The provisions relating to Point of Taxation (POT) are very essential element of any law as it fixes the point when the liability to pay tax arises.

If the provisions relating to POT are not there then assessee always wants to defer the liability of tax and on contrary the government always want that the assessee should discharge the liability at earliest. So to mitigate this issue or contradiction the provisions relating to POT are also framed in GST.

The liability to pay tax on supply of Goods or Services or Both shall arise at TIME OF SUPPLY of GOODS or SERVICES.

Now, the question arises that what is the Time of Supply of Goods or Services before understanding the GST scenario of Point of Taxation (POT) let’s see the PRESENT SCENARIO of POT.

| S.No. | Law | Point of Taxation (POT) |

| 1 | Excise | Incidence of Excise duty arises on manufacture of goods and liability to pay Excise duty arises at the time of removal of excisable goods from factory |

| 2 | Service Tax | Payment of tax is, earliest of following

(1) Receipt of payment or (2) issue of invoice, if invoice raised within stipulated time period otherwise, completion of service |

| 3 | VAT/CST | Incidence of Vat arises on transfer of property in goods including deemed sale in terms of Article 366(29A) of the Constitution. |

TIME OF SUPPLY IN GST SCENARIO:-

For ascertaining time of supply for goods and services, detailed provisions have been prescribed under Chapter-IV of CGST, Act which are as under:

Section 12: Time of Supply of Goods

Section 13: Time of Supply of Services

Section 14: Change in rate of tax in respect of supply of goods or services

Now Let’s discuss in detail:

Section 12 Time of supply of Goods

S.12(1): Enabling Section:-

♦ The liability to pay tax on goods

♦ shall arise

♦ at the time of supply,

♦ as determined in accordance with the provisions of this section.

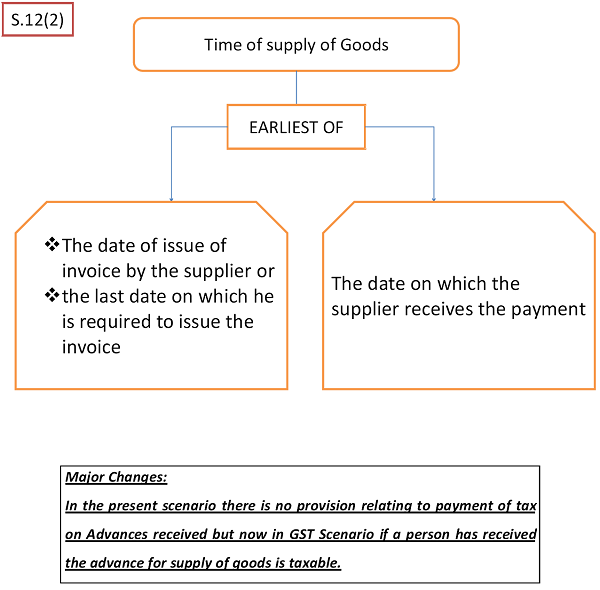

S.12(2): The time of supply of goods shall be the earlier of the following dates, namely:—

(a) the date of issue of invoice by the supplier or the last date on which he is required, under sub-section (1) of section 31, to issue the invoice with respect to the supply; or

(b) the date on which the supplier receives the payment with respect to the supply:

Illustration:

Suppose Mr. A raise bill for goods Rs. 1100/- to B and B paid Rs. 1500/- to A.

In this case A received an advance of Rs 400/- then the time of supply in respect of advance of Rs 400/- will be at the option of Mr. A will be the date of issue of invoice in respect of such excess amount.

