Agenda

Design of GST

Main features of GST Law

Administration and IT Network

Benefits of GST and Way Forward

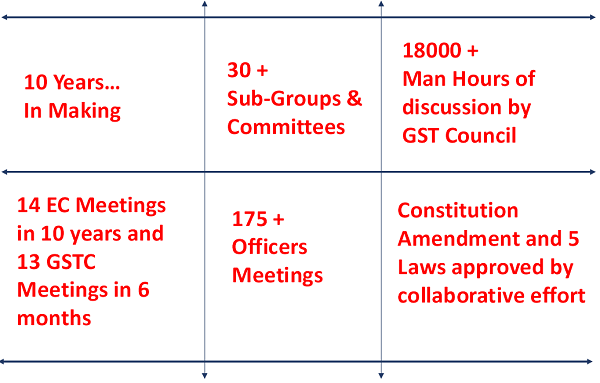

The Effort and Work Done

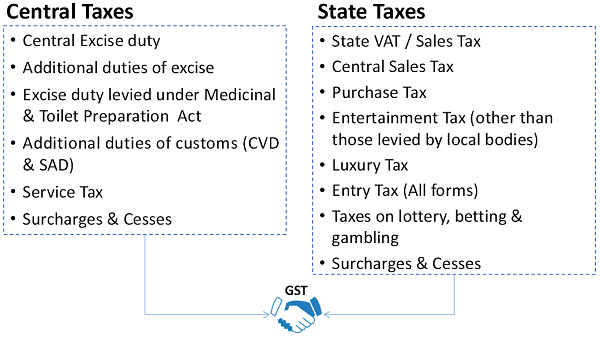

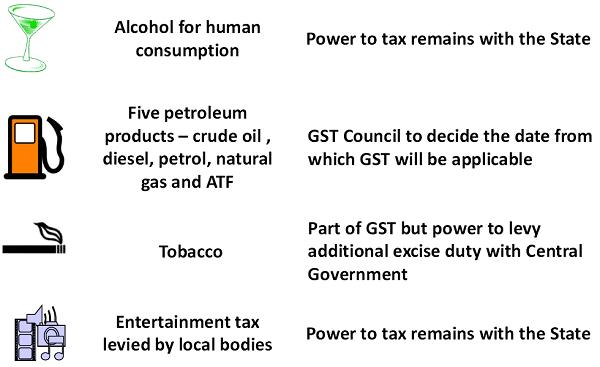

Existing Indirect Tax Structure in India

Constitution amended to provide concurrent powers to both Centre & States to levy GST (Centre to tax sale of goods and States to tax provision of services)

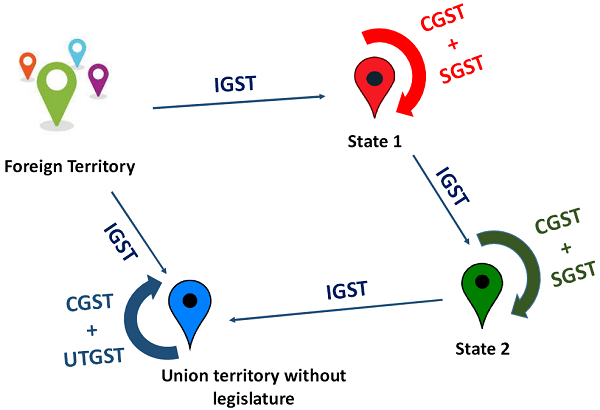

Understanding CGST, SGST, UTGST & IGST

Features of Constitution Amendment Act

GST Council – Constitution

♦ Chairperson – Union FM

♦ Vice Chairperson – to be chosen amongst the Ministers of State Government

♦ Members – MOS (Finance) and all Ministers of Finance / Taxation of each State

♦ Quorum is 50% of total members

♦ States – 2/3 weightage and Centre – 1/3 weightage

♦ Decision by 75% majority

♦ Council to make recommendations on everything related to GST including laws, rules and rates etc.

GST Council – Decisions

◊ Threshold limit for exemption to be Rs. 20 lac (Rs. 10 lac for special category States)

◊ Compounding threshold limit to be Rs. 50 lac with –

| Categories | Tax Rate |

| Traders | 1% |

| Manufacturers | 2% |

| Restaurants | 5% |

◊ Government may convert existing Area based exemption schemes into reimbursement based scheme

◊ Four tax rates namely 5%, 12%, 18% and 28%

◊ Some goods and services would be exempt

◊ Separate tax rate for precious metals

◊ Cess over the peak rate of 28% on specified luxury and sin goods

◊ To ensure single interface – all administrative control over

♦ 90% of taxpayers having turnover below Rs. 1.5 cr would vest with State tax administration

