Chapter 1

Introduction & Background

1.1. Introduction

One of the most significant and influential inventions of 20th century was the Computer. There has been a sea change in the purposes and the manner in which computers are used with advent of microprocessor technology and digital communication. The computer started with being a giant calculating machine. It then metamorphosed itself into a standalone personal tool for performing assorted routine tasks like word processing and accounting and then to today’s network device permeating virtually everything including instantaneous and global personal and business interaction. The way business is conducted and records are maintained today is a far cry from days past. Accordingly, in enforcement agencies including the Income tax department, more and more information is being stored, transmitted or processed in digital form.

The law of the country has also taken cognizance of this reality. The Information Technology Act, 2000 has been enacted recognising electronic records as evidence, governing access to and acquisition of digital and electronic evidence from individuals, corporate bodies and/ or from the public domain. By way of this enactment, amendments were also brought in other laws like Indian Penal Code, Indian Evidence Act and Criminal Procedure Code, (Cr.PC). The Income-tax Act, 1961 has also been amended thrice by way of Finance Act 2001, Finance Act 2002 and Finance Act 2009 thereby according recognition to electronic evidence, facilitating access to them and giving when need be, powers to impound and seize them. By Finance Act, 2001, Clause (22AA) was inserted in Section 2 to provide that the term “document” in Income Tax Act, 1961, includes an electronic record as defined in clause (t) of sub-section (1) of section 2 of the Information Technology Act, 2000. By Finance Act, 2002, Clause (iib) was inserted in Sub-Section (1) of Section 132 requiring any person who is found to be in possession or control of any books of account or other documents maintained in the form of electronic record as defined in clause (t) of sub-section (1) of section 2 of the Information Technology Act, 2000 (21 of 2000), to afford the authorised officer the necessary facility to inspect such books of account or other documents; and by Finance Act, 2009, clause (c) was inserted in sub-section (1) of Section 282 providing that service of notice in the form of any electronic record as provided in Chapter IV of the Information Technology Act, 2000 (21 of 2000) will constitute valid service

Maintaining the integrity of electronic evidence through various processes such as identification of evidence, retrieval of deleted evidence, examination of such evidence, etc., presents problems which are different from the problems encountered in handling of traditional physical or documentary evidence. This Manual attempts to recommend basic operating procedures for handling digital evidence. This includes procedures for getting access to digital evidence, acquisition of the same, their analyses and seizure maintaining the integrity of information taken from stand-alone electronic media, servers and networks where digital information! evidence may be stored.

1.2. The Challenges:

- The records including books of account maintained on papers are mostly replaced by documents in digital form.

- Most organisations use networks connecting different PCs, and servers spread across geographical locations and even sovereign jurisdictions not only for communication but also for conduct of day to day business.

- Computer data including books of account are easy to modify, alter, delete or hide.

- It is very easy to protect data by passwords and encryption making deciphering of real data an extremely difficult task

- The data storage devices come in a large variety of technology, shapes and sizes e.g.

Hard disks- IDE/ATA/PATA/SATA/SCSI/SAS

Laptop Hard Disks – 2.5″ & 1.8″

USB Pen-drives and various types of Flash drives.

USB i-Pods, USB MP3 players

CD & DVD Media, Floppy Media

Mobile SIM cards, Memory Card & Device‘s internal memory

Discovery of these devices and retrieval of the data stored therein presents a challenge.

- Different kind of software, platforms and customized applications used for varied business purposes.

- Digital data being often stored on networked servers which are normally! remotely accessed. Instances of such data being placed on shared International Networks and Platforms having transnational jurisdictions have come to light. The server may not be available for seizure during survey or search. Instead, all data may be stored in, what they call, ―cloud server‖, i.e , a server located in even a foreign country thousands of miles away and the searched ! surveyed party is sitting merely with a monitor! laptop.

- Specialised skills are required to identify relevant data, safely retrieve them, properly analyze them for their evidentiary value, and to subsequently produce them in a manner that their integrity can be established in any formal proceedings such as assessment! appeals and prosecution, etc. With ever changing and improving technology, skills are also required to be honed and updated regularly.

- The environments in which Income-tax Authorities function during field actions are different from other law enforcement agencies. Thus, the requirement of standard procedure for Income-tax Department is slightly different and needs to be flexible as compared to other agencies dealing with other crimes!laws.

1.3. Current practices in the department

There are at present no uniform instructions on how to access computer systems, other digital devices and retrieve digital data during a search operation. Different practices are being followed-

- Taking hard copies of data and seizing the same

- Using a CD writer or USB pen drive or USP Portable Hard Drive to take copy of data on the original hard disk

- Seizing Hard disks or computers and taking them to office

Very often, copying is done with Windows utilities and without any forensic software.

1.4 Shortcomings of current practices

1.4.1 These methods are forensically unsound. If proper procedures are not followed data integrity and authenticity can be compromised. Some of the grounds on which integrity of seized data can be challenged are:

- When a system, seized on a particular date, is switched on! booted at a later date to view its content, the date and time of opening these files automatically get modified.

- If a seized system is not booted on its own and its hard disk is attached to another system, even then Operating System has an automatic functionality to write to all attached media. Folders with the system restore-tag get created in all new disks attached to the Investigator’s ( An officer! official of the department entrusted with the task of investigation) system. Further, the anti-virus software on the Investigator’s system scans files on the seized hard drive, in the process changing the date and time. The anti-virus program may even delete or quarantine critical evidence on the seized disk.

- Accessing a system or hard disk in any way without the use of write-protect‘ devices causes change in the hash value or digital fingerprint of the disk. This can render the evidence on such disks inadmissible.

1.4.2 Sometimes even valuable data may be lost because of the use of unsound

methods:

- Logic Bombs: Some systems are loaded with destructive software tools which get activated if the system is not shut down ! started with a particular set of keystrokes. These can cause severe! unannounced damage to the file systems as well as to critical files if programmed to do so. It is important that the investigating team does not in any way trigger them.

- Live Data: If a system is active or live when the search or survey team enters the premises and if these systems are made to shutdown, then the live data in systems mainly the RAM memory can not be retrieved. Such data are most vital in some cases because RAM may contain recently used passwords, details used in internet transactions etc. The programs and the processes which were running in the system may get closed leaving no clue on such information.

1.4.3 Some other ill consequences of using above methods can be as under:

- Password: In a case where the system has password(s), shutting down the system would create problems in opening the same later without knowing the password(s) and cracking the same is a time – consuming process.

- Another major problem in the current work practices is that the retrieval of hidden, password – protected and deleted files. These files cannot be retrieved by making copies of the hard disk or taking its printouts.

- Lack of knowledge on some new server architecture such as RAID, where

1.5 The objective of Manual

This manual is an attempt to provide basic information about the digital evidence, its nature, legal implications and also to lay down! recommend basic ingredients of standard procedure to handle digital evidence right from its identification to its acquisition! seizure and its analysis.

The aim of this manual is to apprise the user of :

i. The basic nature of digital evidence;

ii. Basic legal provisions relating to digital evidence in Income-tax Act and other laws including Information Technology Act and Indian Evidence Act;

iii. Basics of Computer Forensics and international best practices;

iv. Identification and preliminary analysis of Digital Evidence;

v. Recommended Standard Operating Procedures and documentation to acquire and!or seizure of Digital Evidence maintaining authenticity and integrity of Digital Evidence;

vi. Analysis of Digital Evidence;

vii. Archival of Digital Evidence;

viii. Mobile Forensic

ix. Information about cyber forensic facilities.

x. Case Studies in Digital Evidence Forensic

Though the requisite hardware/ software and technical support is not available in several stations, the departmental officers are advised to take initiative and create necessary infrastructure and awareness and follow the recommended procedures as far as possible. Some of the examples given on various software/hardware are only used for illustration and in no way re commendatory or mandatory to be used.

