Month: December 2025

2,753 articlesIncome Tax

Income Tax

Section 263 Checkmated – ITAT Says PCIT Cannot Reopen Issues Already Before CIT(A)

Goods and Services Tax

Goods and Services Tax

Comprehensive Guidelines on GST for Corporate Guarantees Between Related Parties

Corporate Law

Corporate Law

Should India Move Towards a Debtor-In-Possession Model Like US? A Comparative Analysis

Goods and Services Tax

Goods and Services Tax

Important Clarification on Disclosure of ITC Reclaimed in FY 24–25 of FY 24-25

Income Tax

Income Tax

Reassessment Quashed for Issuing Section 148 Notice Through Wrong Authority

Income Tax

Income Tax

The Culinary Conundrum: Tax Deduction for Food or Business Meal Expenses: A RARE Practical Analysis

CA, CS, CMA

CA, CS, CMA

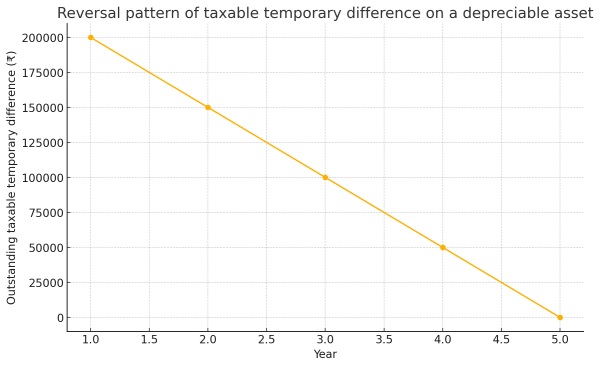

Accounting for Deferred Tax Assets and Liabilities: Ind AS 12 and IAS 12

Income Tax

Income Tax

15% ‘Misdirected’ Discount on NAV Shares, Rs. 8.70 Cr Addition Deleted

Goods and Services Tax

Goods and Services Tax

SC decisions on Maintainability of Writ Where Statutory Remedy Is Available

Income Tax

Income Tax