Case Law Details

Balaka Cold Storage Pvt. Ltd. Vs ACIT (ITAT Kolkata)

The ITAT Kolkata considered the assessee’s appeal against the order of the Commissioner of Income Tax (Appeals), National Faceless Appeal Centre, for Assessment Year 2017-18. During the appellate proceedings, the assessee raised an additional legal ground challenging the validity of the assessment on the basis that the assessment order under Section 143(3) of the Income-tax Act, 1961 had been framed without a valid notice under Section 143(2) and in contravention of CBDT Instruction F. No. 225/157/2017/ITA-II dated 23.06.2017 and CBDT Instruction No. 1/2011 (F. No. 187/12/2010-IT(A-1)) dated 31.01.2011. The assessee contended that the assessment was therefore void and without jurisdiction.

The Tribunal first considered whether the additional ground could be admitted. It observed that the issue raised was purely legal, all relevant facts were already available on record, and no further factual enquiry was required. Relying on the decisions of the Supreme Court in Jute Corporation of India Ltd. v. CIT and National Thermal Power Co. Ltd. v. CIT, as well as the Calcutta High Court decision in PCIT v. Britannia Industries Ltd., the Tribunal held that a pure question of law could be raised for the first time before an appellate authority. Accordingly, it admitted the additional ground for adjudication.

On the merits, the Tribunal noted that the assessee had filed its return of income on 23.10.2017 declaring total income of ₹16,79,259. The assessee’s case was selected for scrutiny through Computer Assisted Scrutiny Selection (CASS), notices under Sections 143(2) and 142(1) were issued, replies were filed, and the assessment was ultimately completed under Section 143(3) on 15.10.2019 by the Assistant Commissioner of Income Tax, Circle 23(1), Hooghly, making various additions.

The Tribunal examined CBDT Instruction No. 1/2011 dated 31.01.2011, which prescribes pecuniary jurisdiction for assessing authorities. Under the Instruction, Income Tax Officers have jurisdiction where returned income is up to ₹20 lakh in metro cities and ₹15 lakh in mofussil areas, while Assistant Commissioners/Deputy Commissioners have jurisdiction only where returned income exceeds those limits. Since the assessee had disclosed total income of ₹16,79,259 and the assessment had been framed by the ACIT, Circle 23(1), Hooghly, the Tribunal held that the assessment had been completed by an officer lacking the prescribed pecuniary jurisdiction under the CBDT Instruction.

The Tribunal relied upon the Calcutta High Court judgment in PCIT v. M/s Shree Shoppers Ltd., which had affirmed the Tribunal’s view that a notice issued by an officer lacking jurisdiction rendered the consequent assessment invalid. It also referred to the jurisdictional High Court’s subsequent decision in PCIT v. Mintu Das, where the High Court held that issuance of a notice under Section 143(2) and completion of assessment by an Assistant Commissioner, despite the returned income falling within the pecuniary jurisdiction of the Income Tax Officer under CBDT Instruction No. 1/2011, constituted a violation of the jurisdictional mandate. The High Court held that such procedural irregularity rendered the assessment proceedings invalid and bad in law.

Applying these binding precedents, the Tribunal concluded that the assessment in the present case had been framed by a non-jurisdictional Assessing Officer in violation of CBDT Instruction No. 1/2011. Consequently, the assessment was held to be invalid and was quashed.

Accordingly, the Tribunal allowed the assessee’s appeal.

Recent Cases Discussed:

- PCIT v. Mintu Das, ITAT/167/2025, IA No. GA/1/2025, GA/2/2025, order dated 14.01.2026.

- PCIT v. M/s Shree Shoppers Ltd., ITAT 39/2023, IA No. GA/1/2023, order dated 15.03.2023.

- PCIT v. Nopany & Sons, (2022) 136 taxmann.com 414 (Cal).

FULL TEXT OF THE ORDER OF ITAT KOLKATA

This is an appeal preferred by the assessee against the order of the National Faceless Appeal Centre, Delhi (hereinafter referred to as the “Ld. CIT(A)”] dated 29.11.2023 for the AY 2017-18.

2. The assessee has raised an additional ground which reads as under:-

“FOR THAT in the facts and circumstances of the instant case, the Ld. Commissioner of Income Tax (Appeals)-N.F.A.C. acted unlawfully in not appreciating that none of the conditions precedent existed for and/or were fulfilled by the Ld. Assistant Commissioner of Income Tax, Circle 23(1).

Hooghly for his specious action of framing the assessment order u/s. 143(3) of the Income Tax Act, 1961 on 15-10-2019 in the instant case de hors any valid notice u/s. 143(2) of the Income Tax Act, 1961 issued in contravention of the C. B. D. T. Instruction F. No. 225/157/2017/ITA-II DateFse]ctiond 23-06-2017 as well as the C.B.D.T. Instruction F. No. 1/2011 [F. NO. 187/12/2010-IT(A-1)]. DATED 31-01-2011 and the impugned inaction on that account renders the assessment order framed ab initio void, ultra vires and null in law.”

