The Insolvency and Bankruptcy Board of India Disciplinary Committee held an insolvency professional guilty of misconduct for failing to conduct proper due diligence and presenting an ineligible resolution plan to the Committee of Creditors in violation of Section 29A of the Insolvency and Bankruptcy Code, 2016. The Committee found that a revised resolution plan submitted after the applicant was declared a wilful defaulter constituted a fresh plan, requiring eligibility assessment at that stage. The professional failed to verify and disclose this disqualification, leading to wrongful consideration and approval of an ineligible plan, causing delays and prejudice to the insolvency process. Additionally, non-cooperation with the investigation authority was established due to failure to respond to specific queries. Emphasizing that due diligence obligations are independent and continuous, the Committee rejected defenses based on limited role and lack of knowledge. Consequently, the professional’s registration was suspended for two years.

INSOLVENCY AND BANKRUPTCY BOARD OF INDIA

(Disciplinary Committee)

Order No. IBBI/DC/317/2026 Dated: 22 April 2026

This Order disposes of the Show Cause Notice (SCN) No. COMP-11012/47/2024-IBBI/488/882 dated 29.07.2024, issued to Mr. Vishal Ghisulal Jain, an Insolvency Professional registered with the Insolvency and Bankruptcy Board of India (IBBI/Board) with Registration No. IBBI/IPA-001/IP-P00419/2017-2018/10742, who is a Professional Member of the Insolvency Professional Agency of the Indian Institute of Insolvency Professionals of ICAI.

1. Background

1.1 The National Company Law Tribunal, Mumbai Bench (AA) vide its order dated 28.07.2020, initiated Corporate Insolvency Resolution Process (CIRP) of M/s. Wadhwa Buildcon LLP (Corporate Debtor / CD) and Mr. Rakesh Kumar Tulsyan was appointed as Interim Resolution Professional (IRP). Subsequently, Mr. Vishal Ghisulal Jain was appointed as the Resolution Professional (RP) of the CD vide the AA order dated 14.10.2020. Subsequently, AA vide order dated 02.07.2024 replaced Mr. Vishal Ghisulal Jain by Mr. Manish Lalji Dawda as RP of the CD.

1.2 The Board took note of the Order of the AA dated 20.03.2024 wherein adverse observations were made against the conduct of Mr. Vishal Ghisulal Jain. The Board vide email dated 26.04.2024 sought the response of Mr. Vishal Ghisulal Jain. Further vide email dated 05.06.2024, the Board requested Mr. Vishal Ghisulal Jain to send the response and provide information to specific queries. The Board also sent a reminder vide email dated 25.06.2024. Mr. Vishal Ghisulal Jain vide email dated 03.05.2024 submitted a copy of recall application filed before the AA for recall of the Order dated 20.03.2024. However, Mr. Vishal Ghisulal Jain failed to reply to the query sent by the Board vide email dated 05.06.2024 read with reminder email dated 25.06.2024.

1.3 The Board in the absence of the specific reply of Mr. Vishal Ghisulal Jain to the observations of the the AA, examined the observations made in the order of the AA vis a vis the reasons provided by Mr. Vishal Ghisulal Jain in the recall application filed before the AA. Based on such examination, the Board formed a prima facie view that Mr. Vishal Ghisulal Jain had contravened the provisions of the Code and the Regulations made thereunder and issued a SCN to Mr. Vishal Ghisulal Jain on 29.07.2024. Mr. Vishal Ghisulal Jain had not submitted the reply to the SCN, however, vide e-mail dated 09.10.2024, he informed that he had preferred a writ petition challenging the SCN i.e., W.P./31074/2024 which is still pending before the High Court of Bombay. Mr. Vishal Ghisulal Jain had prayed for interim relief for staying the effect and operation of the SCN, however, the same has not been granted by the Hon’ble High Court of Bombay. The High Court of Bombay vide order dated 13.01.2025 had observed that the prayer made on behalf of Mr. Vishal Ghisulal Jain for keeping the suspension of his Authorization for Assignment in abeyance cannot be accepted.

1.4 The SCN and the response submitted by Mr. Vishal Ghisulal Jain were referred to the Disciplinary Committee (DC) for disposal. The hearing was initially scheduled on 13.01.2025, however, it was adjourned at the request of Mr. Vishal Ghisulal Jain on account of marriage in his family. The matter was subsequently rescheduled for hearing on 04.03.2025. Mr. Vishal Ghisulal Jain availed the opportunity of personal hearing and appeared along with his counsel. However, vide email dated 05.03.2025, Mr. Vishal Ghisulal Jain submitted that the issue in the SCN is identical to the issue that is currently pending adjudication before the NCLAT in Company Appeal (AT) (Ins) No. 828 of 2024, titled “Ankit Suresh Wadhwa v. Bank of India & Ors.”, wherein Mr. Vishal Ghisulal Jian was arrayed as Respondent No.3. Accordingly, the DC decided to keep the matter in abeyance until the adjudication of the appeal pending before the Hon’ble NCLAT. The NCLAT vide order dated 21.11.2025 had disposed the appeal being devoid of merit.

1.5 Subsequently, the hearing was again scheduled on 08.01.2026, however, it was adjourned at the request of Mr. Vishal Ghisulal Jain. The hearing was subsequently rescheduled for 19.01.2026. On 19.01.2026, Mr. Vishal Ghisulal Jain attended the hearing and appeared through his advocate, Mr. Shadab Jana. Mr. Vishal Ghisulal Jain also submitted additional written submissions on 08.02.2026.

1.6 The DC has considered the SCN, the reply to SCN, oral and written submissions of Mr. Vishal Ghisulal Jain and proceeds to dispose of the SCN.

