Filing the FLA return is an essential requirement for corporate entities (CE) in India to report their Balance of Payment (BoP) positions to the Reserve Bank of India (RBI). By adhering to the prescribed procedures, corporate entities can accurately report their FDI, ODI, and other investment positions in a timely manner. This article provides a comprehensive overview of the filing process, guidelines, and clarifications issued by RBI.

Page Contents

- (A) Introduction on filing of FLA return by Corporate Entity (CE) with RBI

- (B) Clarifications for Filing of FLA return by CE with RBI

- 4. Clarifications for levy of Penalty against Non Filing + late filing (both) FLA returns

- 5. Clarifications for Filing of FLA return based on Unaudited financial statements

- 6. Clarifications for Filing of FLA return for financial year ending on March 31st

- 7. Clarifications for Non Filing of FLA return for financial year ending on March 31st

- 8. Clarifications for Non Filing of FLA return where zero FDI + ODI on March 31st

- 9. Clarifications for Filing of FLA return where No Additional + Fresh FDI + ODI

- 10. Clarifications for Filing of FLA return by LLP + AIF (both)

- 11. Clarifications for Filing of Annual Performance Report (APR) + FLA return (both)

- 12. Clarifications for Non Filing where 100% shares already Transferred to ROI

- 13. Clarifications for Non Filing where FDI received based on Non-Repatriation

- 14. Clarifications for prescribed form to be used for filing FLA return

- 15. Clarifications for Information’s to be filled for filling of FLA return

- 16. Clarifications for filing of Hard Copy for FLA return

- 17. Clarifications for Re-filing of FLA return

- 18. Clarifications for Valuation for FDI received by listed company

- 19. Clarifications for Valuation of FDI received by unlisted company

- 20. Clarifications for Valuation of FDI received by Traded Debt Security (TDS)

- 21. Clarifications for Filing of FLA return for Trade Credits + Trade Payables (both)

- 22. Clarifications for Inclusion of share Premium in FDI + ODI (both) in FLA return

- 23.Clarifications for Bifurcation of FDI between exceeding 10% and not exceeding 10%

- (C) FLA Return’s form + structure of form (both)

- 25. FLA return’s form + structure (both) in V Sections

- 26. Section I– Identification of Particulars of Indian corporate entity

- 27. Section II – Financial details of Indian corporate entity at face value in lakh

- 28. Section III – Foreign liabilities of Indian corporate entity at computed price

- 29. Section IV – Foreign Assets of Indian corporate entity at computed price

- 30. Section V – Variation between previous and preceding to previous year

- 31. Conclusion on filing of FLA returns for FDI + ODI (both)

- (D) User Manual for submission of online FLA Form for Company + LLP + AIF

(A) Introduction on filing of FLA return by Corporate Entity (CE) with RBI

1. Filing of FLA return for collection of Balance of Payment (BoP) position for RBI

- RBI regularly compiling information’s through FLA returns to know India’s BOP position + International Investment Position (IIP) in India + also Outside India on March 31st every year (all).

2. Filing of FLA return through Email (up to March 31st 2018)

- 100% Indian companies + LLPs + Alternative Investment Funds (AIFs) treated Indian corporate entities those required to file in excel format up to July 15th of succeeding year against Foreign Direct Investments (FDI’s) received + Overseas Direct Investments (ODI’s) made through e-mail ID on fla@rbi.org.in based on audited + also unaudited information’s (all).

3. Filing of FLA return through web portal (from March 31st 2019)

(i) RBI providing web-portal like www.flair.rbi.org.in for filing of FLA return by Indian corporate entities.

(ii) Indian corporate entity required to have registration through filing of User Registration Form (URF) containing following information’s:-

(a) Particulars of Identification

(b) Particulars of Business user

(c) Authority letter + also etc. (both)

(iii) (a) LLP + also AIF not required to use dummy Corporate Identification Number (CIN) for filing of FLA return (both).

(b) Dummy CIN not required after registration at web-portal of RBI.

(iv) Web-portal permitted for allowing to generate login-name + password for filing of FLA return after filing of URF + also completion of registration process on web-portal (all).

(v) Indian corporate entities required to furnish details for 100% investors for ODIs + FDIs + Foreign Portfolio Investments (FPIs) in India + also outside India (all).

(vi) Indian corporate entities permitted to receive system generated acknowledgement after successful submission of FLA return.

(vii) Indian corporate entities permitted to revise FLA return when original FLA return already filed.

(viii) Indian corporate entities permitted to view + also to download of information’s when FLA return already filed (both).

(ix) Indian corporate entities permitted to submit + also to revise previous year‘s information’s but after receiving confirmation from RBI through seeking request on email (both).

(x) (a) RBI not clarified till date whether filing of FLA return for year ending on March 31st, 2019 to be resubmitted through web portal when corporate entities already submitted through email.

(b) It’s suggested that corporate entities should file FLA return through web portal for year ending on March 31st, 2019 beside already filed through email to avoid any future’s confrontation with RBI.

(B) Clarifications for Filing of FLA return by CE with RBI

4. Clarifications for levy of Penalty against Non Filing + late filing (both) FLA returns

(i) Non filing + late filing FLA returns treated violation under FEMA, 1999 + liable for levy of maximum penalty @300% against amount of FDI + also ODI (all)

(ii) Generally maximum penalty @300% not being levied under FEMA, 1999 by RBI.

(iii) RBI already prescribed certain criteria’s for levy of penalty under compounding of penalties which are much lower than maximum penalty @ 300%.

5. Clarifications for Filing of FLA return based on Unaudited financial statements

(i) Indian Corporate entities permitted to submit FLA return up to July 15th based on unaudited financial statements on March 31st

(ii) Indian Corporate entities permitted to re-submit FLA return up to Sep 30th based on audited financial statement on March 31st when substantial differences existed between unaudited financial statement and audited financial statements.

6. Clarifications for Filing of FLA return for financial year ending on March 31st

- Indian Corporate entities required to submit FLA return based on financial year like from April to March each year beside actual accounting period other than from April to March.

7. Clarifications for Non Filing of FLA return for financial year ending on March 31st

(i) Indian Corporate entities not required to submit FLA return when share application money received but allotment of shares not made up to March 31st.

