ITO Vs Narpatchand Devichandji Mehta HUF (ITAT Mumbai)

ITAT Mumbai upholds deletion of ₹5.73 Cr addition u/s 68 – Assessee proved identity, creditworthiness & genuineness of loans; repayment with interest clinched the issue

Assessee, a HUF, filed its return declaring income of ₹22.42 lakh for AY 2022-23. The case was selected for scrutiny due to high liabilities & substantial loans appearing in Form 3CD despite low income. During assessment, AO noticed unsecured loans aggregating ₹5.71 crore from multiple parties. He asked for confirmations, bank statements & supporting details. Assessee furnished PAN, confirmations, ITR acknowledgments, bank statements & audited accounts of the lenders.

Despite this, AO concluded that Assessee failed to establish creditworthiness & genuineness of some creditors & made an addition of ₹5,71,82,289 u/s 68 r.w.s. 115BBE treating the loans as unexplained cash credits.

Before CIT(A), Assessee argued that it had discharged its primary onus by filing all necessary documents proving identity (PAN & ITRs), genuineness (banking channel transactions) & creditworthiness (bank statements & balance sheets). Importantly, Assessee demonstrated that the loans were subsequently repaid to the creditors along with interest, on which TDS was deducted & deposited. These repayments were not disputed by Department in subsequent assessments.

CIT(A) held that once Assessee had provided all evidence, the burden shifted to AO to disprove the claim by bringing contrary material. AO made no further enquiry, did not summon any creditor, nor pointed out any defect in the documents. He simply rejected the loans without investigation. CIT(A) further observed that repayment of loan with interest is a strong corroborative evidence of genuine loan transactions, & if the Department accepted TDS & interest in later years, it cannot deny the loan in this year. Accordingly, CIT(A) deleted the entire addition of ₹5.73 crore u/s 68.

Department appealed to ITAT arguing that CIT(A) accepted documents at face value without applying the test of human probabilities & surrounding circumstances. Department claimed that Assessee failed to prove creditworthiness & genuineness in substance.

Tribunal examined the records & agreed with CIT(A). It noted that Assessee had produced PAN, confirmations, ITR acknowledgments, bank statements & balance sheets of all creditors. It also proved actual loan repayment in subsequent years, & payment of interest with TDS, which was accepted by Department. Tribunal held that identity, creditworthiness & genuineness were fully established.

Tribunal also relied on binding precedents:

- PCIT v. Ambe Tradecorp (P) Ltd. (Guj HC) – once identity of lenders is proved & loans are repaid, no addition u/s 68 is permissible.

- CIT v. Ayachi Chandrashekhar Narsangji (Guj HC) – if loan is repaid in next year & Department accepts repayment, addition u/s 68 is not justified.

- DCIT v. Hetal Nitin Shah (ITAT Mumbai, 2024) – when assessee furnishes confirmations, bank statements, ITRs & proves repayment with interest, addition u/s 68 cannot stand.

Tribunal concluded that Assessee had discharged the onus u/s 68. AO made the addition without any contrary evidence or investigation, which is unsustainable. Repayment of loan further supports genuineness. Therefore, CIT(A)’s order deleting the addition was correct.

Result: ITAT dismissed the Revenue’s appeal & upheld deletion of ₹5.73 crore addition. Assessee was not required to prove more than identity, creditworthiness & genuineness – all of which stood established.

Once assessee produces confirmations, bank statements, ITRs & proves actual repayment with interest & TDS, the burden shifts to AO. In absence of contrary evidence, Section 68 addition cannot be made.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

This appeal has been preferred by the Assessee against the order dated 07/04/2025 impugned herein passed by the National Faceless Appeal Centre (NFAC)/Commissioner of Income Tax (Appeals), Delhi (in short, ‘Ld. Commissioner’) u/sec. 250 of the Income Tax Act, 1961 (in short, ‘Act’) for the A.Y. 2022-23.

2. In the instant case, the Assessee had declared total income at Rs. 22,42,320/- by filing its return of income on dated 30/09/2022, which was selected for scrutiny on the following issues: –

i. High liabilities as compared to low income/receipts

ii. Substantial loans given by the Assessee as per Form 3CD of debtors in comparison to Gross Total Income shown in the ITR

