Case Law Details

Karti P. Chidambaram Vs Union of India (NCLT Chennai)

The National Company Law Tribunal (NCLT), Chennai disposed of an application filed under Rule 11 of the NCLT Rules, 2016, seeking to vacate an ad interim order dated 4 November 2025 passed in Company Petition No. 110 of 2025. The applicant sought defreezing of his current and fixed deposit accounts, removal of attachment over movable assets, and defreezing of the bank accounts of his family members.

The proceedings arose from an investigation into the affairs of Vasan Health Care Private Limited (VHCPL). Based on the investigation report dated 21 March 2024, the Ministry of Corporate Affairs directed the filing of a petition under Section 212(14A) of the Companies Act, 2013.

The applicant contended that he was neither a shareholder nor a director of the entities under investigation and that his association with Advantage Strategic Consulting Private Limited (ASCPL) was limited to an indirect shareholding through Ausbridge Holdings and Investments Private Limited (AHIPL) for less than ten months. He also submitted that he had resigned as a director of AHIPL in March 2012 and thereafter had no role or authority in its affairs. According to the applicant, there was no material establishing his involvement in the day-to-day affairs of VHCPL.

The applicant further argued that although the Tribunal’s earlier order directed freezing of his bank accounts, its implementation extended beyond its scope by resulting in the freezing of accounts belonging to his wife, daughter, mother-in-law, and his company. He submitted that these actions disrupted his personal and professional life by preventing payment of employee salaries, rent, statutory dues including GST, TDS, PF and ESI, educational expenses of his daughter, and essential medical and travel expenses. He also stated that the freezing of his salary and allowances account affected his ability to discharge his Parliamentary functions. The applicant pointed out that ASCPL had been permitted to operate its bank accounts for routine business while his accounts remained completely frozen, describing the differential treatment as arbitrary.

The Serious Fraud Investigation Office (SFIO) opposed the application, contending that the investigation established that the applicant exercised both de facto and de jure control over ASCPL within the meaning of the Companies Act. It relied on internal email communications, approval of payments, control over bank accounts, decisions relating to overseas assets, and directions issued to company directors to contend that the applicant continued to exercise effective control even after his formal resignation. The SFIO further alleged that unlawful gains of Rs. 48 crore had been routed through ASCPL under the applicant’s directions, making him the ultimate beneficiary. It also alleged that the applicant had furnished incorrect PAN details during the investigation, resulting in the freezing of certain family members’ accounts when banks linked those accounts to the PAN disclosed by him.

After considering the rival submissions, the Tribunal observed that in investigations under Section 212(14A), interim freezing orders are intended to secure the alleged proceeds of fraud and prevent alienation or siphoning of assets pending final adjudication. The Tribunal held that the investigation report contained serious allegations regarding the applicant’s continued control over ASCPL and the routing of unlawful gains. Since these allegations required detailed examination during the final hearing, the Tribunal declined to vacate the freezing order relating to the applicant’s savings accounts, current accounts, fixed deposits, and movable assets listed in Schedules 1 and 2. It held that lifting the freeze at the interim stage could defeat the purpose of Section 212(14A).

However, the Tribunal distinguished the applicant’s salary and allowances account maintained with the State Bank of India, Parliament House Branch, New Delhi. Referring to Sections 3 and 4 of the Salary, Allowances and Pension of Members of Parliament Act, 1954, it held that the salary account formed part of the applicant’s livelihood and was necessary for discharging his Parliamentary duties and meeting basic subsistence expenses. The Tribunal also noted that the respondent had agreed during the hearing to the defreezing of this account. Accordingly, it directed the immediate defreezing of the salary and allowances account.

Regarding the accounts of the applicant’s family members, the Tribunal accepted the respondent’s explanation that those accounts had been frozen only because they were linked to the PAN disclosed during the investigation and not because they were specifically identified as containing proceeds of fraud. It therefore directed the immediate defreezing and restoration of normal operations in all family members’ accounts listed in Schedule 3.

