Introduction

The growing adoption of the new tax regime has led to a widespread perception that it is more beneficial for salaried individuals due to lower tax rates and simplicity.

However, in 2025, with evolving compensation structures and renewed relevance of certain allowances under the Income Tax framework, this assumption may not hold true in all cases.

Where income is structured efficiently and eligible deductions are optimally utilised, the old tax regime can still result in significantly lower tax liability.

This article presents a case study illustrating how a salaried individual earning ₹20.54 lakh annually can potentially achieve nil tax liability under the old tax regime, subject to certain assumptions.

Objective of the Analysis

- To evaluate the impact of exemptions and deductions under the old tax regime

- To compare the treatment of income under the old and new tax regimes

- To illustrate how structured income components can materially reduce taxable income

Case Context

Consider a salaried individual earning a gross annual income of ₹20.54 lakh.

Under a structured compensation framework and by availing applicable exemptions and deductions, the taxable income under the old tax regime can be significantly reduced.

What Has Changed?

For a long time, several allowances under the old tax regime had lost relevance because their limits were too low to make any meaningful impact.

That is now beginning to change.

Recent revisions and structured utilisation of allowances have made them meaningful again in the context of tax planning:

- Child Education Allowance has been increased from ₹100 per month per child to ₹3,000 per month.

For two children, this translates to an annual exemption of ₹72,000. - Meal Allowance has been enhanced from ₹50 per meal to ₹200 per meal.

Assuming 22 working days and two meals per day, this results in an annual exemption of ₹1,05,600. - Gift Allowance has been revised from ₹5,000 to ₹15,000 per annum.

- Hostel Allowance has increased from ₹300 to ₹9,000 per month per child.

For two children, this amounts to ₹2,16,000 annually. - Employer Loan Benefit: Interest on loans provided by the employer is exempt up to ₹2,00,000 per annum.

In addition, the scope of House Rent Allowance (HRA) has expanded.

Cities such as Bangalore, Hyderabad, Pune, and Ahmedabad are now eligible for the higher exemption threshold of 50% of basic salary, a benefit that was earlier restricted to metro cities.

Individually, these changes may appear incremental.

Collectively, they can significantly reduce taxable income.

A Comparative View: Old vs New Tax Regime

The key distinction between the two regimes lies in the treatment of exemptions and deductions.

Under the new regime, most exemptions are not available, and tax benefits arise primarily from lower slab rates.

Under the old regime, higher tax rates are offset by the availability of multiple deductions and exemptions.

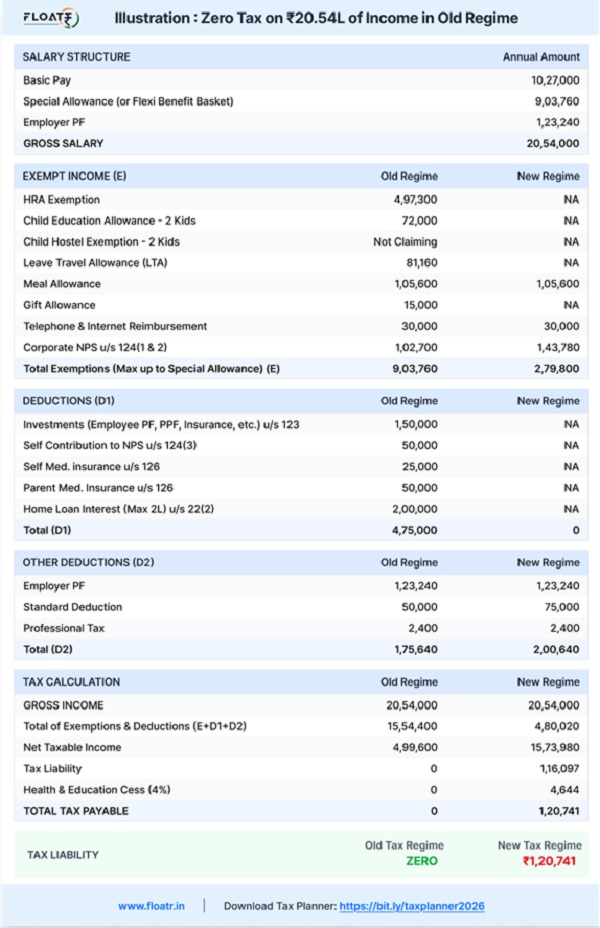

Illustration: Tax Computation for ₹20.54 Lakh Salary

The following illustration demonstrates the impact of exemptions and deductions under both regimes, assuming a structured salary and eligible claims.

It enables:

- Comparison of tax liability under both regimes

- Identification of applicable exemptions and deductions

- Evaluation of tax optimisation opportunities

Note: This illustration does not consider education loan interest.

If an education loan is also serviced, taxable income can reduce even further, as there is no upper limit on deduction under Section 80E.

Key Assumptions

The above illustration is based on the following assumptions:

- Salaried individual with HRA eligibility

- Structured salary including allowances

- Two dependent children

- Full utilisation of Section 80C

- Health insurance premium claimed under Section 80D

- Housing loan interest claimed under Section 24

- No education loan considered in base case

Actual tax outcomes may vary depending on individual circumstances.

Key Observations

- The old tax regime continues to provide significant benefits where multiple deductions are available

- The new tax regime may be more suitable for individuals with minimal or no deductions

- The difference between the two regimes increases as income and financial commitments increase

- Tax liability is influenced more by income structure than by income level alone

Practical Implication

Effective tax optimisation requires a detailed and structured approach.

It is not just about choosing between tax regimes—but about understanding how income is structured, what exemptions are applicable, and how deductions can be optimally utilised.

A structured tax planning approach can help individuals:

- Evaluate both regimes accurately

- Identify eligible exemptions and deductions

- Optimise their overall tax outcome

Conclusion

The choice between the old and new tax regimes is not absolute.

While the new regime offers simplicity, the old regime—particularly in the current context—remains highly relevant for individuals with structured income and eligible deductions.

This case study demonstrates that, under specific structured conditions, it is possible to achieve zero tax liability even at higher income levels.

A comparative evaluation, rather than a default assumption, is essential before selecting a tax regime.

Author Bio