Page Contents

Direct Tax Budget 2026 Bulletin analyzing the key direct tax proposals as stated in the Budget for the Income Tax Act, 1961

The Union Budget 2026–27 outlines wide-ranging income-tax reforms aimed at easing compliance, reducing litigation, and decriminalising minor offences while sustaining growth amid global uncertainty. Key proposals include clarifying transfer pricing timelines retrospectively, extending return-filing deadlines for non-audit business taxpayers, allowing longer windows for revised and updated returns (with graded fees), and permitting updated returns even after reassessment notices with higher additional tax to curb disputes. Reassessment procedures are clarified to separate pre-notice enquiries from faceless assessments, while technical defects like DIN quoting errors will no longer invalidate assessments. Penalty processes are streamlined by integrating penalties into assessment orders and granting immunity where additional tax is paid on updated returns. A major thrust is decriminalisation—replacing rigorous imprisonment with simple imprisonment or fines, especially for low-value defaults—alongside graded punishments linked to tax amounts. Rate structures largely remain unchanged, but tax on unexplained income is sharply reduced, MAT is rationalised, and presumptive taxation exclusions are widened for non-residents.

UNION BUDGET 2026-27

Key Direct Tax Proposals

With reference to amendments made in Income-tax Act, 1961 (Part 1)

FOREWORD

The Indian Budget for the fiscal year 2025-26 has been set amidst geo-political turmoil, USA unsettling international norms of business and of international relations. Most countries have become inward looking and the concept of the world being a global village is slowly disintegrating, which will have challenges for India as we move forward, probably to a new world order, where each nation will be for itself.

The Indian economy grew by 7.3% in 2025-26 and is expected to grow by 6.8% to 7.2% in 202627. The fiscal deficit at 4.3% of GDP in 2025-26 and is expected to be 4.3% of GDP in 2026-27, seems to be in control, however, one would need to factor in the borrowings which are not included in the budget, like the borrowing of PSUs, etc.

The budget aims to rev up the economy by increasing the contribution of the industrial sector to GDP, giving a boost to the services sector and trying to increase the productivity of the agriculture sector. The budget intends to sustain economic growth, generate employment, and ensure inclusive development. However, when one sees the details of the budget, a different picture tends to emerge, wherein the rural population, the agricultural sector, the MSME and SME sectors still lag in their growth and in their contribution to the economy.

Agriculture and Rural Development

Agriculture remains the backbone of the Indian economy, employing nearly 45% of the workforce and contributing only around 17.5% of the GDP. Agriculture and allied activities continue to play a stabilising role in India’s growth cycle by supporting rural demand and providing income security to a large section of the population. The sector is expected to grow by 3.1 percent and has sustained the growth in India’s GDP.

Industry and Manufacturing

Industry and manufacturing are pivotal in driving India’s economic growth, however its share in India’s GDP at approximately 27% has largely remained stagnant as compared to the previous years. It also employs around only 25 percent of the workforce.

The stress should be on reviving growth in the MSME and SME sectors as that will also boost employment in the semi urban and rural areas.

Services Sector

The services sector is the largest contributor to the Indian economy, accounting for nearly 55% of the GDP and employing around 30% of the workforce. The budget for 2026-27 highlights the importance of digital transformation, stress on developing emerging technologies such as AI, tourism, and increasing the spread and growth of higher education and strengthening financial services.

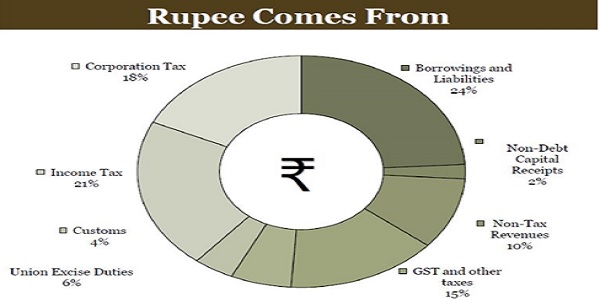

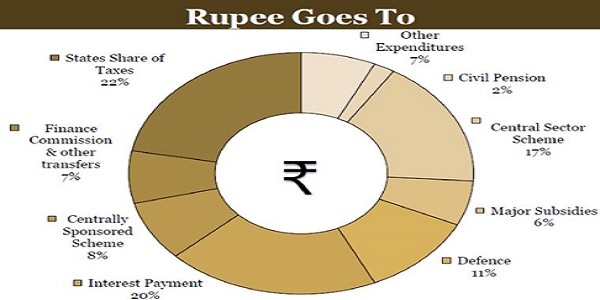

Contribution to Direct Taxes

The fiscal landscape clearly demonstrates that the taxation system of India seems to be lopsided as Personal income taxes continued to contribute a higher percentage of total direct tax revenue at INR 13,12,000 crores and Corporate taxes contribute only INR 11,09,000 cores as per revised estimates for 2025-26, thus, the individuals pay more taxes than the Corporates. It needs to be seen whether this is the best way forward or share of Corporate tax revenue should be increased as they get the bulk of the advantage of the fiscal measures of the government and the burden of taxation should be reduced for the individuals, as they bear the brunt of both direct and indirect tax. This could give fillip to consumption and help boost the economy.