Chapter 2

The Digital Evidence

2.1 What is Digital Evidence?

“Digital evidence” or ―”Electronic Evidence” is any probative information stored or transmitted in digital form that may be used before the courts/ Income-tax authorities. Section 79A of the IT(Amendment) Act 2008 defines electronic form evidence as

“any information of probative value that is either stored or transmitted in electronic form and includes computer evidence, digital audio, digital video, cell phones, digital fax machines”

The main characteristics of the digital evidences are,

1. It is latent as fingerprints and DNA

2. Can transcend national borders with ease and speed

3. Highly fragile and can be easily altered, damaged or destroyed and also time sensitive.

For these reasons, special precautions should be taken to document, collect, preserve and examine this type of evidence.

2.2- Digital Devices: Sources for Digital Evidences

The use of digital devices in day to day life has increased tremendously. Accordingly, we may come across a wide range of the digital evidence which include E-mail word processing documents, data base tables, files saved from accounting programmes, digital photographs, ATM transaction logs, instant message histories, internet browser histories, the contents of computer memory, computer back-up, global positioning system tracks, digital video or sound files, data stored in mobile telephones and the data stored in all types memory storage devices. To help the understanding of the investigating officers, a compilation of various devices and the potential evidences these devices may contain is provided below:

|

Sl No |

Digital Device | Potential Evidence |

| 1 | A Desktop Computer | The device contains all the files and folders stored including deleted files and information which may not be seen normally. Analysis of key document files like word documents, excel files, email‘s tally data may help in unearthing potential evidences. Retrieval of deleted files using Cyber Forensics can help get key evidences that have been destroyed. |

| 2 | Pen Drives | The device stores many files and may be hidden easily. In many cases the parallel books of accounts maintained as tally data or excel sheets are kept in Pen Drives that can be easily hidden |

| 3 | Hard Drives | The device stores many files and may be hidden easily. Backup of earlier years may be kept and may be easily hidden. |

| 4 | Handheld Devices like Mobile Phones ( Smart Phones), Electronic Organizer, IPAD, Personal Digital Assistant etc |

Much information can be obtained from the devices like Address Book, Appointment calendars/information, documents, emails, phone book, messages( text and voices),video recording, email passwords etc. Many applications like CHAT, Whatsapp application can store many crucial conversations important for the investigations. Remittances and transactions are done by fund transfer through mobile phone service providers utilizing money deposited with the latter bypassing banking channels. A person may do all his business through a mobile phone without any computer or laptop or warehouse for his inventory – as example, online business platform www.amazon.com maintains huge warehouse at several places in India where online traders can store their merchandise. In such cases the trader may make all transactions through mobile phone and store in small external microchips making detection difficult. |

| 5 | Smart cards, Dongles and Biometric Scanners |

The device itself enables to understand the user level access to various information and places. |

| 6 | Display Monitor ( CRT/LCD/TFT etc), Screens of Mobile Phones if switched on |

All the graphics and files that are open and visible on the screen in the switched on systems can be noted as electronic evidence. This evidence can be captured only in video, photographs and through description in seizure memos |

| 7 | Answering Machines | The device can store voice messages and sometimes, the time and date information about when the message was left. It may have details such as last number called, memos, phone numbers and names, caller identification information and also deleted messages. |

| 8 | Local Area Networks (LAN) Card or Network Interface Cards | The device itself is a digital evidence and may contain crucial evidences |

| 9 | Modems, Routers, Hubs and Switches | The device may contain details of IP addresses where the actual data is stored. |

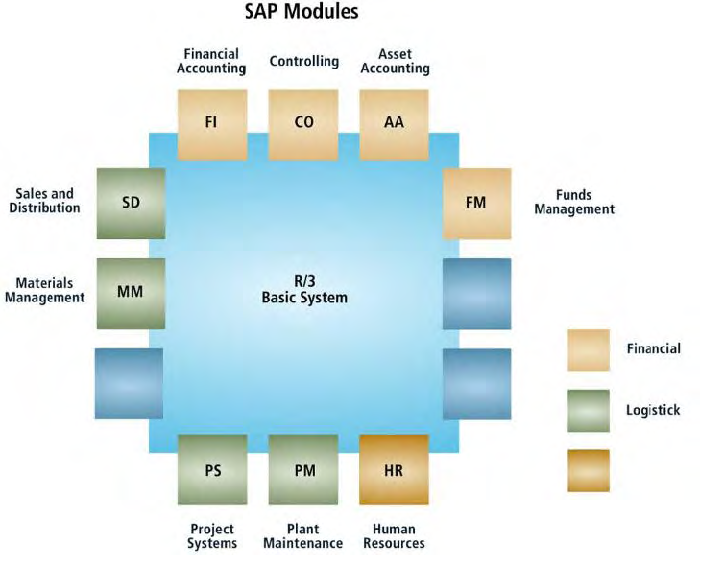

| 10 | Servers | Contains crucial data on business related applications like SAP, ERP, CRM, Mail Servers. The device is a potential evidence for pulling out audit logs using forensic analysis. Analysis of emails of key persons from Mail Servers can help in finding crucial evidences required for the case. |

| 11 | Removable storage devices like SD Cards in Mobile phones | All new generation phones use these and store files in which evidence can be found. |

| 12 | Scanners and Copiers | The device itself, having the capability to scan may help prove illegal activity like making bogus bills etc. Copiers may also contains stored data which can be crucial evidences. |

| 13 | Digital Cameras | The device can be looked for images, videos, sounds, removable cartridges, time and date stamps |

| 14 | Pagers | The device can be looked for address information, Text message and phone numbers |

| 15 | CD/DVDs/ | The device stores many files which may contain the evidence |

| 16 | Facsimile Machines | The device stores some documents, phone numbers, send/receive logs that can contain the evidence. |

| 17 | Global Positioning Systems(GPS) | The device may provide travel logs, home location, previous destinations etc which may be crucial in finding places where evidences may be stored. |

| 18 | Cloud Data Servers | The device is available on all smart phones and tablets. The Cloud may be used to store hidden data where crucial evidences may be stored. Some enterprises offer service for storage of commercial data in servers located in foreign countries and business data are stored there through internet – which can be accessed as per terms and conditions. |

From the digital devices, two types of evidences are possible, one is persistent evidence and other is volatile evidence:

- Persistent evidence: the data that is stored on a local hard drive and is preserved when the computer is turned off. For example, Documents (word, slide, sheet, pdf), Images, Chat log, Browser history, Registry, Audio / Video, Application, Email, SMS / MMS,Phone book, Call log

- Volatile evidence: any data that is stored in memory, or exists in transit, that will be lost when the computer loses power or is turned off. For example, Memory, Network status and connection, Process running, Time information

It is to be noted that in certain cases, where volatile evidence is crucial, switching off a switched on system may result in destruction of volatile evidence.

2.2- Digital Forensics-What is it and its significance?

Digital forensics is the process of identifying and collecting digital evidence from any medium, while preserving its integrity for examination and reporting. It can be defined as the discipline that combines elements of law and computer science to collect and analyze data from computer systems, networks, wireless communications, and storage devices in a way that is admissible as evidence in a court of law.

Digital evidence gathering is becoming an increasingly powerful tool for the department in its fight against tax-evasion. It can be used individually as key evidence or alongside more traditional methods of evidence gathering, where it could serve as a complement to other types of evidence. Furthermore, digital evidence may help in the course of the investigation phase to prepare the next steps.

