With the onset of pandemic in 2019 and the second wave worsening the situation in India, the sudden or say over demanding requirement of covid-19 supplies like Medicines, medical grade oxygen, oxygen concentrators and cylinders (hereinafter called ‘such supplies’) have come into place in 2021. The government had been imposing taxes on all of such covid-19 supplies till 14th June 2021.

Till then the government did not reduce any rates and when states started procuring the same the demand for rate cuts/exemption for GST on such items have come into place.

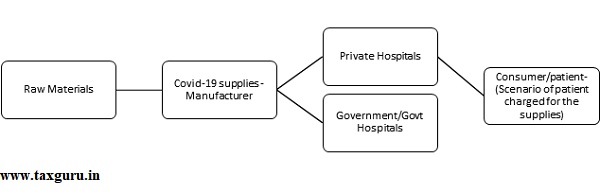

The process flow chart of the supplies is as below:

Raw Materials->Covid-19 supplies(Manufacturer)->Private /Govt Hospitals->End Consumer/Patient

(Scenario of patient charged for the supplies)

What has been done by the government on tax rates of such supplies?

The government did not want to completely exempt such supplies for the below reasons:

- There are various legs in this transaction and granting of exemption should be made taking into consideration every part of it till the end consumer.

- Suppose the exemption is provided at the leg between manufacturer and the hospitals,

- The manufacturer would have purchased all his raw materials by paying GST and that would form part of his ITC.

- If his final product is exempt, he would not be able to pass on the ITC paid on purchase and that would form part of accumulated tax credit in his books.

- The only means shall be refund which is not available for a manufacturer who is supplying exempt supplies, also in terms of S.17 he would be denied in availing the ITC

- Hence the ITC will form part of a cost to him which will be ultimately passed on as cost to every other person in the supply chain and would lead to double taxation and higher cost.

- Hence the option of exemption was not opted to be provided and a concessional reduction in the rate of taxes has been opted to be implemented vide (Notification No 05/2021- Central Tax Rate & Integrated Tax Rate)

Why would it still be eligible ITC as most of the supplies are partly exempted?

In terms of S.17, an ITC would be ineligible if it is used for effecting exempt supplies. As per S.2(47) of the CGST Act, Exempt supply has been defined to include supplies which is wholly exempt only. Hence partly exempt supplies would not qualify as exempt supplies and would be eligible for ITC availment.

Will it be eligible for refund- as the manufacturer most likely to have inverted tax structure?

In terms of S.54 of the CGST Act, refund shall be claimed only when the supplier makes zero rated supplies and if ITC is accumulated on account of higher tax rates on inputs than the output supplies. Further it only restricts refund for NIL rated and fully exempt supplies.

Therefore, since these supplies are not fully exempt, the ITC accumulated on account of inverted tax structure can be claimed as refund.

Conclusion:

This reduced rate of tax has therefore been a win-win move for the manufacturers, government as well as the end consumer with lower taxes, refund of ITC and with no double taxation.

Author Bio