The Reserve Bank of India (RBI) announced on August 6, 2025, that the Monetary Policy Committee (MPC) has unanimously decided to keep the policy repo rate unchanged at 5.50 percent. This decision, made in a context of robust domestic growth and moderating headline inflation, aims to allow previous rate cuts to fully transmit through the economy. The RBI noted that while overall inflation has fallen to a 77-month low of 2.1 percent due to lower food prices, core inflation remains steady around 4 percent and is projected to rise in the future. The RBI also introduced new developmental policies, including standardizing the procedure for settling claims of deceased bank customers to improve customer service. Additionally, it has enabled an auto-bidding facility on its RBI Retail Direct portal for investors to systematically purchase Treasury bills. The projected real GDP growth for 2025-26 remains at 6.5 percent.

RESERVE BANK OF INDIA

Statement on Developmental and Regulatory Policies

August 06, 2025

This Statement sets out the developmental and regulatory policy measures relating to (i) Regulation; (ii) Financial Markets.

I. Regulation

1. Standardisation of procedure for settlement of claims in respect of deposit accounts of deceased customers of banks

Under the provisions of Banking Regulation Act, 1949, nomination facility is available in respect of deposit accounts, articles kept in safe custody or safe deposit lockers. This is intended to facilitate expeditious settlement of claims or return of articles or release of contents of safe deposit locker upon death of a customer and to minimise hardship caused to family members. The extant instructions require banks to adopt a simplified procedure to facilitate expeditious and hassle-free settlement of claims made by survivors/ nominees/ legal heirs, the procedures vary across banks. With a view to enhance customer service standards, it has been decided to streamline the procedures and standardise the documentation to be submitted to the banks. A draft circular in this regard shall be issued shortly for public consultation.

II. Financial Markets

2. Introduction of Auto-bidding facilities in RBI Retail Direct for Investment and Re-investment in T-bills

The Retail Direct portal was launched in November 2021 to facilitate retail investors to open their Gilt accounts with the Reserve Bank under the Retail Direct Scheme. The scheme allows retail investors to buy Government Securities (G-Secs) in primary auctions as well as buy and sell G-Secs in the secondary market. Since the launch of the Scheme, various new features, in terms of product as well as payment options, have been introduced, including launch of a mobile app in May 2024.

To enable investors to systematically plan their investments, an auto-bidding facility for Treasury bills (T-bills), covering both investment and re-investment options, has been enabled in Retail Direct. The new functionality helps investors to mandate automatic placement of bids in primary auctions of T-bills.

(Puneet Pancholy)

Chief General Manager

Press Release: 2025-2026/843

Governor’s Statement: August 6, 2025

Namaskar and greetings to all in this month of Raksha Bandhan, Independence Day, Janmashtami, Parsi New Year and Ganesh Chaturthi. May this pious and auspicious month bring good luck to all of us and to our economy.

The monsoon season has been progressing well. We are also approaching the festival season, which typically brings greater enthusiasm and buoyancy in economic activity. This favourable domestic setting, together with supportive policies of the Government and the Reserve Bank, augurs well for the Indian economy in the near term, as geopolitical uncertainties have somewhat abated, even though global trade challenges continue to linger. Over the medium-term also, the Indian economy holds bright prospects in the changing world order drawing on its inherent strength, robust fundamentals, and comfortable buffers. Opportunities are there for the taking, and we are making all efforts to create enabling conditions through a multi-pronged yet cohesive approach to policymaking.

2. Globally, policy makers are faced with muted growth and slowing pace of disinflation, with some advanced economies even witnessing an uptick in inflation. As the dust settles and a new equilibrium emerges in the new global order, policymakers will have a tough task navigating a world characterised by modest growth, sticky inflation and elevated public debt levels.

3. At the Reserve Bank, leveraging on the room provided by a significant moderation in inflation, we have taken decisive and forward-looking measures to support growth. The coordinated use of various tools available to us has helped accelerate monetary policy transmission in the current easing cycle.

Decisions of the Monetary Policy Committee (MPC)

4. The Monetary Policy Committee (MPC) met on the 4th, 5th and 6th of August to deliberate and decide on the policy repo rate. After a detailed assessment of the evolving macroeconomic and financial developments and the outlook, the MPC voted unanimously to keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 5.50 per cent; consequently, the standing deposit facility (SDF) rate shall remain unchanged at 5.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 5.75 per cent. The MPC also decided to continue with the neutral stance.

