Case Law Details

Award Vintrade Pvt. Ltd. Vs ITO (ITAT Kolkata)

Section 147/144B Reassessment Quashed for Lack of NFAC Jurisdiction Before Section 151A Notification: ITAT Kolkata

The assessee filed appeals against the orders of the National Faceless Appeal Centre (NFAC), Delhi dated 02.03.2026 and 04.03.2026 for Assessment Years 2013-14, 2014-15 and 2017-18, including appeals against penalty levied under Section 271(1)(c) by order dated 11.11.2021. As the issues were identical, the Tribunal treated the appeal for AY 2017-18 as the lead case.

For AY 2017-18, the assessee challenged the validity of the assessment order passed by NFAC on 21.03.2022 under Sections 147 read with 144B, contending that it was without jurisdiction. The assessee had filed its return declaring a loss of ₹5,290. The Assessing Officer recorded that the assessee had allegedly received ₹1,70,00,490 through rotation of funds in the guise of bogus share premium and bogus investment from entities managed and controlled by Shri Mukesh Banka. The case was transferred to NFAC, which issued notice under Section 142(1) on 02.12.2021. After the assessee responded, NFAC completed the reassessment under Sections 147 read with 144B on 21.03.2022 by assessing total income at ₹1,70,16,700.

The assessee argued that although Section 151A relating to faceless assessment of income escaping assessment had been inserted with effect from 01.11.2020, the scheme was notified only on 29.03.2022 through Notification No. 18/2022. Therefore, NFAC lacked jurisdiction to issue notice under Section 142(1) on 02.12.2021 and to complete the reassessment on 21.03.2022. The Department contended that the assessment had been framed in accordance with Section 151A, which had already been introduced with effect from 01.11.2020.

After considering the rival submissions, the Tribunal noted that while Section 151A was introduced with effect from 01.11.2020, the faceless reassessment scheme was notified only on 29.03.2022. Since the notice under Section 142(1) and the reassessment order had been issued prior to 29.03.2022, the Tribunal held that the assumption of jurisdiction by NFAC was without valid authority. It relied upon the coordinate Bench decision in MD Mahimud SK Vs. ITO, which had held that reassessment proceedings initiated by NFAC before the notification dated 29.03.2022 were without jurisdiction. The Tribunal also noted that the coordinate Bench had relied upon Nabiul Industrial Metal Pvt. Ltd. Vs. ITO on the same issue.

Following the coordinate Bench decision, the Tribunal quashed the reassessment framed by the Assessing Officer/NFAC and allowed the appeal for AY 2017-18. It held that the same reasoning applied mutatis mutandis to the appeals for AYs 2013-14 and 2014-15, and accordingly allowed those appeals as well.

With regard to the penalty appeal, the Tribunal observed that since it had already quashed the assessment in the corresponding quantum appeal, the penalty levied by the Assessing Officer and confirmed by the CIT(A)/NFAC also could not survive, as the foundation for levy of penalty no longer existed. Accordingly, the penalty appeal was also allowed. The Tribunal concluded by allowing all four appeals of the assessee. The order was pronounced on 29.06.2026.

Cases Discussed:

- MD Mahimud SK Vs. ITO, ITA Nos. 2230 & 2229/KOL/2024, order dated 04.03.2025.

- Nabiul Industrial Metal Pvt. Ltd., Paschim Medinipur Vs. I.T.O., ITA No. 1328/KOL/2024 for A.Y. 2017-18, order dated 15.10.2024.

FULL TEXT OF THE ORDER OF ITAT KOLKATA

These are appeals preferred by the assessee against the order of the National Faceless Appeal Centre, Delhi (hereinafter referred to as the “Ld. CIT(A)”]even dated 02.03.26, 04.03.2026 for the AYs 2013-14,2014-15, 2017-18. The penalty was levied u/s 271(1)(c) of the Act vide order dated 11.11.2021 by NFAC, Delhi.