(ii) Indian Corporate entities required to submit FLA return when share application money received but allotment of shares not made up to March 31st + also share application money received from existing non-resident investors (both).

8. Clarifications for Non Filing of FLA return where zero FDI + ODI on March 31st

- Indian Corporate entities not required to submit FLA return when FDI + ODI not outstanding on March 31st beside foreign trade receivable + also foreign trade payables outstanding on March 31st (all).

9. Clarifications for Filing of FLA return where No Additional + Fresh FDI + ODI

- Indian Corporate entities required to submit FLA return beside no additional + no fresh FDI + also ODI received during year under consideration (all).

10. Clarifications for Filing of FLA return by LLP + AIF (both)

(i) LLP + AIF permitted for FDI + also ODI in selected areas (both)

(ii) LLP + AIF required to submit FLA return for FDI + also ODI (all).

11. Clarifications for Filing of Annual Performance Report (APR) + FLA return (both)

- Indian corporate entities required to submit FLA return beside APR already filed for ODI.

(i) Indian corporate entities not required to submit FLA return when 100% non-resident shareholding already transferred to Resident of India (ROI) before March 31st.

(ii) Indian corporate entities required to inform RBI when 100% shareholding already transferred to Resident of India through AD Bank in India

13. Clarifications for Non Filing where FDI received based on Non-Repatriation

- Indian corporate entities not required to submit FLA return when FDI received from non-resident investor on non-repatriable basis.

14. Clarifications for prescribed form to be used for filing FLA return

- Indian corporate entities required to submit FLA return through updated FLA return’s form on RBI web-portal.

15. Clarifications for Information’s to be filled for filling of FLA return

- Indian corporate entities permitted to get any clarification for submission of FLA return on landline no. of RBI :- (022) 26578662 + 26578217 + 26578348 + 26578214 + 26578340 + 26578241 + also E-mail ID surveyfla@rbi.org.in (both).

16. Clarifications for filing of Hard Copy for FLA return

- Indian corporate entities not required to submit hard copy of FLA return

17. Clarifications for Re-filing of FLA return

- Indian corporate entities required to re-submit return when error noticed by RBI.

18. Clarifications for Valuation for FDI received by listed company

- Closing share price at BSE or NSE on March 31st be adopted for valuation of FDI.

19. Clarifications for Valuation of FDI received by unlisted company

(i) Foreign liability be valued based on Own Fund of Book Value (OFBV) similar to Net Owned Fund (NOF) in India.

(ii) Closing net worth of Indian corporate entity be multiplied with % of FDI for valuation based on OFBV.

20. Clarifications for Valuation of FDI received by Traded Debt Security (TDS)

(i) TDS be valued at Market Realizable Price (MRP) + also other debts like loan + trade credit + deposit + other account payable – receivable be valued at book value.

(ii) Indian Corporate entities required to use in foreign currency rate available for March 31st for current + also previous years (both).

(iii) Net worth be computed equivalent to paid up Equity capital + paid up Participating Preference share + free reserves + share premiums + other Surplus –(minus) accumulated losses (all).

21. Clarifications for Filing of FLA return for Trade Credits + Trade Payables (both)

(i) Indian corporate entities required to include debts under other capitals like trade credits + ECBs + other structure loan (if any) + convertible + non-convertible debentures + non-participating preference share capital + other payable –(minus) other receivable when FDI + also ODI outstanding on March 31st (all).

(ii) Paid up equity capital + paid up participating preference share capital not twicely be included under other capital + also equity share capital (all).

(iii) Indian corporate entities not required to submit FLA return when FDI + ODI not outstanding on March 31st beside trade credit + also trade payable outstanding on March 31st (all).

- Indian corporate entities required to include amount of Share premiums under head free reserves + also other surpluses for computation of OFBV (both).

23.Clarifications for Bifurcation of FDI between exceeding 10% and not exceeding 10%

- Indian corporate entities required to bifurcate for FDI exceeding 10% + also not exceeding 10% (both).

24. Clarifications for Special Instructions for Filing of FLA return

(i) (a) Indian corporate entities required to study definitions before filing of FLA return

(b) Definitions available in excel format of FLA return prescribed form + also available in Annex-1 attached with FLA return Form (both).

(ii) Indian corporate entities required to report in lac in Block 1 + 2 + 4 + 5 + also to report in actual Foreign Currency in Block 3A of section IV under Foreign Asset (all).

(C) FLA Return’s form + structure of form (both)

25. FLA return’s form + structure (both) in V Sections

(i) Section I under Identification Particulars of Indian corporate entity

(ii) Section II under Financial details of Indian corporate entity

(iii) Section III under Foreign Liability of Indian corporate entity

(iv) Section IV under Foreign Asset of Indian corporate entity

(v) Section V under Variation report

26. Section I– Identification of Particulars of Indian corporate entity

(i) Under Name + address (both)

(ii) Under PAN

(iii) Under CIN

(iv) Under Contact details

(v) Under Account closing date

(vi) Under Nature of business + etc (both)

27. Section II – Financial details of Indian corporate entity at face value in lakh

(i) Under Total paid up capital

(ii) Under Non-resident shareholdings

(iii) Under Profit and loss account

(iv) Under Reserve + Surplus (both)

(v) Under Sale + Purchase (both)

(vi) Under Number of employees on payroll

28. Section III – Foreign liabilities of Indian corporate entity at computed price

(i) Investment in India under head FDI when equity participation exceeding 10%

(ii) Other capital like liability to direct investor + also claim on direct investor (both)

(iii) Disinvestment in India during year under consideration

(iv) Investment in India under FDI when equity participation not exceeding 10%

(v) Investment in India under FPI in corporate entity other than FDI at computed price

(vi) Other Investment like outstanding liability towards unrelated foreign party

29. Section IV – Foreign Assets of Indian corporate entity at computed price

(i) ODI when equity participation exceeding 10%

(ii) Equity capital + reserve + also surplus of foreign entity known Direct Investment Enterprise (DIE) all.