5. The MPC noted that, while headline inflation is much lower than projected earlier, it is mainly due to volatile food prices, especially of vegetables. Core inflation, on the other hand, has remained steady around the 4 per cent mark, as anticipated. Inflation is projected to go up from the last quarter of this financial year. Growth is robust and as per earlier projections though below our aspirations. The uncertainties of tariffs are still evolving. Monetary policy transmission is continuing. The impact of the 100 bps rate cut since February 2025 on the economy is still unfolding.

6. On balance, therefore, the current macroeconomic conditions, outlook and uncertainties call for continuation of the policy repo rate of 5.5 per cent and wait for further transmission of the front-loaded rate cut to the credit markets and the broader economy. Accordingly, the MPC unanimously voted to keep the repo rate unchanged. The MPC further resolved to maintain a close vigil on the incoming data and the evolving domestic growth-inflation dynamics to chart out the appropriate monetary policy path. Accordingly, all members decided to continue with the neutral stance.

Assessment of Growth and Inflation Growth

7. Domestic growth is holding up and is broadly evolving along the lines of our assessment even though some high-frequency indicators showed mixed signals in May-June. Rural consumption remains resilient1 while urban consumption revival, especially discretionary spending, is tepid2. Fixed investment3 supported by buoyant government capex continues to support economic activity.

8. On the supply side, steady southwest monsoon4 is supporting kharif sowing,5 replenishing reservoir levels6 and boosting agriculture activity. Moreover, services activity remains steady, though some high-frequency indicators recorded a modest expansion.7 Services PMI8 increased to an 11-month high of 60.5 in July 2025. Construction activity continues to exhibit resilience.9 However, growth in the industrial sector remained subdued and uneven across segments, pulled down by electricity and mining.10 While the manufacturing Purchasing Managers’ Index (PMI)11 remained elevated in Q1, the Index of Industrial Production (IIP)12 showed moderation.

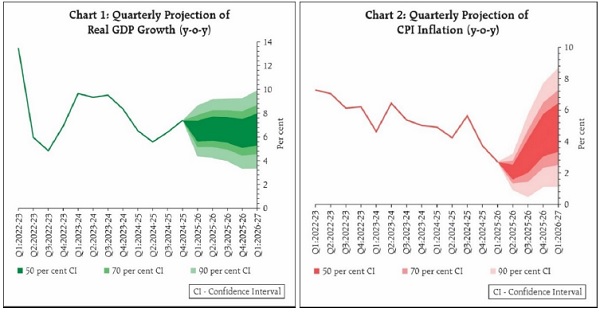

9. Turning to the growth outlook, the above normal southwest monsoon, lower inflation, rising capacity utilisation, and congenial financial conditions continue to support domestic economic activity. The supportive monetary, regulatory and fiscal policies including robust government capital expenditure,13 should also boost demand. With sustained growth in construction and trade segments, the services sector is expected to remain buoyant in the coming months. Prospects of external demand, however, remain uncertain amidst ongoing tariff announcements and trade negotiations. The headwinds emanating from prolonged geopolitical tensions, persisting global uncertainties, and volatility in global financial markets pose risks to the growth outlook. Taking all these factors into account, real GDP growth for 202526 is projected at 6.5 per cent, with Q1 at 6.5 per cent, Q2 at 6.7 per cent, Q3 at 6.6 per cent, and Q4 at 6.3 per cent. Real GDP growth for Q1:2026-27 is projected at 6.6 per cent. The risks are evenly balanced.

Inflation

10. CPI headline inflation declined for the eighth consecutive month to a 77-month low of 2.1 per cent in June.14 This was driven primarily by a sharp decline in food inflation, led by improved agricultural activity and various supply side measures. Food inflation recorded its first negative print since February 2019 at (-) 0.2 per cent in June. Double-digit deflation in vegetables and pulses drove this contraction.15 High-frequency price indicators signal a continuation of the lower price momentum in food prices to July as well. Fuel group inflation moderated over two successive months to record 2.6 per cent in June.16 Core inflation,17 which remained within a narrow range of 4.1-4.2 per cent during February-May, increased to 4.4 per cent in June, partly driven by a continued increase in gold prices.