2. As the facts and circumstances are exactly identical in the appeals bearing ITA Nos. 973, 994, 995/KOL/2026, hence, we take ITA No. 995/KOL/2026 for A.Y. 2017-18 as lead case and decide the issue accordingly.

ITA Nos. 973/KOL/2026

3. The only issue raised by the assessee is against upholding the assessment order by the National Faceless Appeal Centre, Delhi [the learned CIT (A)] vide order dated 21.03.2022, which is without jurisdiction and is accordingly, invalid.

4. The facts in brief are that the assessee filed the return of income on 29.09.2014 for A.Y. 2017-18, showing total loss at 5,290/-. The Id. AO noted that assessee was a beneficiary, who had received 170,00,490/- through rotation of funds in the guise of bogus share premium money, bogus investment etc from the Banka Group entities managed and controlled by Shri Mukesh Banka. Subsequently, the case of the assessee transferred to NaFAC. Thereafter, notice u/s 142(1) of the Act dated 02.12.2021 was issued which was replied by the assessee. Finally , the impugned assessment order was passed u/s 147 r.w.s. 144B on 21.03.202 by the NFAC, Delhi by assessing income at 170,16,700/- to the total income of the assessee.

2. The Id. AR vehemently submitted before us that the order passed by the NFAC is without jurisdiction as though the provisions dealing with the faceless assessment of income escaping the assessment u/s 151A of the Act were brought on statute book by Taxation and Other Law (Relaxation and Amendment of Certain Provisions) Act, 2020, with effect from 01.11.2020, however, the same were notified on 29.03.2022 vide notification no. 18/2022 on e-assessment of income escaping income of Assessment Scheme, 2022. Therefore, the Id. Counsel for the assessee submitted that the assessment framed by the National faceless assessment Centre was without valid jurisdiction as the provisions of Section 151A of the Act had not come into operation on that date when the jurisdiction was assumed by the National Faceless Assessment Centre, Delhi.The Id. AR submitted that the notice u/s 142(1) of the Act was issued by NFAC on 02.12.2021 even prior to 29.3.2022 and therefore, the whole of assessment is without jurisdiction and not sustainable in law and may be quashed.

3. The Id. DR on the other hand submitted that the assessment has been framed by the NFAC after issuing notice as per the provisions of Section 151A of the Act which were brought on the statute book with effect from 1.11.2020. Therefore, the legal issue raised by the assessee may kindly be dismissed.

4. After hearing the rival contentions and perusing the materials available on record, we note that the assessment has been framed by the NFAC vide order dated 21.03.2022. We further find that the Section 151A of the Act deals with the faceless assessment of income escaping assessment and was brought on the statue book by taxation and other law (relaxation and amendment of certain provisions) Act, 2020, with effect from 01.11.2020 which was notified on 29.03.2022 vide notification no.18/2022/F. No. 370142/16/2022-TPL(Part)]. Therefore, the issuance of notice u/s 142(1) of the Act and thereafter framing of assessment by the NFAC, in our opinion, are without valid jurisdiction as the Provisions of Section 151A of the Act were effective from 29.03.2022. In considered opinion the assessment framed is without jurisdiction and cannot be sustained. The case of the assessee is squarely covered by the decision of the co-ordinate in case of MD Mahimud SK Vs. ITO in ITA no. 2230 & 2229/KOL/2024 vide order dated 04.03.2025, wherein the co-ordinate Bench has decided the issue by observing and holding as under: –