Accordingly, the Tribunal ordered the immediate defreezing of the applicant’s salary and allowances account and the bank accounts of his family members while directing that the interim freezing order over the applicant’s other bank accounts and movable assets under Schedules 1 and 2 would continue until further orders. The application was disposed of with these directions, which were directed to take immediate effect.

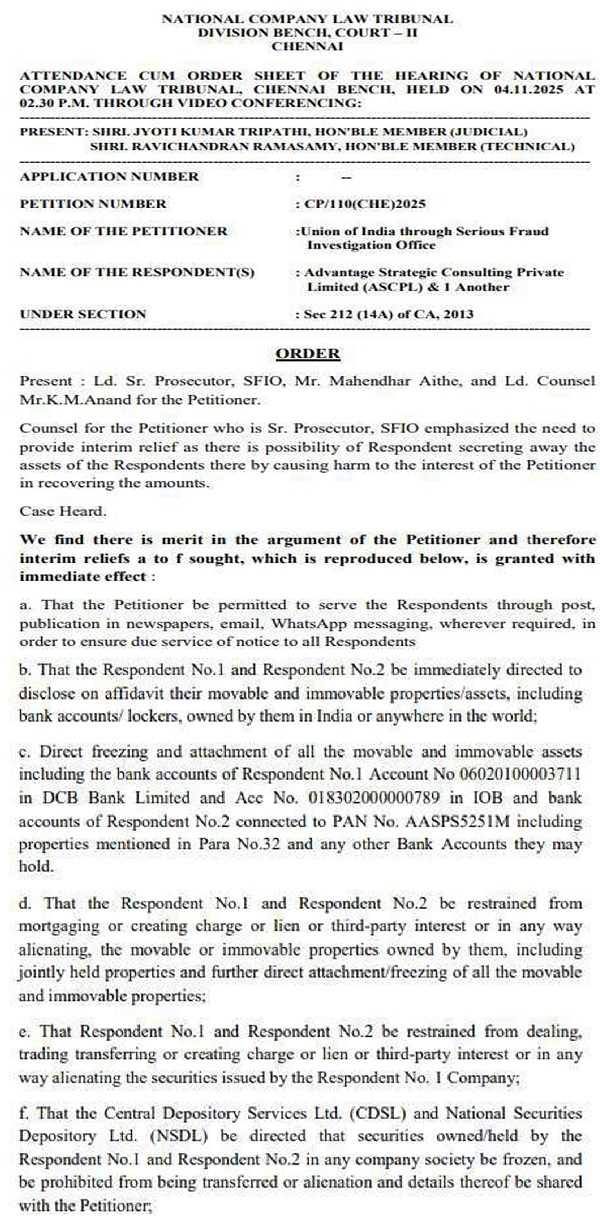

FULL TEXT OF THE NCLT JUDGMENT/ORDER

Present : Ld. Counsel Ms. Varsha Jain for the Applicant.

Ld. Counsel Mr.K.M. Anand for the Respondent.

Vide separate order pronounced in open court, Cont.A(C.A)/4/CHE/2025 is Disposed off.

This application has been filed by the Applicant Karti P Chidambaram under Rule 11 of NCLT rules 2016, and has sought for following relief,

a) Vacate the ad interim order passed by this Tribunal dated 4thNovember 2025, in Company Petition No.110 of 2025 against the Applicant herein.

b) Direct the defreezing of the Applicants current and fixed accounts as mentioned in Schedule 1

c) Direct for the removal of the attachment of the moveable assets of Applicant 1 as mentioned in Schedule 2.

d) Direct for the defreezing of the Applicants family members accounts as mentioned in Schedule 3.

e) Pass such further or other orders as the Hon’ble Tribunal may deem fit and proper in the circumstances of the case and thus render justice.