11. The inflation outlook for 2025-26 has become more benign than expected in June. Large favourable base effects combined with steady progress of the southwest monsoon, healthy kharif sowing, adequate reservoir levels and comfortable buffer stocks of foodgrains18 have contributed to this moderation. CPI inflation, however, is likely to edge up above 4 per cent in Q4:2025-26 and beyond, as unfavourable base effects, and demand side factors from policy actions come into play. Barring any major negative shock to input prices, core inflation is likely to remain moderately above 4 per cent during the year. Weather-related shocks pose risks to inflation outlook. Considering all these factors, CPI inflation for 2025-26 is now projected at 3.1 per cent with Q2 at 2.1 per cent; Q3 at 3.1 per cent; and Q4 at 4.4 per cent. CPI inflation for Q1:2026-27 is projected at 4.9 per cent. The risks are evenly balanced.

External Sector

12. India’s current account deficit (CAD) moderated to 0.6 per cent of GDP in 202425 from 0.7 per cent of GDP in 2023-24 due to robust services exports and strong remittances receipts despite higher merchandise trade deficit. Merchandise trade deficit further widened in Q1 of 2025-26. India’s share in world services exports has risen markedly from about 2 per cent in 2005 to 4.3 per cent in 2024, driven by strong software and business services exports. Robust services exports19 coupled with strong remittance receipts are expected to keep CAD within the sustainable level during the current financial year.

13. On the external financing side, gross foreign direct investment (FDI) to India remained strong during April-May 2025-26. However, net FDI moderated during this period due to higher outward FDI.20 Foreign portfolio investment (FPI) inflows to EMEs have remained strong in May and June 2025.21 However, net FPI to India recorded outflows of US$ 0.8 billion in 2025-26 so far (April-July 31) due to outflows in the debt segment.22 External commercial borrowings, on the other hand, witnessed higher net inflows compared to last year. Inflows under non-resident deposits too remained positive, albeit witnessing some moderation.23 As on August 1, 2025, India’s foreign exchange reserves stood at US$ 688.9 billion, sufficient to cover more than 11 months of merchandise imports.24 Overall, India’s external sector remains resilient.25 We remain confident of meeting our external financing requirements comfortably.

Liquidity and Financial Market Conditions

14. System liquidity, as measured by the net position under the Liquidity Adjustment Facility (LAF), has been in surplus, on an average of ₹3.0 lakh crore per day since the last MPC, as compared to an average daily surplus of ₹1.6 lakh crore during the previous two months.26 Going ahead, as the CRR cut announced in the last policy comes into effect in a staggered manner beginning September, it would further support liquidity conditions.

15. The comfortable liquidity in the banking system has reinforced transmission of the policy repo rate cuts to the money27, bond28 and credit markets during the current easing cycle. In the credit market, the weighted average lending rate (WALR) of scheduled commercial banks declined by 71 basis points for fresh rupee loans (of which 55 bps is due to interest rate reduction) and 39 basis points for outstanding rupee loans from February 2025 to June 2025. On the deposit side, the weighted average domestic term deposit rate (WADTDR) on fresh deposits moderated by 87 bps during the same period. Moreover, the transmission to lending rates has been broad based across sectors.

16. Going ahead, the Reserve Bank will continue to be nimble and flexible in its liquidity management. We will endeavour to maintain sufficient liquidity in the banking system so that the productive requirements of the economy are met and transmission to money markets and credit markets remains smooth.

17. An internal Working Group has reviewed the Reserve Bank’s extant Liquidity Management Framework (LMF), operative since February 2020. The Group has submitted its report and the same will be placed on the RBI website shortly for public consultation. The weighted average call rate (WACR) is found to be highly correlated with other overnight money market rates (TREPS and Market Repo) in the collateralised segments. Further, WACR is also found to be effective in transmitting signals to other money market instruments across maturities. Therefore, the Group has recommended continuation of overnight WACR as the operating target of monetary policy. The Group has, inter alia, also recommended to continue with the variable rate auction mechanism for repo and reverse repo operations of various tenors with the objective of maintaining the operating target rate at the policy rate.

