Securities and Exchange Board of India

Consultation Paper regarding developing “One Commodity One Exchange”

1. Objective:

1.1. The objective of this consultation paper is to solicit comments/views from the public on the proposal regarding developing the concept of “One Commodity One Exchange” so as to reduce fragmentation of liquidity and help every stock exchange to develop an exclusive set of un-fragmented liquid contracts.

2. Background:

2.1. Internationally, it has been observed that derivatives contracts on a specific commodity are traded as liquid contracts only on one particular commodity exchange and the said specific commodity/contract is almost identified with that commodity exchange. Historically, such a situation of one liquid commodity contract on one specific commodity exchange has evolved either based on competition or by way of regulatory desire and encouragement. Over the years, this practice has aided in developing and deepening the commodity derivatives markets in those jurisdictions. Allowing derivative contracts on a unique set of commodities to be developed and traded at specific exchanges has not only helped in preventing avoidable fragmentation of liquidity among various commodity exchanges but also has helped some of these exchanges/countries to become price setters in those specific commodities and their futures prices are being referred to as benchmark prices for both futures and spot markets for that commodity in other jurisdictions of the world.

2.2. The table below enumerates the major exchanges in the world whose traded futures prices are considered as global benchmark prices for the underlying commodities in other jurisdictions as well:

Table A: Price of major exchanges acts as benchmark prices for the underlying commodities

| Exchange | Region | Benchmark prices for major commodities |

| BMD | Malaysia | Crude Palm Oil (CPO) |

| CME Group | USA | Soybean, Corn, Wheat, Gold, Silver, Crude Oil and Natural gas |

| ICE Futures | USA/Europe | Cocoa, Coffee, Sugar, Cotton and Crude Oil |

| LME | UK | Non-ferrous metals such as Aluminum, Nickel, Zinc and Lead etc. |

| TOCOM | Japan | Rubber |

| DCE | China | Iron Ore |

2.3. As mentioned at para 2.1, the aforesaid phenomenon of one benchmark price by one commodity exchange has evolved over a period of time under conducive regulatory environment of those jurisdictions. It is also observed that many International commodity exchanges generally do not launch derivatives contracts on the same commodity which is already listed for trading in another commodity exchange of the same jurisdiction to avoid fragmentation of liquidity. As a result, the exchanges are able to focus on a specific commodity for its development and also develop a deep connect with all the stakeholders of that specific commodity.

2.4. With such a unique set of commodity derivatives products being available for trading at each of the above noted commodity exchanges, liquidity in those contracts does not get fragmented amongst various exchanges and focus of the specific exchange always remains on the product development and deepening derivative market on the said commodity instead of whiling away resources in competition to take away liquidity on the same commodity/products from other commodity exchanges.

2.5. As per media reports, over the last two years, the drivers of global price discovery in many commodities are shifting from West to the East due to increase in consumption and production. For example, despite being one of the world’s largest consumer of many commodities, China till a few years ago was a price-taker and not the price-setter for those products. Now, it has a long-term say in commodity prices and in some commodities, it has become a strong rival price setter thereby influencing markets in other jurisdictions. On other hand, though India is also either one of the largest consumers or producers of a number of commodities, we have little or negligible say in setting the commodity prices, in such products.

3. Background of the concept:

3.1. In the aforesaid context, there is a felt need that India should consider exploring the idea of developing exchange specific unique set of commodities so as to reduce fragmentation of liquidity and help every exchange to develop an exclusive set of unfragmented liquid contracts on a specific set of commodities. This would help in developing the Indian commodity derivatives markets in the following manner:

3.1.1. increased focus of the stock exchanges would be on product development and connecting with the entire value chain and stakeholders, which is a time consuming process, instead of battling competition on the same products from other stock exchanges from day one of launching a contract;

3.1.2. liquidity in such contracts would not get fragmented amongst various stock exchanges during early stage of the contract life cycle;

3.2. India is the largest producer or consumer of a large number of goods, including pulses, rice, spices, rubber, cotton, tea, iron ore, steel, gold, silver, diamond etc. Of these commodities, diamonds, rice, gold, rubber, sugar etc., form major part of India’s export / import.

3.3. Currently, 91 goods have been notified by the Central Government as eligible for trading in commodity derivatives segment, which can be reviewed by the Government from time to time. Of these 91 goods, contracts that are available for trading comprise around 40 such goods (including the variants) and in most of these contracts the volumes as well as open interest are not very significant. Though the contracts on many commodities are commonly traded on multiple exchanges albeit with slight variations in contract specifications, the liquidity of such contracts on specific commodities is practically concentrated on specific stock exchanges. For example, NCDEX dominates in agricultural commodity derivatives such as soybean complex, Guar seed, Spices etc., while MCX dominates in bullion and metal commodity derivatives such as gold, aluminum, copper, lead, nickel, etc.