In a nutshell, the significance of digital evidence analysis is that it:

- Help reconstruct past event or activity

- Show the evidence of policy violation or illegal activity

- Ensure the overall integrity of network infrastructure

2.2- Digital Forensics-Various Branches

The branch of Digital forensics can be classified as follows:

1. Disk Forensics deals with extracting information from storage media in the form of active , deleted files and data from unallocated , slack spaces

2. Network Forensics is a branch of Cyber forensics dealing with monitoring and analysis of computer network traffic for the purposes of information gathering, legal evidence or intrusion detection

3. Database Forensics is a branch of digital forensic science relating to forensic study of databases and their related meta data. This may be of help in understanding the time stamp of the database data created to see whether any manipulations where done in the original database

4. Mobile device forensics deals with examining and analyzing mobile devices to retrieve call logs, SMS/MMS, videos, audios, photos etc.

5.Email Forensics deals with recovery and analysis of emails including deleted emails, calendars and contacts

6. GPS Forensics deals with examining and analyzing GPS devices to retrieve Track logs, Track points, routes , stored locations, home offices etc

2.3- Key Elements of Digital Forensics

Key Elements of Digital Forensic are as follows:

1. The identification and acquiring of digital evidence: Knowing where the digital evidence is present, stored and what are the processes that can be used to retrieve the digital evidences is the first step. It is noticed that usually in big corporations, where huge number of digital devices is present, identification of crucial digital evidences will save time in analysis of digital evidence and also cost. Many a times it is noticed that Customized software’s like ERP/SAP are used and strategy to retrieve the entire software should be discussed with the system administrator. It is also important to identify the types of information stored and the appropriate technology that can be used to extract it. After the evidence is identified the forensic examiner/investigator should image/clone the hard disk or the storage media

2. The preservation of digital evidence should be done in such a manner that there is no possible alteration, damage, data corruption or virus introduction during the process of examination.

3. The analysis of digital evidences involves discovering all the files on the subject system. This includes existing normal files, deleted yet remaining in Recycle bin, hidden files, password-protected files and encrypted files. The analysis also includes retrieval of deleted files and also gives accesses to hidden files, temporary files and protected files. In many business specific applications like customized jeweler software/real estate software, may give details of reports required for day to day functioning of the organization.

4. Report the findings, means giving the findings, in a simple lucid manner, so that any person can understand. The report should give description of the items, process adapted for analysis, chain of custody on the movement of digital evidence, hard and soft copies of the findings, glossary of terms etc

5. The presentation and use of digital evidence in assessment order and presentation of the same in court of the law in matters of appeal involves stating the credibility of the processes employed during analysis for testing the authenticity of the data.

2.4- What Cyber Forensics Can Reveal to AO

Digital Evidence actually has several advantages over other kinds of physical evidence:

- It can be duplicated exactly and a copy can be examined as if it were the original. Importantly, copies made following proper procedures have the same evidentiary value as the original. It is a common practice when dealing with digital evidence, to examine a copy thus avoiding the risk of damaging the original.

-

With the right tools it is very easy to determine if digital evidence has been modified or tampered with by comparing with the original.

- It is possible to recover and analyze deleted files that have not been overwritten, as well as carving out portions of files and text from unallocated and slack space

- It is possible to do String and Key word searching for finding key files either present, deleted files etc

- It is possible to do time line analysis to see when the digital evidence was created, modified, changed, merged with other files etc

- It is possible to know manipulations in data by seeing changes done by unauthorized persons in the data.

2.5 The challenges in dealing with Digital Evidence.

- The digital evidence collected and presented should be admissible in law and steps should be taken to maintain integrity of the data.

- Digital evidence, which is ephemeral, poses problems for searching and seizing. Computer data changes moment by moment and is invisible to the eye. It can be viewed indirectly only after applying proper procedures and processes for collecting evidence.

- Problems posed by recovery of deleted evidence are the challenges which law enforcement agencies have to tackle.

- It is very easy to keep digital data in encrypted or password protected mode. It is difficult to decipher the real information without knowing and getting the password or without having the key to the encryption

2.6-The Legal Background:

2.6.1 The Information Technology Act-2000 has been enacted to provide legal recognition to transactions carried out by means of electronic data interchange and other means of electronic communication, which involve the use of alternatives to paper-based methods of communication and storage of information. The same enactment has also brought amendments in the Indian Penal Code, 1861, the Indian Evidence Act, 1872, the Bankers’ Books Evidence Act, 1891 and the Reserve Bank of India Act, 1934.

2.6.2 As far as Income-tax Act, 1961 is concerned, it has been amended thrice by way of Finance Act, 2001, Finance Act, 2002 and Finance Act, 2009 respectively.

- By way of first amendment, provisions of sub-section (12A) of section 2 was inserted to give legal recognition to the books of account maintained on computer and sub-section (22A) to section 2 was inserted to provide definition of ‗document‘ which included ―electronic record‖as defined under Information Technology Act 2000.

Under Information Technology Act 2000 an electronic record has been defined to include data, record or data generated, image or sound stored, received or sent in an electronic form or micro film or computer generated micro file. This definition of electronic record is wide enough to cover person in possession of computer, storage device, server, mobile phone, i-Pod or any such device.

The above amendment has thus specifically given recognition to electronic record as admissible evidence at par with ‘document’. Further, the powers to impound/copy a document during a survey action u/s 133A and power to seize a document during a search and seizure operation has also been automatically extended to electronic records as a result of the amendment.

- By way of second amendment, provisions of section 132 (1)(iib) were inserted facilitating access to the electronic devices including computer, containing document or books of accounts in the form of electronic records by making it obligatory for the person under control of such device to afford the necessary facility to inspect such records.

By Finance Act, 2009, clause (c) was inserted in sub-section (1) of Section 282 providing that service of notice in the form of any electronic record as provided in Chapter IV of the Information Technology Act, 2000 (21 of 2000) will constitute valid service.

2.6.3 Under Indian Evidence Act there are several references to documents and records and entries in books of account and their recognition as evidence. By way of the THE SECOND SCHEDULE to the Information Technology Act Amendments to the Indian Evidence Act have been brought in so as to, incorporate reference to Electronic Records along with the document giving recognition to the electronic records as evidence.

Further, special provisions as to evidence relating to electronic record have been inserted in the Indian Evidence Act, 1872 in the form of section 65A & 65B, after section 65. These provisions are very important. They govern the integrity of the electronic record as evidence, as well as, the process for creating electronic record. Importantly, they impart faithful output of computer the same evidentiary value as original without further proof or production of original. Accordingly, while handling any digital evidence, the procedure has to be in consonance of these provisions.

2.6.4 Under Indian Penal Code several acts of omission and commission relating to various documents and records are treated as offences. By way of the THE FIRST SCHEDULE to the Information Technology Act, Amendments to the Indian Penal Code have been brought in, so as to incorporate reference to Electronic Records along with the document.

2.7 The sanctity and relevance of Digital Evidence

As in the case of written or oral evidence, digital evidence can also be classified into three main categories:

i. Material evidence: Material evidence is any evidence that speaks for itself without relying on anything else. In digital terms, this could be a log produced by an audit function in a computer system, the books of account maintained on a day-to-day basis on the computer, or any inventory management account maintained on the computer etc., if it can be shown to be free from contamination.

ii. Testimonial evidence: Testimonial evidence is evidence supplied by a witness. This type of evidence is subject to the perceived reliability of the witness, But if the witness is considered reliable, testimonial evidence can be almost as powerful as material evidence. For example, word processor documents written by a witness could be considered testimonial as long as the author is willing to depose that he wrote the same.

iii. Hearsay: Hearsay is any evidence presented by a person who is not a direct witness. Word processor documents written by someone without direct knowledge of the incident or documents whose authors cannot be traced fall in this category? Except in special circumstances, such evidence is not admissible in court of law. But even such evidence may constitute material and may be very relevant in Income-tax proceedings, which are not bound by technical rules of evidences. Otherwise also, they can provide important leads for further investigation.