Financial Stability

18. The system-level financial parameters related to capital adequacy, liquidity, asset quality and profitability of Scheduled Commercial Banks (SCBs) continue to remain healthy.29 Credit Deposit Ratio (CD ratio) for the banking system at the end of June 2025 was 78.9 per cent, broadly similar to that an year ago. Similarly, the system-level parameters of NBFCs too are sound, with adequate capital position and improved GNPA ratios.30

19. Bank credit grew at 12.1 per cent during 2024-25. While it is slower than the growth rate of 16.3 per cent in 2023-24, it is higher than the average growth rate of 10.3 per cent recorded in the ten-year period preceding 2024-25. Moreover, while the flow of non-food bank credit during the financial year 2024-25 reduced by about ₹3.4 lakh crore from ₹21.4 lakh crore to almost ₹18 lakh crore, the flow from non-bank sources more than made up for this decrease.31 Thus, even though growth rate of bank credit slowed last year, the overall flow of financial resources to the commercial sector increased from ₹33.9 lakh crore in 2023-24 to ₹34.8 lakh crore in 2024-25. This trend continues during the current financial year as well.32 As transmission to money markets has been faster, large corporates increasingly relied on market-based instruments such as commercial paper and corporate bonds to source funds, reducing their reliance on bank credit.33 Also, as the profitability of large corporates has increased, their internal resources have become an important source for business expansion.

Additional Measures

20. Before I conclude, let me underline that for us at RBI, the interest and welfare of the citizens of India is foremost. It is the people of India, including those at the bottom of the pyramid, who are our raison detre, or the reason of our being. In this regard, I have three consumer-centric announcements to make.

21. One, as Jan-dhan Scheme completes 10 years, a large number of accounts have fallen due for re-KYC. The banks are organising camps at Panchayat level from 1st July to 30th September, in an endeavour to provide services at customer doorsteps. Apart from opening new bank accounts and re-KYC, the camps will focus on micro insurance and pension schemes for financial inclusion and customer grievance redress.

22. Two, we will be standardising the procedure for settlement of claims in respect of bank accounts, and articles kept in safe custody or safe deposit lockers of deceased bank customers. This is expected to make settlement more convenient and simpler.

23. Three, we are expanding the functionality in RBI Retail-Direct platform to enable retail investors to invest in treasury bills through systematic investment plans.

Concluding Remarks

24. I now make my concluding remarks. Despite a challenging external environment, the Indian economy is navigating a steady growth path with price stability. Monetary policy has appropriately used the policy space created by the benign inflation outlook to support growth without compromising on the primary objective of price stability. Transmission of our recent policy actions to the broader economy is underway.

25. As the Indian economy strives to attain its rightful place in the global economy, stronger policy frameworks across domains, and not just limited to monetary policy, will be pivotal in its journey. We, on our part, will continue to be agile and proactive in providing a facilitative monetary policy based on incoming data and the evolution of the growth-inflation dynamics. As always, we will have a clear, consistent and credible communication backed by actions necessary for the task at hand.

Thank you. Namaskar and Jai Hind.

(Puneet Pancholy)

Chief General Manager

Press Release: 2025-2026/842

Monetary Policy Statement, 2025-26

Resolution of the Monetary Policy Committee

August 4 to 6, 2025

Monetary Policy Decisions

The Monetary Policy Committee (MPC) held its 56th meeting from August 4 to 6, 2025 under the chairmanship of Shri Sanjay Malhotra, Governor, Reserve Bank of India. The MPC members Dr. Nagesh Kumar, Shri Saugata Bhattacharya, Prof. Ram Singh, Dr. Poonam Gupta and Dr. Rajiv Ranjan attended the meeting.

2. After assessing the current and evolving macroeconomic situation, the MPC voted to maintain the policy repo rate at 5.50 per cent. Consequently, the standing deposit facility (SDF) rate under the liquidity adjustment facility (LAF) remains unchanged at 5.25 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 5.75 per cent. This decision is in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

Growth and Inflation Outlook

3. The global environment continues to be challenging. Although financial market volatility and geopolitical uncertainties have abated somewhat from their peaks in recent months, trade negotiation challenges continue to linger. Global growth, though revised upwards by the IMF, remains muted. The pace of disinflation is slowing down, with some advanced economies even witnessing an uptick in inflation.