3.4. Pursuant to the concept of universal exchanges mooted by SEBI since October 2018, BSE has launched contracts in Crude Oil, Gold, Cotton, Soybean and turmeric etc., while NSE has launched contracts in Gold and Crude Oil. However, at present, even after a passage of 3 years, turnover and open interest in commodity derivatives contracts at both BSE and NSE are not very significant compared to turnover and open interest at NCDEX and MCX.

3.5. Therefore, it is apparent, that for all practical purposes, liquidity continues to remain concentrated on a specific stock exchange for specific commodities. Thus, although each stock exchange is at liberty to launch contracts on the same commodity which is already being traded on another stock exchange, it may cause shifting of some amount of liquidity from the existing contract already being traded. Ultimately, the liquidity continues to rule in the existing contract but gets fragmented to a certain extent. As a result, the overall liquidity of the specific commodity does not improve and the existing liquid contract does not move in the direction of becoming a benchmark contract, since the priority of product development and deepening of the market gets diluted by competition to share the existing market/liquidity on the said commodity.

3.6. In the past, it has been observed that contracts with same underlying commodity are available for trading on multiple exchanges, as indicated in the table below:

Table B: List of contracts with underlying commodity available for trading on multiple exchanges

| Underlying Commodity | Exchanges |

| Gold | MCX, BSE and NSE |

| Silver | MCX, BSE and NSE |

| Cotton | MCX and BSE |

| Guar Seed | NCDEX, ICEX and BSE |

| Guar Gum | NCDEX and BSE |

| Castor Seed | NCDEX, ICEX and MCX |

| Turmeric | NCDEX and BSE |

| Crude Oil | MCX, NSE and BSE |

3.7. From the experience of having multiple contracts on same commodities, the following observations can be made:

3.7.1. Some contracts which are available for trading on multiple exchanges have almost same contract specifications, with one or more exchanges providing discounts or other benefits to garner trading volume on its platform. As a result, all these exchanges end up pursuing and chasing the same set of market participants. A notable example is Gold/Silver where all the stock exchanges seem to be promoting their contracts amongst behind the same set of the participants without any major product differentiation and development.

3.7.2. Some of the exchanges have not been able to launch the contracts which were approved in the past, perhaps due to lack of good response from the market participants who are already trading on another exchange. Some of them want to launch the contract only with the help of tools like Liquidity Enhancement Scheme. This gives an appearance that the Exchange lacks vision or a tangible plan for product as well as market development in such commodities; and has come to a conclusion that liquidity can only be achieved from use of external support and not from product development.

3.8. It is also seen that while the work of development and research on a specific commodity is carried out by the exchange which has originally launched the contract, the other exchanges try to replicate the contract and based on the work done by first exchange, try to gain advantage on the strength of their resources, finance and dominance in the market. In these circumstances, it can be argued that there will be no incentive for the first exchange to conduct further research and development of the product and it will rather spend resources to prevent existing liquidity from flowing out of its contract.

4. The Concept:

4.1. SEBI has prepared a concept note on developing Exchange specific unique set of commodities for trading in commodity derivatives segment and reducing fragmentation in commodity derivatives markets. The main objectives of developing the concept are as follows:

4.1.1. to help every exchange to develop an exclusive set of un-fragmented liquid contracts on specific commodities;

4.1.2. to ensure that the concerned stock exchange develops all kinds of derivative contracts on a specific commodity exclusively;

4.1.3. to take all such steps which would help in bringing the desired liquidity so that eventually the benefits of the commodity derivatives markets can be passed on to all the stakeholders and value chain participants of those commodities;

4.1.4. to bring about comprehensive development and deepening of the Indian commodity derivatives markets; and

4.1.5. eventually, to help India to be in a position so as to be able to influence the global benchmark pricing of such commodities i.e. become price setter for such commodities.

4.2. Even though multiple exchanges having the option of launching competing contracts on the same commodity may be good for encouraging competition and providing choice to investors, a single exchange launching contracts on a specific commodity may have bigger impact locally as well as internationally. This may be more efficient and low cost in the long run.

5. Pros and Cons for the concept:

5.1. The Pros of the aforesaid concept are given below:

5.1.1. The objective of this concept of “One Commodity One Exchange” is to provide enough time say 3 to 5 years and resources to the stock exchanges to develop the commodity derivatives contract to such an extent wherein there is enough liquidity and depth in the contract and its futures price becomes the reference price for market players domestically as well as internationally.