(iii) Overseas Direct Investment (ODI) outside India when equity participation not exceeding 10%

(iv) Portfolio Investment (PI) Outside India at computed price

(v) Other Investment like outstanding claim from foreign unrelated party

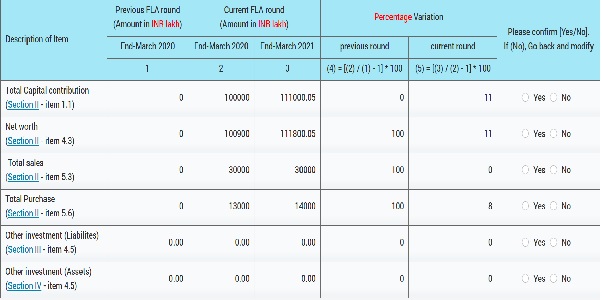

30. Section V – Variation between previous and preceding to previous year

(i) Under Paid up capital

(ii) Under Net worth

(iii) Under Total Sales

(iv) Under Total Purchases

(v)Under Other Investment – liability

(vi) Under Other Investment – asset

31. Conclusion on filing of FLA returns for FDI + ODI (both)

(i) (a) Filing of FLA return by Indian corporate entity permitted through web portal of RBI with unaudited financial statements up to July 15th when FDI + also ODI outstanding on March 31st (both).

+ (plus)

(b) Permitted through web portal of RBI with audited financial statements up to September 30th when FDI + ODI outstanding on March 31st + also substantial variation existed between amounts of unaudited financial statements and audited financial statements (all).

(ii) Filing of FLA return by Indian corporate entity not required when FDI + also ODI not outstanding on March 31st (both).

(iii) (a) Indian corporate entity required to submit FLA return for ODI beside APR already filed.

(b) Hence FLA + also APR (both) be submitted against ODI.

(iv) Indian corporate entities not required to submit FLA return for FDI + ODI:

(a) When FDI already transferred to resident of India before March 31st

(b) When FDI actually received on non repatriation basis in India

(c) When Foreign trade receivable + also trade payable outstanding without FDI or ODI on March 31st (both).

(v) (a) Indian corporate entities liable for penalty not exceeding @ 300% of FDI + ODI under FEMA, 1999 when FLA return filed late + also not filed till date (all).

+ (plus)

(b) Generally RBI not imposing penalty @ 300% but actually compounding contraventions with pre-fixed + also variable penalties (both).

(D) User Manual for submission of online FLA Form for Company + LLP + AIF

(Source for manual www.flair.rbi.org.in)

- Registration

If you want to fill returns for a new entity, you need to register on the FLAIR portal first. Refer to User Manual for FLA User Registration Form present on FLAIR portal for further guidance.

Once the registration process is completed proceed to point 1. In case you are filling the returns for an old entity, you can proceed to point 1 with previously used username and password. No need to register afresh.

1. FLA online form

1.1 Logging on to FLA online form

Step 1: Enter your user name, new password and valid Captcha. (The captcha is case sensitive.)

Step 2: Enter OTP code (the user will receive the OTP on registered E-mail ID for login)

1.2 Entry in FLA online form:

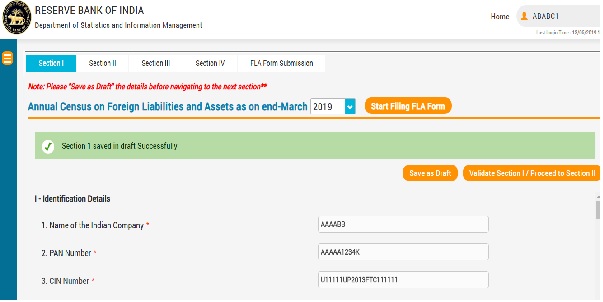

On successful login, the home page (dashboard) is displayed.

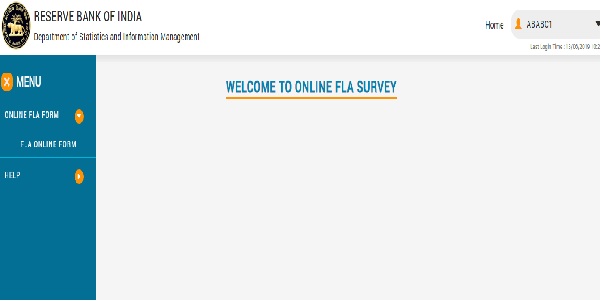

Step 1: Click on the top – left option button to open Menu. Click on “FLA Online Form”.

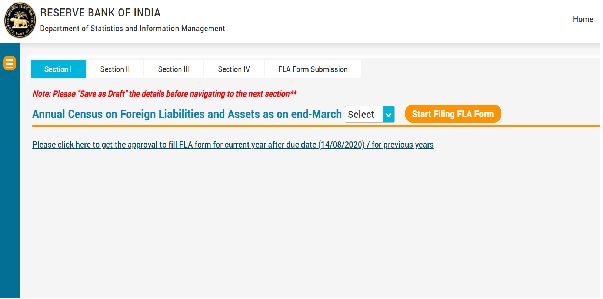

Step 2: Select the appropriate year from the drop-down list. Then click on “Start Filing FLA form”. (In case you want to fill/revise previous year return, you need to take approval from RBI by clicking on the link given below).

Thereafter the following screen will appear:

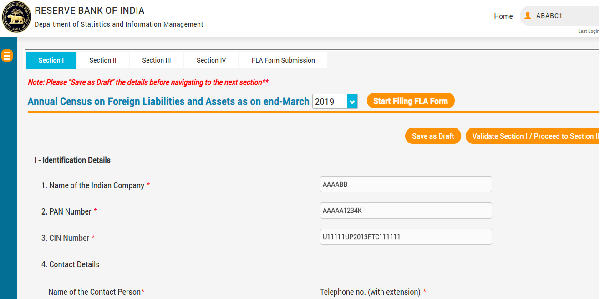

2. Section I

2. Section I

The fields in the FLA online Form for Section I are described in the following table.

All fields are mandatory, can’t be left blank.

| Table 2.1: Fields of Section I in the FLA online Form | ||

| Sr.