4. Domestic growth remains resilient and is broadly evolving along the lines of our assessment. Private consumption, aided by rural demand, and fixed investment, supported by buoyant government capex, continue to boost economic activity. On the supply side, a steady south-west monsoon is supporting kharif sowing, replenishing reservoir levels and boosting agriculture activity. Moreover, services sector and construction activity remain robust. However, growth in industrial sector remained subdued and uneven across segments, pulled down by electricity and mining.

5. As for the growth outlook, the above normal southwest monsoon, lower inflation, rising capacity utilization and congenial financial conditions continue to support domestic economic activity. The supportive monetary, regulatory and fiscal policies including robust government capital expenditure should also boost demand. The services sector is expected to remain buoyant, with sustained growth in construction and trade in the coming months. Prospects of external demand, however, remain uncertain amidst ongoing tariff announcements and trade negotiations. The headwinds emanating from prolonged geopolitical tensions, persisting global uncertainties, and volatility in global financial markets pose risks to the growth outlook. Taking all these factors into account, projection for real GDP growth for 2025-26 has been retained at 6.5 per cent, with Q1 at 6.5 per cent, Q2 at 6.7 per cent, Q3 at 6.6 per cent, and Q4 at 6.3 per cent. Real GDP growth for Q1:2026-27 is projected at 6.6 per cent (Chart 1). The risks are evenly balanced.

6. CPI headline inflation declined for the eighth consecutive month to a 77-month low of 2.1 per cent (y-o-y) in June 2025. This was driven primarily by a sharp decline in food inflation led by improved agricultural activity and various supply side measures. Food inflation recorded its first negative print since February 2019 at (-) 0.2 per cent in June. High-frequency price indicators signal a continuation of the lower price momentum in food prices this year to July as well. Core inflation, which remained within a narrow range of 4.1-4.2 per cent during February-May, increased to 4.4 per cent in June, driven partly by a continued increase in gold prices.

7. The inflation outlook for 2025-26 has become more benign than expected in June. Large favourable base effects combined with steady progress of the southwest monsoon, healthy kharif sowing, adequate reservoir levels and comfortable buffer stocks of foodgrains have contributed to this moderation. CPI inflation, however, is likely to edge up above 4 per cent by Q4:2025-26 and beyond, as unfavourable base effects, and demand side factors from policy actions come into play. Barring any major negative shock to input prices, core inflation is likely to remain moderately above 4 per cent during the year. Weather-related shocks pose risks to inflation outlook. Considering all these factors, CPI inflation for 2025-26 is now projected at 3.1 per cent with Q2 at 2.1 per cent; Q3 at 3.1 per cent; and Q4 at 4.4 per cent. CPI inflation for Q1:2026-27 is projected at 4.9 per cent (Chart 2). The risks are evenly balanced.

Rationale for Monetary Policy Decisions

8. The MPC noted that the inflation outlook in the near term has become more benign than anticipated earlier, and the average CPI inflation this year is expected to remain significantly below the target. This is driven mainly by lower food inflation that entered deflationary territory in June. However, CPI inflation is likely to edge up above the 4 per cent target from Q4:2025-26 onwards. Moreover, core inflation has been rising steadily from the recent low of 3.6 per cent recorded during December-January 2024-25 and averaged 4.3 per cent in Q1 this year. Core excluding precious metals has witnessed an uptick and averaged 3.4 per cent in Q1.

9. Growth has held up well with some pick-up expected in the coming festive season and is evolving in line with our assessment of 6.5 per cent for 2025-26.

10. Thus, while headline inflation is much lower than projected earlier, it is mainly due to volatile food prices, especially of vegetables. Core inflation, on the other hand, has remained steady around the 4 per cent mark, as anticipated. Inflation is projected to go up from the last quarter of this financial year. Growth is robust and as per earlier projections though below our aspirations. The uncertainties of tariffs are still evolving. Monetary policy transmission is continuing. The impact of the 100 bps rate cuts since February 2025 on the economy is still unfolding.

11. On balance, therefore, the current macroeconomic conditions, outlook and uncertainties call for continuation of the policy repo rate of 5.5 per cent and wait for further transmission of the front-loaded rate cuts to the credit markets and the broader economy. Accordingly, the MPC unanimously voted to keep the repo rate unchanged. The MPC further resolved to maintain a close vigil on the incoming data and the evolving domestic growth-inflation dynamics to chart out the appropriate monetary policy path. Accordingly, all members decided to continue with the neutral stance.