2. Alleged contravention, submissions of Mr. Vishal Ghisulal Jain and findings of the DC.

The contravention alleged in the SCN, submissions by Mr. Vishal Ghisulal Jain and findings of the DC are summarized as follows:

2.1. Submission of ineligible resolution plan to CoC.

2.1.1. It was observed that Mr. Vishal Ghisulal Jain had received two resolution plans, one from Mr. Ankit Wadhwa partner of the suspended management of the CD on 21.01.2021, and another jointly from Mr. Bhagwandas Mulchandani and Mr. Hari Mulchandani on 27.02.2021, prior to the holding of 7th CoC meeting on 29.04.2021 and rescheduled on 06.05.2021. It was mentioned in the minutes of the 7th CoC meeting that Bank of India raised objections against conducting the meeting, protested the opening of the resolution plans and the continuation of any agenda items. However, majority of the CoC members insisted on proceeding with the opening of the resolution plan and continuing with the proceedings of the meeting. Consequently, Mr. Vishal Ghisulal Jain authorized his team member to open the resolution plans and state its contents. Nonetheless, the plans were neither discussed nor put to vote before the CoC in the said meeting.

2.1.2. In the 10th CoC meeting held on 25.03.2022, Mr. Vishal Ghisulal Jain informed the CoC about an email received from Mr. Bhagwandas Mulchandani and Mr. Hari Mulchandani (one of the PRAs) making a request to allow to submit a revised resolution plan, along with 30-day timeline extension for the same. The CoC voted in favour of allowing the submission of the revised plans.

2.1.3. Subsequently, on 30.10.2022, Indiabulls Housing Finance declared Mr. Ankit Wadhwa as a wilful defaulter. Despite this, Mr. Ankit Wadhwa submitted a fresh resolution plan on 11.11.2022, which was presented by Mr. Vishal Ghisulal Jain to the CoC, even though Mr. Ankit Wadhwa was ineligible to submit a resolution plan under Section 29A(b) of the Code, which makes wilful defaulters ineligible to be resolution applicant.

2.1.4. Mr. Vishal Ghisulal Jain was under obligation to conduct necessary due diligence of the PRAs and appraise the CoC about Mr. Ankit Wadhwa’s ineligibility under Section 29A(b) at the time of submission of resolution plan. Mr. Vishal Ghisulal Jain action to place an ineligible plan before the CoC for consideration and voting, is contrary to the provisions of Section 29A(b).

2.1.5. In view of the above, the Board was of the prima facie view that Mr. Vishal Ghisulal Jain had contravened Section 29A(b), 208(2)(a) and (e) of the Code, Regulation 7(2) (a) and (h) of the IP Regulations, Clause 14 of the Code of Conduct for Insolvency Professionals provided under First Schedule to IP Regulations (Code of Conduct).

Submissions by Mr. Vishal Ghisulal Jain.

2.1.6. Mr. Vishal Ghisulal Jain submitted that, in discharge of his duties, he has taken adequate care and conducted the necessary due diligence in the performance of his functions. Mr. Vishal Ghisulal Jain submitted that the timeline of the events and developments leading up to the Order dated 20.03.2024 is important and hence, placed on record. Further, the said events are based on the minutes of the meetings of the CoC, which have been duly approved and ratified from time to time. The timeline of events is as follows: –

| Date | Event |

| 28.07.20 | Order passed by Adjudicating Authority initiating Corporate Insolvency Resolution Process of Wadhwa Buildcon LLP (“Corporate Debtor”) |

| 14.10.20 | Order passed by Adjudicating Authority appointing Mr. Vishal Ghisulal Jain as the Resolution Professional. |

| 20.11.20 | Form G issued and published inviting Expressions of Interest. |

| 21.01.21 | Resolution plan received from Mr. Ankit Wadhwa (“PRA”) along with supporting Affidavit affirming on oath as regards compliance with Section 29A of IBC. |

| 29.04.21

& 06.05.21 |

7th CoC meeting takes place wherein plans were opened with the consent and concurrence of majority members of COC. It is pertinent to note that Bank of India tried to stall the CIR process and restrained the RP from opening the plans. |

| 25.03.22 | 10th CoC meeting takes place wherein CoC members allowed

extension of time for all prospective bidders to submit revised plans |

| 30.10.22 | Indiabulls Finance conducts proceedings under the RBI Circular and declares the PRA as a “wilful defaulter” |

| 11.11.22 | Revised resolution plan submitted by PRA. |

| 05.01.23 | Bank of India, one of the CoC members, gained knowledge of the fact that the PRA has been declared as a wilful defaulter. |

| 06.01.23 | Due Diligence Report (Section 29A) is received by the Resolution Professional inter alia prime facie opining that the PRA is compliant in terms of Section 29A as on original plan submission date i.e. 21.01.2021. |

| 18.01.23 | 14th CoC meeting is held wherein the Due Diligence Report dated 06.01.23 is shared with the members and comments are called for. |

| 20.01.23 | 15th CoC meeting is held wherein the members discuss and vote upon the plans. By majority vote of 66.42%, the CoC approved the resolution plan of the PRA |

| 27.01.23 | Resolution Professional filed I.A. No. 402/2023 before the Adjudicating Authority under Section 30 of the IBC for approval of resolution plan |

| 28.02.2023 | One IA 828 of 2023 preferred by Bank of India. |

| 20.03.24 | Order passed by the Adjudicating Authority in I.A. No. 828 of 2023 rejecting the resolution plan on the basis that PRA is ineligible under Section 29A of IBC on the basis that Indiabulls Finance has declared PRA as a wilful defaulter on 30.10.22. |

2.1.7. Mr. Vishal Ghisulal Jain submitted that the aforesaid timeline clearly demonstrates that Mr. Ankit Wadhwa, the Successful PRA had submitted its resolution plan on 21.01.2021. Notably, at that stage, the PRA had neither incurred any disqualification under Section 29A of the Code nor had it been declared a wilful defaulter by Indiabulls Housing Finance Limited. In this regard, he submitted that, in terms of Section 29A of the Code, the stage for determining ineligibility attaches at the time of submission of the resolution plan by the resolution applicant. In support of this contention, Mr. Vishal Ghisulal Jain placed reliance on the judgment of the Hon’ble Supreme Court of India in ArcelorMittal India Private Limited v. Satish Kumar Gupta.

2.1.8. Mr. Vishal Ghisulal Jain further submitted that it is pertinent to note that, in the 12th meeting of the CoC, the lenders, including Bank of India, had voted with the requisite majority to extend the timelines for submission of the revised resolution plan by the PRA. Therefore, it was clear that the revised plans submitted by the PRA did not amount to a fresh submission but were merely revisions pursuant to the extension granted by the CoC.