Accordingly, merely gathering electronic evidence is not sufficient. Efforts have to be made to corroborate the contents therein vis-à-vis other evidence such as material and oral. Preliminary and detailed statements of the persons in control of computers/ electronic devices are always very important.

2.8 Importance of standard procedures to deal with Digital Evidences

From the above discussion on the nature and legality of digital evidence, it is clear that investigation in an automated environment require standard methods and procedures for the following main reasons:

i. Evidence has to be gathered in such a way that the same would be accepted by a court of law. This should be easier if standard procedures are formulated and followed. This would also facilitate exchange of evidence in cases having interdepartmental and international ramifications especially if investigators from other departments and countries collect evidence in similar manner.

ii. Every care must be taken to avoid doing anything which might corrupt or add to the data, even accidentally or cause any other form of damage. The use of standard methods and procedures would diminish this risk of damage. In some cases, some data may be changed or over-written during the process of examination. Thus, there is need for a thorough understanding of technology which is being used by the investigator for examination and also need for its documentation so that it would be possible to explain the causes! effects later on in a court of law.

iii. Some of the most important reasons for improper evidence collection are poorly written policies, lack of an established incidence response plan, incidence response training and a broken chain of custody.

“Chain of custody” is the roadmap that shows how evidence was collected analyzed and preserved in order to be presented as evidence. Establishing a clear chain of custody is critical because electronic evidence can be easily altered. A clear chain of custody would demonstrate that electronic evidence is trustworthy. Preserving a chain of custody for electronic evidence, at a minimum, requires that;

i. No data has been added, changed, deleted from the seized information evidence.

ii. The seized !information evidence was duplicated exactly and completely.

iii. A reliable and validated duplication process was used.

iv. All media were secure and safe.

2.9 Fundamentals of procedure to deal with digital evidence.

2.9.1 For ensuring integrity of the evidence being seized – Write Blocking

- It is essential that no changes should be made while handling digital evidence. A change of a single Bit may render the whole evidence inadmissible. This can be achieved by write blocking the storage media which is intended to be acquired/seized by adopting a technology commonly referred to as “Write Block”

- This is a technology, which ensures that nothing is written on a particular storage media that has been write blocked.

- This technology can be implemented both through hardware and software.

2.9.2 Duplicating evidence for analysis – Acquisition of Evidence- Bit flow technology

- It is essential and advisable that the original evidence should not be used for analysis, since digital technology permits to make exact replicas of any digital evidence. This can be done safely by making a bit stream back-up.

- Bit steam Back-up: This is a process by which a storage media is copied by reading each bit and then transferring it to another storage media thereby ensuring that an exact copy of the original digital evidence is prepared.

- Bit stream imaging differs from copying in that copying applies to data that is not deleted and whose location is recorded in the FAT whereas, bit-stream imaging captures and copies all data on a disk including deleted files, swap files, slack space, FAT unallocated space and FAT unaddressed space. Bit-stream backup is a mirror image of the copied disk with the same hash value.

2.9.3 For Authentication and Seizure of Evidence -Mathematical Hashing:

Mathematical hashing is equivalent to one-way encryption. Every digital evidence at the lowest level translates into a big numerical number. When the digital device or data is encrypted using a hashing algorithm, it results in a new number of a fixed length called the dark message digest. The hashing algorithm has some unique characteristics, which are as follows:

- Message digest always of a fixed length: The digital evidence may be of any size, but on application of the hash algorithm the resultant message digest would always be of a fixed length.

- Message digest is a randomly generated number: The message digest is a randomly generated number. However, if the contents of the digital evidence remain the same, the hash algorithm would generate the same message digest every time it is applied on the digital evidence. This property is useful in authenticating seized digital evidence before a court of law. If application of hash algorithm on digital evidence in a court of law results in the same message digest as was obtained during the time of seizure, it indicates that the presented evidence is the same as what was seized.

- One-way hash function: It is computationally not feasible to determine the contents of the digital evidence if somebody knows the message digest. Hash algorithm is a one-way function. This property is of great importance from the legal point of view, since it prevents manipulation of digital evidence as no one can predict the message digest that would be generated of evidence is manipulated.

- Collusion free hash: The odd that two digital evidences with different contents have the same message digest is roughly 2 to the power128 (i.e. 34 followed by 37 zeros). Their properties have two advantages:

- Each digital evidence can be seized uniquely by specifying its message digest.

- If two digital evidences have the same message digest there is a reasonable certainty that their contents match exactly.

Limitations

By comparison of the message digest of acquired evidence with the message digest of the original the integrity of the acquired can be authenticated, if both message digests are same. However, if the two messages do not match, it is impossible to determine what has changed.

2.8 Important terms in collection of Digital Evidence

- Seizure: The process of generating a unique identity (Message Digest) of the digital evidence in a write block, and trusted environment, which is thereafter taken in the custody of the law enforcement official for the purpose of investigation.

- Acquisition: The process of making Bit-stream image of the digital evidence proposed to be seized in a write block and trusted environment. The process is deemed to be successfully completed if the message digest of the original digital evidence being seized matches with the message digest of the Bit stream backup copy made on a forensically sterile storage media.

- Seizure and Acquisition – The process of simultaneously generating a message digest and a bit-stream backup of the digital evidence proposed to be seized in write block and trusted environment. The process is deemed to be successfully completed if the message digest of the original digital evidence being seized matches with the message digest of the bit stream backup copy made on a forensically sterile storage media.

2.10 Search and seizure of Physical Evidence vs. Digital Evidence

2.10.1 The search & seizure action u!s. 132 of the I T Act is authorized when the designated authorities have reasons to believe that;

i) A person is in possession of certain books of account/documents which are relevant for or useful to any proceedings under Income-tax Act which the said person has not produced when asked to do so or there is a likelihood of such person not producing these documents! books of account before Income-tax authorities.

or

ii) The person is in possession of money, bullion, jewellery or other valuable article or thing (assets) which represent wholly or partly some undisclosed income.

2.10.2 In the conventional search of a premise the search team physically searches for the relevant documents! books of account and assets in the premises. The relevant assets! documents are also seized during the course of search. It is very easy to visualize the search operations involving a physical item including an asset or document other than an electronic document. The rules and procedures are also well laid out in respect of search and seizure of physical items. The authorized officers are also generally very clear about identification of relevant documents and assets which are required to be seized.

2.10.3 The act of entering the premises triggers a “search”. Once legitimately inside the premises, the Search team is entitled to force access to all places within the said premises. When the search team has a warrant, it is allowed to take away any evidence of undisclosed income! asset. The widespread use of computers in recent years has led to a new type of situation in searches of data stored on computer hard drives and other storage devices. Though it is fundamentally similar to the search of physical evidence but in practice is substantially different. The Rules and Procedure governing search of data and its acquisition are still not well settled.

2.10.4 The question is, how should provisions of section 132 of the I T Act apply to the retrieval of data from data storage devices? The dynamics of computer searches turn out to be substantially different from the dynamics of conventional searches. The entire-search, identification of evidence-seizure dynamic of premises searched is replaced by things like scan, acquisition, search and identification of evidence dynamics. Computer forensics analysis is typically performed subsequent to a search operation at the Income-tax Office or cyber forensics laboratory. Weeks or month after the computer has been seized from the target’s premises,an analyst may comb through the world of information inside the computer and try to find the relevant evidence.

