CA Mayur P. Kharche

In the commercial world, generally what we see is transactions occurring between two unrelated entities. Though, sometime transactions may occur between units of one legal entity (what has been referred to as ‘inter-unit / intercompany transactions’ in commercial sense). To give an example of what these ‘intercompany transactions’ may involve, it involves –

- Purchase and sale of goods and/or services;

- Declaration and payment of dividend;

- Borrowing and lending activities;

- Inventory (stock) transfer from one unit to another unit, whether on cost-plus-margin method or at fair value or at cost, etc.

When financial reporting is required at group level, meaning at Consolidated Level where all units of the entity will be regarded as a single whole unit, to avoid the misrepresentation of consolidated entity’s financial statement, occurrence of intercompany transactions need to be removed by adopting predefined steps for consolidation, which have been discussed in this article elsewhere.

This article will help you understand what principle guides the elimination of certain transactions before the preparation of consolidated presentation of financial data of an entity. Also, we will try to understand various types of the elimination entries and steps followed in elimination entry identification and its way into consolidation procedure.

After understanding from a point of an accountant, we will also try to see from the point of view of auditors, who cross-examines from independent sources and methods the correctness and accuracy of the elimination entries. So let’s look into the elimination entries.

Understanding of elimination in the consolidation procedure –

The management of an organization might wish to maintain separate accounting records at each branch or unit level of the organization. Any transactions happened between these units of an entity may be effected at cost. In fact, sometimes the management views its organization’s units as independent reporting units and hence, mandates them to act as an individual profit center and any sale made from one unit to another unit will include some profit element. In other way, what this means that the organization starts earning profit from the inter-unit / inter-company transactions.

I would like to give another example which we need to consider for understanding some other intercompany transactions. Let’s suppose Idea Cellular India Limited purchases majority (say, 51%) of the shares of Vodafone India Limited. Being the majority shareholder, Idea will be the owners of Vodafone. Let’s suppose the net assets value of Vodafone India Limited was Rs.100 Crores, i.e., Idea will be required to pay a minimum of Rs.100 Crores to buy Vodafone Company. Let’s suppose Idea proposes to buy Vodafone for Rs.100 Crores. Now, Idea will show Rs.100 Crores in its balance sheet under the head ‘Investment in the equity shares’ of Vodafone. At the same time, Vodafone India Limited will include Rs.100 Crores in its equity share capital.

Now, in first example, when the organization prepares its whole entity level financial statements and in second example, when Idea Cellular Limited prepares its Consolidated financial statements, what will be the treatment of inter-unit sales made at profit and the treatment of investment in the equity shares of Vodafone India Limited.

To understand the treatment, we need to go to the basics of accounting, where the Business Entity Concept has been given and which is followed in the whole accounting profession, all over the world. An entity cannot make profits from its own unit/branch transactions. For a business transaction to be recorded and reported at an entity level, there has to be two unrelated business entities.

In our first example of inter-unit sale and purchase transactions, an inter-unit sale and purchase will be recorded in the accounts of both units, assuming their individual separate legal existence and as if those are at arm’s-length. Coming at group/consolidation level, the transaction can be seen as unrealized since the goods sold by one unit to another unit reflected within group transactions and does not involve unrelated party. And therefore, the inter-unit transaction needs to be interpreted differently than it was by either of the participating units. Upon proper identification, we will come across certain accounts which would generally result in the removal of such balances before preparation of consolidated financial statements.