2.1.9. Mr. Vishal Ghisulal Jain submitted that as regards presentation of resolution plan is concerned, the role of a resolution professional is extremely limited and the Resolution Professional cannot take any decision with respect to the eligibility or ineligibility of any resolution applicant insofar as the vetting process of the plans is concerned. The Resolution Professional has no power or authority either to reject or decide the eligibility of any resolution applicant in the context of Section 29-A. The limited role of the Resolution Professional is to verify completeness of such plans by conducting due diligence. Mr. Vishal Ghisulal Jain further submitted that in terms of Section 25 of the Code, the Resolution Professional is bound to present all plans before the CoC and cannot omit to or reject any plan which may or may not be complete or eligible under section 29-A of IBC.

2.1.10. Mr. Vishal Ghisulal Jain further submitted that the Hon’ble Supreme Court in Arcellor Mittal (Para 81) has laid down that for the purpose of examination and vetting the prospective resolution applicants the concerned Resolution Professional must take guidance from a due diligence report. Accordingly, Mr. Vishal Ghisulal Jain tabled the proposal before the CoC to carry out a due diligence exercise through appointment of a third-party professional appointment of such a third-party professional was approved and ratified by the CoC in its 11th meeting held on 01.10.2022.

2.1.11. Mr. Vishal Ghisulal Jain submitted that the Due Diligence Report was received on 06.01.2023. The said report examined the disqualification criteria prescribed under Section 29A of the Code including the aspect relating to disqualification under Section 29A(b) concerning wilful default, and opined, on the basis of information and documents available in the public domain, that the PRA did not suffer from any ineligibility under Section 29A of the Code. Mr. Vishal Ghisulal Jain further submitted that the said Due Diligence Report, categorically opined that the PRA was eligible to submit its resolution plan, was placed before the CoC in its 14th meeting held on 18.01.2023, wherein Bank of India was also present. During the said meeting, the report was deliberated upon, and comments from CoC members were invited. However, none of the members of the CoC, including Bank of India, raised any objection or furnished any comment regarding the alleged ineligibility of the PRA.

2.1.12. Mr. Vishal Ghisulal Jain submitted that, under the Code, the Resolution Professional has no power or authority to decide or reject the eligibility of a resolution applicant under Section 29A of the Code, and that his role is limited to verifying the completeness of the resolution plans by conducting due diligence. Mr. Vishal Ghisulal Jain submitted that any opinion expressed by the Resolution Professional on eligibility is merely prima facie in nature and is neither conclusive nor binding upon the CoC. In terms of Sections 25 and 30(2) of the Code read with Regulation 36A of the CIRP Regulations, the RP is obligated to place all resolution plans before the CoC and cannot reject or omit any plan on the ground of alleged ineligibility.

2.1.13. Mr. Vishal Ghisulal Jain further submitted that, in compliance with Regulation 36A(8), due diligence was conducted on the basis of material available on record, and there was nothing to indicate that any PRA, was ineligible under Section 29A. Despite this, Mr. Vishal Ghisulal Jain sought to appoint a legal professional to vet eligibility, however, the agenda for such appointment was repeatedly rejected by the CoC, including by Bank of India, in its 7th, 10th and 11th meetings. Ultimately, all resolution plans, including that of the PRA, were placed before the CoC for voting on 20.01.2023, pursuant to which the resolution plan submitted by the PRA was approved by 66.42% of the voting share of the CoC, though Bank of India voted against the same.

2.1.14. Mr. Vishal Ghisulal Jain submitted that although the PRA was declared a wilful defaulter on 30.10.2022, the fact of such declaration was neither disclosed nor communicated by the PRA to him at any point in time. Mr. Vishal Ghisulal Jain further submitted that, in terms of the affidavit furnished by the PRA pursuant to Section 29A of the Code, the PRA was under a specific obligation to forthwith intimate the RP and the CoC, if it incurred any ineligibility under Section 29A of the Code. However, no such disclosure was made.

2.1.15. Mr. Vishal Ghisulal Jain further submitted that the declaration of the PRA as a wilful defaulter was not within his knowledge and could not reasonably have been within his knowledge, since dissemination of such information by banks is made only to Credit Information Companies (CICs) in terms of the applicable regulatory framework. Mr. Vishal Ghisulal Jain further submitted that the Reserve Bank of India’s Master Directions on Wilful Defaulters dated 01.07.2014 mandate reporting of wilful defaulters by banks and financial institutions exclusively to CICs (and in certain cases to RBI), and that dissemination of such information is limited in nature, with only suit-filed cases being made publicly available on CIC websites. In view thereof, the information relating to the PRA’s alleged wilful default was neither publicly accessible nor available to the RP in the ordinary course. Further, Mr. Vishal Ghisulal Jain had conducted an extensive search and found that the name of the PRA did not appear as a wilful defaulter on the public databases of CRIF High Mark Credit Information Services Private Limited, Equifax Credit Information Services Private Limited, Experian Credit Information Company of India Private Limited, or Credit Information Bureau (India) Limited (CIBIL).

2.1.16. Mr. Vishal Ghisulal Jain submitted that the Due Diligence Report, which opined that the PRA was eligible under Section 29A of the Code was placed before the CoC on 18.01.2023, and the members, including Bank of India, were specifically invited to provide their comments, however, no objection regarding the alleged ineligibility of the PRA was raised at that stage. Mr. Vishal Ghisulal Jain submitted that it was only after the Resolution Professional filed I.A. No. 402/2023 under Section 30 of the Code for approval of the resolution plan that Bank of India, for the first time, raised an objection alleging that the PRA was ineligible under Section 29A, and in support thereof filed I.A. No. 828 of 2023 annexing a CIBIL report. Significantly, the said CIBIL report indicated that it had been available with Bank of India since 05.01.2023, yet this fact was not disclosed to him or to the CoC at the relevant time. Mr. Vishal Ghisulal Jain further submitted that, since such credit information was neither available in the public domain nor accessible to the RP under the applicable legal framework, there was no manner in which he could have known or discovered the alleged disqualification of the PRA.