2.10.5 Computer searches and premises searches are similar fundamentally in so far as, in both cases, the search teams attempt to find and retrieve useful information hidden inside a closed container. However, the process of searching computers turns out to be considerably different from the process of searching physical spaces.

2.10.5.1 For a physical item, the combing action is generally concluded at the premises itself, exact physical evidence or asset is identified and seized at the premises searched. For example, if the search team is looking for unaccounted jewellery – it will enter in to the premises – search each and every room – in each room it will search for various containers/secret places such as almirah, lockers, etc., – in almirah, lockers, etc., it will look for jewellery – make an attempt to find out the jewellery which is unaccounted and seize the unaccounted jewellery.

2.10.5.2 In case some almirah or lockers are found locked – the search team will either break open the same and will look for the jewellery or put prohibitory order and subsequently after opening the almirah / locker/ room complete the search and seizure procedure. Thus, in our situation only the relevant asset will be seized.

2.10.5.3 Just because 20 boxes are found in a premise would not mean seizure of all 20 boxes. Physically also this is not possible. The search team applies its skills and discretion at the premises to make specific seizure.

2.10.5.4 Similarly the physical documents are also checked and the relevant documents only are seized. Even if the identification of relevant documents is not précise, the authorized officer uses his experience and skills to at least exclude the totally irrelevant documents and make seizure of only those documents which are found relevant or which at least has a possibility of being relevant. Thus, the search and seizure action of physical item is quite specific.

2.10.5.5 Though the computer search and physical search of a place are similar fundamentally because the search team attempts to find and retrieve relevant evidence hidden inside the computer. Search of a computer is easy as well as difficult for many reasons. In computers, just like 20 boxes in above example, there may be thousands of folders. The authorized officer may not know as to in which folder relevant documents/ information is lying. He can however, acquire/seize entire data if he chooses to. But identification of specific and relevant data is very time consuming job and possibly can not be completed in the premises itself in most of cases. task, therefore is to first scan various devices to identify the device which may contain relevant evidence and acquire them, instead of acquiring each and every device containing digital evidence. It is required to be done in a manner that proper balance is struck between indiscriminate acquisition/ seizure of huge data which will make task of identification of relevant evidence tougher and at the same time ensuring acquisition of data from device wherever there is a possibility of locating relevant evidence.

2.10.6 There are 4 basic differences between premises searched and computer search i.e., the environment, copying procedure, the storage mechanism and the retrieval mechanism, which authorized officer should understand. This will help him make an appropriate decision in identifying the relevant data which needs to be acquired/ seized.

A. The Environment: Premises vs. Hard Drives

Premises offer predictable, specific and discrete physical regions for physical searches. A search team can enter through a door or window and can walk from room to room. They can search individual rooms by observing their contents, opening drawers and other containers, and rummaging them.

Computer storage devices are different. They come in many forms, including hard drives, floppy disks, thumb drives, Zip disks etc.. All these devices perform the same basic function: they store zeros and ones that a computer can convert into letters, numbers and symbols. Every letter, number or symbol is understood by the computer as a string of eight zeros and ones. For example, the upper-case letter “M” is stored by a computer “01001101,” and the number “6” as “00110110.” Each string is known as a “byte” of information and the number of bytes represents the total storage available on a storage device. For example, a forty gigabyte hard drive can store roughly forty billion bytes, or about 320 billion zeroes and ones

While houses are divided into rooms, computers are more like virtual warehouses. When a user seeks a particular file, the operating system must be able to find the file and retrieve it quickly. To do this, operating systems divide all of the space on the hard drive into discrete sub part know as “clusters” or “allocation unit” Different operating systems use clusters of different sizes; typical cluster sizes might be four kilobytes or thirty-two kilobytes. A cluster is like a filing cabinet of a particular size placed in a storage warehouse. Just as a filing cabinet might store particular items in a particular place in the warehouse, the operating system might use a cluster to store a particular computer file in a particular place on the hard drive. The operating system keeps a list of where the different files are located on the hard drive; this list is known as the File Allocation Table or Master File Table (MFT), depending on the operating system. When a user tells his computer to access a particular file, the computer consults that master list and then sends the magnetic / optical heads over to the physical location of the correct cluster.

The search of data on digital device thus can be made by examining data lying on it, which is a very time-consuming job. Thus, a preliminary search at the premises is generally followed by a detailed search subsequently, while in the case of search of premises, the search has to be finally concluded before the search party leaves the premises. The decision of assessing officer to acquire/seize data from various devices should take into account this flexibility.

B. The Copying Process:

When a search team searches a premises, the premises and assets it searches typically belong to the target of the investigation. Once again, computers are different. To ensure the evidentiary integrity of the original evidence, the computer forensics process always being with the creation of a perfect ” bistream”

A bitstream copy is different from the copy users normally make when copying individual files from one computer to another. A normal copy duplicates only the identified file, but the bistream copy duplicates every bit and byte on the “target” drive including all files, the “slack space”, master file table and metadata in exactly same order as they appear on the original. Thus, the copying procedure ensures that all relevant as well as irrelevant information stored on computer are acquired. Thus, identification of relevant devices is the key once a device containing relevant data is identified, copy of entire device is generally required to be made.

C. The Storage Mechanism: The Premises vs. Computer Storage

The third important difference between computers and premises concerns how much they can store and how much control people have over what they contain. Premises can store anything including computers of course, but their size tends to limit the amount of evidence they can contain. A room can only store only a limited number of packages and a premises can only contain limited number of rooms. Further, individuals tend to have considerable control over what is inside their premises. They can destroy evidence and usually know if it has been destroyed. Computers can only store data, but the amount of data is staggering.

While computers are compact at a physical level, every computer is akin to a vast warehouse of information. Computers are also remarkable for storing tremendous amount of information that most users do not know about and cannot control. For example, forensic analysts can often recover deleted files from a hard drive.

Computer operating systems and programs also generate and store a wealth of information about how the computer and its contents have been used. As more programs are used, those information, called ‘metadata‘, become broader and more comprehensive. For example, the popular Windows operating system generates a great deal of important metadata about exactly how and when a computer has been used.

Common word processing programs such as Word Perfect and Micro-soft Word generate temporary files that permit analysts to reconstruct the development of a file. Word processing documents can also store data about who created the file, as well as the history of the file. Similarly, browsers used to surf the World Wide Web (www) can store can store a great deal of detailed information about the user’s interests, habits, identity, and online whereabouts, which often the user also may not be aware of. Browsers are typically programmed to automatically retain information about the websites which the users have visited in recent weeks. Understanding the above, will help authorized officer to take more appropriate decision in identification of crucial devices from where data is to be acquired.

Importantly, the person in control of physical premises knows and has control over what has been stored in the premises. But he has a very limited control and knowledge about what is stored in the computer.

D. The Retrieval Mechanism: Physical vs. Logical

Conducting physical search of a premise generally requires physical search of all processes where recovery of the evidence for which search operation is mounted is possible. Search team look from room to room for the evidence sought in the warrant. If the evidence sought is large, the search team will plan its search accordingly: If they are looking for a stolen car, for example, they can‘t look inside a suitcase to find it. After the search team has searched the space for the items sought, the search is done, and the search team will leave.

Computer searches tend to require fewer people but more time. Analysis of a computer hard drive takes as much time as the analyst has to give it.

In contrast to physical searches, digital evidence searches generally occur at both a “logical” or “virtual” level and a “physical” level. The distinction between physical searches and logical searches is fundamental in computer forensics: while a logical search is based on the file systems found on the hard drive as presented by the operating system, a physical search identifies and recovers data across the entire physical drive without regard to the file system.