5.1.2. The ingredients for a developed or mature derivative market are, viz:-adequate warehousing and storage, transport, communication technologies, standardisation in grades and standards of commodities traded etc. When stock exchanges have specific commodity contracts for trading exclusively on their platforms, they are likely to focus on developing the aforesaid aspects for that particular commodity. Such measures by all stock exchanges for their respective commodities would lead to development of commodity derivatives market in the long run.

5.1.3. The concept is not against the concept of universal exchanges and is not being developed to bring any restrictions. Rather, the concept has been developed to curb the practice of stock exchanges who merely copy the product launched by other stock exchanges and depend on shift of demand rather than building up new demand, by providing various incentives to the market participants. The concept aims at incentivising the stock exchange for undertaking research and to allow it sufficient time to develop and create liquidity in a specific contract.

5.1.4. With around 50 products remaining in the notified list of goods on which contracts can be launched, even if each stock exchange focuses on 2-3 products, we may develop 10-15 products in 2-3 years’ time. Such an effort by stock exchanges, if successful, may give the necessary forward push to the Indian commodity derivatives market in some of the commodities and may be successful in bringing the attention of the world to our markets.

5.1.5. The concept does not aim to thwart the competition amongst stock exchanges but rather provide new impetus to stock exchanges to develop market in their own chosen commodities for the benefit of the stakeholders rather than chasing the same set of stakeholders of a particular commodity.

5.1.6. If the concept is implemented, stock exchanges are likely to be encouraged to focus and develop new products on a specific commodity selected by them. It is expected that stock exchanges would undertake more comprehensive research and extensive study of the entire value chain before proposing for any fresh product for approval to SEBI. Such measure may lead to development of the commodity market as a whole.

5.2. There are certain cons as well underlying this concept, as indicated below:

5.2.1. The concept of “One Commodity Once Exchange” may create artificial barriers at the cost of other markets and value chain participants, leading to increased overall costs including trading, compliance, technology, etc.

5.2.2. Exchanges may block certain products for themselves but subsequently may not meaningfully develop them. An exchange, after making efforts for an initial period of 6 months to a year, may lose interest and decide not to invest further in that product and at the same time other exchanges may not able to consider the same product or even cannot launch contracts in its associated products.

5.2.3. Allowing only one exchange to offer products on a commodity for 3-5 years may go against market development as the designated exchange may fail to build liquidity, but at same time would continue to enjoy a monopoly status in the said commodity for so much period.

5.2.4. The main rational of having a universal exchange could be lost as participants will have to maintain active trading accounts in each of the stock exchanges in order to trade unique products offered by each exchange.

5.2.5. No new highly traded liquid commodities have come in to replace traditional liquid commodities in the last so many years.

CDAC’s Feedback:

The issue was debated in the Commodity Derivatives Advisory Committee (CDAC) of SEBI. CDAC has, inter-alia, recommended following:

6.1. Some products require consolidation of volume and building of liquidity which seem to be possible with the proposal on One Commodity One Exchange.

6.2. The commodities may be divided into “Broad” and “Narrow” categories based on a pre-defined criterion.

6.3. For “Broad” commodities there may not be any restriction.

6.4. For commodities qualifying as “Narrow”, SEBI may adopt the mechanism as proposed, with appropriate modifications, as required. This can be done in an objective, fair and transparent manner.

6.5. The protection or incentive given to a Stock Exchange should be clearly defined in terms of number of years and the process should be subject to performance of the contracts.

7. Joint Working Group:

7.1. A Joint Working Group comprising the five stock exchanges viz. BSE, ICEX, MCX, NCDEX and NSE was constituted to further explore and deliberate the above concept and came out with tangible recommendations.

7.2. The Joint Working Group held discussions and prepared a report on the subject matter. Based on the report of the working group, the following proposals are being made.

8. Proposal:

The salient features of the proposed concept are as under:

8.1. The concept may only be applicable for narrow agri-commodities. As per circular dated July 25, 2017, the agricultural commodities have been classified into three categories viz., sensitive, broad and narrow as below: –

8.1.1. Sensitive Commodity: An agricultural commodity shall be classified as a sensitive commodity if it:

8.1.1.1. is prone to frequent Government/External interventions. These interventions may be in the nature of stock limits, import/export restrictions or any other trade related barriers; or

8.1.1.2. has observed frequent instances of price manipulation in past five years of derivatives trading.

8.1.2. Broad Commodity: An agricultural commodity shall be classified as ‘Broad Commodity’ if it is not ‘Sensitive Commodity’ and satisfies following criteria;

8.1.2.1. Average deliverable supply for past five year is at least 10 lakh Metric Ton (MT) in quantitative term and is at least INR 5,000 crore in monetary term.

