Month: January 2026

2,391 articlesGoods and Services Tax

Goods and Services Tax

Avoiding Errors in Table 10 & 11 of GSTR-9 of 24-25- A Practical Reporting Guide

Corporate Law

Corporate Law

Beyond Human Creativity: Legality of AI-Generated Content under Indian Copyright Law

CA, CS, CMA

CA, CS, CMA

Compliance Under Customs & FEMA For Exporters of North Eastern Region: A Comprehensive Legal Guide

Finance

Finance

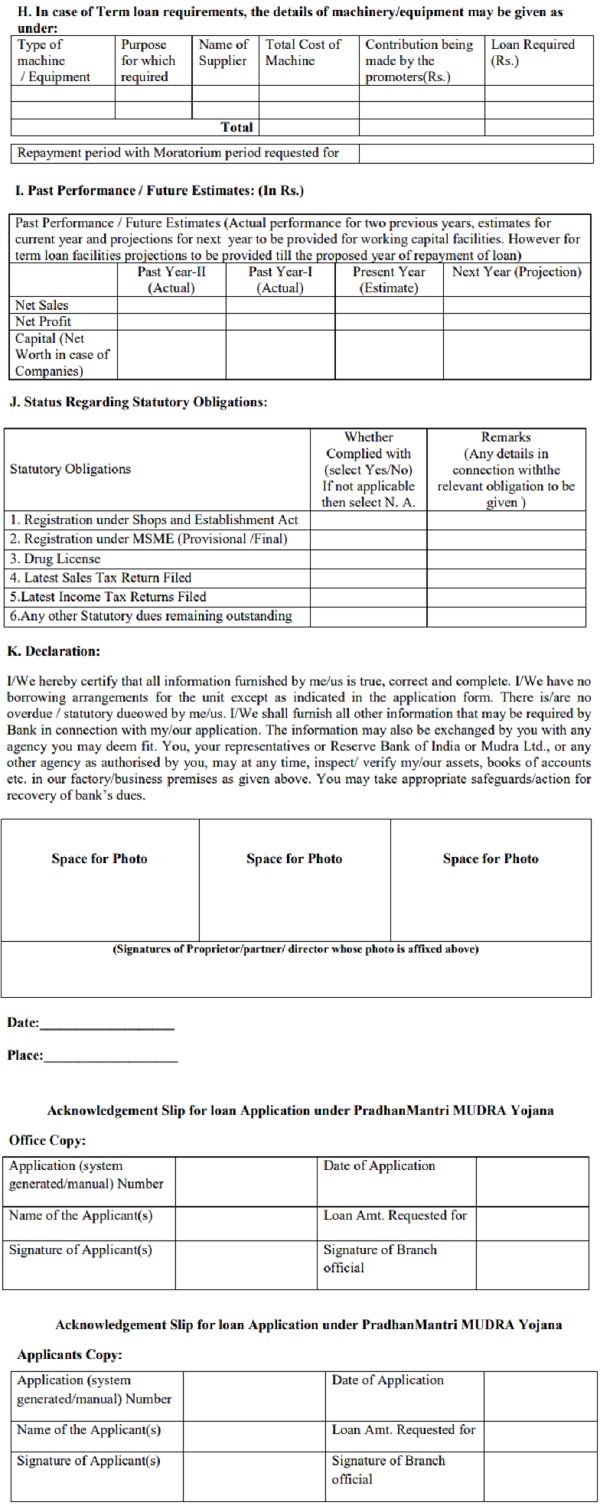

MUDRA Loans: A Complete Guide to Shishu, Kishore, Tarun & Tarun Plus Loans

Income Tax

Income Tax

How to Disclose Foreign Assets & Income in Schedule FA of ITR & Avoid Penalties

Income Tax

Income Tax

Bombay High Court disposes Revenue Income Tax Appeal for having low tax effect

Corporate Law

Corporate Law

IBBI Launches Revised Forms for the Liquidation Process

Corporate Law

Corporate Law

SEZ Reorganization Rules Clarified for IFSC Units

Goods and Services Tax

Goods and Services Tax

Adjustment of Tax Liability or Refund through GST Credit Note

Goods and Services Tax

Goods and Services Tax