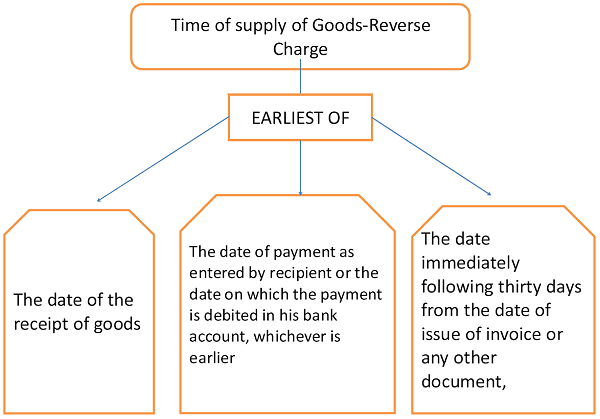

12(3) Time of Supply goods in Reverse charge:-

In case of supplies in respect of which tax is paid or liable to be paid on reverse charge basis, the time of supply shall be the earliest of the following dates, namely:—

(a) the date of the receipt of goods; or

(b) the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier; or

(c) the date immediately following thirty days from the date of issue of invoice or any other document, by whatever name called, in lieu thereof by the supplier:

√ Provided that where it is not possible to determine

√ the time of supply of goods in reverse charge basis as above

√ the time of supply

√ shall be the date of entry in the books of account

√ of the recipient of supply.

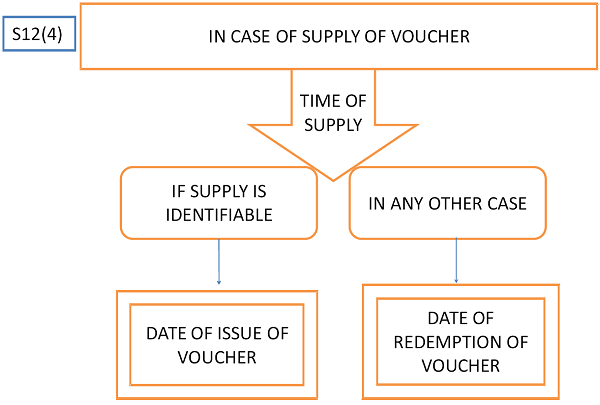

S-12(4) Time of Supply of voucher :-

In case of supply of vouchers by a supplier, the time of supply shall be—

(a) the date of issue of voucher, if the supply is identifiable at that point; or

(b) the date of redemption of voucher, in all other cases.

Illustration:

Suppose Pizza Hut has given vouchers to Raymond and then Raymond issues these vouchers to his staff.

Now, If the value of the voucher is identifiable then for Pizza Hut the Time of Supply will be the date of issue of Voucher and if the value is not identifiable then the Time of supply will be the Date of redemption of Voucher.

12 (5) Residual Provision:-

Where it is not possible to determine the time of supply under sub-section (2), (3) or (4), the time of supply shall––

(a) in a case where a periodical return has to be filed, be the date on which such return is to be filed;

or

(b) in any other case, be the date on which the tax is paid.

12 (6) The time of supply

♦ for addition in the value of supply by way of

♦ interest,

♦ late fee or

♦ penalty for delayed payment of any consideration

♦ shall be the date on which the supplier receives such addition in value.

Major Changes:

♦ In the present scenario there is no provision relating to taxation of Interest, Late Fees or penalty for delayed payment but now in GST Scenario the same is taxable.

S.13 TIME OF SUPPLY OF SERVICES

S.13(1) Enabling Section:-

♦ The liability to pay tax on services

♦ shall arise

♦ at the time of supply,

♦ as determined in accordance with the provisions of this section.

13 (2) The time of supply of services shall be the earliest of the following dates, namely:—

(a) the date of issue of invoice by the supplier, if the invoice is issued within the period prescribed under sub-section (2) of section 31 or the date of receipt of payment, whichever is earlier; or

(b) the date of provision of service, if the invoice is not issued within the period prescribed under sub-section (2) of section 31 or the date of receipt of payment, whichever is earlier; or

(c) the date on which the recipient shows the receipt of services in his books of account, in a case where the provisions of clause (a) or clause (b) do not apply:

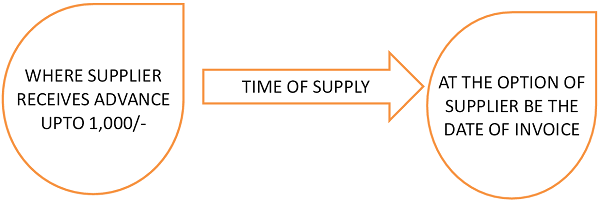

√ Provided that where the supplier of taxable service receives an amount upto onethousand rupees in excess of the amount indicated in the tax invoice, the time ofsupply to the extent of such excess amount shall, at the option of the said supplier, bethe date of issue of invoice relating to such excess amount

Illustration:

Suppose A raise bill for services of Rs. 1100/- to B and B paid Rs. 1500/- to A.