3. After hearing the rival contentions and perusing the material on record, we find that the assessee has raised the above additional ground of appeal challenging the jurisdiction of the AO to make addition. In our opinion the issued raised in the additional ground is a purely a legal issue qua which all the facts are available in the appeal folder and no further verification of facts are required from any quarter whatsoever. In our considered view the assessee is at liberty to raise any legal issue before any appellate authority for the first time even when the same has not been raised before the lower authorities. The case of the assessee is squarely covered by the decisions of the Apex court in the case of i) Jute Corporation of India Ltd. Vs CIT in 187 ITR 688 , ii) National Thermal Power Co. Ltd v. CIT [1998] 229 ITR 383 and also by the decision of Hon’ble Calcutta High Court in PCIT vs. Britannia Industries Ltd. [2017] 396 ITR 677 (Cal). Therefore, we are inclined to admit the same for adjudication.

4. The facts in brief are that the assessee filed the return of income on 23.10.2017, declaring total income at t 6,79,259/. The assessee is engaged in the business of running of cold storage besides having income from other sources. The case of the assessee was selected for scrutiny under Computer Assisted Scrutiny Selection (CASS). Notice u/s 143(2) and 142(1) of the Income-tax Act, 1961 (the Act) along with questionnaire were duly served upon the assessee which were replied by the assessee. Finally, the assessment was framed by the Id. AO making various additions to the income of the assessee in the assessment framed u/s 143(3) of the Income-tax Act, 1961 (the Act) vide order dated 15.10.2019.

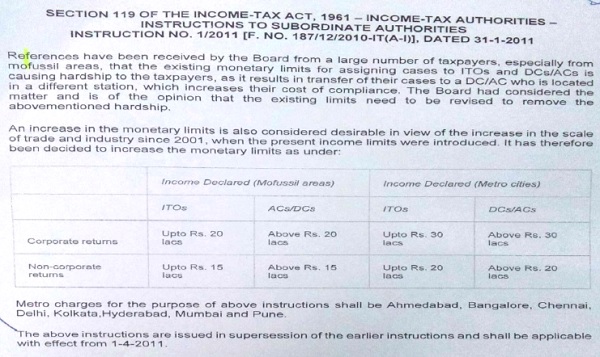

5. At the outset, we note that the return of income was filed by the assessee declaring total income of 16,79,259/-, whereas the assessment has been framed by the ACIT, Circle 23(1), Hooghly which is in violation of pecuniary jurisdiction of the CBDT instruction No.1/2011 (F. No. 187/12/2010-IT(A-1), Dated 31.01.2011. According to the said instruction, the ITO has pecuniary jurisdiction where the income is upto 20 lacs in the Metro Cities and 15 lacs in Mofussil areas whereas the DC/AC have jurisdiction above 20 lacs in Metro cities and above 15 lacs in the Mofussil areas. The said instructions reads as under:-

6. In the present case, the assessee filed the return of income on 23.10.2017, disclosing total income of 16,79,259/-. We note that assessment framed by ACIT, Circle 23(1), Hooghly which is in violation of the CBDT Instruction No.1/2011 (F. No. 187/12/2010-IT(A-1), Dated 31.01.2011. Therefore, the said assessment has been issued by non-jurisdictional AO which is invalid and cannot be sustained. The case of the assessee find support from the decision of the Hon’ble Calcutta High Court in the case of PCIT vs. M/s Shree Shoppers Ltd. in ITAT 39/2023, IA No. GA/1/2023, dated 15.03.2023, wherein the Hon’ble Court has decided the issue in favour of the assessee by upholding the order of the Tribunal. The Tribunal in ITA No. 865/KOL/2018 for A.Y. 2012-13 in case of M/s Shree Shoppers Ltd. Vs. DCIT has held that notice issued by ITO, Ward 39(4), Kolkata, u/s 143(2) of the Act was without valid jurisdiction and therefore the consequent assessment framed by the DCIT, circle 9(2), Kolkata is invalid. The Hon’ble Tribunal followed the decision of jurisdictional High Court in case of PCIT vs. Nopany & Sons (2022) 136 taxmann.com 414 (Cal), while passing the order.

7. Similarly, the case of the assessee also find support from the decision of Hon’ble Jurisdictional High Court Calcutta in case of PCIT Vs. Mintu Das in ITAT/167/2025, IA No. GA/1/2025, GA/2/2025 vide order dated 14.01.2026, wherein it has held as under:-

“We, after hearing the rival submissions of the parties and perusing the materials available on record note that the return of income of the assessee was of Rs.16,50,920/ which falls under the jurisdiction of the ITO, Ward-28(2), Kolkata but notice u/s 143(2) of the Act was issued by ACIT, Circle-28, Kolkata and also the assessment order was duly framed by ACIT, Circle-28. Kolkata, which is clearly a violation of the jurisdictional mandate under CBDT Circular No. 1/2011 dated 31.01.2011. We note that this procedural irregularity rendered the assessment proceedings invalid and bad in law.”

This Court observes that the jurisdictional issue has rightly been determined by the learned Tribunal and no substantial questions of law arises in this appeal.

In view of the above, we dismiss the appeal. Accordingly, the stay petition (GA/2/2025) is also dismissed.”

8. Considering the facts and circumstances of the case and also relying on the above decisions, we hold the assessment framed by the Id. AO as invalid and accordingly quashed the same.

9. In the result, the appeal of the assessee is allowed.

Order pronounced on 16.06.2026.

Author Bio