12. The minutes of the MPC’s meeting will be published on August 20, 2025.

13. The next meeting of the MPC is scheduled from September 29 to October 1, 2025.

(Puneet Pancholy)

Chief General Manager

Press Release: 2025-2026/841

Notes:-

1 Tractor sales and retail two-wheeler sales posted a growth of 9.2 per cent and 4.9 per cent, respectively, during Q1 of 2025-26.

2 As per the NielsenIQ’s Retail Audit Service, FMCG sales volume grew by 6.0 per cent during Q1:2025-26, with rural and urban areas recording a growth of 8.4 per cent and 4.3 per cent, respectively. Retail sales of passenger vehicles grew by 3.0 per cent

during Q1 and domestic air passenger traffic expanded by 5.3 per cent during this period.

3 Central government capital expenditure grew at a strong 52.0 per cent (y-o-y) during Q1:2025-26. Index of Industrial Production of capital goods expanded by 10.0 per cent and import of capital goods increased by 12.6 per cent in Q1:2025-26.

4 As of August 4, 2025, the cumulative south-west monsoon (SWM) rainfall is 4 per cent above the long period average (LPA).

5 The area sown under kharif crops as on August 1, 2025, is 5.1 per cent higher than the corresponding acreage of previous year.

6 As of July 31, 2025, reservoir levels were at 69 per cent of the full capacity, well above last year’s level as well as decadal average of 46 per cent.

7 E-way bills increased strongly by 19.3 per cent in June 2025 and toll collections increased by 15.2 per cent in June-July 2025. Growth of gross GST collections moderated to 6.9 per cent in June-July 2025 after a 16.4 per cent growth in May. Domestic air

cargo posted a growth of 2.6 per cent in June 2025; port cargo witnessed a growth of 5.6 per cent in Q1:2025-26; sales of commercial vehicle contracted by 0.6 per cent in Q1.

8 PMI services climbed up to 60.4 in June 2025 and further to 60.5 in July, from 58.8 in May.

9 Steel consumption grew by 7.9 per cent in Q1:2025-26 and cement production posted a growth of 8.4 per cent during this period.

10 Mining and electricity output contracted by 3.0 per cent and 1.9 per cent, respectively, during Q1:2025-26.

11 Manufacturing PMI surged to a 16-month high of 59.1 in July 2025, signalling robust momentum in the manufacturing sector.

12 Manufacturing IIP recorded a modest growth of 3.4 per cent during Q1:2025-26.

13 As per the Union Budget 2025-26, the central government’s effective capital expenditure (including grants-in-aid for creation of capital assets) is budgeted to grow by 17.4 per cent.

14 CPI headline inflation declined to 2.1 per cent in June 2025 (lowest since January 2019) from 3.2 per cent in April, witnessing a cumulative fall of around 110 bps. The moderation was primarily driven by a further easing in vegetables, pulses, and cereals prices, which resulted in deflation in the CPI food group for the first time since February 2019, at (-)0.2 per cent in June. Fuel group inflation also moderated to 2.6 per cent in June from 2.9 per cent in April. Core inflation, however, edged up to 4.4 per cent in June 2025 after remaining broadly steady between 4.1 to 4.2 per cent during February to May.

15 Vegetable prices declined by 19.0 per cent while pulses prices declined by 11.8 per cent in June 2025.

16 Fuel group inflation also moderated to 2.6 per cent in June from 2.9 per cent in April.

17 CPI headline excluding food and fuel.

18 As on July 16, 2025, the stocks held by the Food Corporation of India for wheat stands at 1.3 times the buffer norms (stocks highest in last 4 years) and for rice, at 3.9 times the buffer norms.

19 As per provisional figures, India’s services exports grew by 10.1 per cent during April-June 2025-26, while services imports increased by 1.5 per cent during the same period. Net services exports grew by 20.7 per cent during the same period.

20 Gross foreign direct investment (FDI) inflows grew by 5 per cent to US$ 15.9 billion in April-May 2025-26 from US$ 15.2 billion during the same period a year ago. Net FDI inflows contracted by 2.2 per cent to US$ 3.9 billion in April-May 2025-26 from US$ 4.0 billion a year ago.

21 Net portfolio inflows into EMEs during June 2025 stood at US$ 42.8 billion as compared with US$ 16.8 billion in May 2025 (Source: Institute of International Finance).