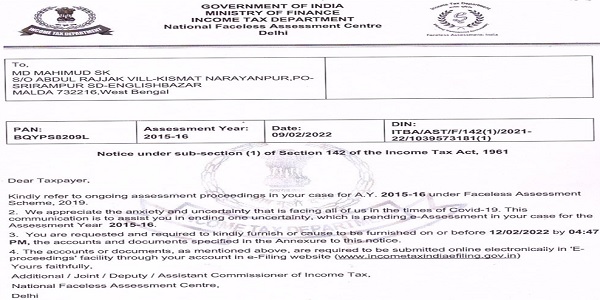

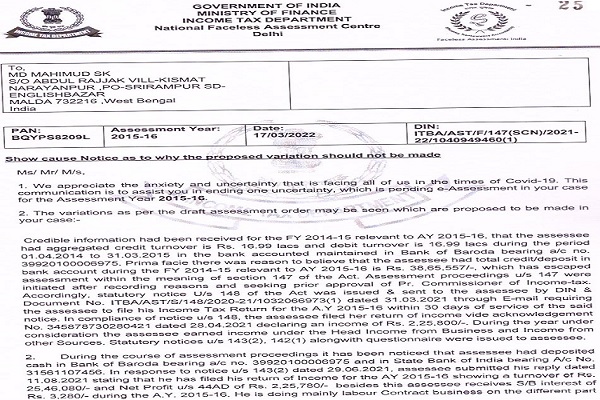

“11. We have perused the section of Section 151A of the Act, which deals with the faceless assessment of income escaping assessment and was brought on the statute book by taxation and other law (realization and amendment of certain provisions) Act, 2020, with effect from 01.11.2020 which was notified on 29.03.2022 vide notification no.18/2022/F. No. 370142/16/2022-TPL(Part)]. Therefore, the assessment proceedings were taken by the National Faceless Assessment Centre, Delhi by issuing notice u/s 142(1) dated 09.02.2022 and thereafter the assessment was framed accordingly after issuing show cause notice which in our opinion is without jurisdiction. The provisionw of Section 151A of the Act were brought on the statute book with effect from 01.11.2020. However, the same were made effective and applicable with effect from 29.03.2022 vide notification no. when the CBDT notified the new scheme for assessment of income escaping assessment scheme, 2022. In our considered view the assessment framed is without jurisdiction and cannot be sustained. The case of the assessee find force from the decision of Nabiul Industrial Metal Pvt. Ltd., Paschim Medinipur VS. I.T.O., in ITA no. 1328/KOL/2024 for A.Y. 2017-18, the order dated 15.10.2024, wherein a similar issue has been decided in favor of the assessee. For the sake of ready reference, the notice issued u/s 142(1) dated 09.02.2022 and show cause notice dated 17.03.2022, are extracted below:-

—

of the country and sometimes in local basis. He receives cash from different contractee and paid to the daily workers on cash basis. Whenever, he does not receive any contract he deposited the cash in the bank accounts and later on he again withdraws cash from Bank and pay the daily workers if he receive any contract work. Notice u/s 142(1) dated 29.12.2021 was issued to the assessee to furnish detailed computation of income, brief note indicating the nature of business/professional activities carried out by him and explain the source of cash deposit in the above said accounts. In response to notice u/s 142(1) dated 29.12.2021, assessee did not submit his reply. After that, again a notice u/s 142(1) dated 09.02.2022 was issued to furnish detailed computation of income, copy of cash flow statement, details of contract made with documentary evidence and details of payment to the labour with documentary evidence. But, assessee again did not submit his reply.

3. A final show cause notice u/s 144 of the I.T. Act, 1961 was issued to the assessee on 23.02.2022 for the sake of natural justice and providing one more and last opportunity to explain requesting him to furnish the requisite details on or before 25.02.2022. The assessee again failed to furnish any reply.

4. It is a part of record that during the course of assessment proceedings sufficient opportunity and reasonable time was granted to the assessee but he did not bother to comply with the notices and to provide the vital information/documents so as to enable the Assessing Officer to complete the assessment. Needless to mention here that when a statutory notice has been issued, it is the duty of the assessee to respond and to furnish the required information. Further, while scrutinizing the case it would be of great importance to have an idea about assessee’s intention behind the non-co-operation. The immediate idea that can be formed is that the assessee might have taken it beneficial to evade the proceedings rather than to co-operate in furnishing the information to avoid further investigation in the matter. Therefore, in the absence of relevant reply from the assessee, the matter is being decided as per the record available.

