Month: January 2026

2,391 articlesCorporate Law

Corporate Law

Utility Models in India: Balancing risks and Innovation

Corporate Law

Corporate Law

Intermediary Liability under Information Technology Act, 2000

Corporate Law

Corporate Law

NCLT/NCLAT Delay Index: How Adjudicatory Backlogs Undermine Value Realisation under IBC

Company Law

Company Law

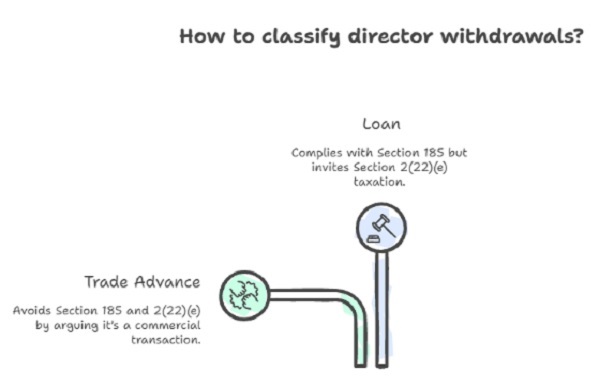

Analysis of Director Loans under Companies Act, 2013 & Income Tax Act, 1961

Goods and Services Tax

Goods and Services Tax

Tobacco leaves packed in small retail pouches classified under 2403 9910 as ‘Chewing tobacco’

Corporate Law

Corporate Law

Cross-Border Insolvency in India & Recent Judicial pronouncements

Goods and Services Tax

Goods and Services Tax

Flavoured milk classifiable under 0402 is subjected to 5% GST: Karnataka HC

Corporate Law

Corporate Law

SC Rejected Capital Subsidy Claim Due to Prior Exhaustion of Incentive Limits

Company Law

Company Law

Post-Facto CSR Payment Not a Defence – Penalty Upheld

Corporate Law

Corporate Law