Introduction- India as a developing economy is in dire need of the funds to boost its development. Tax is one of the major sources of Indian government revenue. Direct Taxes are contributing more than the Indirect taxes. To secure the Direct Tax collection and to curb its avoidance; the GAAR was first introduced in the Direct Taxes Code Bill, 2009 which was later modified in Direct Taxes Code Bill, 2010. First Inclusion of GAAR in Income Tax Act was made by Finance Act 2012. Subsequently a new Chapter X-A was inserted by the Finance Act 2013 by the name of General Anti – Avoidance Rules which will be applicable with effect from 1st April 2016. The old Chapter X-A which was having differences as compared to newer one, was omitted up by Finance Act 2013 in lieu of new chapter. This chapter consists of sections starting from 95 to 102 having various definitions, consequences of entering the Impermissible Avoidance Arrangement and reference to the guidelines in section 101 inserted by IT (Seventeenth Amendment) Rules, 2013, applicable with effect from 1st April 2016. As a corporate professional one must have a clear understanding on this heated topic as this is going to applicable with effect from 1st April 2016. Why GAAR?

Tax avoidance is harming the economy in the same way as tax evasion does. Thus it is equally necessary to conquer tax avoidance. Giving less weight to substance over form may lead to tax avoidance. Hence main emphasis of GAAR is that substance must be given preference over the form along with the commercial substance. Tax avoidance can be done by routing transactions from various channels; some of these routes are curbed by judicial pronouncements and amendments in Act. However, some of the loopholes and lacuna are exists and its advantage is taken by the tax avoiders that’s why the steps have been taken by the government to diminish the avoidance of tax to an acceptable level by introducing GAAR. It empower the income tax authority to deny any kind of tax benefit to the assessee which falls in the ambit of Chapter X-A. This concept is new to India in structured form but not in substance as prior to this India was mitigating tax avoidance through the tool of judicial pronouncements which in another term known as SAAR (Specific Anti – Avoidance Rules). Many developed and matured economies have already implemented GAAR in its required form but now it is time for developing economy to implement the same. In view of the above, it is necessary and desirable to introduce general anti-avoidance rules which will serve as a deterrent against tax avoidance. However, an assessee will not be barred from taking the advantage of bona fide tax mitigation and planning.

TAX AVOIDANCE vs TAX EVASION vs TAX MITIGATION vs TAX PLANNING

Since some of the terms in the heading of this para are used in relation to GAAR repeatedly, hence it is important to explain these terms with the treatment for the same:-

1. TAX AVOIDANCE – Legal or bona fide steps taken by the assessee to reduce the tax burden is referred as the tax avoidance. In tax avoidance commercial substance is ignored or given less weights. This can be done by routing transactions through various channels or by changing the form of transactions which ultimately result in less tax liability. This is taken care by the GAAR introduced in Income tax Laws.

Example of Tax Avoidance – Company A has taxable capital gains. Company A borrows from Company B and uses that borrowed money for buying new share of its 100% subsidiary X having FMV Rs. 100/share at Rs. 500/share. X transfer money in the form of loan to the 100% subsidiary of B that is Y and subsequently A sold the purchased shares of its subsidiary at Rs. 100/share that is at FMV and creates a fictional short term capital loss of Rs. 400/ share which it will be setting off against its other profits as per chapter of setting off.

Now this will come under the lens of GAAR as the above transaction is lacking in commercial expediency even though the routing of transaction is bona fide.

2. TAX EVASION – An illegal practice where an assessee intentionally avoids paying his/her/its true tax liability. It is clearly distinct from the tax avoidance as this is an illegal practice. Specific measures have been taken in law to prevent this as a result of which those caught evading taxes are generally subject to criminal charges and substantial penalties.

3. TAX MITIGATION – “Tax Mitigation” is a situation where the taxpayer takes advantage of a fiscal incentive afforded to him by the tax legislation by actually submitting to the conditions and economic consequences that the particular tax legislation entails. Tax Mitigation is not covered by GAAR.

Example of Tax Mitigation – A good example of tax mitigation is the setting up of a business undertaking by a tax payer in a specified area such as Special Economic Zone (SEZ) and taking the benefit to tax exemptions and deductions.

4. TAX PLANNING – Tax Planning is defined as “arrangement of a person’s business and / or private affairs in order to minimize tax liability”. This term is similar to the term tax mitigation. This is also not covered by the GAAR.

ARRANGEMENT

As per subsection 1 of section 102 arrangement means any step in, or a part or whole of, any transaction, operation, scheme, agreement or understanding, whether enforceable or not, and includes the alienation of any property in such transaction, operation, scheme, agreement or understanding.

