Month: January 2026

2,391 articlesIncome Tax

Income Tax

CBEC Data Mismatch Cannot Justify Addition Without Enquiry: ITAT Delhi

Corporate Law

Corporate Law

From Dispute to Arbitration: The Breaking Point Test

Income Tax

Income Tax

Section 197 Certificates Can’t Be Denied on Overturned Past Assessments: Delhi HC

Company Law

Company Law

Penalty Imposed for Procedural Lapse in Share Allotment Disclosures

Company Law

Company Law

Incomplete Disclosures in Share Allotment Documents Attract Penalty: ROC Pune

Company Law

Company Law

Penalty Imposed for Incorrect AOC-4 Filing Despite Later Rectification

Income Tax

Income Tax

Final Assessment Orders under DRP Route Quashed as Time-Barred: ITAT Delhi

Finance

Finance

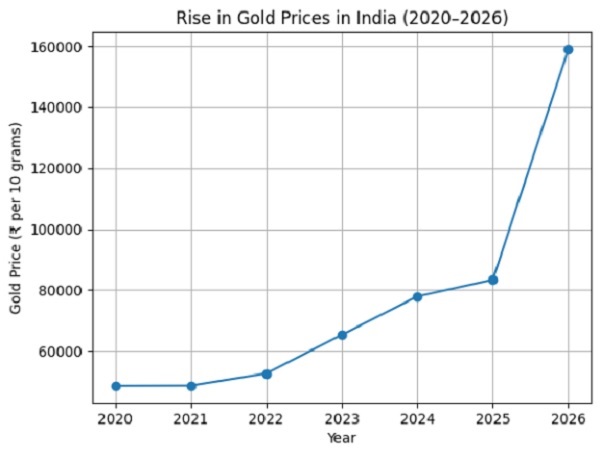

Why Gold Prices Are Rising Sharply: What the Numbers Tell Us

SEBI

SEBI

SEBI (LODR) Amendments Simplified: Key Changes for HVDLE

Income Tax

Income Tax