No. |

Field Name | Field Description |

| 1 | Name of the Indian Company* | Pre-filled, non-editable as per the FLA registration form |

| 2 | PAN number* | Pre-filled, non-editable as per the FLA registration form |

| 3 | CIN number* | Pre-filled, non-editable as per the FLA registration form |

| 4 | Name of the Contact Person* | Enter the name of the contact person |

| 5 | Telephone No. (with extension) * | Mention the telephone number with extension |

| 6 | Mobile Number* | Provide valid mobile number |

| 7 | E-Mail ID (Head of the institution) * | Pre-filled, non-editable as per the FLA registration form |

| 8 | E-Mail of Contact person* | Enter the Email ID of the contact person |

| 9 | Designation* | Mention the designation of the contact person |

| 10 | Website (if any) | Enter the website of the company, if any |

| 11 | Account Closing date* | Choose the date of closing account for submission of current FLA return from the side arrow of calendar |

| 12 | Nature of Business (As per National Industrial Classification (NIC) 2008 Code) * | Choose the nature of business as per National Industrial Classification (NIC) 2008 Code from the drop-down menu. Refer the Annex-1 for the list of National Industrial Classification (NIC) 2008 Codes |

| 13 | Whether your company is merged/amalgamated during year* | Select Yes or No.

In case of Yes is selected, then provide the details of new company merged/amalgamated, number of merged companies and the name of merged entity. |

| 14 | Whether the company is listed? * | Choose appropriate option for your company is listed or not. If your company’s CIN number is started from L, its means, it’s Listed company and then choose Yes, else choose No. |

| 15 | Identification of the reporting company (in terms of inward FDI) * | Choose appropriate option from the drop-down menu. |

| 16 | Type of company* | Select appropriate option from the drop-down menu |

| 17 | Whether the Company is Asset Management Company? * | Select Yes or No. |

| 18 | Whether the Company has Technical Foreign collaboration? * | Select Yes or No. |

| 19 | Whether the company has any business activity during latest financial year? * | Select Yes or No. |

Please note, the fields marked * are mandatory.

Apart from the above fields, the following table needs to be filled with appropriate data:

In case your company is listed; you need to fill the following table as well:

After filling all the details in Section I, click on “Save as Draft”.

Then click on “Validate Section I/Proceed to Section II”.In case some error is found during validation, you will have to rectify the error. After all the validation checks are successfully completed, you will be able to proceed to Section II.

3. Section II (Financial Details)

The fields in the FLA online Form for Section II are described in the following table.

All fields are mandatory, can’t be left blank.

| Table 2.2: Fields of Section II in the FLA online Form | ||

| Sr.

No. |

Field Name | Field Description |

| 1. Total Paid-up Capital of Indian Company | ||

| 1.0 | Total Paid-up Capital | Auto-calculated (sum of point 1.1 and 1.2) Paid-up capital of a company cannot be zero or blank. |

| 1.1 | Total Equity & Participating Preference share Capital | Auto-calculated (sum of ordinary/equity share and Participating Preference share) |

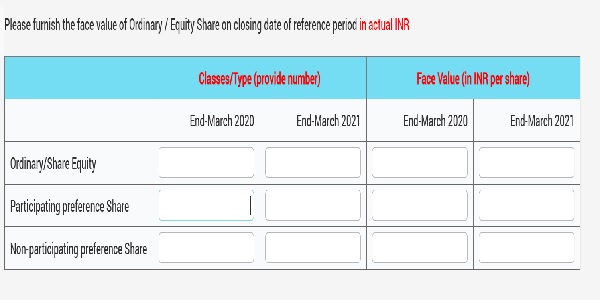

| (a) | Ordinary/Equity Share | Enter number of shares in actual for the end March; Amount will be Auto-calculated.

In case of different class of Equity Shares, consolidated figure should be reported |

| (b) | Participating Preference Share | Enter number of shares in actual for the end March; Amount will be Auto-calculated. |

| 1.2 | Non-Participating Preference share | Enter number of shares in actual for the end March; Amount will be Auto-calculated. |

| 2. Non-Resident Holdings | ||

| 2.1 | Equity and Participating Preference Share Capital | Auto-calculated (sum of item-1 to item-12).

Enter the number of shares in actual for the items (1 to 12) mentioned under the head 2.1 |

| 2.2 | Non-Participating Preference Share | Enter number of shares in actual for the end March. |

| 3.0 | Non Resident Equity & Participating Preference Share Capital% | Auto-calculated. |

| 3. Profit and Loss account (From P/L Account) | ||

| 3.1 | Profit(+)/Loss(-) before tax (during the year) | Enter appropriate amount in INR lakhs for the item 3.1 for the last two financial years. |

| 3.2 | Profit(+)/Loss(-) after tax (during the year) | Enter appropriate amount in INR lakhs for the item 3.2 for the last two financial years. |

| 3.3 | Dividend (Interim and Final Dividend) | Enter appropriate amount in INR lakhs for the item 3.3 for the last two financial years. |

| 3.4 | Tax on Dividend (if any) | Enter appropriate amount in INR lakhs for the item 3.4 for the last two financial years. |

| 3.5 | Retained Profit | Auto-calculated |

| 4. Reserves & Surplus (from Balance sheet) | ||

| 4.1 | Reserves & Surplus | Enter appropriate amount in INR lakhs for the item 4.1during the last two years. |

| 4.2 | Of which, Profit (+) and Loss (-) account balance | Enter appropriate amount in INR lakhs for the item 4.2 during the last two years. |

| 4.3 | Net worth of Company | Formula for Net Worth is = Total Equity & Participating Preference Share capital + Reserves and Surplus (this field is automated in FLA form section-II, companies are not required to compute it separately) |

| 5. Sales and Purchase made during the financial year

Note: To be filled in by all companies/LLPs |

||

| 5.1 | Domestic Sales | Enter appropriate amount in INR lakhs for the item 5.1 for the last two financial years. |

| 5.2 | Exports | Enter appropriate amount in INR lakhs for the item 5.2 for the last two financial years. |

| 5.3 | Total Sales | Auto-calculated (5.1 + 5.2) |

| 5.4 | Domestic Purchase | Enter appropriate amount in INR lakhs for the item 5.4 for the last two financial years. |

| 5.5 | Imports | Enter appropriate amount in INR lakhs for the item 5.5 for the last two financial years. |

| 5.6 | Total Purchase | Auto-calculated (5.4+5.5) |

| 6. Employee Information of reporting Indian company | ||

| 6.1 | No. of employees on payroll (in actual) | Enter actual number of employees on payroll at the end of March (current year as well as previous year) |

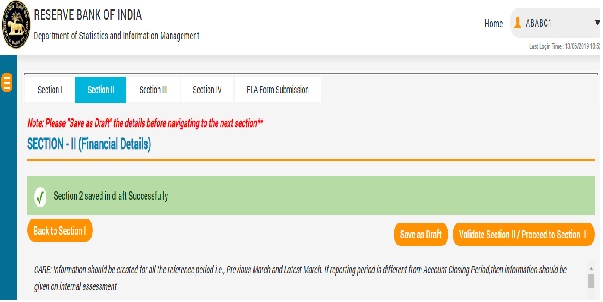

After filling all the details in Section II, click on “Save as Draft”, then click on “Validate Section II/Proceed to Section III”.