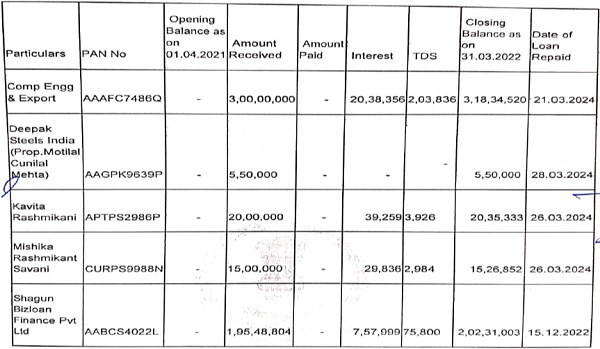

2.1 The Assessing Officer (AO) observed that during the assessment proceedings, the Assessee had taken various loans from the following parties: –

| Sr.No | Description | Amount |

| 1 | Comp Engg. & Exports | 3,18,34,520 |

| 2 | Deepak Stels India | 5,50,000 |

| 3 | Kavita Rashmikantsavani | 20,35,333 |

| 4 | Mishika Rashmikant Savani | 15,26,852 |

| 5 | Shagun Bizloan Finance Pvt. Ltd. | 2,02,31,003 |

| 6 | Vidhi Savani | 15,26,804 |

2.3 The Ld. AO, therefore, in order to verify the aforesaid unsecured loans, asked the Assessee to furnish confirmations of unsecured loans from the said parties.

2.4 The Assessee in support of its claim, furnished confirmations of unsecured loans from various parties with supporting documents.

3. On perusing the details and documents provided by the Assessee, the AO analyzed the same and ultimately, found that Assessee has not proved creditworthiness of the persons, who advanced loans to the Assessee, while in some cases creditworthiness and genuineness of the transactions could not be proved and therefore, he ultimately made the addition of Rs.5,71,82,289/- u/sec. 68 r.w.s. 115BBE of the Act, as unexplained income and added the same to the total income of the Assessee.

4. The Assessee, being aggrieved, challenged the said addition by filing first appeal before the Ld. Commissioner and in order to prove the genuineness, creditworthiness and identity of the loan creditors, furnished following documents: –

i. Copy of ITRs acknowledgments

ii. Loan Confirmations

iii. Bank statements

iv. Audited statement of accounts

4.1 The Assessee before the Ld. Commissioner further claimed that from the ITR acknowledgments, the identity of the parties was proved, as they are known to the Income Tax Department. Further, from the bank statement of the parties, who advanced loans, creditworthiness is also proved. Further, as all the amounts were received through banking channels, genuineness of the transactions is also proved.

4.2 The Assessee before the Ld. Commissioner further claimed that the primary onus casted upon the Assessee, has been discharged and thereafter it was for the AO to examine the evidence and documents and bring material on record to show that the loans were not genuine. The Assessee also claimed that it has already repaid the amount of loans along with interests by deducting the TDS as detailed below: –

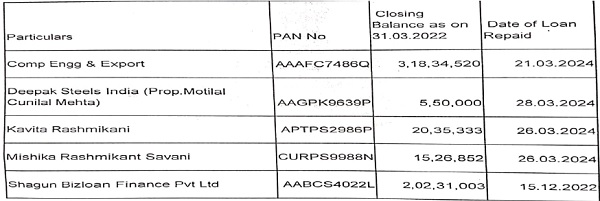

5. The Ld. Commissioner by considering the aforesaid facts and circumstances of the case and documents filed by the Assessee in order to discharge its onus casted upon it, and the loan confirmations and bank statements of the creditors, which reflects that loans taken were already repaid in the subsequent years, detailed below: –

Ultimately, deleted the addition of Rs. 5,73,81,289/- made by the AO u/sec. 68 of the Act, by observing and holding as under: –

“4.4 The contention of the appellate assessee that by submitting the aforementioned documents, it has discharged its onus of prima-facie establishing the identity, genuineness and creditworthiness of the loan creditors, and therefore, if there were any reasons for the AO to doubt the claim of the assess, the AO should have asked for additional documents, or have conducted additional enquiries and has brought new and additional evidences on record to substantiate his claim and could have proven the assessee wrong, seems reasonable. From the AO order, it can be seen that no such course of action was taken by the AO. Therefore, I am of the considered opinion that there is no material to show that the credits in the books of account of the assessee are unexplained cash credits. In these circumstances the addition made u/s 68 of the Act by the AO does not have any reasonable basis, and therefore, on this point itself, this addition is liable to be deleted.

4.5 to 4.13 x x x x x x

4.14 For the reasons given above, and after due consideration of all the facts and circumstances of the case, I am of the considered view that the assessee has been able to establish the identity, genuineness and creditworthiness of the loan creditors, especially in light of the fact that the AO has not been able to bring contrary facts and evidences on record. Further, as the loans have been repaid subsequently the assessee, it also cannot be said that the assessee is the beneficiary of the loans so received. Furthermore, the loan repayment in itself is a corroborating fact in support of the claim of the assess. In light of these, and respectfully following the decisions of the various higher courts cited supra, I direct the AO to delete the addition of Rs. 5,73,81,289/- made u/s 68 of the Act as unexplained cash credit. Accordingly, the ground of appeal no. 1 taken up by the appellant is allowed.”

6. The Revenue Department, being aggrieved with the decision of the Ld. Commissioner in deleting the addition under consideration, has preferred the instant appeal.