2.1.17. Mr. Vishal Ghisulal Jain submitted that there was no delay or deliberate omission on his part in placing the resolution plans before the CoC. The resolution plan was received on 21.01.2021, and repeated efforts were made thereafter to convene meetings of the CoC, however, meetings scheduled in February and early March 2021 were deferred at the instance of Bank of India, and the 6th CoC meeting could ultimately be held only on 25.03.2021. He further submitted that subsequent reconstitutions of the CoC took place pursuant to admission and exclusion of claims, including orders passed by the AA and the NCLAT which altered the voting share from time to time. After March 2021, Bank of India did not hold the requisite majority to unilaterally approve or reject any resolution plan, and by the time the revised resolution plans were received on 05.12.2022, Bank of India voting share stood at 31.80%. The resolution plans, along with vetting reports, were placed before the CoC in its 14th meeting held on 18.01.2023, and were thereafter put to vote in the 15th meeting held on 20.01.2023.

Analysis and findings of the DC.

2.1.18. Section 29A of the Code provides as follows:

29A. Persons not eligible to be resolution applicant. –

A person shall not be eligible to submit a resolution plan, if such person, or any other person acting jointly or in concert with such person—

(a) is an undischarged insolvent;

(b) is a wilful defaulter in accordance with the guidelines of the Reserve Bank of India issued under the Banking Regulation Act, 1949 (10 of 1949);

……

2.1.19. Regulation 36A(8) of the Insolvency and Bankruptcy Board of India (Insolvency Resolution Process For Corporate Persons) Regulations, 2016 (‘CIRP Regulation’) provides as follows:-

“36A. Invitation for expression of interest.

………

(8) The resolution professional shall conduct due diligence based on the material on record in order to satisfy that the prospective resolution applicant complies with- (a) the provisions of clause (h) of sub-section (2) of section 25; (b) the applicable provisions of section 29A, and (c) other requirements, as specified in the invitation for expression of interest.

……

2.1.20. Section 29A(b) of the Code expressly disqualifies a person from submitting a resolution plan if such person is a wilful defaulter in accordance with the guidelines of the Reserve Bank of India issued under the Banking Regulation Act, 1949. The provision applies not only to the person directly but also to any connected person as contemplated under the Explanation to Section 29A of the Code. Regulation 36A of the CIRP Regulations requires the RP to conduct due diligence to verify the eligibility of resolution applicants under Section 29A of the Code.

2.1.21. The DC notes Mr. Vishal Ghisulal Jain’s contention that Mr. Ankit Wadhwa originally submitted resolution plan on 21.01.2021, and at that time, he had not been declared a wilful defaulter and consequently was not ineligible under Section 29A(b) of the Code at that time. The DC notes that Mr. Ankit Wadhwa was declared a wilful defaulter by Indiabulls Housing Finance Limited on 30.10.2022 and submitted the revised resolution plan on 11.11.2022, which was twelve days after he had been declared as wilful defaulter.

2.1.22. The DC also notes that the AA in its order dated 20.03.2024 in I.A 828 of 2023 in C.P. (IB) No. 2946 of 2019 had also dealt with Mr. Vishal Ghisulal Jain’s contention that Mr. Ankit Wadhwa originally submitted resolution plan on 21.01.2021 and only a revised resolution plan was submitted on 11.11.2022 which is in continuation of the resolution plan dated 21.01.2021. In this regard, Mr. Vishal Ghisulal Jain submitted that, in terms of Section 29A of the Code, the stage for determining ineligibility attaches at the time of submission of the resolution plan by the resolution applicant i.e., 21.01.2021 and on that particular date, Mr. Ankit Wadhwa had not been declared a wilful defaulter. This submission was considered by the AA and decided as follows:-

“36. After having appreciated the arguments advance by the Ld. Counsel for the RA and having gone through the documents submitted, it is evident that though the Resolution Plan was submitted on 21.01.2021. This plan was never put up before CoC for consideration not ever opened/discussed or voted upon. The plan put up before CoC was a fresh Plan submitted by Respondent No 6 on 11.11.2022. It cannot by any stretch of imagination be stated to be a negotiated or revised Resolution Plan as the earlier plan was never considered at all. Since it was a fresh plan submitted on 11.11.2022 the eligibility of the SRA /Respondent No. 6 under Section 29A of IBC was required to be seen on the date of submission of Plan i.e. 11.11.2022. The fact is on 11.11.2022 the RA /Respondent no. 6 was ineligible under Section 29A of IBC to submit the Resolution Plan as he was declared willful defaulter on 30.10.2022. Thus the said plan submitted by the SRA could not be approved by the CoC.

37. It is pertinent to note the minutes of the CoC wherein it was held as under –“..Resolution Plan version 1.0 was submitted on 21st January, 2021 which was not taken to consideration as the substantial time was elapsed and many circumstances changed with respect to claims, intrinsic value of the project, estimated cost escalation etc. which directly or indirectly affecting the Resolution Plan amount. RP had sought extension and exclusion from the Hon’ble NCLT Mumbai and the same was allowed. Further the RP allowed to file a Resolution Plan by 11th November 2022.”

Thus, from the perusal of the above it is evident that on 11.11.2022. It was virtually a new plan placed before CoC by the RA. Thus it is this date i.e. 11.11.2022 which is material so as to check the eligibility of the Resolution Applicant under Section 29A of the Code and in the present case the Resolution Professional withheld the information of the eligibility of the Resolution Applicant from the CoC as the plan of the RA may not have been approved by the CoC. If the factum of his having being declared as a ‘willful defaulter’ had come to the knowledge of the CoC. Hence, the requisite information was withheld from the CoC.”

2.1.23. The DC notes that the observations of the AA make it clear that the resolution plan dated 11.11.2022 cannot be treated as a mere continuation or revision of the earlier plan submitted on 21.01.2021, since the initial plan was never placed before or considered by the Committee of Creditors. The DC is in agreement with the observation of the AA that the plan dated 11.11.2022 cannot by any stretch of imagination be stated to be a negotiated or revised Resolution Plan as the earlier plan was never considered at all. Consequently, the relevant date for assessing eligibility under Section 29A of the Code is 11.11.2022, on which date Mr. Ankit Wadhwa stood disqualified due to his classification as a wilful defaulter on 30.10.2022. This ineligibility under Section 29A of the Code, not only renders the plan ineligible for approval but also highlights a serious lapse on the part of Mr. Vishal Ghisulal Jain.

