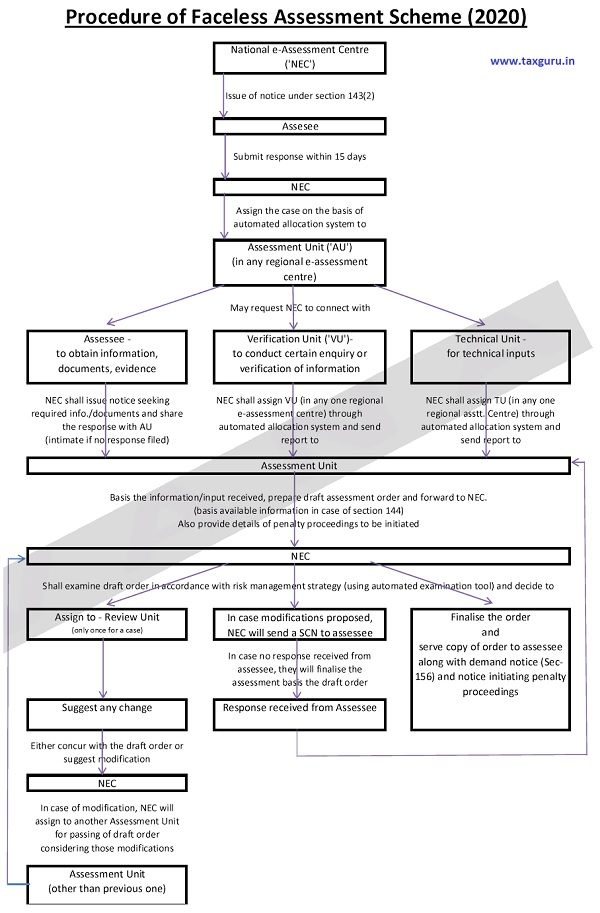

E-Assessment is now Faceless Assessment, CBDT vide Notification no. 60 and 61 of 2020 has amended the earlier provisions for e-assessment and renamed the said scheme as Faceless Assessment. Let’s understand the provisions and procedure as laid down in the Faceless Assessment Scheme. Step by step procedure for Faceless Assessment is tabulated in attached file. Other points to be noted regarding the said scheme are enumerated below:

- All communication among assessment unit (‘AU’), review unit (‘RU’), verification unit (‘VU’), or technical unit (‘TU’) or with assessee or any other person shall be through National e-Assessment Centre (‘NEC’).

- Assessment under section 143(3) and 144 are covered in Faceless Assessment Scheme.

- Transition to Faceless Assessment Scheme – where 143(2) already served by the Income tax authority, or return of income (‘ROI’) not filed in response to 142(1), or ROI not filed in response to 148 and 142(1) also served

- Where Assessee fails to comply with notice issued under section 142(1), or direction under section 142(2A), or notice issued for additional clarification/documents (during assessment proceedings), NEC shall serve show cause notice u/s 144.

- After completion of assessment, NEC will transfer all the electronic records to jurisdictional Assessing Officer (‘AO’), for any further action as required under the Income tax Act.

- NEC may at any stage of assessment proceedings, if considered necessary, transfer the case to jurisdictional AO.

- Assessee/Any Other person shall not be allowed to present in person or through authorised representative

- In case modification proposed in draft order, Assessee (himself or through authorised representative) may seek for personal hearing (for oral submissions in response to show cause notice). Such hearing shall be conducted through video conferencing after taking approval from CCIT/DG of respective regional e-assessment centre

- Any examination or recording of statement shall be through video conferencing only (except under sec 133A)

- CBDT shall establish suitable facilities for video conferencing

- Appeal against such order (or penalty imposed) shall lie before jurisdictional CIT(A) [Section 246A]

- In case of non-compliance of any order, direction, notice (issued under this scheme), any Unit (AU, VU, etc.) in course of assessment proceedings may recommend for initiation of penalty proceedings. Consequent to which, NEC shall serve a notice asking to show cause as to why penalty should not be imposed. Response to such show cause notice shall be shared with Unit, recommended such penalty. Such Unit either drop or make draft order of penalty (and send to NEC). Thereafter, NEC shall serve the order levying penalty to assessee/any other person and transfer records to AO having jurisdiction for further action as required under Income tax Act.

- DSC (‘Digital Signature Certificate’) required or not: NEC – need to use DSC, while Assessee/Any other person : need to use DSC (if otherwise required to use for filing ROI), else may use EVC

- Changes in Notice communication – (i) From NEC to Assessee: Placing copy in assessee’s registered account, or sent on registered e-mail, or uploading on assessee’s mobile app. It shall be followed by real time alert. (ii) From NEC to Any other person: sending on registered email, followed by real time alert

- Assessee need to file response through his registered account

- Officer in charge of NEC, (with due approval of CBDT) shall be allowed to make standards, procedures and processes for service of notice; receipt of response; issue of acknowledgement; provision of ‘e-proceeding’ facility-login, tracking and display; receipt, storage and retrieval; general administration and grievance redressal; circumstances related to personal hearing, etc.

Procedure of Faceless Assessment Scheme (2020)

*****

(The author is a practicing Chartered Accountant in Delhi NCR and can be reached at nak.agg102@gmail.com)

Disclaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice or a formal recommendation. While due care has been taken in preparing this document, certain mistakes and omissions may creep in. V A N A & Associates (or any of its partner) does not accept any liability for any loss or damage of any kind arising out of any inaccurate or incomplete information in this document nor for any actions taken in reliance thereon. No part of this document should be distributed or copied without written permission of the author.