7. The Learned Departmental Representative (DR) has claimed that Ld. Commissioner has erred in deleting the addition without appreciating the fact that the nature of the transactions by accepting the documentations presented by the Assessee at face value, without adequately considering the fact that Assessee has failed to prove the creditworthiness and genuineness of the transactions. Further, Ld. Commissioner failed to apply the test of probabilities, the surrounding circumstances and diligent exercise before deleting the addition under consideration. Further, the onus upon the Assessee to establish the genuineness of the creditors, however, the Assessee has failed to discharge its onus and therefore, the impugned order, is liable to be set aside.

8. On the contrary, learned counsel for the Assessee has demonstrated the fact that Assessee before the authorities below not only filed the details and documents pertaining to receiving the loans from the aforesaid parties, but infact also, provided the loan confirmations along with relevant documents, such as ITR acknowledgments of the loaners and bank statements and details of repayments of loans along with interest and by deducting the TDS etc. just to prove the genuineness of the loan transactions, identity and creditworthiness of the loaners and, therefore, the Assessee has prima-facie discharged its onus caste u/sec. 68 of the Act and thus, the Ld. Commissioner by considering the peculiar facts and circumstances of the case and documents filed by the Assessee in totality, has correctly deleted the addition. Therefore, in the decision of the Ld. Commissioner, no interference is required.

9. Heard the parties and perused the material available on record. Admittedly, the Assessee before the Authorities below, in order to establish genuineness of the transactions and identity and creditworthiness of the loaners has submitted following details and documents: –

| Sr. No. |

Name of party & PAN |

Documents Required by AO |

Supporting evidences/documents of appellant |

Amount added by AO (Rs.) |

| 1 | Comp Engg & Export PAN : |

|

|

3,18,34,520 |

| 2 | Deepak Steels India (Prop. Motilal Chunilal Mehta) PAN : |

|

|

5,50,000 |

| 3 | Kavita Rashmikani PAN: |

|

|

20,35,333 |

| 4 | Mishika Rashmikant Savani PAN : |

|

|

15,26,852 |

| 5 | Shagun Bizloan Finance P. Ltd PAN: |

|

|

2,02,31,003 |

| Total | 5,61,77,708 | |||

9.1 It clearly appears from the orders passed by the authorities below that Assessee in support of its claim qua genuineness of the transactions of loans, has duly filed the PAN cards, ledger confirmations, ITR acknowledgments, bank statements and balance sheets etc. of the loaners. It is also a fact, which has not been disputed by the Department that the Assessee in subsequent years has already repaid the loan amounts, to the respective loaners. It is also a fact that Assessee, except in the case of Deepak Steels India qua loan of Rs. 5,50,000/-, has also paid the interest to other four parties by deducting TDS. It is also not disputed that interest and TDS has also been accepted by the Department, in the relevant assessment years. Therefore, Ld. Commissioner by considering above peculiar facts and circumstances and documents substantiated the genuineness of loans and identity and creditworthiness of the loaners and specific fact that loans have already been repaid with interest thereon by deducting the TDS and respectfully judgements mentioned below deleted the addition under consideration.

9.2 We further observe that decision of the Ld. commissioner is in consonance with the following judgments of the Hon’ble High Courts and the Tribunal.

9.3 In the case of PCIT vs. Ambe Tradecorp (P.) Ltd. [2022] 145 taxmann.com 27 (Guj.), the Hon’ble High Court of Gujrat has held that once the identity of the lenders stood proved and loans were also paid subsequently, then no addition is permissible u/sec. 68 of the Act.

9.4 Further, in the case of CIT vs. Ayachi Chandrashekhar Narsangji [2014] 221 Taxman 146 (Guj.) the Hon’ble Gujarat High Court has also considered the identical issue wherein the loan amounts have been repaid by the Assessee in the immediate next financial year and the Department has accepted the repayment of loans, without disputing it and, therefore, the Hon’ble High Court approved the decision of the Tribunal in holding that the matter is not required to be remanded, as no other view would be possible.

9.5 In the case of DCIT vs. Hetal Nitin Shah in ITA No. 1080/MUM/2023, decided on 22/01/2024 the Tribunal at Mumbai has also held “where the Assessee had taken loan from the parties and discharged its initial onus by showing identity and creditworthiness of the lenders along with genuineness of transaction by producing confirmation, ledger, bank statement of lender and income tax returns and Assessee had also produced evidence of repayment of loan”, impugned addition u/sec. 68 made on account of loan amount received by the Assessee was not justified.

10. Thus, on the aforesaid analyzations, we are of the considered view that the Assessee in the instant case, has been able to discharge its prima-facie onus cast u/sec. 68 of the Act and thus, no addition is warranted and, therefore, the Ld. Commissioner has rightly deleted the addition made by the AO by impugned order or illegality and, therefore, the same is sustained, by dismissing the appeal of the Revenue Department.

11. In the result, appeal filed by the Revenue Department stands dismissed.

Order pronounced in the open court on 09.10.2025.