The differences between computer searches and traditional physical searches raise difficult questions about the rules that should govern computer searches and seizures. Generally it is more difficult to plan a computer search ex ante; the search procedures are more flexible than procedures for physical searches, and they are more of an art than a science.

2.12 Other important aspects of handling digital evidence

Just like in the case of a conventional documentary evidence, merely gathering electronic evidence is not sufficient. It needs to be analyzed in the context of the facts of the case and relevant information needs to be extracted. Efforts have been made to corroborate the contents therein with material and oral evidences to reach to a conclusion useful for, or relevant to the proceedings under the Act. Unlike documentary evidence, extracting information is a tricky job in the case of a digital evidence as it can be password protected, encrypted or hidden. Further data may be properly visible only with the help of specific operating system or software. Thus, some other important aspects need careful consideration while handling digital evidence, which are briefly discussed here:

2.12.1 Preliminary and detailed statements of the persons in control of computers/ electronic devices (including system administrator) would be very important. In preliminary statements information regarding the hardware, operating systems, software and topography of the computers, various users and their roles and passwords should be extracted.

2.12.2 The surrounding of the computers can sometimes prove very crucial. The search party should carefully look for:

i. Computer Printouts in room, on table, in drawers, in dustbins, etc.

ii. Passwords: On casing of computers, on tabletops, stickers, walls etc.

iii. Manuals and reference books pertaining to computers

iv. Physical Evidence such as documents, visiting cards, scribbling pads etc. On examination, relevant physical evidence should be seized.

2.12.3 Under Income tax Act, Section 132(1) (iib) has been specifically brought in to remove difficulties in handling digital evidences found during the course of the search. This section requires any person who is found to be in possession or control of any books of account or other documents maintained in the form of electronic record, to afford the authorized officer the necessary facility to inspect such books of account or other documents. Thus, such person is obliged under law to provide all facilities to access the data inside, which include disclosing the passwords, details of OS and software and their functioning besides the physical access.

Further, provisions of section 275B make failure to comply with provisions of section 132(1)(iib) a punishable offence by imprisonment up to two years.

Thus, if the authorized officer is unable to open or have access to files containing books of account or documents maintained on electronic media, the person incharge of the premises shall be asked to make available such computer codes or passwords in statement under oath, bringing such provisions to his notice. The denial or deliberate non-furnishing of such passwords / secret codes must be brought out in the statement recorded by the authorized officer. The evidence regarding the presence of Panchas, and their statements as witnesses, recorded contemporaneously, would be important to establish the commission of offence under this section. Further, there are a few provisions under IPC also, which may be invoked, in case of non-cooperation in the form of hiding information or furnishing misleading information in sworn statements.

2.12.4 It may be mentioned that if a person who is in control / possession of books of account / documents in electronic media, destroys the same to prevent their access by the authorized officer, it would constitute an offence u/s 204 of IPC.

2.13 Seizure of original device vs. Acquisition of data

a) In Income-tax Law, the “seizure” of documents etc., in the form of digital storage device means seizure of original device. Thus, for the crucial digital evidence, wherever possible seizure of original device is recommended.

b) However one should understand that all computer data is a copy. Computer hard drives work by generating copies; accessing a file on a hard drive actually generates a copy of the file to be sent to the computer’s central processor. more broadly, computers work by copying and recopying information from one section of the machine to another. From a technical perspective, it usually makes no sense to speak of having an “original” set of data. Generating and analyzing bit-stream copies are routine parts of the forensics process, and no court has ever considered copies as different from originals. In terms of evidentiary value, the copy/clone made with bit flow technology using proper forensic tools is as good as original and is recognized as such in the Information Technology Act 2000 read with Indian Evidence Act. Therefore, seizure of original device may be done selectively. But it should be kept in mind that such acquisition of data by making copy/clone may not amount to seizure of data as per the present provisions of Income Tax Act 1961 e.g section 153C of I T Act 1961.

Chapter 3

Introduction to Digital Evidence Investigation &

International Best Practices

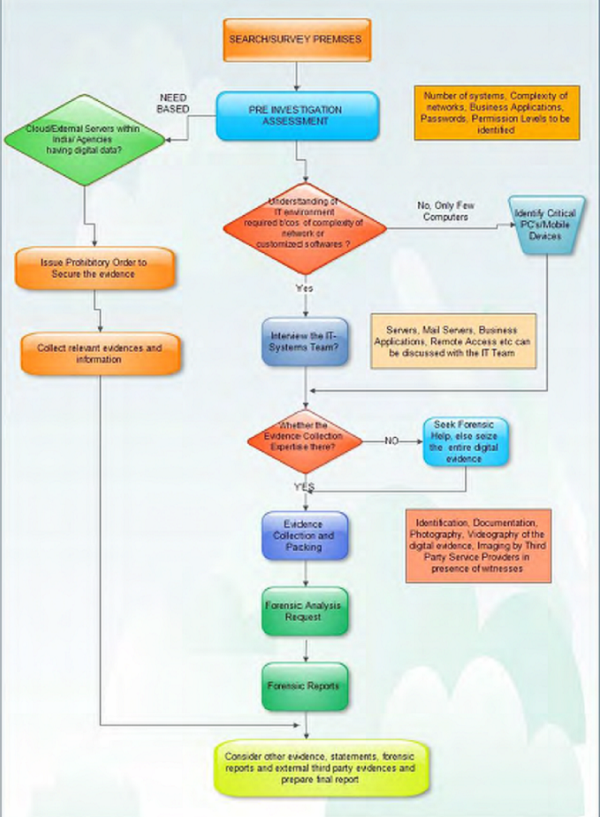

Digital Evidence is highly fragile and can be tampered easily and precautions are required during the search, collection, preservation, transportation and examination of evidence. The flow chart for Digital Evidence is given below:

The sequences of Digital Evidence Investigation are as follows:

1. Pre Investigation Assessment which involves identification of key digital evidences and securing the same so that any data is not lost

2. Collection of Evidence

a. Procedure for gathering evidences from Switched off systems

b. Procedure for gathering evidence from live systems

3. Forensic Duplication

4. Labelling and Documenting of the evidence,

5. Packaging and transportation of the evidence

6. Analysis of Forensic Data by retrieval of deleted files and present files

7. Publication of the Forensic Report by linking all the reports and circumstantial evidences.

3.2 Some International Best Practices

Some important international best practices are-

♦ Reading/examining the data storage device under examination (subject device) through ‗write blockers‘ which prevents any kind of writing on the subject device during the process of viewing the data on it;

♦ Making clones of the subject device (as distinct from copies) so that entire data on the subject device including hidden files, deleted data, slack space, formatted or deleted partition can be obtained, and using such clones for study/ examination while keeping the subject device undisturbed and safe. The cloning process produces a true image of the data storage device including the deleted data and hidden sectors.

♦ Authenticating the cloned disks by taking hash value of the subject device and the clones.

♦ Maintaining log of activities carried on the cloned disk.

3.3 Use of Cyber Forensic in Income-tax Department

♦ Acquisition /Acquiring: forensically acquiring digital data found during the course of a search and seizure or survey operation.

♦ Analysis & Documentation: analysing the digital data for uncovering hidden, password protected data, and deleted data

♦ Archival: safe archival of cloned disks for reference and future production

♦ Once all digital data have been recovered, the work of examining them for identifying violations of provisions of the Income-tax Act can be carried out.