In this case A received an advance of Rs 400/- then the time of supply in respect of advance of Rs 400/- will be at the option of Mr A will be the date of issue of invoice in respect of such excess amount.

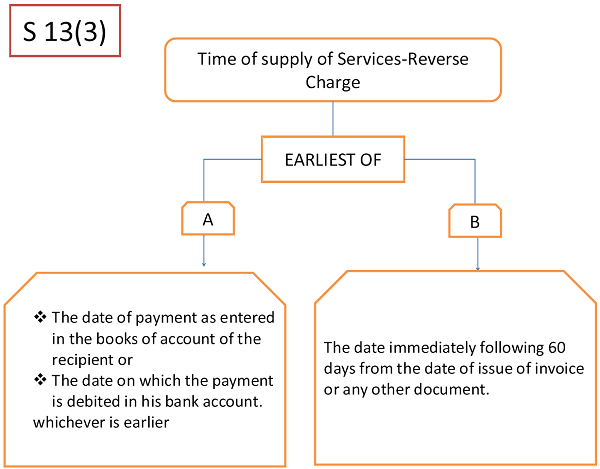

13(3) Time of Supply of services –Reverse Charge

In case of supplies in respect of which tax is paid or liable to be paid on reverse charge basis, the time of supply shall be the earlier of the following dates, namely:–

(a) the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier; or

(b) the date immediately following sixty days from the date of issue of invoice or any other document, by whatever name called, in lieu thereof by the supplier:

√ Provided that where it is not possible to determine the time of supply under clause (a) or clause (b), the time of supply shall be the date of entry in the books of account of the recipient of supply:

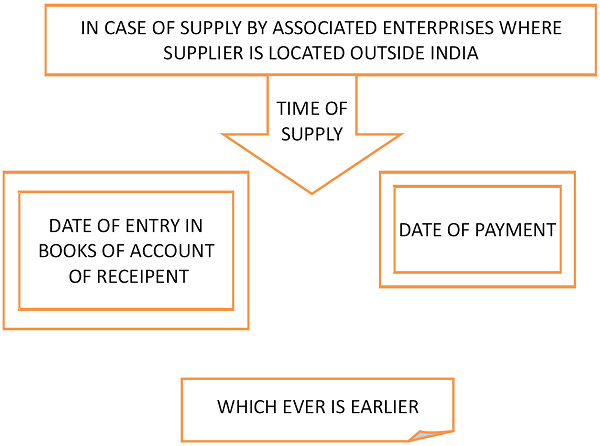

√ Provided further that in case of supply by associated enterprises,

√ where the supplier of service is located outside India,

√ the time of supply shall be

√ the date of entry in the books of account of the recipient of supply or

√ the date of payment,

√ whichever is earlier.

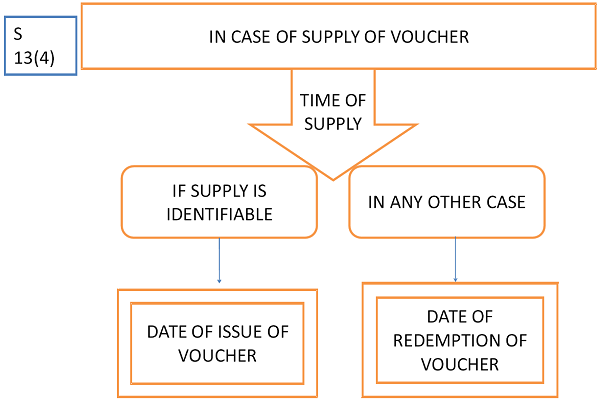

13(4) Time of supply in case of vouchers:-

In case of supply of vouchers by a supplier, the time of supply shall be–

(a) the date of issue of voucher, if the supply is identifiable at that point;

Or

(b) the date of redemption of voucher, in all other cases.

