“Preventive action is better than corrective action”

In terms of provisions of Companies Act, 2013, Government is supposed to constitute National Financial Reporting Authority (NFRA) soon.

WHY NFRA

The objectives of National Financial Reporting Authority inter alia shall be as follows:

1. Make recommendations on formulation of accounting and auditing policies and standards for adoption by companies, class of companies or their auditors;

2. Monitor and enforce the compliance with accounting standards, monitor and enforce the compliance with auditing standards;

3. Oversee the quality of service of professionals associated with ensuring compliance with such standards and suggest measures required for improvement in quality of service, and

4. Perform such other functions as may be prescribed in relation to aforementioned objectives.

If we analyze the basic objects of NFRA, it seems that more or less these objects are the objects which had been successfully achieved by ICAI since many years. If we talk about formulation and recommendation of accounting standards then since many years ICAI is doing the same Job and ICAI is specialized too in this field. Later on Company Law Board, CBDT all has started to the same job while they are not supposed to be specialized for the same.

If we talk about monitoring of compliance accounting standard as well as auditing standard, more or less majority of CA firms are getting complied with it and they are peer reviewed for the same too. In order to ensure this object’s achievement, what is needed is just tightening the norms of peer review.

Even, if we talk about quality of service by associated professionals, it was up to the mark and very good a decade back. Now a day’s quality is being compromised in some cases i.e. in majority of cases quality of Indian firm’s are still better than desired standards. My this view is based on the fact that if we see the black listing by RBI/SEBI and a like controlling agencies then we will find that multinational firms are being banned in more cases than Indian firms. And it is known fact that in-spite of the high level connections and large resources Multinational audit firms were banned which proves the gravity and sensitivity of compromises they have made while performing the attestation function.

When we analyze the reasons behind decrease in quality of assurance services, specifically in banking sector, in last one decade, I could conclude two reasons:

1. Competition with BIG4 and other Multinational audit firms: During the last two decades, BIG4 audit firms are spreading their wings and by hook or crook they have procured the assurance assignments either via using their political connections or via creating pressure through foreign direct investors. This has created scope for compromises in order to survive in the competitive environment for Indian audit firms.

2. Independency of auditor is hammered or hampered whatever you call it. Few years back, autonomy was given to banks by RBI for the selection of auditors. On the one side this autonomy to bankers for selecting their auditors and on the other side heavy competition with largely resourced multinational audit firms, both has given power to auditee (Made is buyers choice) to ask for compromises while performing audit function or other choice of audit firm was with them so it has boosted compromising nature of few firms but not all.

Now, we come to NFRA again, from the above discussion, it is clear that quality of assurance services has got hampered, so government has planned to create stick in the form of NFRA with which a fear is supposed to be created to provide quality services. Now here what government has done, they are trying to start again a new post-mortem activity i.e. going to take a corrective action rather than going to route cause and curing the same. Route cause behind the quality compromises is the lack of independency to Auditors. So I my view, rather than taking corrective measures, government should ensure auditors independence so that quality of services will improve automatically.

In order to ensure independency of auditors, I suggest overall change in the auditor’s appointment procedure so that no one should be able to influence auditors. In today’s modern technological environment, this can be achieved by creating Automated Auditor Appointment Agency (4A). By Creating 4A, I believe that the object of ensuring quality of services and compliance can be achieved.

Automated Auditor Appointment Agency (4A).

Constitution of Agency: Agency should comprise 4-6 members nominated by Government and appointed by president of India. Members of Agency may be:

1. One retired Industrialist with undisputed image like Mr. RATAN TATA/NANDAN NELKANI

2. President of ICAI

3. Chairmen of SEBI

4. Deputy Governor/Governor of RBI

5. Vice Chairmen of CLB

6. Chairmen of NABARD.

7. Chairmen of CBDT

8. Chairmen of GST Council

Function/responsibility of Agency Members:

1. To finalize and approve the criteria/norms for selection of auditors along with remuneration looking to nature of audit assignment.

2. To finalize and approve the reporting norms for auditor

3. To finalize and approve performance rating points and criteria for auditors.

4. To Review every third year the above norms and amend if needed.

Auditor’s Selection process:

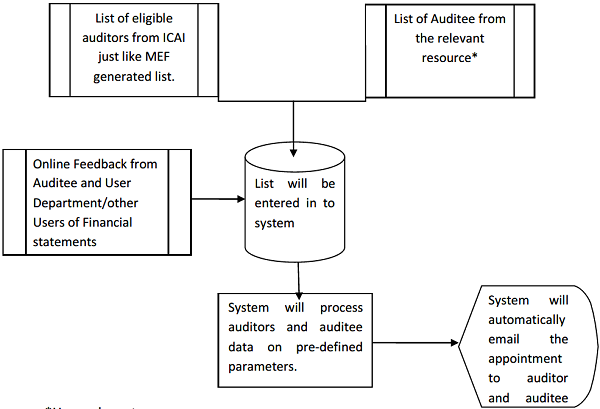

Auditors should be selected in automated process. To automate the process, software can be developed fixing the criteria as approved by the agency as selection process. No manual intervention should be allowed while selecting the auditors as all parameter should be prefixed. Every appointment through this selection process should have a control number so that their auditors JOB can be reviewed and ranked easily as well as their experience’s record can be kept in software only. How it will function can be depicted as follows:

*Here relevant resource means:

1. In Reference to Companies: ROC

2. In Reference to Direct Tax Assessee: CBDT (For assessee having turnover more than specified Sum)

3. In Reference to indirect Tax Assessee: CBEC (For assessee having turnover more than specified Sum)

4. In Reference to Societies and co-operative societies: Respective registrars.

5. Other Cases: Auditee firm themselves, if they feel about crossing turnover limits or otherwise.

Icai peer review board is a puke

Throw it out soon

I agree with the author for 4A

Consider the housing societies in Mumbai. As per govt rules, they should get their accounts audited. The societies select an auditor, close to them and within their budget.

How will 4A help them?

Very good idea indeed. I think reason for compromise in quality, apart from monopoly of few, could be the considerable time required for a fresh practitioner to establish himself. I mean, in his desire to retain whatever audit work he has got, he may possibly be inclined to adopt a softer attitude towards deviations/violations in the name of being practical. I am damn sure that the 4A system of allotment of all audit assignments will make him free from this business like worries and render required assurance to all the SMEs/upcoming CAs which will allow them to better concentrate on quality of audit.

Since inception Auditors Independence is never established;.because of From appointment to payment of remuneration decided by the owner,Big 4 & other bigs influenced to seek appointments.

Dear Sir,

This is a good idea to have an Independent AUDIT authority which may have the powers to collect and siege the RELEVANT documents in respect of all financial irregularities / Frauds etc perpetuated by ANY NATWARLAL or Institutions/ COMPANIES OR FIRMS .

.Beside there should be some representative from THE COMPTROLLER GENERAL OF INDIA–THE SUPREME AUDIT AUTHORITY— ON the board of Such AUTHORITY ie 4 A

Very Goods Article.

Not only was the article informative but it also talks of a road map….

Kudos

Well said jhamb sir. And some process abt new chartered accountats that are aspiring big shd be associated with ethical auditors so tht thy can value and learn.