Introduction :- One of the main purposes of bringing GST is that it would remove cascading effect by facilitating seamless flow of credit of tax paid on receipt of goods and services used in furtherance of business, ITC ( Input tax credit) is backbone of GST regime.

Who can take credit :- Every GST registered person, with some exceptions, is entitled to take credit of input tax charged on any supply of goods or services or both which are used or intended to be used in the course of furtherance of his business.

Who cannot take credit:-

a) A registered person working under composition scheme even when received goods or services are used in furtherance of his business.

b) A non- resident taxable person on receipt of goods and services except on goods imported by him.

Input tax credit (ITC):- Sec 2(63) The term ‘Input tax credit’ means the Credit of input tax.

Sec 2 (62) “Input tax” in relation to a registered person, means the central tax, State tax, integrated tax or Union territory tax charged on any supply of goods or services or both made to him and includes— (a) the integrated goods and services tax charged on import of goods;

(b) The tax payable under the provisions of sub-sections (3) and (4) of section 9;

(c)The tax payable under the provisions of sub-sections (3) and (4) of section 5 of the Integrated Goods and Services Tax Act;

(d) The tax payable under the provisions of sub-sections (3) and (4) of section 9 of the respective State Goods and Services Tax Act; or

(e) The tax payable under the provisions of sub-sections (3) and (4) of section 7 of the Union Territory Goods and Services Tax Act,

Time limit to Claim ITC:-

The time limit to claim ITC against an invoice or debit note is earlier of two dates, given below:

a) The due date for filing GST returns for September (20th Oct) of the next financial year.

(In Recent Budget Proposed – Limit of due date of filling date is 30th Nov.( No Proper clarification till date)

b) The date of filing the annual returns in form GSTR-9 relating to that financial year.

Where to take Credit: – Credit has to be taken in electronic credit Ledger (Register)

Basic Conditions for taking Credit:-

1) Possession of taxpaying documents such as tax invoice, debit note, etc.

2) Goods/ service should have actually been received/ deemed to be received by the taxable person.

3) Tax charged on the invoice and should have been paid to the credit of government.

4) Returns should have been furnished by the taxpayer.

5) Credit for goods against an invoice received in lots or installments can be availed only on last lot in installment.

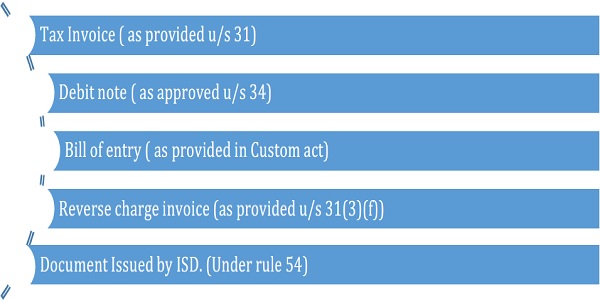

Documents required for availing ITC Sec 16(2)

Take Credit On the Basis of GSTR 2A/ GSTR 2B only.

Is it mandatory to claim ITC as per GSTR-2B or can be claimed as per books of accounts. What would be the implication for claiming of ITC as per books instead of GSTR-2B. Since GSTR-2B is showing much less than books of accounts.

Note :- As per Rule 36(4) Input tax credit to be availed by a registered person in respect of invoices or debit notes, the details of which have not been furnished by the suppliers under sub-section (1) of section 37, shall not exceed 5 per cent. of the eligible credit available in respect of invoices or debit notes the details of which have been furnished by the suppliers under sub-section (1) of section 37 in FORM GSTR-1 or using the invoice furnishing facility.

As per Rule 60(7) an auto-drafted statement containing the details of input tax credit shall be made available to the registered person in FORM GSTR-2B, for every month, electronically through the common portal, and shall consist of –

(i) the details of outward supplies furnished by his supplier, other than a supplier required to furnish return for every quarter under proviso to sub-section (1) of section 39, in FORM GSTR-1, between the day immediately after the due date of furnishing of FORM GSTR-1 for the previous month to the due date of furnishing of FORM GSTR-1 for the month.

As per above provisions ITC is to be claimed as per form GSTR-2B. However, it is auto populated in GSTR-3B but it can be changed as per Rule 36(4).

ITC Not eligible to take Credit Sec 17(5)

SECTION 17(5)(a)

(1) Motor Vehicle for transportation of person having approved seating capacity of not more than 13 persons (including driver of vehicle).

(2) Vessels and Aircraft Except when used for:

1. Further Supply

2. Transportation of passengers

3. Imparting training on navigating such vessels

4. Imparting training on flying such aircraft

5. Transportation of Goods.

NOTE THAT:-

i) Earlier ITC was prohibited for all motor vehicles and now seating capacity criteria has been inserted in new clause. Further specific prohibition for ITC on services of general insurance, servicing, repair and maintenance of motor vehicles was not there in old clause and in new clause it has specifically been prohibited to avoid disputes in this regard. Although normally tax payers were not availing ITC on such services.

ii) ITC would further be admissible for leasing, renting or hiring of motor vehicles when such motor vehicles are used for above said purposes or where the recipient is engaged in the manufacture of such motor vehicles or in the supply of general insurance services in respect of such motor vehicles insured by him. iii) The above notes i) & ii) are applicable to vessels also.

