In order to provide relief and lessen the burden on small taxpayers, the Government had announced the tax rebate scheme by introducing Section 87A in the Income Tax Act.

Introduction of Section 87A

Section 87A was introduced in Income Tax Act through the Finance Act, 2003. As per the Income Tax Act, any individual being a resident of India, having a taxable Income below the exemption limit is entitled to claim a rebate of a certain amount.

Criteria to avail the rebate under Section 87A

As per the existing provisions, any Indian Resident individual whose income lies below Rs 5,00,000 is eligible to claim a tax amount rebate under this section. The amount of tax rebate can be either 100% of the total tax amount calculated of his total income or Rs 12500, whichever is lower.

Note:

Earlier the maximum tax rebate limit was ₹2,500 for individuals having net taxable income below Rs. 3,50,000. Through the Union Budget, 2019, the government further hiked the net taxable income to Rs. 5,00,000 and minimum tax rebate limit to Rs 12,500 under Section 87A.

Section 87A – Eligibility

To claim rebate under Section 87A one should:

– Be a resident individual taxpayer of India

– Hold total income after deducting eligible deductions under Section 80, below the total exemption limit i.e., below ₹5,00,000.

Note:

The rebate shall

– Be available on an amount of tax calculated before adding any Education or related cess.

– Be available to only an Individual & not to any Firm/Company/HUF.

– Be available to Senior citizens above 60 years opting for old tax regime

– Is not available to super senior citizens aged above 80 years and opting for old tax regime.

– Is available under both the old tax regime and new tax regime.

Adjustment Of Tax Liability Against Rebate

This rebate can be claimed against the tax liability in respect of normal income which is taxed at the slab rate, long term capital gains under Section 112 of the Income Tax Act. (Section 112 applies for long term capital gains on sale of any capital assets other than listed equity shares as well as equity oriented schemes of mutual funds.) This rebate is also available against the tax liability for short term capital gains on listed equity shares as well as equity oriented schemes of mutual funds under Section 111A of the Act, on which tax is payable at flat rate of 15%.

Section 87A – Form

To claim exemption under Section 87A one has to put the value of tax amount in the column ‘Rebate under Section 87A’ while filling the Income tax return under any respective ITR form, ITR 1, ITR2, ITR4 etc.

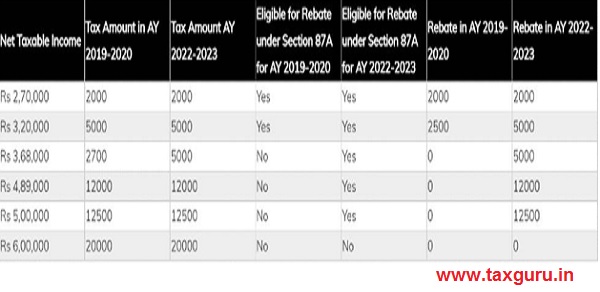

Illustration

Author Bio

My business income is 240000 and short term capital gain is 300000 (111A)i want to add STCG In basic exemption limit my question is am i liable for rebate 87A ?