3. Section III Foreign Liabilities (Investment made in India)

Please consider the below points while entering the data in section III:

- Information should be reported for all the reference period, i.e. Previous March and Latest March.

- If Account Closing Period of the company is different from reference period, then information should be reported on internal assessment basis for the reference period.

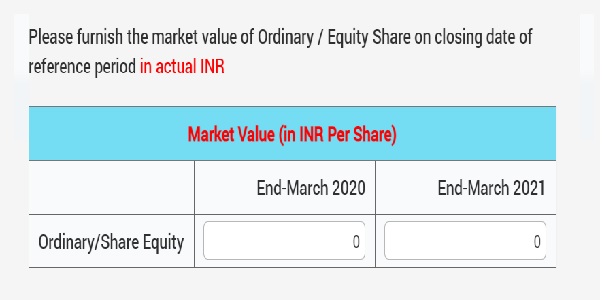

- In case of listed companies, equity is valued using share price on closing date of reference period (this is automated field).

- In case of unlisted companies, Own Fund of Book Value (OFBV) Method is used for equity valuation (this is automated field).

The fields in the FLA online Form for Section III are described in the following table.

All fields are mandatory, can’t be left blank.

|

Table 2.3: Fields of Section III in the FLA online Form |

|||

| Sr. No. | Field Name | Field Description | |

| Block 1. Investment in India under Foreign Direct Investment (FDI) scheme

(10% or more Equity Participation) Please furnish here the outstanding investments made under the FDI Scheme in India by Non-resident Direct investors, who were individually holding 10 per cent or more ordinary/equity & preference shares of your company on the reference date. |

|||

| 1.a | No. of foreign direct investors during the year (10% or more Equity participation) | Enter the number of foreign direct investors during the year. | |

| 1.a.1 | Month and Year of receiving FDI first time (in your company) | Select appropriate month from the drop down menu and enter the year of receiving the FDI first time. | |

| 1.b FDI

Based on number of foreign direct investors mentioned in 1.a, there will be auto display thelist of 1.b.1 FDI 1, 1.b.2 FDI2 … and up to number of FDIbased on previous year FLA return. For example, if no. of FDI “3” is entered in 1.a, then system willdisplay the list of 3 FDI investors in1.b block i.e. 1.b.1 FDI1, 1.b.2 FDI2, 1.b.3 FDI3.

|

|||

| Equity & Participating Preference Share Capital holding | Enter the percentage of Equity & Participating Preference Share Capital holding as at the end of previous year and latest year. | ||

| 1.0 | Equity Capital | Auto-calculated | |

| 1.1 | Liabilities to Direct Investors | Auto-calculated | |

| 1.2 | Claims on Direct Investors

(Reverse investment) |

Enter appropriate amount in INR lakhs for the item 1.2at the end-March of the reporting year and its previous year. | |

| 2.0 | Other Capital | Auto-calculated | |

| 2.1 | Liabilities to Direct Investor | Enter appropriate amount in INR lakhs for the item 2.1at the end-March of the reporting year and its previous year. | |

| 2.2 | Claims on Direct Investor | Enter appropriate amount in INR lakhs for the item 2.2at the end-March of the reporting year and its previous year. | |

| 3.0 | Disinvestments in India during the year | Enter appropriate amount in INR lakhs for the item 3.0at the end-March of the reporting year and its previous year. | |

|

|||

Block 2 Investment in India under Foreign Direct Investment (FDI) scheme (Less than 10% Equity Holding)

|

|||

| 2.a | Number of countries (with less than 10% Equity holding) from each during the year | Enter the number of countries with less than 10% Equity holding from each during the year. | |

| 2.b DI- Direct Investment

Based on number of countries mentioned in 2.a, there will be auto display thelist of 2.b.1 DI 1, 2.b.2 DI2 … and up to number of countries of non-resident investor. For example, if no. of DIas “3” is entered in 1.a, then system willdisplay the list of 3 DI investors in 2.b block i.e. 2.b.1 DI1, 2.b.2 DI2, 2.b.3 DI3.

|

|||

| Equity & Participating Preference Share Capital holding | Enter the percentage of Equity & Participating Preference Share Capital holding as at the end of previous year and latest year. | ||

| 1.0 | Equity Capital | Auto-calculated | |

| 1.1 | Liabilities to Direct Investors | Auto-calculated | |

| 1.2 | Claims on Direct Investors (Reverse investment) | Enter appropriate amount in INR lakhs for the item 1.2at the end-March of the reporting year and its previous year. | |

| 2.0 | Other Capital | Auto-calculated | |

| 2.1 | Liabilities to Direct Investor | Enter appropriate amount in INR lakhs for the item 2.1at the end-March of the reporting year and its previous year. | |

| 2.2 | Claims on Direct Investor | Enter appropriate amount in INR lakhs for the item 2.2at the end-March of the reporting year and its previous year. | |

| 3.0 | Disinvestments in India during the year | Enter appropriate amount in INR lakhs and details of disinvestments also need to be provided for the item 3.0at the end-March of the reporting year and its previous year. | |

|

|||

| Block 3 Portfolio Investment in India

Please furnish here the outstanding investments by non-resident investors, other than those made under Foreign Direct Investment Scheme in India (i.e. other than those reported in 1.b FDI&2.b DI). |

|||

| Equity & Participating Preference share capitalholding | Enter the percentage of Equity & Participating Preference share capitalholding as at the end of previous year and latest year | ||

