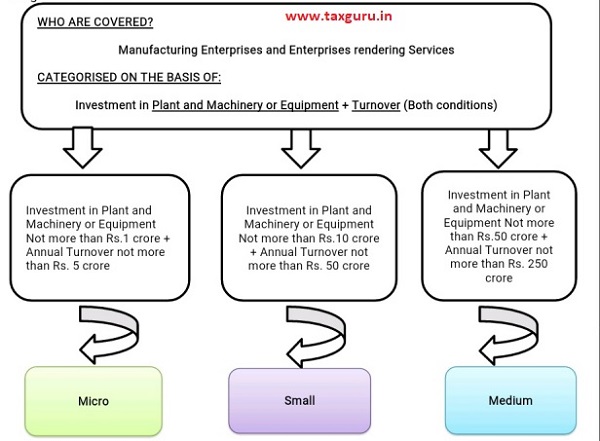

MSME UPDATES:

The Ministry of MSME through its Office Memorandum (O.M) dated 06th August 2020 has issued a clarification on Existing EM i.e. Enterpreneurs Memorandum Part —III-UAM.

The Ministry has drawn the attention of public on its previous notification dated 26th June 2020 and in its link has clarified certain points:

THE NEW UPDATES ARE AS FOLLOWS:

1. The EM Part II and UAMs issued till 3Clul June, 2020 shall remain valid only upto 31st march 2021.

2. The Existing UAM Holders may edit or amend their de-tails on the UAM Portal prior to the 31st Day of March 2021.

3. Those enterprises that have not entered theft Aadhar Number or Pan number details are advised to obtain UAM before 31.03.2021.

4. Existing UAM holders are advised to obtain Fresh Registration via Udyam Registration Portal by visting the official government page https://udyamregistration,qpv.ip.

The Registration Process is Free of cost and should be done through the Government portal.

Q. Now a question arises that will the already registered enterprises will be re classified as per the New Defination ?

Yes, ail enterprises registered till 30106/2020 will be re-classified in accordance with the notification dated 26.06.2020.

5. The existing UAM Holders or the new Entrepreneurs should provide the Value of plant and machinery or Equipment. For taking into account the definition of plant and machinery or Equipment the definition as per Income Tax Rules, 1962 shall be taken into account and it shall include all tangible assets (other than land and budding furniture and fittings).

6. Stating here under the most important point while considering the value of Plant and Machinery or Equipments as per the 0,M sub point OH) of point 5:

“The value of Plant and Machinery or Equipments for all purposes of the Notification N0. S.O. 2119(E) dated 26.6.2020 and for all the enterprises shall mean the Written Down Value (WDV) as at the end of the Financial Year as defined in the Income Tax Act and not the cost of acquisition or original price, which was applicable in the context of the earlier classification criteria.”

*****

Disclaimer The Article is my opinion and interpretation in respect of the Notifications/ Office memorandum issued by the Ministry. The article is prepared taking into account the Various circulars/ notification/clarificalions and general highlights issued by the MSME.The Article is based on the Relevant Provisions and as per the information existing at the time of the preparation. In no event I shall be liable for any direct and indirect result from this Article. This is only a knowledge sharing initiative.

Author Bio