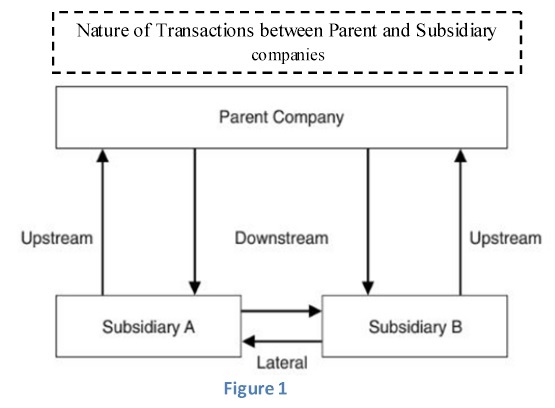

Transactions between units of an entity can take several forms and can occur between any units of the entity. Figure 1 [Taken from Wiley Publications] demonstrates various possible directions of intercompany transactions. Imagining Parent company at the top, entering into transaction with a subsidiary company will be termed as downstream transaction. Reverse of the same, a transaction initiated from a subsidiary to the parent company will be termed as upstream transaction. While a transaction between two subsidiaries of a parent company will be seen as lateral transaction.

Intercompany elimination is the process of elimination of / removal of certain transactions between the companies included in the group in the preparation of consolidation financial statements, which include Consolidated Statement of Profit and Loss, Consolidated Balance Sheet and Consolidated Cash Flow Statement, along with relevant notes.

When one unit of an entity is involved in a transaction with another unit of the same entity, we term it as intercompany transaction. Whatever the reason behind occurrence of such transactions, they often occur in the normal course of the business. The purpose of establishing an unit provides logic behind the inter-unit transactions. When I am referring to inter-units, its form may be that of the parent and a subsidiary, two divisions, or two departments of one entity. In the vertically integrated entity, it is common to notice transfer of inventory among various units of the whole organization. Transfer of plant asset from one unit to another unit where the demand is rising can be seen as intercompany transaction[1].

Generally Accepted Accounting Framework on Elimination Procedures –

In the Indian Generally Accepted Accounting Procedures (I-GAAP), Accounting Standard 21 – Consolidated Financial Statements and IND AS 110 – Consolidated Financial Statements provides illustrative guidance on the consolidation procedures to be followed in the preparation of consolidated financial statements, which also provides the guidance on the identification certain transactions which are required to be removed from the consolidated accounts.

Generally, following steps are involved in the consolidation procedure[2] –

1. To Combine – The reporting organization gathers the trial balances of all of its units and combines the like items such as assets, liabilities, revenue, expenditure accounts and a consolidated trial balance before adjustments is prepared in the functional currency of the reporting enterprise as per the applicable GAAP.

2. To Offset (Eliminate) – The Reporting Company eliminates the carrying amount of the parent’s investment in each subsidiary and the parent’s portion of equity of each subsidiary.

3. To Remove – Based on the nature of business and transactions incurred for the period under reporting, the company identifies the intra group transactions which are required to be removed and these transactions are reversed from the consolidated trial balance.

4. To Prepare – After eliminating what is required to eliminated, consolidated financial statements are prepared.

Types of Elimination Entries –

1. Elimination of Equity Ownership in the subsidiary companies –

Stockholder’s equity account in the subsidiary company is eliminated against the investment in equity shares account of the parent company and assets and liabilities are added line-by-line in the consolidated trial balance.

2. Elimination of intercompany debt –

Loan advanced by the parent company to its subsidiary company is a type of intercompany transaction which needs to be removed before consolidation. The nature of such borrowing and investing activity can be observed as notes payable, notes receivable, loans and advances, inter corporate deposits, etc. Such loan, unless discounted with banks in case of notes receivables, needs to be eliminated from the consolidated accounts.

3. Elimination of intercompany revenue and expenses, assets and liabilities –

Sale and purchase transactions incurred between the subsidiary companies, stock transfers made during the reporting period from one subsidiary company / unit and such stock being in unsold condition lying in the books of another subsidiary company / unit, involving unrealized profit element, intra group accounts receivables and accounts payables, etc. are certain types of transactions which are required to be removed from consolidated trial balance, worshiping the Business Entity Concept.

Certain events also give rise to some transactions which will be invalid as per Business Entity concept, such as mergers and one company being absorbed by another. It is highly essential in such case to clean up the consolidated accounts to comply with the applicable GAAP and also to honor the substance over form, where one can’t make profits from his own transactions.