2.1.24. The DC notes that the act of submitting a revised plan on 11.11.2022 constitutes, in effect, a fresh submission of a resolution plan, and the eligibility of the resolution applicant must necessarily be tested as on that date as well i.e. on 11.11.2022.

2.1.25. The DC notes that Mr. Ankit Wadhwa had provided affidavit in compliance with Section 29A of the Code, wherein he was obligated to reveal such disqualification to the Resolution Professional and the Committee of Creditors. The relevant extract of the given affidavit is reproduced below:-

“11. That if, at any time after the submission of this affidavit and before the approval of the Resolution Applicant’s resolution plan by the Hon’ble National Company Law Tribunal under the Code, the resolution applicant that becomes ineligible to be a resolution applicant as per the provisions of the Code (and in particular Section 29-A of the code), the fact of such ineligibility shall be forthwith brought to the attention of the RP and CoC.”

2.1.26. The DC notes that it is evident from the contents of the affidavit submitted by the PRA that the eligibility of the PRA must be ensured at every stage, up to the approval of the resolution plan by the Adjudicating Authority. Accordingly, merely being eligible under Section 29A of the Code and submitting an affidavit at the time of submission of the resolution plan does not discharge the responsibility of the Resolution Professional to ensure the continued eligibility of the PRA under Section 29A of the Code. Such responsibility extends to all subsequent stages, including at the time of submission of any revised resolution plan and at the time of filing the application seeking approval of the resolution plan before the AA, and continues until the approval of the plan by the AA.

2.1.27. The DC notes Mr. Vishal Ghisulal Jain’s contention that the Due Diligence Report received on 06.01.2023 opined that the PRA was compliant with Section 29A as of 21.01.2021 i.e., the date of original plan submission. The DC notes that the Due Diligence Report admittedly assessed the eligibility of the PRA particularly on the basis of the affidavit for no-disqualification dated 30.11.2020 under Section 29A of the Code as submitted by Mr. Ankit Wadhwa as of the date of the original submission and did not address the disqualification arising from the wilful defaulter declaration on 30.10.2022 and the eligibility as on submission of revised resolution plan on 11.11.2022. The relied upon due diligence exercise that is limited to a date i.e., 21.01.2021 has not considered a subsequent material event i.e., declaration of Mr. Ankit Wadhwa on 30.10.2022 as wilful defaulter cannot constitute adequate compliance with Mr. Vishal Ghisulal Jain’s obligations as vested under the Code, 2016 to ensure that the PRA is compliant with Section 29A of the Code. Accordingly, the DC cannot accept Mr. Vishal Ghisulal Jain’s reliance on the Due Diligence Report for ascertaining the eligibility of the PRA under Section 29A of the Code.

2.1.28. The DC further notes Mr. Vishal Ghisulal Jain’s contention that the Bank of India, was invited to comment upon the Due Diligence Report and failed to raise any objection. The DC notes that RP’s duties are not contingent upon the CoC flagging deficiencies. The Code places a direct and independent obligation upon the RP to conduct due diligence and to inform the CoC of any material ineligibility. The DC notes that mere presentation of the Due Diligence Report before the CoC does not absolve Mr. Vishal Ghisulal Jain of his independent obligations to conduct due diligence of the PRA under the Code and the Regulations made thereunder. Mr. Vishal Ghisulal Jain cannot shift or dilute his obligation of due diligence by pointing to the silence or inaction of CoC members.

2.1.29. The DC notes Mr. Vishal Ghisulal Jain’s contention that Bank of India remained silent despite having knowledge of the PRA’s wilful defaulter status since 05.01.2023. The DC notes that such conduct of a CoC member cannot and does not mitigate Mr. Vishal Ghisulal Jain’s own independent statutory obligations to verify the eligibility of the PRA. The DC further notes that Mr. Vishal Ghisulal Jain is duty bound to discharge his duties independently of the conduct of the CoC members, and the failure of Bank of India to disclose this information does not constitute a defence available to him.

2.1.30. Section 25 of the Code lays down the duties of the Resolution Professional. The relevant extract is:

“25. Duties of resolution professional. –

(1) It shall be the duty of the resolution professional to preserve and protect the assets of the corporate debtor, including the continued business operations of the corporate debtor.

(2) For the purposes of sub-section (1), the resolution professional shall undertake the following actions, namely:

…..

(h) invite prospective resolution applicants, who fulfil such criteria as may be laid down by him with the approval of committee of creditors, having regard to the complexity and scale of operations of the business of the corporate debtor and such other conditions as may be specified by the Board, to submit a resolution plan or plans.

(i) present all resolution plans at the meetings of the committee of creditors. ”

2.1.31. Section 25 of the Insolvency and Bankruptcy Code, 2016 provides that it shall be the duty of the Resolution Professional to preserve and protect the assets of the corporate debtor and, for that purpose, to undertake various functions including inviting prospective resolution applicants and presenting all resolution plans at the meetings of the Committee of Creditors.

2.1.32. The DC notes the contention of Mr. Vishal Ghisulal Jian that the role of a resolution professional in presentation of resolution plan is extremely limited and he is duty bound to put the resolution plans before the CoC. The DC notes that this limited role does not imply a mere mechanical forwarding of all plans. The statutory framework, when read harmoniously with Section 30(2) of the Code, imposes an obligation on the Resolution Professional to examine each resolution plan and conduct due diligence to assess whether it complies with the provisions of the Code, including the eligibility criteria laid down under Section 29A. The DC notes that while the Resolution Professional is duty-bound to place all resolution plans before the CoC in terms of Section 25(2)(i) of the Code, such presentation must be accompanied by a clear indication of whether the plans are compliant with the requirements of the Code. The Resolution Professional must, therefore, inform the CoC of any deficiencies or ineligibility arising under Section 29A, based on the due diligence undertaken. Section 30(3) of the Code provides that the resolution professional shall present to the committee of creditors for its approval such resolution plans which confirm the conditions referred to in sub-section (2). Hence, the Resolution Professional can present only the compliant plan(s) for the approval of the CoC, while it has to present all plans before the CoC.