FACTS OF THE CASE

1. On investigation into the affairs of Vasan Health Care Private Limited (VHCPL) the Investigation Report dated 21.03.2024 has been submitted to the Ministry of Corporate Affairs, and the Central Government has directed filing of the present petition under Section 212(14A).

2. The Applicant states that the applicant is neither a shareholder/director in Ms Advantage Strategic Consulting Private Limited or Vasan Healthcare Private Limited (VHPL), it is stated by the applicant that various ex-parte interim injunction is passed against the applicant.

3. It is stated that the relationship between the Applicant and ASCPL is limited to the applicants indirect shareholding for a limited period through an entity called Ausbridge Holdings and Investments Private Limited (“AHIPL”). The Applicant submits that AHIPL had shareholding in ASCPL only from 25.03.2011 and the present Applicant was a shareholder of AHIPL from 26.02.2006 to 05.10.2011. Therefore, it is the period of overlap between AHIPL’s holding in ASCPL and the Applicants shareholding in AHIPL is less than 10 months i.e. between 25.03.2011 to 05.10.2011.

4. It is stated that the Applicant was only a director in AHIPL for a limited period starting 28.02.2006 to 08.03.2012 further the applicant submits that after his resignation on 08.03.2012, he had absolutely no role, authority, or involvement in the functioning of AHIPL.

5. It is stated that there is no material on record to show that the Applicant is connected with the day to day affairs of the Vasan Healthcare Private Limited, the Company which is being investigated by the Petitioner/1st

6. It is stated that while the order dated 04.11.2025 only calls for the freezing of the Applicant’s bank accounts the operation of the order has gone beyond the scope of the order. The Petitioner/R1 has written to various banks calling for the freezing of accounts of the Applicant’s wife Mrs. Srinidhi Chidambaram, the Applicants Daughter, Miss. Aditi Nalini Chidambaram, the Applicants mother-in-law, Dr. Vasanthi Rangarajan (senior citizen of 89 years) and the applicants company M/s Chess Advisory Services.

7. It is stated that The attachments have severely affected the Applicants day to day functioning of

- Pay monthly salaries and retain essential employees.

- Pay rent, electricity, maintenance, and other recurring office and household overheads.

- Make statutory payments including GST, TDS, PF, ESI and other government dues.

- Make payments for his daughter’s education and expenses abroad.

- Essential Medical and Travel expenses.

8. In the counter filed by the respondent it is submitted that The Investigation has categorically established that Applicant exercised de facto and de jure control over ASCPL within the meaning of Section 2(27) -“Control”, Section 2(59)- “Officer”, and Section 2(69) – “Promoter “Internal email communications, approval of payments, control over bank accounts, decisions relating to acquisition of assets in India and abroad. Further directions issued to directors of ASCPL clearly show that the Board was accustomed to act on the instructions of Applicant.

9. The respondent stated that the investigation has revealed that formal resignation does not sever actual control and that the Applicant continued to approve payments from ASCPL accounts control overseas subsidiaries direct acquisition and management of properties in the UK, France and Spain, and exercise supervisory control over financial and operational decisions. Directors and key functionaries of ASCPL continued to seek approval from Applicant even after the alleged resignation.

10. It is stated by the respondent that the investigation has conclusively shown that unlawful gains of ₹48 Crores were routed through Respondent No.2 Company and were utilized strictly under the directions and control of Applicant making him the ultimate beneficiary.

11. The respondent stated that the Applicant’s conduct raises serious concerns, including (a) Providing incorrect personal identification data in the course of recording statement under oath during a statutory investigation (b) Causing misleading data to enter the record (c) Obstructing and derailing the investigative process (d) Creating avoidable complications leading to innocent third-party prejudice.

12. The respondent stated that the interim order dated 4.11.2025 this Tribunal had directed freezing of all bank accounts connected to the PAN of the Applicant. SFIO merely implemented the judicial direction. If any account standing in the name of the Applicant’s relatives came to be frozen the same was solely because such accounts were found by banks to be linked with the Applicant’s PAN and not due to any independent action or allegation by SFIO.