| 1.0 | Equity Securities (at Market Value) | Enter appropriate amount in INR lakhs for the item 1.0at the end-March of the reporting year and its previous year. | |

| 2.0 | Debt Securities | Auto-calculated | |

| 2.1 | Money Market Instruments

(Original Maturity up to 1 year) |

Enter appropriate amount in INR lakhs for the item 2.1at the end-March of the reporting year and its previous year. | |

| 2.2 | Bonds and Other instruments (original maturity more than 1year) | Enter appropriate amount in INR lakhs for the item 2.2at the end-March of the reporting year and its previous year. | |

| 3.0 | Disinvestments in India during the year | Enter appropriate amount in INR lakhs for the item 3.0at the end-March of the reporting year and its previous year. | |

| Note: Please ensure that Non-resident Equity & Participating Preference share capital mentioned at item 2.1 of Section II should be reported in either 1.b FDI or 2.b DI or 3. PI at Market Value i.e. sum of equity % in 1.b FDI, 2.b DI&3. PI must be equal to the item 2.3 of section II. | |||

| Block 4 Other Investment (Outstanding liabilities with Foreign Unrelated Parties)

This is a residual category that includes all financial liabilities not considered as direct investment or portfolio investment. |

|||

| 1.1 | Trade Credit | Enter appropriate amount in INR lakhs for the item 1.1at the end-March of the reporting year and its previous year. | |

| 1.2 | Loans | Enter appropriate amount in INR lakhs for the item 1.2at the end-March of the reporting year and its previous year. | |

| 1.3 | Currency & Deposits | Enter appropriate amount in INR lakhs for the item 1.3at the end-March of the reporting year and its previous year. | |

| 1.4 | Other receivable and payable accounts | Enter appropriate amount in INR lakhs for the item 1.4at the end-March of the reporting year and its previous year. | |

| Total | Auto-calculated | ||

After filling all the details in Section III, click on “Save as Draft”, then click on “Validate Section III/Proceed to Section IV”

5. Section IV (Foreign Assets)

The fields in the FLA online Form for Section IV are described in the following table.

All fields are mandatory, can’t be left blank.

| Table 2.4: Fields of Section IV in the FLA online Form | ||

| 1.Please use the exchange rate as at end-March Previous FY and end-March Latest FY(as applicable) of reporting year while reporting the Foreign Assets in INR lakh.

2.Incase if overseas company is listed,equity should be valued using share price on closing date of reference period(Item 1.1 of 1.b ODI, item 1.1 of 2.b DI and item 1.1 of 3. PI) 3.If overseas company is unlisted,Own Fund of Book Value (OFBV)Method should be used for the valuation of equity investments (Item 1.1 of 1.b ODI, item 1.1 of 2.b DI and item 1.1 of 3. PI) 4. Imports, Exports, Total Sales and Total Purchase of Direct Investment Enterprise (DIE) Abroad (more than 50% equity holding by Indian reporting company) |

||

| 1. Equity Capital (PUC), Reserves & Surplus of Direct Investment Enterprise (DIE) Abroad (10% or more equity holding by Indian reporting company).

[Please report here the total equity of DIE, equity held by your company, reserves (excluding P&L Account) and Profit & Loss Account of those DIEs in each of which your company hold 10% or more equity shares on the reference date.] |

||

| 1. Direct Investment Abroad under Overseas Direct Investment (ODI) Scheme (10% or more equity holding) | ||

| 1.a | No. of Direct Investment Enterprises (DIE) Abroad as on end-March 2019 | Enter the number of Overseas Direct Investment (ODI) Enterprises during the year. |

| 1.a.1 | Month and Year of ODI made first time (by your company) | Select appropriate month from the drop-down menu and enter the year when the ODI made first time. |

| 1.b ODI

Based on number of Overseas Direct Investment (ODI) mentioned in 1.a, there will be auto display thelist of 1.b.1 ODI 1, 1.b.2 ODI2 … and up to number of DIEs as you have mentioned in 1.a. For example, if no. of ODI “3” is entered in 1.a, then system willdisplay the list of 3 ODI investors in 1.b block i.e. 1.b.1 ODI1, 1.b.2ODI2, 1.b.3ODI3.

|

||

| Equity & Participating Preference Share Capital holding | Enter the percentage of Equity & Participating Preference Share Capital holding as at the end of March previous year and reporting year. | |

| 3.1 | Reported Foreign Currency | Choose reported foreign currency from the drop-down menu |

| 3.2 | Total Equity of DIE (Paid Up Capital of DIE) | Enter Total Equity amount of DIE in Foreign Currency (in actuals) as at the end of March previous year and reporting year. |

| 3.3 | Equity of DIE held by you (at face value) | Enter Equity of DIE held by you in Foreign Currency (in actuals) as at the end of March previous year and reporting year. |

| 3.4 | Reserves and Surplus | Enter reserves and surplus in Foreign Currency (in actuals) as at the end of March previous year and reporting year. |

| 3.4.1 | Of which, Profit (+) and Loss (-) account balance | Enter appropriate amount in Foreign Currency (in actuals) as at the end of March previous year and reporting year. |

| 3.5 | Net Worth of DIE | Auto-calculated |

| 3.6 | Exchange rate in Rs.per unit foreign currency* | EnterExchange rate of reporting foreign currency against Indian Rs. should be given as on closing date of reference period. |

| 3.7 | Total Sales | Enter total sales in Foreign Currency (in actuals) as at the end of March previous year and reporting year. |

| 3.7.1 | of which Exports | Enter Exports of total sales in Foreign Currency (in actuals) as at the end of March previous year and reporting year. |

| 3.8 | Total Purchase | Enter total Purchase in Foreign Currency (in actuals) as at the end of March previous year and reporting year. |

| 3.8.1 | of which Imports | Enter Imports of total sales in Foreign Currency (in actuals) as at the end of March previous year and reporting year. |

| 3.9 | No. of Employees on Payroll | Enter number of employees on payroll as at the end of March previous year and reporting year. |

| Please furnish here the market value of outstanding investments in DIE, made by your company under the ODI Scheme, in each of which your company hold 10% or more equity shares on the reference date. | ||