8.1.3. Narrow Commodity: An agricultural commodity which is not falling in either of the above two categories, viz ‘Sensitive’ or ‘Broad’ commodity, shall be classified as ‘Narrow Commodity’.

8.2. Commodities on which derivative contracts have already been launched by the exchanges for trading should continue as usual.

8.3. Exchanges can choose to ‘block’ a commodity with SEBI if that commodity is eligible for development as an exclusive commodity contract, prior to initiating in-depth research and large-scale market interactions, by obtaining an in-principal consent letter from SEBI.

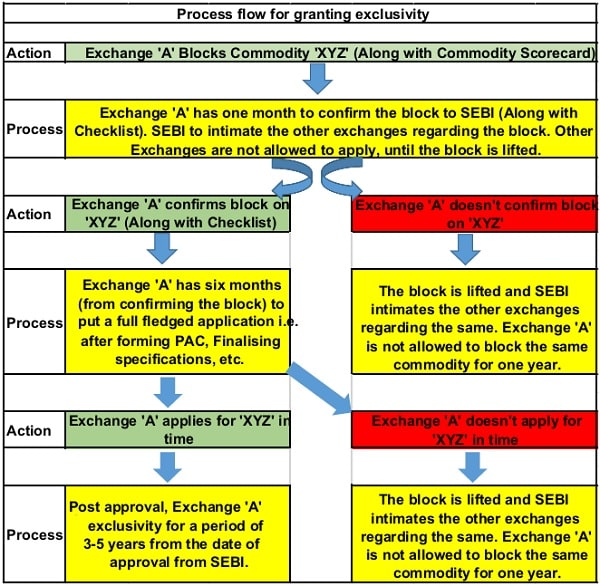

8.4. Post the blocking, the exchanges will get a period of one month to do detailed research and analysis of the proposed commodity and confirm the ‘block’ by sharing a feasibility report in a Checklist form as per the SEBI guidelines. All Exchanges shall be kept informed of any specific commodity which is blocked by any Exchange at any point in time. Blocking would be done based on First in First out (FIFO) method by SEBI.

8.5. If the exchange doesn’t ‘confirm’ to block within a month, then the block will be automatically released on that particular commodity.

8.6. While a commodity is ‘blocked’ by one Exchange, it cannot be blocked by another exchange. No more than two commodities can be ‘blocked’ or be in ‘Exclusive status’ for an exchange at any point in time. There should be a gap of at least one month between blocking of two separate commodities by the same exchange.

8.7. Application for product approval to regulator to be submitted within six months of confirming the ‘blocking’ of a commodity else, the block shall be automatically released. On failure, the exchange will not be allowed to apply for exclusivity on the same product for at least a period of one year, commencing from the missed due date. The other exchanges can apply to block the commodity once the block of the previous exchange is released.

8.8. The ‘Exclusivity’ status of a commodity will last for a period of around of 3-5 years from the date of SEBI approval. The exchange, if it so desires, can discontinue the exclusivity status before the period of 3-5 years. The exchange has to take a call on whether they want to remove the exclusivity from the product only after it becomes continuously liquid for 12 months.

8.9. Derivative contracts on new commodities would be traded only on a single stock exchange for a period of 3-5 years during which the said stock exchange would be allowed to launch all kind of permissible products i.e., futures, futures on options and options on goods etc.

Non-Agri Commodities: Narrow Vs Broad

8.10. It may not be appropriate to segregate Non–Agri commodities into ‘Narrow’ and ‘Broad’ for the purpose of adopting the ‘One Commodity One Exchange’ policy, as in the case of Agri commodities, based on annual physical market size. Instead, the Joint Working Group has suggested that the policy should be such that ‘One Commodity One Exchange’ should not be allowed in those non-agricultural commodities where:

8.10.1. India is not a major producer of the commodity, or

8.10.2. India is a price taker of international prices, or

8.10.3. significant correlation between Indian prices and international prices exist or

8.10.4. India is not excessively import dependent, etc

Process flow for granting exclusivity:

8.11. The steps involved in the proposed process of blocking and granting exclusivity on a commodity is depicted below:

9. Public Comments:

9.1. Public comments are invited on the proposal contained at Para 8 in this consultation paper. Comments/suggestions may kindly be provided in the format given below:

| Name of Entity/Person intermediary/ Organization | |||

| Sr. No. | Para No. of Paper | Suggestions* | Rationale |

| Para 8.1 to 8.11 | |||

| *Any other suggestions on the subject including on issues not covered in this paper, may also be given | |||

9.2. Comments/suggestions may be sent by email to cdmrd_ocoe@sebi.gov.in within one month from date of uploading of this consultation paper on the SEBI Website.

Mumbai

December 7, 2021

**********