13 (5) Where it is not possible to determine the time of supply under the provisions of sub-section (2) or sub-section (3) or sub-section (4), the time of supply shall–

(a) in a case where a periodical return has to be filed, be the date on which such return is to be filed;

Or

(b) in any other case, be the date on which the tax is paid.

13 (6) The time of supply

♦ to the extent it relates to an addition in the value of supply

♦ by way of interest,

♦ late fee or

♦ penalty for delayed payment of any consideration shall be

♦ the date on which the supplier

♦ receives such addition in value.

Major Changes:

♦ In the present scenario there is no provision relating to taxation of Interest, Late Fees or penalty for delayed payment but now in GST Scenario the same is taxable.

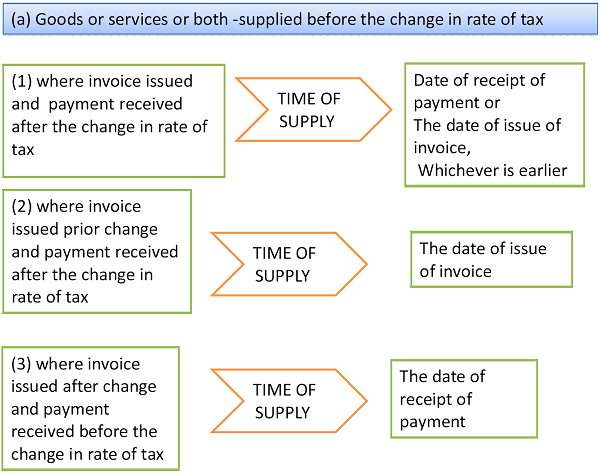

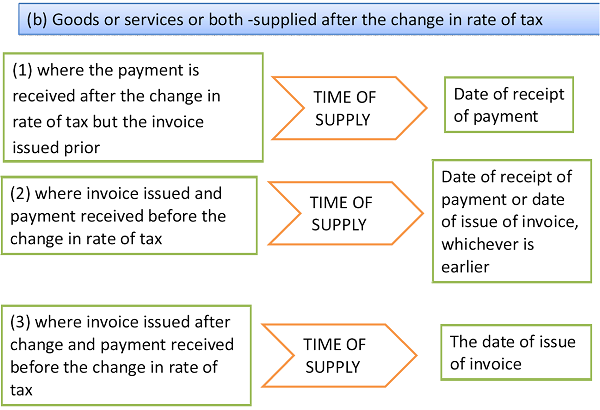

S 14 Change in rate of tax in respect of supply of goods or services.

The time of supply, where there is a change in the rate of tax in respect of goods or services or both, shall be :-

Illustration:

Goods and/ or Services supplied on 15.06.2018 and date of Change in rate 30.06.2018

| S.No | Invoice | Payment | Time of Supply |

| 1 | 05.07.2018 | 15.07.2018 | 05.07.2018 |

| 2 | 15.06.2018 | 15.07.2018 | 15.06.2018 |

| 3 | 05.07.2018 | 20.06.2018 | 20.06.2018 |

Illustration:

Goods and/ or Services supplied on 15.06.2018 and date of Change in rate 30.06.2018

| S.No | Invoice | Payment | Time of Supply |

| 1 | 15.06.2018 | 15.07.2018 | 15.07.2018 |

| 2 | 15.06.2018 | 20.06.2018 | 15.06.2018 |

| 3 | 15.07.2018 | 20.06.2018 | 15.07.2018 |

Author Details- CA Manish Aggarwal ,Practicing Chartered Accountant, B.Com(H), FCA, DISA (ICAI), +91-8860741030, aggarwalca@outlook.com- Add: M-175, Shastri Nagar, Delhi-110052