APPLICABILITY OF GAAR

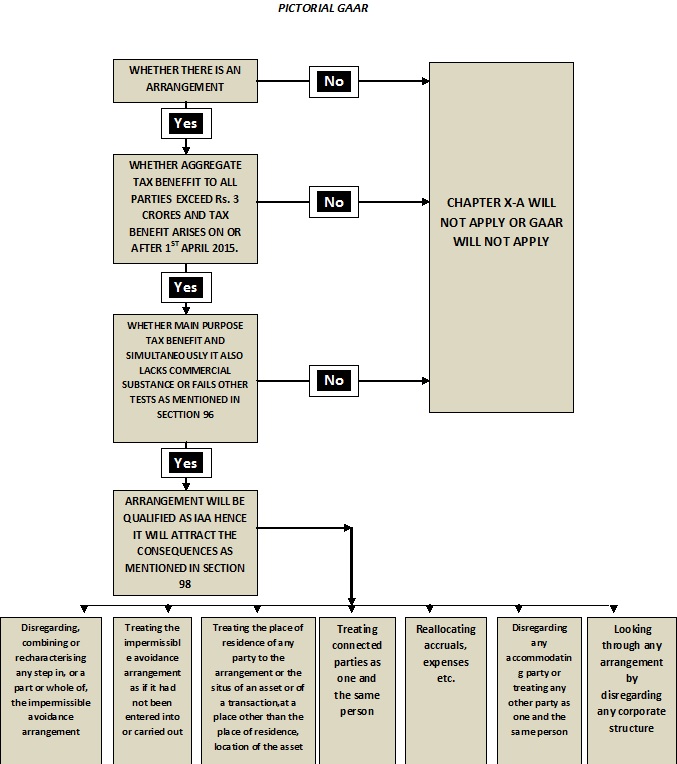

The provisions of GAAR will be applied on all the assessee irrespective of the residential status of the assessee. By virtue of Section 101 read with Rule 10U, provision of Chapter X-A will apply if an arrangement where the tax benefit in the relevant assessment year arising, in aggregate, to all the parties to the arrangement exceed a sum of Rs. 3 crore. Then said arrangement will come under purview of GAAR and then by virtue of section 96 its impermissibility will be evaluated, which defines it and if it is an Impermissible Avoidance Agreement (herein after referred as IAA) then by virtue of section 98, assessee has to bear the consequences as mentioned in said section.

By dint of Rule 10U GAAR will not apply to the arrangements as follows:

1. A person, being a non-resident, in relation to investment made by him by way of offshore derivative instruments or otherwise, directly or indirectly, in a Foreign Institutional Investor.

2. Any income accruing or arising to, or deemed to accrue or arise to, or received or deemed to be received by, any person from transfer of investments made before the 30th day of August, 2010 by such person. However, if the tax benefit from IAA is derived on or after 1st April 2015 irrespective of the date of arrangement then the provisions of GAAR will apply.

3. Foreign Institutional Investor,—

(i) who is an assessee under the Act;

(ii) who has not taken benefit of an agreement referred to in section 90 or section 90A as the case may be; and

(iii) who has invested in listed securities, or unlisted securities, with the prior permission of the competent authority, in accordance with the Securities and Exchange Board of India (Foreign Institutional Investor) Regulations, 1995 and such other regulations as may be applicable, in relation to such investments;

HOW TO DECIDE IMPERMISSIBILITY AND AVOIDANCE AN ARRANGEMENT

By dint of section 96, arrangements to be declared as impermissible if main purpose of entering the arrangement is tax benefit and which also actually or deemed to lacks commercial substance, misuse or abuse the provisions of the Act, or arrangement are not ordinarily entered into for bona fide purposes. Even if a part of the arrangement resulting into tax benefit then it will be presumed that the main purpose is tax benefit. Onus of proving that the arrangement is an IAA is on the revenue.

If main purpose of entering an arrangement is tax benefit but it’s not lacking commercial substance, then said arrangement cannot be an IAA and if main purpose of entering an arrangement is not the tax benefit but its lacking commercial substance, then also said arrangement cannot be an IAA. Thus, an arrangement to qualify as an IAA must have to fulfill both the above criteria.

CONSEQUENCES OF AN IAA

Main consequence of entering an IAA is the denial of Tax Benefit but not limited to denial only. Section 98 of the Act deals with it which inter-alia provides as follows:

If an arrangement is declared to be an impermissible avoidance arrangement, then, the consequences, in relation to tax, of the arrangement, including denial of tax benefit or a benefit under a tax treaty, shall be determined, in such manner as is deemed appropriate, in the circumstances of the case, including by way of but not limited to the following, namely:—

(a) Disregarding, combining or recharacterising any step in, or a part or whole of, the impermissible avoidance arrangement;

(b) Treating the impermissible avoidance arrangement as if it had not been entered into or carried out;

(c) Disregarding any accommodating party or treating any accommodating party and any other party as one and the same person;

(d) Deeming persons who are connected persons in relation to each other to be one and the same person for the purposes of determining tax treatment of any amount;

(e) Reallocating amongst the parties to the arrangement—

1. any accrual, or receipt, of a capital nature or revenue nature; or

2. any expenditure, deduction, relief or rebate;

(f) Treating—

(i) the place of residence of any party to the arrangement; or

(ii) the situs of an asset or of a transaction,

at a place other than the place of residence, location of the asset or location of the transaction as provided under the arrangement; or

(g) Considering or looking through any arrangement by disregarding any corporate structure.

CA Hemant Sharma – Membership No. 535518

CA Hemant Sharma – Membership No. 535518

For feedback and queries please feel free to mail @ hemant.sharma53@outlook.com

Thanks to all other professional colleagues for your positive appraisal.

Sorry for late reply

The chapter of GAAR will also cover Transfer Pricing cases. Provisions of Chapter XA by virtue of section 95 overrules whole Act. If any arrangement Either of TP or any other qualifies to be an Impermissible Avoidance Agreement then definitely GAAR will be invoked on that TP transaction. It is an supplementary measure to curb avoidance of tax in addition with the provisions contained in Chapter X itself.

Does it cover transfer pricing or not? IF yes, then justify.

Good work Hemant Ji. Thanks for your analysis.

Very much informative….nuances of the subject matter have been explained…Thank you very much

Thanks Hemant.

you have done marvellous job in demystifying the GAAR concept.