| 1.0 | Equity Capital | Auto-calculated |

| 1.1 | Claims on Direct Investment Enterprise | Enter appropriate amount on claims on DIEunder Equity capital in INR lakhs at the end-March of the reporting year and its previous year. |

| 1.2 | Liabilities to Direct Investment Enterprise (Reverse investment) | Enter appropriate amount of liabilities to DIEunder Equity capital in INR lakhs at the end-March of the reporting year and its previous year. |

| 2.0 | Other Capital | Auto-calculated |

| 2.1 | Claims on Direct Investment Enterprise | Enter appropriate amount on claims on DIEunder other capital in INR lakhs at the end-March of the reporting year and its previous year. |

| 2.2 | Liabilities to Direct Investment Enterprise (Reverse investment) | Enter appropriate amount on liabilities on DIEunder other capital in INR lakhs at the end-March of the reporting year and its previous year. |

| 3.0 | Disinvestments abroad during the year | Enter appropriate amount of disinvestment abroad during the year in INR lakhs. |

| #: Other capital, item 2.1 & 2.2 of 2.b ODI includes all other liabilities and claims at Nominal value, except equity, (i.e. trade credit, loan, debentures, Non-participating share capital, other accounts receivable and payables etc.) of Indian reporting company with non-resident companies where Indian company holds less than 10 per cent equity and also with related parties. | ||

|

||

Block 2 DI – Direct Investment Abroad (Less than 10% equity holding)

|

||

| 2.a | No. of Countries where your co. holds less than 10 % equity shares in each under the ODI Scheme | Enter the number of countries with less than 10% equity shares in each under the ODI Scheme during the year.

|

| 2.b DI- Direct Investment

Based on number of countries mentioned in 2.a, there will be auto display thelist of 2.b.1 DI 1, 2.b.2 DI2 … and up to number of countries. For example, if no. of DI “3” is entered in 1.a, then system willdisplay the list of 3 DI investors in 2.b block i.e. 2.b.1 DI1, 2.b.2 DI2, 2.b.3 DI3.

|

||

| Equity & Participating Preference Share Capital holding | Enter the percentage of Equity & Participating Preference Share Capital holding as at the end of March previous year and reporting year. | |

| 1.0 | Equity Capital | Auto-calculated |

| 1.1 | Claims onDirect Investment Enterprise | Enter appropriate amount in INR lakhs for the item 1.1as at the end of March previous year and reporting year. |

| 1.2 | Liabilities to Direct Investment Enterprise (Reverse investment) | Enter appropriate amount in INR lakhs for the item 1.2as at the end of March previous year and reporting year. |

| 2.0 | Other Capital | Auto-calculated |

| 2.1 | Claims on Direct Investment Enterprise | Enter appropriate amount in INR lakhs for the item 2.1as at the end of March previous year and reporting year. |

| 2.2 | Liabilities to Direct Investment Enterprise (Reverse investment) | Enter appropriate amount in INR lakhs for the item 2.2as at the end of March previous year and reporting year. |

| 3.0 | Disinvestments abroad during the year | Enter appropriate amount in INR lakhs for the item 3.0as at the end of March previous year and reporting year. |

|

||

| Block 3 Portfolio Investment in India

Please furnish here the market value of outstanding investments in non-resident enterprises, other than those made under ODI scheme reported in Block 2.b.1. |

||

| 3.a | Country of Non-Resident Enterprise | Enter the number of countries of Non-Resident Enterprise |

| 3.b PI

Based on number of Country of Non-Resident Enterprise (PI) mentioned in 3.a, there will be auto display thelist of 3.b.1 PI1, 3.b.2 PI2 … and up to number of PIbased on previous year FLA return. For example, if no. of PI “3” is entered in 1.a, then system willdisplay the list of 3 PI investors in 3.b block i.e. 3.b.1 PI1, 3.b.2PI2, 3.b.3PI3. It will display the Country of non-resident investor.

|

||

| Country of DIE | Choose country from the drop down menu | |

| 1.0 | Equity Securities (at Market Value) | Enter appropriate amount in INR lakhs for the item 1.0at the end-March of the reporting year and its previous year. |

| 2.0 | Debt Securities | Auto-calculated |

| 2.1 | Money Market Instruments

(Original Maturity up to 1 year) |

Enter appropriate amount in INR lakhs for the item 2.1at the end-March of the reporting year and its previous year. |

| 2.2 | Bonds and Other instruments

(original maturity more than 1year) |

Enter appropriate amount in INR lakhs for the item 2.2at the end-March of the reporting year and its previous year. |

| 3.0 | Disinvestments in India during the year | Enter appropriate amount in INR lakhs for the item 3.0at the end-March of the reporting year and its previous year. |

| Block 4 Other Investment (Outstanding Claims with Foreign Unrelated Parties)

This is a residual category that includes all financial claims not considered as direct investment or portfolio investment. |

||

| 1.1 | Trade Credit | Enter appropriate amount in INR lakhs for the item 1.1at the end-March of the reporting year and its previous year. |

| 1.2 | Loans | Enter appropriate amount in INR lakhs for the item 1.2at the end-March of the reporting year and its previous year. |

| 1.3 | Currency & Deposits | Enter appropriate amount in INR lakhs for the item 1.3at the end-March of the reporting year and its previous year. |

| 1.4 | Other receivable and payable accounts | Enter appropriate amount in INR lakhs for the item 1.4at the end-March of the reporting year and its previous year. |

| Total | Auto-calculated | |

After filling all the details in Section IV, click on “Save as Draft”, then click on “Validate Section IV/Proceed to FLA Form Submission”, screenshot of which is given below:

6. Variation report

The table given in the screenshot below will come with numbers in column 1, 2 and 3 in accordance with what is entered in the previous Sections:

Please check if the entries corresponding to the items mentioned in the 1st column (Description of Item) is in accordance with what is mentioned in your records. If there is some discrepancy, go to the respective Section and enter correct details. Once all the data in the variation report are correct, select “Yes” in the last column of the above table, corresponding to all the rows. Then, “Confirm” the declaration which will be present at the bottom of the above table. Thereafter, submit the FLA Form to RBI by clicking on the “Submit to RBI” button that pops up on the screen. Links to download the submitted FLA Form and a system – generated acknowledgement form will be generated. Download these documents and keep for your future reference.