5. After pursuing the reply of the assessee and the return of income filed u/s 148, it was found that the assessee is deriving income from the business and income from other sources. After considering the reply of the assessee, the reply is not found tenable because the assessee has not produced proper books of account coupled with non-production of documentary evidence of contract business. Hence, cash deposited in Bank of Baroda bearing A/c No. 39920100006975 amounting to Rs. 16,96,682/- and in State Bank of India bearing A/c No. 31561107456 amounting to Rs. 4,09,500/-, totaling Rs. 21,06,182/-, is treated as unexplained credit entries in the books of the assessee and accordingly, addition of Rs. 21,06,182/- is proposed to be added back to the income of the assessee u/s 69A r.w.s. 115BBE of the Income Tax Act, 1961. Penalty proceedings u/s 271(1)(c) of the Income-tax Act, 1961 for inaccurate particulars of income are initiated separately.

Returned Income: Rs. 2,25,800/-

Add: As per para 5 – Rs. 21,06,182/-

Assessed Income: Rs. 23,31,982/-

Issue penalty notice u/s 271(1)(c) and 271(1)(b) of the Income Tax Act, 1961.

Assessed issued requisite documents to the assessee.

This order is being passed u/s 147/143(3) r.w.s. 144B of the I.T. Act, 1961.

You are hereby given an opportunity to show cause why proposed variation should not be made and the assessment should not be completed accordingly.

3. Kindly submit your response through your registered e-filing account at www.incometax.gov.in by 23:59 hours of 21/03/2022, whereby you may either:–

a. accept the proposed variation; or

b. file your written reply objecting to the proposed variation; or

c. If required, after filing written reply you may request for personal hearing so as to make oral submissions or present your case. The request can only be made by clicking the Seek Video Conferencing button available against the SCN in the view notices of this proceeding in the e-proceedings tab on e-filing portal. The request can be made only before expiry of compliance date & time. On approval of request, personal hearing shall be conducted exclusively through video conference.

4. In case no response is received by the given time and date, the assessment shall be finalized as per the draft assessment order.

Yours faithfully,

Additional / Joint / Deputy / Assistant Commissioner of Income Tax

Income-tax Officer,

National Faceless Assessment Centre,

12. Considering the above facts and legal position, we are of the considered opinion that the order passed by the NFAC, Delhi is without jurisdiction and is hereby quashed. The appeal of the assessee is allowed.

13. The additional ground raised in ITA No. 2230/Kol/2024 A. Y.2017-18 is similar to one as decided by us in ITA No. 2229/Kol/2024 A.Y. 2015-16. Therefore, our decision would, mutatis mutandis, apply to this appeal as well. The appeal of the assessee is allowed.

14. In the result, the appeal of the assessee is allowed.”

4.1. In view of the above facts and circumstances and following the decision of the coordinate bench as discussed above , we are inclined to quash the assessment framed by the Id. AO/ NFAC.

5. The appeal of the assessee is allowed.

ITA No. 994 & 995/KOL/2026

The issue invlolved in these appeals is similar to one as decided by us in ITA No. 993/Kol/2026(supra). Therefore our decision in ITA No. 993/Kol/2026(supra) would , mutatis mutandis, apply to these appeals as well. Accordingly the appeals are allowed.

For A.Y. 2013-14

ITA No. 974/KOL/2026

6. This is an appeal filed against the upholding penalty order by Id. CIT(A) in ITA No. 974/KOL/2026. Since we have already quashed the assessment framed by the Id. AO/ NFAC while adjudicating the quantum appeal of the assessee in ITA No.973/KOL/2026(supra), therefore, the penalty levied by the Assessing Officer and confirmed by the Id. CIT(A) /NFAC would also stand quashed as the very foundation of levy of penalty does not more survive. The appeal is allowed.

7. In the result, all four appeals of the assessee are allowed.

Order pronounced on 29.06.2026.

Author Bio