13. In the written submission filed by the applicant it is submitted that The Applicant’s banking operations have come to a standstill. Since November 2025, he has been unable to pay employee salaries or rent, to meet his statutory and regulatory obligations, or to fund his daughter’s education and from 04.11.2025 to 03.04.2026, the only account the Applicant could operate was the salary and allowances account maintained with the State Bank of India Parliament House Branch New Delhi. The 1st Respondent’s email dated 02.04.2026 to the Applicant’s banker which froze his salary and allowances account is a direct assault on his ability to discharge his Parliamentary duties.

14. It is stated that the 1st Respondent in CP/110(CHE)/2025, ASCPL, has been permitted to operate its bank accounts for routine operations vide this Tribunals order dated 03.12.2025, whereas the Applicant’s accounts have been frozen in their entirety. ASCPL is the very entity whose affairs are alleged to be connected to the matters under investigation, yet it continues to transact. This differential treatment is arbitrary and discriminatory and offends Article 14 of the Constitution of India.

15. The applicant states that the attachment halts all of the Applicant’s banking operations, prevents payment of employee salaries, rent, and statutory dues, and impairs the discharge of his Parliamentary functions, goes far beyond anything required to secure the alleged amount particularly when that amount is already represented by assets within ASCPL and a less restrictive measure of the kind already extended to ASCPL would adequately serve any legitimate interest. An interim measure that is more onerous than necessary, and harsher on the Applicant than on the entity at the centre of the investigation, cannot be sustained.

FINDINGS OF THIS TRIBUNAL

16. Heard the counsel and perused the document placed on record.

17. The applicant has filed this application seeking to vacate interim stay 04.11.2025 in CP/110/2025, the relevant portion of the order is extracted below,

18. The applicant in this application has sought to Direct the defreezing of the Applicants current and fixed accounts as mentioned in Schedule 1, Direct for the removal of the attachment of the moveable assets of Applicant 1 as mentioned in Schedule 2, Direct for the defreezing of the Applicants family members accounts as mentioned in Schedule 3

19. The Applicant has argued that the freezing of all banking channels has brought his personal, professional, and Parliamentary obligations to a standstill, causing severe collateral prejudice to his family members and employees. On the other hand the Respondent (SFIO) has contended that formal resignations do not automatically sever de facto control of the applicant.

20. In evaluating these conflicting positions, this Tribunal notes that in cases of statutory corporate investigation it is imperative to analyse the actual mind and conscience operating behind the alleged fraud. Also this tribunal notes that intent of an interim freezing order under Section 212(14A) is to secure the fruits of the alleged fraud and prevent the alienation or siphoning of assets pending final adjudication.

21. The respondent contended that Investigation has categorically established that the Applicant exercised de facto and de jure control over ASCPL within the meaning of Section 2(27) -“Control”, Section 2(59)- “Officer”, and Section 2(69) -“Promoter”, and Internal email communications, approval of payments, control over bank accounts, decisions relating to acquisition of assets in India and abroad, and directions issued to directors of ASCPL clearly show that the Board was accustomed to act on the instructions of Applicant, It is further stated that Applicant continued to exercise decisive influence over the affairs of ASCPL even after his resignation from AHIPL. It is stated that formal resignation does not sever actual control, and that the Applicant continued to approve payments from ASCPL accounts, control overseas subsidiaries, direct acquisition and management of properties in the UK, France and Spain, and exercise supervisory control over financial and operational decisions It is stated that the directors and key functionaries of ASCPL continued to seek approval from Applicant even after the alleged resignation.