Annex-1

| NIC DIVISION DESCRIPTION | NIC CODE |

| Crop and animal production, hunting and related service activities | 1 |

| Forestry and logging | 2 |

| Fishing and aquaculture | 3 |

| Mining of coal and lignite | 5 |

| Extraction of crude petroleum and natural gas | 6 |

| Mining of metal ores | 7 |

| Other mining and quarrying | 8 |

| Mining support service activities | 9 |

| Manufacture of food products | 10 |

| Manufacture of beverages | 11 |

| Manufacture of tobacco products | 12 |

| Manufacture of textiles | 13 |

| Manufacture of wearing apparel | 14 |

| Manufacture of leather and related products | 15 |

| Manufacture of wood and products of wood and cork, except furniture | 16 |

| Manufacture of paper and paper products | 17 |

| Printing and reproduction of recorded media | 18 |

| Manufacture of coke and refined petroleum products | 19 |

| Manufacture of chemicals and chemical products | 20 |

| Manufacture of pharmaceuticals, medicinal chemical and botanical products | 21 |

| Manufacture of rubber and plastics products | 22 |

| Manufacture of other non-metallic mineral products | 23 |

| Manufacture of basic metals | 24 |

| Manufacture of fabricated metal products, except machinery and equipment | 25 |

| Manufacture of computer, electronic and optical products | 26 |

| Manufacture of electrical equipment | 27 |

| Manufacture of machinery and equipment n.e.c. | 28 |

| Manufacture of motor vehicles, trailers and semi-trailers | 29 |

| Manufacture of other transport equipment | 30 |

| Manufacture of furniture | 31 |

| Other manufacturing | 32 |

| Repair and installation of machinery and equipment | 33 |

| Electricity, gas, steam and air conditioning supply | 35 |

| Water collection, treatment and supply | 36 |

| Sewerage | 37 |

| Waste collection, treatment and disposal activities; materials recovery | 38 |

| Remediation activities and other waste management services | 39 |

| Construction of buildings | 41 |

| Civil engineering | 42 |

| Specialized construction activities | 43 |

| Wholesale and retail trade and repair of motor vehicles and motorcycles | 45 |

| Wholesale trade, except of motor vehicles and motorcycles | 46 |

| Retail trade, except of motor vehicles and motorcycles | 47 |

| Land transport and transport via pipelines | 49 |

| Water transport | 50 |

| Air transport | 51 |

| Warehousing and support activities for transportation | 52 |

| Postal and courier activities | 53 |

| Accommodation | 55 |

| Food and beverage service activities | 56 |

| Publishing activities | 58 |

| Motion picture, video and television programme production, sound recording and music publishing activities | 59 |

| Broadcasting and programming activities | 60 |

| Telecommunications | 61 |

| Computer programming, consultancy and related activities | 62 |

| Information service activities | 63 |

| Financial service activities, except insurance and pension funding | 64 |

| Insurance, reinsurance and pension funding, except compulsory social security | 65 |

| Other financial activities | 66 |

| Real estate activities | 68 |

| Legal and accounting activities | 69 |

| Activities of head offices; management consultancy activities | 70 |

| Architecture and engineering activities; technical testing and analysis | 71 |

| Scientific research and development | 72 |

| Advertising and market research | 73 |

| Other professional, scientific and technical activities | 74 |

| Veterinary activities | 75 |

| Rental and leasing activities | 77 |

| Employment activities | 78 |

| Travel agency, tour operator and other reservation service activities | 79 |

| Security and investigation activities | 80 |

| Services to buildings and landscape activities | 81 |

| Office administrative, office support and other business support activities | 82 |

| Public administration and defence; compulsory social security | 84 |

| Education | 85 |

| Human health activities | 86 |

| Social work activities with accommodation | 87 |

| Social work activities without accommodation | 88 |

| Creative, arts and entertainment activities | 90 |

| Libraries, archives, museums and other cultural activities | 91 |

| Gambling and betting activities | 92 |

| Sports activities and amusement and recreation activities | 93 |

| Activities of membership organizations | 94 |

| Repair of computers and personal and household goods | 95 |

| Other personal service activities | 96 |

| Activities of households as employers of domestic personnel | 97 |

| Undifferentiated goods- and services-producing activities of private households for own use | 98 |

| Activities of extraterritorial organizations and bodies | 99 |

Conclusion: Filing the FLA return is a crucial obligation for corporate entities in India to report their BoP positions to RBI. Understanding the guidelines and clarifications provided by RBI ensures compliance and avoids penalties for non-filing or late filing. By adhering to the prescribed procedures, corporate entities can accurately report their FDI, ODI, and other investment positions in a timely manner.

*****

(Author can be reached at email address satishagarwal307@yahoo.com or on Mobile No. 9811081957)

Disclaimer : The contents of this article are solely for informational purpose. Neither this article nor the informations as contained herein constitutes a contract or will form the basis of a contract. The material contained in this article does not constitute or substitute professional advice that may be required before acting on any matter. While every care has been taken in the preparation of this article to ensure its accuracy at the time of publication. Satish Agarwal assumes no responsibility for any error which despite all precautions may be found herein. We shall not be liable for direct, indirect or consequential damages if any arising out of or in any way connected with the use of this article or the informations as contained herein.

Author Bio

If the company is closed before 31st March 2023.

Do we still have to file FLA return before 15th July 2023 ?

Hi Sir,

If an foreign investor purchases Shares of an Indian Company from an existing Resident share holder. whether the company needs to file FLA in this case?

In which Regulation/Master Direction the revised FLA return is mentioned?

Question: What information should be reported in FLA return, if balance sheet of the company is not audited before the due date of submission?

Answer: If the company’s accounts are not audited before the due date of submission, i.e. July 15, then the FLA Return should be submitted based on unaudited (provisional) account. Once the accounts gets audited and there are revisions from the provisional information submitted by the company, they are supposed to submit the revised FLA return based on audited accounts by end – September.

Source:- Q.2 of FAQ under the head General Instruction dated 18/06/2014

https://m.rbi.org.in/Scripts/FAQView.aspx?Id=95