Identification of Intercompany transactions –

Identification of intercompany / inter-unit transactions can be a difficult task, seeing the lakhs and crores of transactions incurred throughout a financial year. In light of this, it would be advisable to the management to set up a system of controls to identify such intercompany transactions at source level and identified transactions are brought to the attention of accounting staff, for their future reference. When a company acquires new organization through absorption or merger, this issue might of particular importance since the newly acquired company might not possess a robust internal control system. In such places, Enterprise Resource Planning (ERP) system provides helpful hand to the management to implement the control system throughout the organization and to flag such related party / inter-unit transactions for easy reference and monitoring. ERP software provides facilities of quoting a separate transaction code for entering and identifying the intercompany transactions for easier management reporting function and auditor’s examination.

Once the control system is in place to identify the intercompany transaction, it is highly possible that the same type of transaction will occur again in the future period and accordingly accounting staff can make list of all inter-unit transactions and modify the accounting system to by default highlight such transactions whenever occurred in future. Hence, it is importantly to document such controls and resulting voucher/entries for its detailed review by the company’s auditors.

Intercompany Eliminations – From Auditors’ Perspective: –

Since the intercompany transactions, being related parties transactions, involve the possibility that a related party relationship may be a tool for fraud by management, the generally accepted auditing practices provides immense importance to validating the accuracy and fairness of such intra-group transactions. These transactions might also be more of disclosure-oriented than fraud-oriented. However, given the risks involved for an auditor, such intra-group transactions cannot be assumed to be outside the ordinary course of business.

Following guidance is generally followed by the Auditors while evaluating the fairness of consolidated financial statements in context of intercompany transactions and their eliminations –

1. Auditors firstly need to ensure that the management has identified all the inter company units and properly flagged in the accounting systems. He needs to bear the risk of undisclosed related parties or inter-units which might cast material adverse or favorable impact on the consolidated performance of the reporting entity. Many factors exists which can provide the Auditors a possibility of related party transactions. Such factors may include excess capacity at one unit and rising demand at another unit, market volatility in one geography affecting performance of its local unit adversely and pressure on the management to revival and growth of the business, etc.

2. After identifying the parties of related nature, the Auditors focus on the management’s process of identification of intercompany transactions and how they have ensured the completeness of intercompany transactions which needs to be considered for elimination procedure of consolidation. Elimination entries passed by the management are cross-verified by the Auditors, including cancellation of ownership stake in the subsidiary units and investment account in the parent’s books. Line-by-line addition from the subsidiary accounts to the parent’s consolidated trial balance is also reviewed by the Auditors to ensure that no account has been skipped from being considered for consolidated trial balance and there is no intercompany account balance which carries balance in the consolidated financial statements.

3. Based on the identified nature of intercompany transactions, the Auditors also ensures proper disclosures of related parties transactions in the notes to financial statements which are eliminated from the consolidated accounts but requires separate disclosure in the consolidated financial statements as per applicable governing laws and regulations.

Conclusion –

Being an integral and important step in the consolidation procedure, intercompany transactions eliminations holds importance to both, the Company’s management as well as the Auditors. The Company’s management can benefit from better presentation of individual unit’s performance and can also generate consolidated results after following systematic and controlled accounting procedures and practices. Though identifying intercompany transactions identification may involve difficulty, it can be identified at the source, by implementing robust control system, thus enabling elimination of such transactions smoothly and completely.

[1] Wiley’s INTERCOMPANY TRANSACTIONS. Available at: http://www.wiley.com/college/bline/0471327751/samplechapter/ch04.pdf (Accessed: 30 January 2017).

[2] Government of India – Ind AS – 110 Consolidated Financial Statements. Available at: http://mca.gov.in/Ministry/pdf/INDAS110.pdf(Accessed: 30 January 2017).

Dear Sir

How should one consolidate a company which has become subsidiary by virtue of composition of board of directors??