2.1.33. The DC notes that Mr. Vishal Ghisulal Jain had placed reliance on the Hon’ble Supreme Court judgement in Arcelor Mittal (Para 80) to support the contention that under Section 25(2)(i), the Resolution Professional is required to present all resolution plans at the meetings of the Committee of Creditors. The DC had perused the judgement relied upon and find the judgement further clarified that the Resolution Professional is not required to take any decision, but to ensure that the resolution plans submitted are complete in all respects before they are placed before the CoC. The judgement also clarified that the fact that it is the duty of the Resolution Professional to confirm that a resolution plan does not contravene any of the provisions of law for the time-being in force, including Section 29A of the Code, and thereafter a prima facie opinion is to be given to the Committee of Creditors. In this case, no such prima facie opinion regarding the plan being not compliant was given to the CoC and therefore the reliance on the judgement does not help his case.

2.1.34. The DC notes that though the ultimate decision-making authority with regard to the approval of the Resolution Plan rests with the CoC, the scheme of the Code does not permit consideration or approval of a resolution plan submitted by an ineligible PRA. Consequently, no voting can validly take place on a resolution plan that is found to be ineligible under Section 29A based on the due diligence conducted by the RP. The requirement of eligibility is a threshold condition, and permitting a vote on such a plan would be contrary to the mandatory provisions of the Code. The DC further notes that the due diligence exercise was limited to a specific date, i.e., 21.01.2021. However, the revised resolution plan was submitted on 11.11.2022, by which time a substantial period had elapsed. Accordingly, Mr. Vishal Ghisulal Jain, being the Resolution Professional, ought to have conducted due diligence considering the contemporaneous facts. Therefore, the contention of Mr. Vishal Ghisulal Jain cannot be accepted.

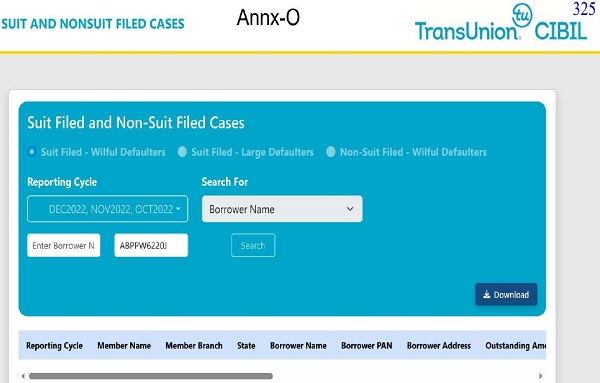

2.1.35. The DC notes the submission of Mr. Vishal Ghisulal Jain that the declaration of Mr. Ankit Wadhwa as a wilful defaulter was neither within his knowledge nor could reasonably have been within his knowledge, as dissemination of such information by banks is restricted to Credit Information Companies (CICs) under the applicable regulatory framework. Mr. Vishal Ghisulal Jain further submitted that only limited information, such as suit-filed cases, is available in the public domain. The DC also notes Mr. Vishal Ghisulal Jain’s submission that he had conducted an extensive search of publicly accessible databases of CICs, including CRIF High Mark Credit Information Services Private Limited, Equifax Credit Information Services Private Limited, Experian Credit Information Company of India Private Limited, and Credit Information Bureau (India) Limited (CIBIL), and found that the name of the PRA did not appear as a wilful defaulter. In this regard, he has furnished the following screenshot as a proof of the result of extensive search in the public domain, wherein he could not find any wilful defaulter with the name of Mr. Ankit Suresh Wadhwa as well as by DIN of Mr. Ankit Suresh Wadhwa (DIN – 02781013) :-

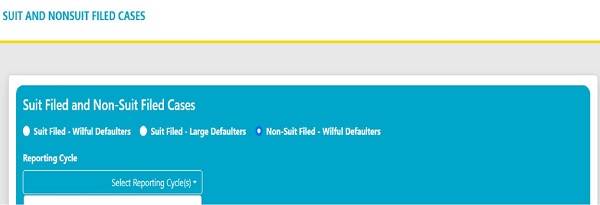

2.1.36. In this regard, the DC notes that details of wilful defaulters are available in the public domain, including both suit-filed and non-suit-filed cases, on the website https://suit.cibil.com/. The DC had conducted search to check whether the list of wilful defaulters under the category of non-suit filed is available in the

Accordingly, the submission of Mr. Vishal Ghisulal Jain that only limited information, such as suit-filed cases, is available in the public domain, cannot be accepted.

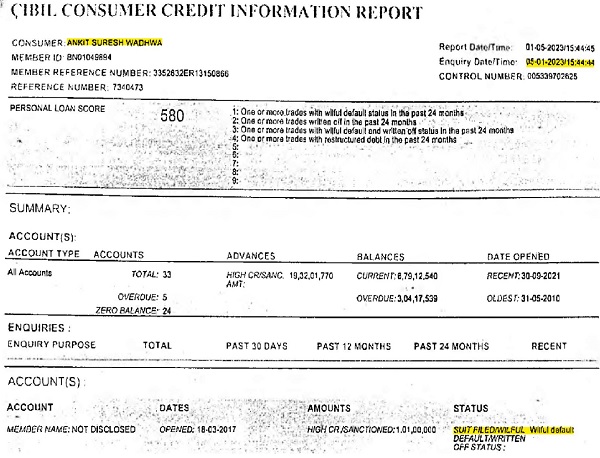

2.1.37. The Screenshot of Mr. Ankit Wadhwa’s CIBIL report dated 05.01.2023 as provided by Mr. Vishal Ghisulal Jain is extracted below:-

2.1.38. On perusal of CIBIL report dated 05.01.2023 as submitted by Mr. Vishal Ghisulal Jain, the DC notes that the status is mentioned as ‘Suit filed/ wilful default”. Hence, the contention of Mr. Vishal Ghisulal Jain that case of Mr. Ankit Suresh Wadhwa will not be displayed as it is a non-suit filed case is not correct as the extract of the CIBIL report shows that Mr. Ankit Suresh Wadhwa has been declared wilful defaulter in a suit filed case.

