“Explore Faceless Assessments under the Income Tax Act, 1961 – a digital approach for fair and efficient tax processes. Learn about the structure, procedures, and key considerations to navigate this technology-driven tax assessment model seamlessly.”

With the advancement of technology, now taxation related proceedings are also become digital. Now, ITR Filing, tax payment, ITR Assessment are all done through online mode to provide convenience to taxpayer. In this move, Income Tax Department has introduced concept of Faceless Assessment of Income Tax Return. Now, cases that are selected for Scrutiny are assessed through faceless assessment model only. By this concept, department has eliminated the person-to-person interface between the taxpayer and the Department and provide for optimal utilization of resources and a team-based assessment with dynamic jurisdiction.

For doing fair and litigation free Faceless Income Tax Assessment, the department has been divided into 5 Parts:

> National Faceless Assessment Centre

> Assessment units

> Verification units

> Technical units

> Review units

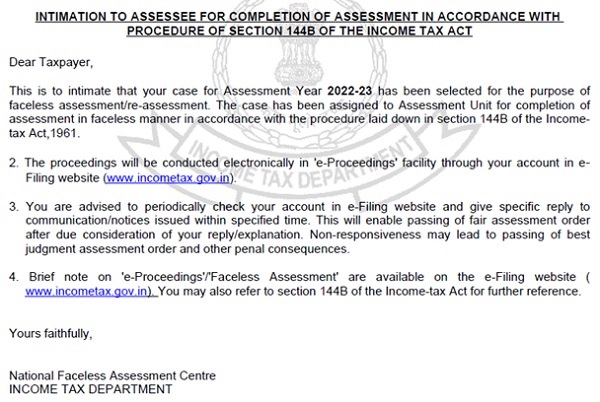

Faceless Assessment under Income Tax Act, 1961 is governed by Section 144B of Income Tax Act. In this section, when a case is selected for Scrutiny as per pre- decided Criteria, then assignment of case is done on automatic allocation basis and intimation is sent to assessee by NaFAC. Below is snapshot of 1st Notice.

Along with this notice, a detailed questioner is sent where, initial documents are demanded which are required for Faceless Income Tax Assessment. After that, a number of communications need to be done between Assessment Unit and assessee. After all communication a show cause notice showing draft Assessment order is shared with the assessee describing the assessable income as determined by Assessment unit.

The assessee has to respond to this show cause notice within specified time period. As we all know, that in case of faceless Assessment all communication is done through written material, there may be chance that, something may be left that can only be expressed, presented by oral/ video presentation, so department gives an opportunity to assesee that, if he require personal hearing through Video Conferencing then he may request to the department for this. After all these procedure, final Assessment order will be passed which becomes binding on assessee. If still assessee is not satisfied with Assessment then he may prefer appeal before CIT(A).

Points to Consider while attending Faceless Assessment

√ You should update a mail ID and Mobile number on income tax portal which you can access easily. As and when any notice/ intimation is sent by department then it is delivered on that mail id.

√ Keep your replies and responses to the point, relevant, and specific to the query raised in the notice.

√ Provide accurate and complete information to the tax authorities.

√ Keep a record of all communication with the tax authorities.

√ Do not panic about receiving any notice/intimation/correspondence from the Income Tax Department. If you are not aware about law and difficulty in replying then, you should take help of professional in handling the case. Wrong communications may lead to wrong Assessment and invite income tax demand from department.

√ Do not ignore and be careless in submitting responses or replies to the assessment notices and intimations.

√ If you thinks that video conferencing is helpful for you to explain your case to the department then do not hesitate in taking video conferencing facility.

√ Provide all material disclosures required in respect of the furnishing particulars of income. Do not try to escape income because now department has almost all information related to you.

*****

Disclaimer: This article is for the purpose of information and shall not be treated as solicitation in any manner and for any other purpose whatsoever. It shall not be used as legal opinion and not to be used for rendering any professional advice. The author will not be held responsible for any lose, if occur after using above information. Kindly consult your professionals before taking any action. This article is written on the basis of author’s personal experience and provision applicable as on date of writing of this article. Adequate attention has been given to avoid any clerical/arithmetical error, however; if it still persists kindly intimate us to avoid such error for the benefits of others readers. The Author “CA. Shiv Kumar Sharma” can be reached at mail –shivsharma786@gmail.com and Mobile/WhatsApp–9911303737