The Securities and Exchange Board of India (SEBI), through its amendments to the Listing Obligations and Disclosure Requirements (LODR) Regulations dated 18th November 2025, has introduced significant changes to the regulatory framework governing Related Party Transactions (RPTs). These amendments aim to streamline compliance requirements, bring greater clarity to approval mechanisms, and enhance the ease of approval of audit committee for the transaction in which subsidiary is a party but listed entity is not. This note analyses the key amendments and their practical implications for listed entities and their subsidiaries.

Material amendments in Related Party Transactions:

The Securities and Exchange Board of India (SEBI), through its amendments to the Listing Obligations and Disclosure Requirements (LODR) Regulations dated 18th November 2025, has introduced significant changes to the regulatory framework governing Related Party Transactions (RPTs). These amendments aim to streamline compliance requirements, bring greater clarity to approval mechanisms, and enhance the ease of approval of audit committee for the transaction in which subsidiary is a party but listed entity is not. This note analyses the key amendments and their practical implications for listed entities and their subsidiaries

1) Amendments in definition of “Related Party”

| Erstwhile provisions | Current Provisions |

| Regulation 2, sub-regulation (1), clause (zc), in the first proviso, in clause (e):

Retail purchases from any listed entity or its subsidiary by its directors or its employees, without establishing a business relationship and at the terms which are uniformly applicable/offered to all employees and directors |

Regulation 2, sub-regulation (1), clause (zc), in the first proviso, in clause (e):

Retail purchases from any listed entity or its subsidiary by its the directors or key managerial personnel of the listed entity or if subsidiary, and relatives of such directors or key managerial |

–

| Impact:

Directors and KMP of Listed Company or of Subsidiary and Relative of such director and KMP can make retail purchase on a uniformly applicable terms without being treated as Related Party |

2) Relaxation for RPT where Subsidiary is a party but Listed Entity is not

| Erstwhile provisions | Current Provisions |

| Reg 23(2)(b): a related party transaction to which the subsidiary of a listed entity is a party but the listed entity is not a party, shall require prior approval of the audit committee of the listed entity if the value of such transaction whether entered into individually or taken together with previous transactions during a financial year exceeds ten per cent of the annual consolidated turnover, as per the last audited financial statements of the listed entity; |

b) a related party transaction above Rs. 1 Crore, whether entered into individually or taken together with previous transactions during a financial year, to which Subsidiary of a Listed Entity is a party but listed entity is not a party, shall require prior approval of audit committee of the listed entity if the value of such transaction exceeds lower of the following:

(i) 10% of Annual Standalone Turnover of Subsidiary as per latest audited financial statement of a subsidiary; or (ii) the threshold for material related party transactions of listed entity as specified in Schedule XII of SEBI LODR Regulations. |

| Reg 23(2)(c): with effect from April 1, 2023, a related party transaction to which the subsidiary of a listed entity is a party but the listed entity is not a party, shall require prior approval of the audit committee of the listed entity if the value of such transaction whether entered into individually or taken together with previous transactions during a financial year, exceeds ten per cent of the annual standalone turnover, as per the last audited financial statements of the subsidiary; | (c) In the event of a related party transaction above Rs. 1 Crore, whether entered into individually or taken together with previous transactions during a financial year, to which Subsidiary of a Listed Entity is a party but listed entity is not a party, and such subsidiary does not have audited financial statements for a period of at least one year, prior approval of the audit committee of the listed entity shall be obtained, if the value of such transaction exceeds lower of the following:

(i) 10% of aggregate Paid Up Capital and Securities Premium of the Subsidiary; or (ii) the threshold for material related party transactions of listed entity as specified in Schedule XII of SEBI LODR Regulations. Further, the aggregate of Paid-Up Capital and Securities Premium shall not be older than three months prior to the date of seeking approval of Audit Committee. |

–

| Impact:

1) Audit Committee approval is triggered only when the transaction exceeds Rs. 1 crore and the above applicable percentage-based threshold. This is particularly beneficial for subsidiaries with low or negligible turnover. 2) This brings more clarity from the perspective of the prior approval of Audit Committee of the Companies, which are subsidiaries of a bigger conglomerate and whose value of RPT does not exceed 10% of Annual Standalone turnover of a Subsidiary but exceeds the materiality limit of Rs. 1000 Crore. 3) This also brings clarity from the approval perspective of the newly incorporated subsidiaries which do not have audited financial statements for at least one year. |

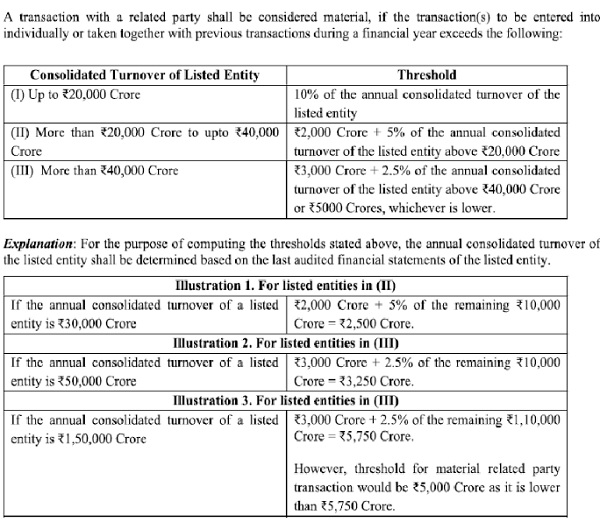

3) Enhanced the limit of Materiality:

| Erstwhile provisions | Current Provisions |

| Reg 23(1): a transaction with a related party shall be considered material, if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceeds Rs. 1000 crore or 10% of the annual consolidated turnover of the listed entity as per the last audited financial statements of the listed entity, whichever is lower | Reg 23(1): a transaction with a related party shall be considered material, if the transaction(s) to be entered into individually or taken together with previous transactions during a financial year, exceeds the threshold specified schedule XII of SEBI LODR Regulation. |

Schedule XII is as follows:

| Impact:

1) This new amendment introduces a dynamic, tiered threshold system that scales with the size of the company. 2) The Materiality thresholds shall be determined based on the size of the Company on the basis of Annual Consolidated turnover of the Listed Entity, thereby reducing the compliance burden on the Company. 3) The maximum limit of material Related Party Transaction has been kept as Rs. 5000 crores against an absolute limit of Rs. 1000 Crore. |

4) Introduction of Provisions of Omnibus approval of Material RPT by the Shareholders:

SEBI these amendments dated 18th November, 2025, have inserted the a proviso clause in Regulation 23 (4) which states the following:

|

–

| Impact:

SEBI has align the provisions of Reg. 23 of SEBI LODR with the Para C, Section III-B of Master circular for compliance with the provisions of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 by listed entities dated 11th November, 2024 |

*****

Prepared by: CS Gagan Gupta | Assistant Manager | Transaction Square LLP

In case of any query or suggestion pls feel free to contact at: Mobile: 8274915682| Email: gagan.knowles@gmail.com

Disclaimer: The entire contents of this document have been prepared based on relevant provisions and as per the information existing at the time of the preparation. Although care has been taken to ensure the accuracy, completeness, and reliability of the information provided, I assume no responsibility, therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws. The user of the information agrees that the information is not professional advice and is subject to change without notice. I assume no responsibility for the consequences of the use of such information

Best article ever