A home loan is one of the few financial commitments that actually reduces your tax outgo. For Individuals or any other person repaying a housing loan in FY or Tax year 2026-27, the New Income Tax Act,2025 gives you deductions on both the interest component and the principal component of your EMI in Old regime. Knowing which section covers what, and how much you can actually save, makes a real difference to your tax planning.

This guide covers every home loan tax benefit FY 2026-27, the situation under the new regime and old regime, and how to calculate your actual savings with real numbers.

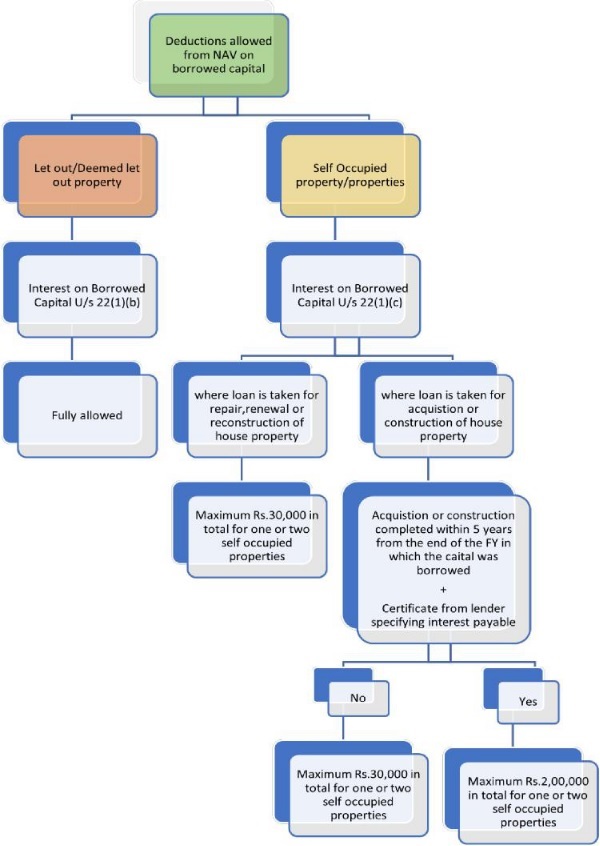

Deductions allowed on Borrowed capital with respect to Interest and principal

| Section number under IT Act,1961 | Section number under IT Act,2025 | What It Covers | Maximum Deduction | Regime Applicable |

| Section 24(b) | Section 22(1)(b)& 22(1)(c) | Interest on home loan (self-occupied) | Rs. 2,00,000 per year | Old regime only |

| Section 24(b) | Section 21 |

Interest on home loan (let- out property) | Actual interest (no cap) | Old and new regime both |

| Section 80C | Section 123 | Principal repayment | Up to Rs.

1,50,000 (within |

Old regime only |

| Section 80EEA | Section 131 | Additional interest | Rs. 1,50,000 over and above Section 22(1)(b) | Old regime only (loan sanctioned before March 31, 2022) |

(1) Section 22(1)(b) & Section 22(1)(c) – (Deduction from House property)

- In case of property or properties self-occupied, the aggregate amount of deduction under [sub-section (1)(b) and (c)] shall not exceed—

(1) Rs. 2,00,000, subject to following condition: –

(i) the property has been acquired or constructed with borrowed capital and such acquisition or construction is completed within five years from the end of tax year in which capital was borrowed;

(ii) the assessee furnishes a certificate from the person to whom interest is payable on such capital; and

(2) Rs. 30000 in any other case.

Note:-(1) Pre-construction interest allowable as deduction in 5 equal instalments from the P.Y. of completion of construction.

(2) If a portion of property is let out and a portion self-occupied then, income will be computed separately forlet out and self-occupied portion.

(3) The deduction u/s 22(1)(c) shall be computed after reducing the interest referred to in the said section by any amount already allowed as a deduction under any other provisions of this Act.

(2) Section 123 and 131 (General Deduction from Total Income)

(i) Section 123-Deduction for life insurance premia, deferred annuity, contributions to provident fund, etc.

An individual or a Hindu undivided family, shall be allowed a deduction of the whole of the amount paid or deposited in the tax year, being the aggregate of the sums enumerated in Schedule XV, as does not exceed Rs. 1,50,000, while computing the total income for that year, subject to the conditions specified in that Schedule.

Schedule XV includes deduction in respect of various payments like premium for LIC, deferred annuity, contribution to PF, etc. and one of them is payment made for purchase or construction of a residential house property the income from which is chargeable to tax under the head “Income from house property”

Deduction for repayment of the amount borrowed(principal) by the assessee from any bank, including a co-operative bank is allowed subject to maximum deduction of Rs.1,50,000 u/s 123 in total including other deductions.

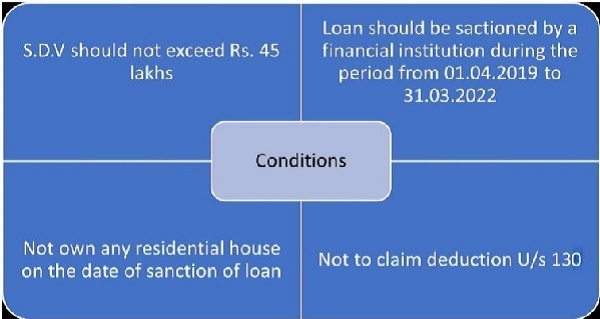

(ii) Section 131- Deduction in respect of interest on loan taken for certain house property.

An assessee, being an individual not eligible to claim deduction under section 130, shall be allowed a deduction of interest payable on loan taken by him from any financial institution for the purpose of acquisition of a residential house property, subject to a maximum limit of Rs. 1,50,000 in a tax year and on fulfilment of conditions specified in sub-section (2), for the tax year beginning on the 1st April, 2019 and subsequent tax years.

(2) The conditions referred in sub-section (2) shall be the following:—

Note :-If you sell the property within 5 years of possession, all Section 123 deductions claimed for principal repayment in earlier years are reversed and added back to your taxable income in the year of sale.

New regime 115BAC(1A) :-

None of the deductions available above in old regime is available in new regime except for Interest on borrowed capital u/s 21 in case of property let-out with no limit.(Whole interest can be allowed as deduction).

Joint Home Loan: Doubling the Tax Benefit

If a home loan is taken jointly, each co-borrower who is also a co-owner of the property can claim deductions independently in case of property self-occupied. This is one of the most effective ways to maximize home loan tax benefits.

| Co-borrower | Section 24(b) Claim | Section 80C Claim | Total Deduction |

| Husband | Rs. 2,00,000 | Rs. 1,50,000 | Rs. 3,50,000 |

| Wife | Rs. 2,00,000 | Rs. 1,50,000 | Rs. 3,50,000 |

| Combined | Rs. 4,00,000 | Rs. 3,00,000 | Rs. 7,00,000 |

Both must be co-owners and co-borrowers. The share of interest and principal is typically claimed in proportion to ownership share, though in practice both can claim the full limit as long as the actual amounts paid support it.

Conclusion:-

Whether to opt for old regime or new regime is a very subjective decision depending on various circumstances like number of house properties, loan statement, heads of income, option of opting out of default regime available only once in case of income from business and profession, joint loan deduction benefit and many more.

To conclude, if considered appropriately all the factors, deduction of Rs. 5,00,000 is available (1 self-occupied only) in total if opted out of default regime. There exists still a possibility that selection of old regime becomes beneficial subject to various matters with proper tax planning .