2.1.39. The DC further refers to the Reserve Bank of India (Treatment of Wilful Defaulters and Large Defaulters) Directions, 2024, particularly Clause 11 of CHAPTER III Reporting of Wilful Defaulters and Large Defaulters on “Treatment of compromise settlements,” which provides as follows:

“(1) Any account included in the LWD, where the lender/ARC has entered into a compromise settlement with the borrower, shall be removed from the LWD only when the borrower has fully paid the compromise amount;

(2) till such time as only part payment is made, the name of the borrower shall not be removed from the LWD even if the outstanding amount falls below the prescribed threshold;

(3) such compromise settlement shall be in accordance with the board-approved policy of the lender/ARC; and

(4) such settlement shall be without prejudice to the continuation of criminal proceedings against the wilful defaulter.”

The DC notes from the above directions that upon full payment of the compromise amount, the borrower’s name is removed from the List of Wilful Defaulters (LWD). In the present case, Mr. Ankit Suresh Wadhwa had entered into a compromise settlement with the financial creditor and has fully paid the outstanding dues as recorded in the Hon’ble NCLAT order dated 21.11.2025. Therefore, the name of Mr. Ankit Suresh Wadhwa will not appear in the List of Wilful Defaulters after he paid the outstanding dues which is before the NCLAT order dated 21.11.2025 as this order records this fact. Therefore, search on this website after this date will not show his name as wilful defaulter.

In this context, the DC notes that the submission of Mr. Vishal Ghisulal Jain that he had conducted an extensive search of publicly accessible databases of CICs, including CRIF High Mark Credit Information Services Private Limited, Equifax Credit Information Services Private Limited, Experian Credit Information Company of India Private Limited, and CIBIL, and did not find the name of the PRA as a wilful defaulter. Mr. Vishal Ghisulal Jain not being able to find the find the name of Mr. Ankit Wadhwa in the List of Wilful Defaulters is because the same is required to be removed from the List of Wilful Defaulters upon completion of the settlement.

The screenshot reproduced above in para 2.1.35 shows that the search has been conducted on 08.02.2026. Since, Mr. Vishal Ghisulal Jain has searched the database on 08.02.2026, the same will not be visible on the list of wilful defaulters. However, if the database had been checked on the date of due diligence report dated 06.01.2023 or date of submission of the revised resolution plan i.e., 11.11.2022, the name of Mr. Ankit Wadhwa would have appeared as wilful defaulter making him ineligible to be a Prospective Resolution Applicant.

2.1.40. The DC notes that by placing the revised resolution plan of Mr. Ankit Wadhwa before the CoC for consideration and voting on 20.01.2023, without first apprising the CoC of the PRA’s disqualification under Section 29A(b) of the Code arising from declaration of Mr. Ankit Wadhwa as a wilful defaulter on 30.10.2022 by Indiabulls, Mr. Vishal Ghisulal Jain failed to discharge his duties as required under the Code and the Code of Conduct. This failure resulted in the CoC voting upon and approving a plan submitted by an ineligible resolution applicant, which was subsequently rejected by the Adjudicating Authority by its Order dated 20.03.2024 in I.A. No. 828/2023, thereby causing significant delay, additional cost, and prejudice to the CIRP. The DC further notes that although the Resolution Professional is required to present all resolution plans received to the CoC, this obligation does not absolve Mr. Vishal Ghisulal Jain of his concurrent duty to inform the CoC of any known or reasonably discoverable ineligibility of a resolution applicant before the plan is placed for consideration and voting.

2.1.41. In view of the above, the DC finds Mr. Vishal Ghisulal Jain in contravention of Section 29A(b), 208(2)(a) and (e) of the Code, Regulation 7(2) (a) and (h) of the IP Regulations, Clause 14 of the Code of Conduct for Insolvency Professionals provided under First Schedule to IP Regulations (Code of Conduct).

2.2.Non-Cooperation with the IA

2.2.1. It is observed that the Board had sought information from Mr. Vishal Ghisulal Jain, vide email dated 05.06.2024, regarding the steps that were undertaken by Mr. Vishal Ghisulal Jain to conduct due diligence of PRAs to ascertain their eligibility under Section 29A. In response, Mr. Vishal Ghisulal Jain caused to be replied, vide email dated 05.06.2024, from Mr. Biswaksen Panda that Mr. Vishal Ghisulal Jain will submit the response in 3-4 days. As no response was received from Mr. Vishal Ghisulal Jain’s end, the Board, vide email dated 25.06.2024, sent a reminder, requesting for submission of Mr. Vishal Ghisulal Jain’s reply. However, Mr. Vishal Ghisulal Jain failed to provide the requisite information till date.

2.2.2. In view of the above, the Board was of the prima facie view that Mr. Vishal Ghisulal Jain had contravened Regulation 7(2)(a) and (h) of the IP Regulations, Clause 19 of the Code of Conduct for Insolvency Professionals.

Submissions by Mr. Vishal Ghisulal Jain.

2.2.3. Mr. Vishal Ghisulal Jain submitted that he had acknowledged, vide his email dated 03.08.2024, that the information sought by the Board through emails dated 26.04.2024 and 05.06.2024 was already contained in the Recall Application submitted by him vide his email dated 03.05.2024.

2.2.4. Mr. Vishal Ghisulal Jain further submitted that the present allegation is consequential to the allegation regarding submission of an ineligible resolution plan to the CoC. Mr. Vishal Ghisulal Jain contended that since there is no cogent reason or basis for sustaining the allegation relating to submission of an ineligible resolution plan to the CoC, the present allegation of non-cooperation would not survive and would automatically dissipate once the primary allegation is decided.

2.2.5. Mr. Vishal Ghisulal Jain submitted that, as the information and documents sought by the Board were provided vide emails dated 03.05.2024 and 31.08.2024, as well as through additional written submissions, the alleged contravention on account of non-cooperation stands cured.

Analysis and findings of the DC.