II. SECTION 17(5)(b) Following Services not eligible of ITC

(i) Foods & beverages, outdoor catering, beauty treatment, health insurance, cosmetic & plastic surgery.

Except it is used for:

Making outward taxable supply of the same category of services or an element of mixed or composite supply.

NOTE:

ITC would be available when the inward supply of goods or services or both of a particular category is used by a registered person for making an outward taxable supply of the same category of goods or services or both or as an element of a taxable composite or mixed supply.

(ii) Membership of a club, health and fitness Centre (No exception)

(iii) Rent a Cab, Life Insurance, and Health Insurance.

Except;

i) Where it is made obligatory by Government

ii) It is used for making outward taxable supply of the same category of services or an element of mixed or composite supply.

NOTE:

i) ITC would be admissible where it is obligatory for an employer to provide such supplies to its employees under any law for the time being in force.

ii) Travel Benefits to Employees; Provided that the Input Tax Credit in respect of such goods or services or both shall be available, where it is obligatory for an employer to provide the same to its employees under any law for the time being in force.

III. SECTION 17(5)(c)

NOTE :-

a) The term “construction” includes re-construction, renovation, additions or alterations or repairs, to the extent of capitalisation, to the said immovable property;

b) Further the expression “plant and machinery” means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services or both and includes such foundation and structural supports but excludes—

(i) Land, building or any other civil structures;

(ii) Telecommunication towers; and

(iii) Pipelines laid outside the factory premises.

IV. SECTION 17(5) (d)

Goods & Services received for construction of immovable property (not plant & machinery) on his own account including when such Goods/services are used in Business. (Construction includes re-construction, renovation, additions or alteration or repairs to the extent of capitalization, to the said immovable property)

NOTE:

a) The term “construction” includes re-construction, renovation, additions or alterations or repairs, to the extent of capitalisation, to the said immovable property;

b) Further the expression “plant and machinery” means apparatus, equipment, and machinery fixed to earth by foundation or structural support that are used for making outward supply of goods or services or both and includes such foundation and structural supports but excludes—

(i) Land, building or any other civil structures,

(ii) Telecommunication towers,

(iii) Pipelines laid outside the factory premises.

V. SECTION 17(5)( e)

Person who made the payment of tax under Composition (Section 10 of the CGST Act, 2017)

NOTE:

It may note here that under composition scheme the tax cannot be charged by supplier from the recipient and accordingly question ITC availment by recipient does not arise.

VI. SECTION 17(5) (g)

ITC cannot be availed on goods/service received by non-resident taxable person except; Only Goods imported by him.

NOTE: – ITC is admissible only in respect of supplies taken for business purposes. Thus supplies received for personal purposes are blocked.

VII. SECTION 17(5)(h)

Goods lost, stolen, destroyed, written off or given off as gift or free sample.

NOTE: – Such goods being not used for providing taxable supplies, the ITC thereon is blocked u/s 17(5).

VIII. SECTION 17(5)(I)

Any tax paid due to fraud cases which has resulted into –

i) Tax paid under Section 74 – tax not paid /short paid due to fraud.

ii) Tax paid under Section 129- tax paid on detention and release of goods and conveyance in transit.

iii) Tax paid under section 130-tax paid on confiscation of goods or conveyance and levied of penalty thereof. NEW PROVISION General Insurance, Servicing, repair & maintenance in so far related to such vehicles, Vessels, aircraft are not allowed Except if it is used for

1. Purpose specified therein.

2. If above services received by manufacturer of such vehicles, vessels, and aircrafts.

3. If above services received by general insurance service provider in respect of such motor, vehicles.

Author Bio

Sir,

In ARS Steels & Alloy International Pvt. Ltd. v. State Tax Officer (2021) 35 J.K.Jain’s GST & VR 12 (Mad), it was held that;

“the reversal of ITC involving S.17(5)(h) by the revenue, in cases of loss by consumption of input, proportionate to the loss of the input, which is inherent to manufacturing loss is misconceived & such loss is not contemplated/covered by the situations adumbrated u/s 17(5)(h).

In the case of Union of India & Ors. v. Hindustan Zinc Ltd. and Ors. (2014) 21 J.K.Jain’s Vat Reporter (SC), full ITC was allowed on the entire raw material used for manufacture of final product irrespective of tax free bye-product produced as a result of technological necessity.

Such loss of Inputs is not contemplated/covered by the situations adumbrated u/s 17(5)(h), GST Act. As such, no Proportionate ITC reversal is needed for Loss of Inputs in the Manufacturing Process.

Read my detailed Article in (2022) 37 J.K.Jain’s GST & VR Page R7

CA OM Prakash Jain s/o J.K.Jain , Jaipur

Tel:9414300730