♦ 10% of taxpayers having turnover below of Rs. 1.5 cr. would vest with Central tax administration

♦ taxpayers having turnover above Rs. 1.5 cr. would be divided equally between Central and State tax administration

◊ Revenue of all taxes subsumed in GST by the State for 2015-16 as the base

◊ Assumption of 14% Annual Growth Rate

◊ Compensation to be provided through Cess

◊ Cess only on few specified luxury and demerit goods

Main Features of the GST Act

◊ All transactions and processes only through electronic mode – Non-intrusive administration

◊ PAN Based Registration

◊ Registration only if turnover more than Rs. 20 lac

◊ Option of Voluntary Registration

◊ Deemed Registration in three working days

◊ Input Tax Credit available on taxes paid on all procurements (except few specified items)

◊ Credit available to recipient only if invoice is matched – Helps fight huge evasion of taxes

◊ Set of auto-populated Monthly returns and Annual Return

◊ Composition taxpayers to file Quarterly returns

◊ Automatic generation of returns

◊ GST Practitioners for assisting filing of returns

◊ GSTN and GST Suvidha Providers (GSPs) to provide technology based assistance

◊ Tax can be deposited by internet banking, NEFT / RTGS, Debit/ credit card and over the counter

◊ Concept of TDS for certain specified categories

◊ Concept of TCS for E-Commerce Companies

◊ Refund to be granted within 60 days

◊ Provisional release of 90% refund to exporters within 7 days

◊ Interest payable if refund not sanctioned in time

◊ Refund to be directly credited to bank accounts

◊ Comprehensive transitional provisions for smooth transition of existing tax payers to GST regime

◊ Special procedures for job work

◊ System of GST Compliance Rating

◊ Anti-Profiteering provision

GST Network (GSTN)

◊ A section 25 private limited company with Strategic Control with the Government

◊ To function as a Common Pass-through portal for taxpayers-

◊ submit registration application

◊ file returns

◊ make tax payments

◊ To develop back end modules for 25 States (MODEL –II)

◊ Infosys appointed as Managed Service Provider (MSP)

◊ 34 GST Suvidha Providers (GSPs) appointed

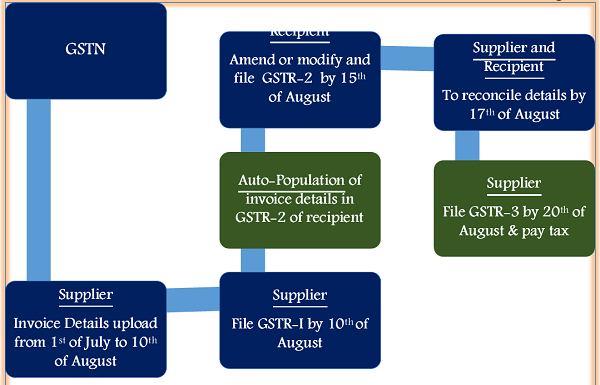

Return Process (Example : Return for July 2017)

Role of CBEC (Now CBIC)

◊ Role in Policy making: Drafting of GST Law, Rules & Procedures – CGST, UTGST & IGST Law

◊ Assessment, Audit, Anti-evasion & enforcement under CGST, UTGST & IGST Law

◊ Levy & collection of Central Excise duty on products outside GST – Petroleum Products & Tobacco

◊ Levy & collection of Customs duties

◊ Developing linkages of CBEC – GST System with GSTN

◊ Training of officials of both Centre & States

◊ Outreach programs for Trade and Industry

Benefits of GST

Way Forward

◊ SGST law to be passed by the State Legislatures

◊ GST Council to fit tax rates to various categories of Goods or Services

◊ Sector Wise guidance notes to be prepared

◊ Migration and handholding of existing tax payers

◊ Outreach program for trade and industry

◊ Change Management

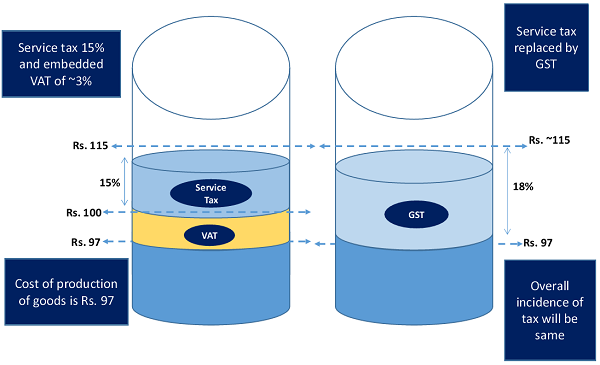

Reduction in Price of Goods under GST

Reduction in Price of Goods under GST