2.2.6. Regulation 8 of the Inspection and Investigation Regulations mandates a resolution professional to provide all assistance to the IA during the process of investigation and states as follows:

“8. Conduct of Investigation

(4) It shall be the duty of the service provider and an associated person to produce before the Investigating Authority such records in his custody or control and furnish to the Investigating Authority such statements and information relating to its activities within such time as the Investigating Authority may require…. …

(8) It shall be the duty of the service provider and an associated person to give to the Investigating Authority all assistance which the Investigating Authority may reasonably require in connection with the investigation”.

2.2.7. Further Clause 19 of the Code of Conduct provides that:

“19. An insolvency professional must provide all information and records as may be required by the Board or the insolvency professional agency with which he is enrolled.”

2.2.8. The DC notes that the Board, vide email dated 05.06.2024, had sought clarification from Mr. Vishal Ghisulal Jain regarding the manner in which due diligence of the PRAs was conducted, specifically the steps undertaken to ascertain their eligibility under Section 29A. Subsequently, Mr. Vishal Ghisulal Jain, vide email dated 05.06.2024, stated that he would provide his reply within 3–4 days. However, upon non-receipt of the said reply, a reminder email dated 25.06.2024 was sent to him seeking submission of his response to the query. Despite the same, Mr. Vishal Ghisulal Jain failed to furnish any reply to the aforementioned query.

2.2.9. The DC notes the submission of Mr. Vishal Ghisulal Jain that he had vide his email dated 03.08.2024, submitted that the information sought by the Board through emails dated 03.05.2024 and 05.06.2024, was already contained in the Recall Application submitted by him vide his email dated 03.05.2024. The DC notes that the matter was examined based on the reasons provided by Mr. Vishal Ghisulal Jain in his application filed before the NCLT seeking recall of the said NCLT order. The DC also notes that Mr. Vishal Ghisulal Jain cannot conveniently rely solely on the recall application filed before the AA to enable the Board to extract the required information. Mr. Vishal Ghisulal Jain was obligated to fully cooperate and provide specific replies to the queries and clarifications sought by the Board.

2.2.10. The DC notes the contention of Mr. Vishal Ghisulal Jain that the information sought by the Board vide email dated 05.06.2024 was already furnished through his recall application submitted on 03.05.2024. The DC notes that the Board, through its email dated 05.06.2024, had raised specific queries regarding the manner in which due diligence of the PRAs was conducted, particularly with respect to their eligibility under Section 29A, and Mr. Vishal Ghisulal Jain had acknowledged the same and sought time to provide a response within 3–4 days. Despite such assurance, and even after a reminder dated 25.06.2024, he failed to furnish any reply. The DC notes that merely relying on a previously submitted recall application does not discharge his obligation to respond to the Board’s specific queries, specially when he has sought time to provide response. Even if Mr. Vishal Ghisulal Jain was of the view that the information sought was already available on record, he was duty-bound to explicitly inform the Board accordingly, either by providing a clear response or by making specific references to the relevant portions of the earlier submission. Mr. Vishal Ghisulal Jain’s failure to do so demonstrates a lack of adequate cooperation with the Board, which cannot be justified on the ground that the information had allegedly been furnished earlier.

2.2.11. The DC deems it pertinent to mention that the Board was established under Section 188 of the Code. The Board has a statutory mandate to oversee the processes under the Code and monitor the performance of Insolvency Professionals, who are the main driving force of such processes. Section 196 of the Code vests powers and functions on the Board to regulate and monitor the performance of Insolvency Professionals. The monitoring of regulated entities through inspections and investigations is an important function which is exercised by the Board. It is the duty of all regulated entities or Insolvency Professionals registered with the Board to cooperate with the Board in exercising its statutory mandate for the overall purpose of achieving the objectives of the Code. Not extending support to the Board is an act of dissidence by such an Insolvency Professional and makes mockery of the statutory obligations enshrined under the Code.

2.2.12. In light of the above, the DC is of the view that Mr. Vishal Ghisulal Jain is in contravention of, Regulation 7(2)(a) and (h) of the IP Regulations read with Clause 18 and 19 of the Code of Conduct for Insolvency Professionals.

3. ORDER

3.1. In view of the foregoing discussions, the DC finds that Mr. Vishal Ghisulal Jain has failed to conduct contemporaneous due diligence to verify the eligibility of the PRA under Section 29A of the Code as on the date of submission of the resolution plan before the CoC. Further, Mr. Vishal Ghisulal Jain has failed in extending necessary cooperation to the IA during the investigation process.

3.2. The DC in exercise of the powers conferred under Section 220 of the Code read with Regulation 13 of the IBBI (Inspection and Investigation) Regulations, 2017 hereby suspends the registration of Mr. Vishal Ghisulal Jain (Registration No. IBBI/IPA-001/IP-P00419/2017-2018/10742) for a period of two years.

3.3. This Order shall come into force on expiry of 30 days from the date of its issue.

3.4. A copy of this order shall be sent to the CoC/ Stakeholders Consultation Committee of all the Corporate Debtors in which Mr. Vishal Ghisulal Jain is providing his services, if any and the CoC/SCC may decide on the continuation of services of Mr. Vishal Ghisulal Jain.

3.5. A copy of this order shall be forwarded to the Indian Institute of Insolvency Professionals of ICAI where Mr. Vishal Ghisulal Jain is enrolled as a member.

3.6. A copy of this order shall also be forwarded to the Registrar of the Principal Bench of the National Company Law Tribunal, New Delhi, for information.

3.7. A copy of this order shall be forwarded to the Managing Director & CEO of the Bank of India to take necessary action after inquiring as to why the authorised CoC member of Bank of India had not apprised the CoC/ Mr. Vishal Ghisulal Jain in the 15th CoC meeting held on 20.01.2023 considering the resolution plan(s) about the ineligibility of Mr. Ankit Wadhwa in the CoC meeting when they had found out that he was ineligible as per CIBIL report dated 05.01.2023.

3.8. Accordingly, the show cause notice is disposed of.

Sd/-

(Sandip Garg)

Whole Time Member

Insolvency and Bankruptcy Board of India

Place: New Delhi

Dated: 22 April 2026