CBDT amends Rule 10CB relating to interest income computation for secondary adjustments (Notification No. 76/2019/ F.No.370142/12/2017-TPL)

Introduction

The Finance Act, 2017 inserted Section 92CE in the Income-tax Act, 1961 (the Act) w.e.f. 1 April, 2018 to provide for secondary adjustment, where, as a result of primary adjustment to the transfer price, there is an increase in the total income or reduction in the loss, as the case may be, of the assessee, the excess money which is available with its associated enterprise, if not repatriated to India within the time as may be prescribed, shall be deemed to be an advance made by the assessee to such associated enterprise and the interest on such advance, shall be computed in such manner as may be prescribed.

The Central Board of Direct Taxes (CBDT), vide a notification1 dated 15 June, 2017, introduced Rule 10CB in the Income-tax Rules (the Rules), 1962, to provide for computation mechanism of notional income pursuant to these secondary adjustments.

CBDT has now, vide a notification2 dated 30 September 2019, amended Rule 10CB of the Rules, (the Rules), which provides for computation of interest income pursuant to secondary adjustments. The said notification is effective from the date of the publication in the Official Gazette, that is, with immediate effect and will be applicable from AY 20 19-20 and onwards.

1. Time limit for the repatriation of money:

In order to provide for a uniform treatment in respect of various situations of primary adjustments as per section 92CE(1), the time limit for repatriation pursuant to secondary adjustment is set as on or before ninety days, in respect of various scenarios. The CBDT has amended Rule 10CB (1) (iii) and Rule 10CB (1) (v) vide the notification.

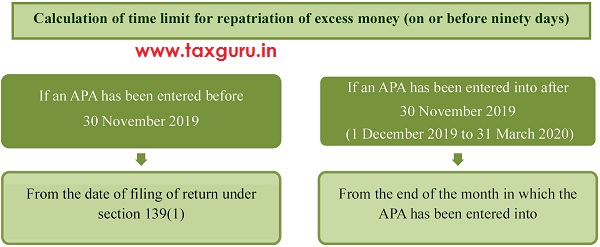

– Rule 10CB(1) (iii) covers a case, where primary adjustment to transfer price is determined by an advance pricing agreement (APA) entered into by the assessee under section 92CC of the Act, in respect of a previous year. The same is amended to provide the following:

| As per old sub-rule (iii) | As per new sub-rule (iii) |

| The time limit for repatriation of excess money shall be on or before ninety days: | The time limit for repatriation of excess money or part thereof shall be on or before ninety days: |

| “from the due date of filing of return under sub-section (1) of section 139 of the Act ……” | (a) from the date of filing of return under sub-section (1) of section 139 of the Act if the APA has been entered into on or before the due date of filing of return for the relevant previous year

(b) from the end of the month in which the APA has been entered into if the said agreement has been entered into after the due date of filing of return for the relevant previous year |

For the purposes of the below illustration, 30 November 2019 has been taken as due date of filing return of income under section 139(1):

– Rule 10CB (1) (v) is applicable in the case of an agreement made under the mutual agreement procedure under a Double Taxation Avoidance Agreement entered into under section 90 or 90A of the Act [Mutual Agreement Procedure (MAP)]. The same is amended to provide the following:

| As per old sub-rule (v) | As per new sub-rule (v) |

| The time limit for repatriation of excess money shall be on or before ninety days: | The time limit for repatriation of excess money or part thereof shall be on or before ninety days: |

| “from the due date of filing of return under sub-section (1) section 139 of the Act ..” | “from the date of giving effect by the Assessing Officer under rule 44H to the resolution arrived at under MAP….” |

2. Rule 10CB(2) provides computation of the rate of interest to be charged on the excess money which is not repatriated into India within the prescribed time limit of 90 days.

3. A new sub-rule (3) has been inserted [Rule 10CB(3)], which provides the chargeability of interest, in cases where excess money or part thereof is not repatriated, within the prescribed time limit of 90 days:

| Sub-rule | Situation | Where a primary adjustment to transfer price |

Time limit of imputation of interest |

| 10CB(3)(a) | 10CB(1)(i) | Suo motu by the assessee in his return of income | From the due date of filing of return under section 139(1) of the Act |

| 10CB(1)(iii)(a) | Determined by an APA entered into by the taxpayer under Section 92CC – from the date of filing of return under sub-section (1) of section 139 of the Act if the APA has been entered into on or before the due date of filing of return for the relevant previous year | ||

| 10CB(1)(iv) | Made as per the safe harbour rules under Section 92CB | ||

| 10CB(3)(b) | 10CB(1)(ii) | Made by the Assessing Officer (AO) and has been accepted by the assessee | From the date of the order of AO or the appellate authority |

| 10CB(3)(c) | 10CB(1)(iii)(b) | Determined by an APA entered into by the taxpayer under Section 92CC – from the end of the month in which the APA has been entered into if the said agreement has been entered into after the due date of filing of return for the relevant previous year | From the end of the month in which the APA has been entered into by the assessee |

| 10CB(3)(d) | 10CB(1)(v) | Resulted from a MAP resolution under Section 90 or Section 90A | From the date of giving effect by the AO under rule 44H to the resolution arrived at under MAP |

4. The term ‘international transaction’ shall have the same meaning as provided in section 92B of the Act.

5. The rate of exchange for the calculation of the value in rupees of the international transaction denominated in foreign currency shall be the telegraphic transfer buying rate of such currency on the last day of the previous year in which such international transaction was undertaken and the “teleO aJhicVt aLFfe VbuyinOV ate” shall have the same meaning as provided in Explanation to Rule 26 of the Rules.

Our Comments:

The Notification states that the amended Rules would apply with immediate effect. This could lead to litigation, as there is a substantial change in the methodology of computing the time period from when the notional interest would start, as compared to the Rules before this amendment. Thus, whether the amended Rules would be effective from Assessment Year 2019-20 or Assessment Year 2020-21 would be the point of debate.

Note