Chapter 4

Important Related Terms

4.1 Definitions:

♦ Hash value: A hash value is a unique and compact numerical representation of a piece of data. It is computationally improbable to find two distinct inputs that hash to the same value (or “collide”). In short we can say Hashing is the transformation of a string of characters into a usually shorter fixed-length value or key that represents the original string.

♦ Wiper:

Wiper is a software or hardware tool which will wipe the complete Hard Disk Drive by replacing either 0 or 1 or a user defined value to its each sector. After wiping, the Hard Disk Drive will not be having data in any form on it.

♦ Write blocker:

It is a hardware tool which, when used with any data storage device, will not allow to write on or modify the data in the storage device under examination.

♦ FRED:

It is a complete computer machine with additional in built write blocker and some drive bays, which can be used for both acquisition and analysis purpose.

♦ FREDDIE:

It is almost same as FRED but is a portable one which can be taken to the premises.

♦ Cyber Check: It is software tool developed by CDAC, Trivandrum, which is used for both acquisition and analysis purpose

♦ RAID: an acronym for Redundant Array of Independent Disks. It is a technology that divides and replicate data among multiple hard disk drives. This distributes data across multiple hard disks but is seen by the computer user and operating system as one single disk. The Hard Disk Drives arrayed using RAID architecture, individually have no existence and therefore data cannot be extracted from individual hard disks.

♦ Live forensics: Live forensic implies taking the data from system (imaging or cloning) while it‘s running

♦ Customised software: Softwares which are prepared by some vendor for a specific purpose for a company. Normally these softwares are based upon database such as oracle, MS-SQL etc.

♦ Imaging: Disk Imaging is the process of copying content of source digital media on destination digital media sector by sector, bit by bit, in the image file format such as *.EØ or *.PØ depending on the software used.

♦ Cloning: Disk cloning is same process as that of imaging. These two terms are interchangeably used. The only difference is that in the case of disk cloning, one can replace the source disk with the destination disk and the computer system will boot and work because cloning is done either for a whole disk or a partition in the same disk geometry.

♦ Logical Partition & Physical Partition: In the computer two types of partitions are present-

» Physical Partition ± A number of hard drives physically present in a computer system.

» Logical Partition ± A number of partitions on a given hard drive. Normally shown in a computer as, C, D drives and so on.

♦ BIOS: Basic I/O System is used to store the information required for starting the system.

♦ Logical bombs: A logical bombs is usually a hostile piece of computer code that wipes out files or does damage to evidence. The hostile code may destroy critical data with great precision or the logical bomb could be an actual bomb that would physically damage the computer and it‘s disks.

♦ CMOS: CMOS battery is present on mother board which is used to store time and some kind of password.

4.2 Types of Hard Disk Drive and their connectors:

♦ SATA

♦ IDE

♦ SCSI

This type of SCSI hard disk is normally used.

Ports of other different type of SCSI hard drive.

♦ SAS

There also may be many other kind of SAS HARD DISK DRIVEs but normally used type is shown in figure:

4.3 Types of digital Storage:

- Hard Disk Drive

- Flash Drive

- CD/DVD

- External Hard Disk Drive

- Floppy Drive

- SIM Card

- Memory card

- Tape Drives

- I-POD/ MP3 players

4.4 Abbreviations:

♦ RAM: – Random Access Memory

♦ Types of HARD DISK DRIVE:-

i. SATA: Serial Advance Technology Attachment.

ii. IDE: Integrated Development Environment.

iii. SCSI: Small Computer System Interface

iv. SAS: Serial Attached SCSI

♦ BIOS: Basic Input Output System

♦ CMOS: Complementary Metal Oxide Semiconductor

♦ Storage Units: GB (Gigabytes), TB (Terabytes).

♦ Forensic tools:-

i. FRED: Forensic Recovery of Evidence Device

ii. FREDDIE: Forensic Recovery of Evidence Device Diminutive Interrogation Equipment.

Chapter 5

Pre Investigation Assessment of Digital Evidences

5.1- General Principles

When dealing with digital evidence, the following general forensic and procedural principles should be followed:

- Actions should be taken to secure and collect digital evidence in such a way that it does not affect the integrity of the evidence.

- Persons conducting an examination of digital evidence should be trained for such purpose.

- Activity relating to the seizure, examination, storage, or transfer of digital evidence should be documented, preserved, and available for review.

The first step in Digital Evidence Analysis is the Pre-Investigation Assessment of what Digital Evidences needs to be acquired, imaged etc. The officer in charge may take clue from certain guidelines discussed below when deciding the potential digital evidences which needs to be acquired or imaged.

5.2- Preliminary review of the Premises

Typically premises can be broadly dealt under,

1. Residence with one or few computers, hand held devices

2. Office with few computers

3. Companies /Organizations with vast and complicated network of systems

At the premises, the investigating officer should carefully survey the premises, observe and assess the situation and decide on the steps for proceeding further. The digital evidence is highly fragile and it will be available in a number of devices, locations and in various formats. Hence it is important to do a preliminary review of the premises to identify the key digital devices in the premises. For example, in an organization which has multiple branches, it is not necessary to take digital evidence at all branches since all the data of the branches will be in the central database of the company at the headquarters. So the key digital device is the servers on which this data is stored in the headquarters.

5.3- Evaluating the Premises

- The officer in charge should secure the premises and none should be allowed to access any computer without the permission of the officer in charge. The officer in charge may take note of every individual physically present at the premises and their role at the time of securing the premises. In case of big organizations, ask who is the system administrator

- Disable the internet connection: Internet connection should be immediately turned off to avoid remote internet access to prevent changes in data through internet.

How to disable internet:

i. Switch off modem/routers.

ii. If cannot find modem/routers then either switch off the LAN or unplug the LAN cable.

- Disable the LAN: If possible, disable LAN from the server. If there is no work to do through the network like taking printout or any other kind of data analysis, the LAN should be disabled to avoid unauthenticated access to data.

How to Disable LAN:

i. Switch off the LAN switch.

ii. or Go to Control Panel »Network and Sharing Center » Local Area Network »Disable.

iii. If you locate the switch or cannot find setting of LAN in the system final option can be to unplug the LAN cable from the server.

- Disable CCTV : Ask about the CCTV server location. Usually security guard should know.

A typical CCTV back panel looks as follows:

Disconnect all video and audio inputs as soon as possible if you still want access to the videos. If not directly disconnect the power to turn it completely off.

- Identify Important PC‟s:

Find out if there is an organizational chart for all the senior management. If none, then ask around to create one yourself. Ask the staff to identify their offices/desks. Note all the electronic devices/computers and storage media for each person. Attach paper stick-it notes to each such device noting the person name and make/model of the device.

E.g. ‘John Doe – Laptop Dell Vostro’.

Let the officer in command know that you have identified the computers for important personnel at the company. Wait for their instructions as to what to do with each; backup/imaging etc. If the main accounting server has not been identified yet, then try to find it by asking around. Wait for officer instruction on what to do with the accounting machine.

Ask if there are any cash counting machines on premises. Typically it would be next to a computer where data entry takes place. In case cash counting machine is present, and if officer has already verified a particular person who is responsible for data entry for cash transactions, then note down location of the computer where they do data entry on and wait for further instructions from the officer. Identify important persons who deal with sales, purchase, banking etc. Tag their machines with sticky notes to indicate what activity happens on that particular PC.

Identify the systems which have data related to the case under investigation or which belong to important persons such as computers of accountants, managers, directors or owner(s) where important digital data including deleted files can be found relevant to the case which may be required to be cloned. This step will simplify work and will help to take important information out of huge amount of data. This is a manual process and for this, the assessee has to be asked about the user for each of the computer systems available at the premises. Some standard interviews can be conducted with the key IT personnel, the details of which are given at the end of this chapter.

