Month: December 2025

2,753 articlesIncome Tax

Income Tax

Leave Encashment Revolution: Decoding New ₹25 Lakh Exemption

Income Tax

Income Tax

Section 144C(13) Delay Fatal: Tribunal Cancels Assessments

Income Tax

Income Tax

Section 148 notice issued by a JAO instead of FAO is without jurisdiction: ITAT Chandigarh

Goods and Services Tax

Goods and Services Tax

No Interference in ITC Fraud Order; Only Appeal Permitted not Writ: SC

Income Tax

Income Tax

No Incriminating Evidence, No Addition: ITAT Deletes Jewellery Charges

Corporate Law

Corporate Law

Bank Held Liable as SC Finds No Customer Negligence in Fraudulent Transactions

Goods and Services Tax

Goods and Services Tax

VAT-Era Security Deposits Must Be Refunded After GST Regime: Tripura HC

Income Tax

Income Tax

Section 11 exemption cannot be denied solely for delayed Form 10B uploading

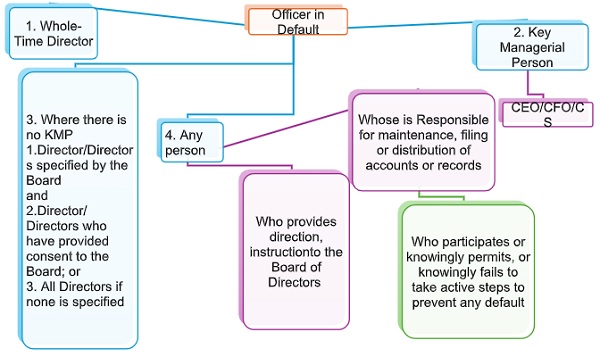

Company Law

Company Law

CSR Penalties Rise: Why Non-Compliance Under Section 135 Proves Costly

Income Tax

Income Tax