22 During April-July 2025, there were net inflows of US$ 2.6 billion in equity segment whereas debt segment witnessed a net outflow of US$ 3.5 billion.

23 Net inflows under external commercial borrowings to India increased to US$ 3.5 billion during April-June 2025-26 as compared with US$ 1.6 billion a year ago. Non-resident deposits recorded a net inflow of US$ 1.9 billion in April-May 2025-26, lower than US$ 2.8 billion in the same period last year.

24 Based on actual merchandise imports (on a BoP basis) during the four quarters period (Q1:2024-25 to Q4:2024-25) and around 94 per cent of total external debt as on end-March 2025.

25 India’s CAD/GDP ratio moderated to 0.6 per cent in 2024-25 from 0.7 per cent during 2023-24. India’s external debt to GDP ratio increased to 19.1 per cent at end-March 2025 from 18.5 per cent at end-March 2024. The net International Investment position to GDP ratio improved to (-) 8.7 per cent from (-) 10.1 per cent during the same period.

26 The average daily net absorption under the liquidity adjustment facility (LAF) during April and May stood at ₹1.5 lakh crore and ₹1.8 lakh crore, respectively. The average daily net absorption under the LAF further increased to ₹2.82 lakh crore in June 2025 and ₹3.12 lakh crore in July 2025. The daily average absorption under the SDF increased to ₹2.17 lakh crore during June-July from ₹2.06 lakh crore during April-May 2025.

27 In response to the cumulative policy repo rate cut of 100 basis points (bps) in the current easing cycle (up to August 4), the WACR moderated by 108 bps. Since the February policy, 3-month T-bill rate declined by 110 bps, 3-month CP issued by NBFCs by 161 bps and 3-month CD rate by 170 bps.

28 The 5-year and 10-year G-sec yield (6.79 GS benchmark) declined by 63 bps and 28 bps, respectively since the February policy. Over the same period, 5-year AAA corporate bond yields declined by 56 basis points. During this period, the Indian bond market was one of the best performers globally.

29 SCB Parameters: The outstanding credit and deposit on a y-o-y basis increased by 9.9 per cent and 10.5 per cent, respectively, between June-24 and June-25. The system-level Capital to Risk Weighted Assets Ratio (CRAR) of 17.44 per cent in June 2025 was well above the regulatory minimum level. Ratio of non-performing loans improved further (GNPA ratio at 2.24 per cent in June 2025 vis-à-vis 2.67 per cent in June 2024, NNPA Ratio at 0.53 per cent in June 2025 vis-à-vis 0.60 per cent in June 2024). Liquidity buffers were robust, with an LCR of 132.80 per cent as of end June 2025. The annualised return on assets (RoA) and return on equity (RoE) stood at 1.34 per cent and 12.70 per cent, respectively, in June 2025. Net Interest Margin was 3.24 per cent for June 2025 (3.54 per cent in June 2024).

30 NBFC Parameters: Total CRAR of NBFCs was 25.78 per cent and Tier I CRAR was 23.83 per cent in June 2025, well above the minimum regulatory requirements. GNPA ratio has improved from 2.47 per cent in June 2024 to 2.21 per cent in June 2025, while NNPA ratio also improved from 1.08 per cent in June 2024 to 0.95 per cent in June 2025. RoA for the sector decreased slightly from 3.23 per cent in June 2024 to 3.11 per cent in June 2025. NIM has slightly decreased from 4.82% in June 2024 to 4.40% in June 2025.

31 The total flow of resources from non-banks (including domestic and foreign sources) increased by ₹4.3 lakh crore from ₹12.5 lakh crore in 2023-24 to ₹16.8 lakh crore in 2024-25.

32 Bank Credit recorded a growth (y-o-y) of 9.8 per cent as on July 11, 2025 as compared to 14.0 per cent a year ago. Despite the slowdown in bank credit, the total flow of financial resources remained at almost similar levels during April-July 2025-26 as compared with the corresponding period of last year.

33 CP issuances by non-financial entities increased to 0.78 lakh crore in FY:2025-26 (up to June) compared to 0.30 lakh crore a year ago. Corporate bonds issued by non-financial entities increased to 0.95 lakh crore in FY:2025-26 (up to June) compared to 0.09 lakh crore a year ago.