- Identify the location of servers: Identify different servers along with their physical location and find out which servers are related to the case under investigation such as File server, Database Servers, Mail Servers and Accounting Servers etc.

In most cases there will other machines around where CCTV server is placed. Typically this will be the server room. Ask to identify the function of each machine. There is high probability of main storage server and accounting server being in the same server room. Inform the officer in command that you have located their main accounting server and storage server. Wait for their instructions as to what to do with each; backup/imaging etc. A typical server room will contain rack mounted servers with networking hardware. It can look something like following:

- Collect Passwords: There may be many kinds of password in computer to get access to that computer or to the files such as:

- BIOS password: The first thing to do is to ask the assessee to provide password. If he doesn’t, we can remove the BIOS password by removing the CMOS battery for half an hour, again put it in the system and restart the system. The BIOS password will be removed.

- Operating System password: Ask the assessee for the password. If he does not provide the password, then there are some password crackers for normal use operating system such as Windows XP, and Windows Vista.

- Password for MS office files: Ask the assessee. If he does not provide the same, then there are some password cracker tools such as Rainbow Table.

- Password for Tally files and any customized software: In this case, it is somewhat difficult to crack. We may ask the assessee for the passwords. But with some efforts, Tally file passwords can also be cracked.

- Password for Gmail, Hotmail etc: If web based email (Gmail, Yahoo, Hotmail, other hosted email service ) then get username and password for all important accounts.

- Password for Online Accounting Software: If there are any web based accounting systems which are present then relevant username and passwords

In case of passwords, the best option is to ask the assessee to provide password. The assessee is bound by law to provide such password. It is only when the assessee has not provided passwords that we use crackers for the same.

- Securing Mail Boxes: Acquire the user id and password of email account of assessee and some important persons of the business concern, if there is any, and change the password immediately to secure the mail box. The changed passwords should be noted down at a secured place for further analysis of emails.

- Identify Volatile Data if any: Volatile data refers to data on a live system that is lost after a computer is powered down or due to the passage of time. Volatile data may be lost as a result of other actions performed on the system. So officer in charge should consider acquiring volatile data ( if crucial for investigation ) on priority over non-volatile data

- Identify Server Hardware Architecture: Identify the hardware architecture, whether it is a normal server or a RAID server. At the time of acquisition, this should be kept in mind because acquisition process will vary depending upon the architecture of the server.

- Identify Customized Software Used: Identify the customized \TftwareD\ which are being used by the assessee, and collect information such as vendor of the \TftwareD\, database used by the software, their file format and passwords. If the software are operated with smart card/dongle keys, (small hardware token keys generally validated through the USB port); then one must take possession of the smart card/dongle keys as in the absence of such keys software will not function.

- Identify Cloud Data: Cloud data is any data which is stored on a remote server. The types of data typically stored on remote servers can be email, ERP application data or company intranet. Cloud hosting can be of following types:

- Physically hosted server (also knownas Colocation hosting) : Colocation hosting is when server is stored off-premises in a dedicated secure data center owned by a large service provider like Tata Communications, NetMagic, BalaSai etc. Usually this should be in the same city or a nearby metro location. Sometimes this can also be located in another state of country. Such types of installations are typically managed by third party IT consultants. Getting the name of such consultant should make extract data from such servers easy. The data backup or image acquisition is better done on premises only. This would require proper security clearance from data center staff on premises.

- Virtually hosted server : Typically virtually hosted servers have no dedicated physical hardware assigned to it. Examples are Amazon EC2, Digital Ocean, Linode etc. In order to extract data from such remote servers, administrator level access on the Virtual machine is required. The data backup or image acquisition has to be run remotely and it will take a very long time for such acquisition to complete because of the bandwidth issues.

- Cloud hosted data : There are a number of online data storage providers like Google, Yahoo, Microsoft, Dropbox, Box.net etc. Extracting data from such providers without username and password will involve lengthy legal procedures. Even if username and password is available, bandwidth limitations will seriously hamper backup process.

- Artifacts of cloud data: User browser history, email client settings, cloud sync applications like dropbox etc. would giveaway whether the user is utilizing cloud data or not.

- Identify all Key Mobile Devices: All Key Persons Mobile Devices should be taken in to control and ensure that there is no scope for deletion of data in the Mobile Devices. The Mobile Devices if no volatile data exists, should be kept in switched off mode. Identify any cloud data which is present or not. Login into cloud and change the password so that no one else can login into the system from outside to destroy the data in cloud.

- Identifying Encrypted Volume of Data: There are some cases where Assesses store its important data in encrypted volume using application like TrueCrypt, Bitlocker etc. Using a program call TCHunt we can detect an encrypted Volume. To use TCHunt open command prompt and change directory to TCHunt location.

run the command

>TChunt.exe –d Drive_Letter: 2>nul

e.g. >TCHunt.exe –d C: 2>nul

similarly run the same command for other logical drives.

If Tool detects any Encrypted Volume it will show you the actual path for that volume.

- Identifying history of USB media connections

In many cases we have found a printed piece of paper of interest but no corresponding document. Even after searching all the PCs on premise no trace of such document can be found. One the possible explanation of such a puzzling situation may be that the document it-self is stored on portable media such as USB drive. In such case, it is important to ascertain whether USB devices were connected and how recently on all on premise PCs. A tool called USBDeview.exe help in such investigation.

Double Click on USBDeview.exe it will show you the USB device history.

If the USB connection log shows a regular pattern of USB device connection then let the Authorised officer know your findings so that he/she may include that in their investigation.

- If the systems are Off, they should not be turned ON for the inspection. If systems are on, it is advised to leave them ON

- If systems are ON at the scene of offence, Officer in Charge should take appropriate steps to photograph it, plan for the seizure of the evidences at the earliest and document it. Officer in Charge should ensure that perishable evidences ( volatile data) are appropriately recovered without any loss.

5.4- Model Questionnaire/Checklist for Pre – Investigation Assessment at Corporate Organization with multiple computers or vast network of computers

1. Who are the key members of the Information Technology Department?

2. What applications and software, databases are being used by the Organization?

3. Who are the developers of the applications that are used?

4. Who provides the support and maintenance for the application?

5. Where are the actual servers located?

6. Who has the administrative and super user privileges?

7. What is the backup policy of the organization?

8. What kind of backups is taken and how long they are retained?

9. What levels of access are given to employees? Are they allowed to carry thumb drives, CDs, or other devices?

10. Has anybody access to remote login or VPN to any of the servers?

11. Are the employees permitted to use the official laptops for accessing internets?

12. Is there an email server present if so where is it located?

13. From where is the website hosted? Does the company own any cloud space where data is stored?

14. Whether the company is giving company owned mobile numbers to its employees? Obtain the list of mobile numbers used by the key employees

5.5- Model Questionnaire/Checklist for Pre – Investigation Assessment at Offices/Home with few PC‟s

1. Identify the number of PC‘s/Computer System

2. Identify the type of connections ( Wi-Fi/Ethernet)

3. How many computer systems are used for internet connection?

4. Who are the persons with access to system?

5.Obtain the details about the removable storage media (including external hard disk) used/owned by the user.

6. Obtain details about the network topology and architecture(client-server) if any

7. Obtain the details of all passwords of emails

8. Secure all mobile phones and the details of the persons in whose name the SIM is registered.

The above formats for pre-investigation assessment will help the investigating officer to understand the situation in detail and decide on the kind of technical support to be requisitioned, to proceed with the acquisition of evidences.

Chapter 6

Forensic Collection of Digital Evidences

6.1 -Identifying/Seizing of the devices needs to be forensically imaged for analysis