22. The respondent has stated that findings of investigation, demonstrate continuous control exercised by Applicant even after his alleged resignation, In view of the above mentioned contention we are of the considered opinion that savings account, current accounts, fixed deposits, and movable assets listed in Schedule 1 and Schedule 2, shall continue to be frozen as the findings of the Investigation Report present serious allegations regarding the Applicant exercising de facto and de jure control over ASCPL and routing of unlawful gains to the tune of ₹48 Crores and his positioning as the ultimate beneficiary. We are of the considered view that these matters require detailed adjudication during the final hearing, and at this interim stage, completely vacating the freezing order on commercial and personal asset portfolios would risk potential alienation or siphoning of assets, thereby defeating the very purpose of Section 212(14A).

23. Further it is stated by the applicant that The Applicant’s banking operations have come to a standstill, and he is unable to pay employee salaries or rent, to meet his statutory and regulatory obligations, or to fund his daughter’s education. and from 04.11.2025 to 03.04.2026, the only account the Applicant could operate was the salary and allowances account maintained with the State Bank of India Parliament House Branch, New Delhi and the 1st Respondent vide email dated 02.04.2026 froze salary and allowances account of the applicant which has affected his ability to discharge his Parliamentary duties.

24. we are of the considered view that while the seriousness of an investigation conducted by the Serious Fraud Investigation Office (SFIO) cannot be undermined, the interim measures under Section 212(14A) of the Companies Act 2013, must be invoked only to the extent of safeguard the proceeds proposed to be dispersed to the account of the government, at this juncture we refer to the section 3 and section 4 of the salary allowances and Pension of members of Parliament act 1954, which states about the salaries and daily allowances to the member of parliament, we are of the view that salary and allowance account shall be defrozen as it forms a part of livelihood of the person. Further respondent has also agreed to the de freezing of the salary account in the hearing held. Therefore we are of the view that the salary and allowance account maintained with the State Bank of India, Parliament House Branch, New Delhi, shall be defrozen immediately to ensure he can discharge his public obligations and meet basic subsistence expenses.

25. It is stated by the respondent that PAN No. AASPS5251M came to be reflected in the petition filed by this respondent under section 212(14A) solely on account of the disclosure made by Applicant himself during the course of his examination conducted by SFIO under Section 217 of the Companies Act, 2013. The applicant was asked to furnish his PAN details and instead of providing his own PAN, he had supplied the PAN belonging to his spouse and the respondent has acted on it.

26. It is stated that interim order dated 4.11.2025, this Tribunal direct freezing of all bank accounts connected to the PAN of the Applicant. SFIO merely implemented the judicial direction and if any account standing in the name of the Applicant’s relatives came to be frozen, the same was solely because such accounts were found by banks to be linked with the Applicant’s PAN, and not due to any independent action or allegation by SFIO.

27. Therefore, in view of the contention of the respondent we are of the considered view that the account of the family members which have been frozen as per schedule 3 filed in the application shall be de freeze as the freezing of the account was based on the fact the account is linked to the applicant’s bank account and not due to specific attachment for having proceeds of fraud.

28. In view of the above-mentioned reasons and contention we pass the following directions,

1) The 1st Respondent (SFIO) and the concerned banks are directed to immediately defreeze the Applicant’s salary and allowances account maintained with the State Bank of India, Parliament House Branch, New Delhi. This relaxation is granted under Sections 3 and 4 of the Salary, Allowances and Pension of Members of Parliament Act, 1954, solely to ensure that the Applicant can discharge his public/Parliamentary obligations and meet basic day-to-day expenses.

2) Defreezing of Family Members’ Accounts (Schedule 3)

The 1st Respondent and the respective banks are directed to defreeze and restore normal operations in all bank accounts belonging to the Applicant’s family members (as detailed in Schedule 3)

3) However, with respect to the accounts mentioned in schedule 1 &2 the interim order dated 04.11.2025 shall continue to operate until further order.

29. In view of the above-mentioned reasons and contentions the Application filed by the applicant is Disposed of with the above directions.

30. The above order takes immediate effect.

Author Bio