject to such disclosures being made in the placement memorandum in order to manage their asset liability mismatch.

For e.g. an insurance company may be offered staggered redemption, however mutual fund may be offered bullet payment.

7.3. Also, in case of any modification in terms or structure of the issue viz. change in terms of payment, change in interest pay-out frequency etc. the issuer may make such modification by following procedure as has been laid out in Regulation 59 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (hereinafter referred to as SEBI LODR Regulations, 2015).

7.4. Record Date: There may be cases where multiple record dates would arise on account of staggered payment or other cases viz. frequency of payment etc. In such a case, when announcing multiple record dates, the issuer has to disclose clearly to the stock exchanges the basis of payment to the investors viz. pro-rata, first come first serve basis etc.

8. Amendment to the AoA/ charter/ constitution of the issuer: In order to comply with the provisions of regulation 49 (a) of the SEBI NCS Regulations, 2021 the issuer shall make an enabling provision in its AoA/ charter/ constitution to carry out consolidation and re-issuance of debt securities.

9. Reporting and Monitoring:

1. Issuers:

a) The issuer shall within fifteen days from the end of every half year (i.e. April 15 and October 15), submit a statement, to the stock exchange, where its debt securities are listed, as well as to the depository containing data in the format as prescribed below:

Table 1: Format for half-yearly reporting by the issuer

b) In case there is any modification in terms or structure of the issue viz. change in terms of payment, change in interest pay-out frequency as specified above, the issuer shall, forthwith, inform the same to the Stock Exchange21 and depository.

9.2. Obligations of stock exchanges and depositories:

a) Upon receipt of the report as specified above:

i. the stock exchange shall upload the same on its website as well as the Integrated Trade Repository for debt securities.

ii. The depositories shall upload the same on the centralized database for corporate bonds/ debentures as well as the Integrated Trade Repository for debt securities.

b) The stock exchange shall within five working days of the expiry of the period as specified in paragraph 8.1 above, send the reports received by it to the depositories for the purposes of their reconciliation.

c) The depositories shall thereafter within five working days of receipt of reports from the stock exchanges, send a status report to the latter regarding utilization of ISINs by the issuers.