The chart below depicts the revenue categorization:

India faces a lot of challenges in the external environment and with fast paced disruptive technologies displacing labour and existing supply chains. Thus, economic policies that help in increasing agricultural productivity, modernising agriculture with best cultural practices, reviving MSME and the SME sectors, increasing rural welfare measures and reducing the burden of taxes and compliances on the individuals, will be the key in generating employment, and having sustainable and equitable development

KEY INCOME-TAX PROPOSALS

TRANSFER PRICING

| Time-limit for passing of order by TPO

[Section 92CA]

|

– Section 92CA(3A) states that the TPO is required to pass an order before 60 days prior to the date on which period of limitation under section 153 (regular assessment) or, in section 153B (search assessment) for making the order of assessment or reassessment or recomputation or fresh assessment, as the case may be, expires.

– The section is now amended by inserting sub-section (3AA) to make it abundantly clear that the date of limitation of the assessment will be included in the computation of sixty days. For example, if the date of limitation of assessment order is 31st March 2026, the time-limit for passing order by TPO would be 30th January of that year (and not 29th January as was being interpreted by Court judgments earlier. The above amendment will take effect retrospectively from 1st June, 2007. |

| VTPA Comment | – The amendment by the legislature is perhaps to nullify the effect of Court judgments like Pfizer cases, wherein the Courts were holding that the last day of the limitation period was not to be considered in computing the period of 60 days prior to the date on which period of limitation specified in section 153 or section 153B expires.

– The Hon’ble Madras High Court in the case of Pfizer Healthcare India Pvt. LTD [TS-199-HC-2022(MAD)-TP], observed as under: “… The submission of the revenue is to the effect that limitation expires only on 12 am of 01.01.2020. However, this would mean that an order of assessment can be passed at 12 am on 01.01.2020, whereas, in my view, such an order would be held to be barred by limitation as proceedings for assessment should be completed before 11.59.59 of 31.12.2019. The period of 21 months therefore, expires on 31.12.2019 that must stand excluded since Section 92CA(3A) states’ before 60 days prior to the date on which the period of limitation referred to Section 153 expires’. Excluding 31.12.2019, the period of 60 days would expire on 01.11.2019 and the transfer pricing orders thus ought to have been passed on 31.10.2019 or any date prior thereto. Incidentally, the Board, in the Central Action Plan also indicates the date by which the Transfer Pricing orders are to be passed as 31.10.2019. The impugned orders are thus, held to be barred by limitation.” – The important point for consideration is whether the proposed amendment with retrospective effect can cure the defect of not adhering to the timelines as originally legislated. This amendment may therefore lead to litigation as to the constitutional validity of the retrospective nature of the amendment. |

FILING OF RETURNS

| Rationalisation of income tax return filing deadlines

[Section 139] |

– At present assessees (not being a company, or who are required to furnish a report under section 92E – Accountant’s Report on Transfer Pricing) and partners of firms or individuals who are having income from business or profession but are not required to get their accounts audited under this Act or any other law in force, they are required to file their return by 31st July in the assessment year.

– These small taxpayers and those partners of such firms and spouses of such partners, if spouses are governed by the Portuguese Civil Code in Goa, still require time to prepare their accounts and complete required compliances, it is proposed to give them an additional one month for filing the return under section 139(1). – Accordingly, the due dates for filing income tax returns for the above assessees who file their return in ITR-3 only is extended to 31st August. – However, for individuals filing ITR-1 and ITR-2, the due date for filing the return will continue to be 31st July. – To give effect to this amendment, the existing Explanation 2 to section 139(1) is being substituted by a new Explanation 2 along with a Table showing the due date for filing of the return. – This amendment will apply for Assessment Year 2026-27. |

| VTPA Comment | – The assessees having income from profits and gains of business or profession whose accounts are not required to be audited under this Act or any other law for the time being in force, still require time to complete their books of account for different compliances.

– Hence, it is proposed to give one additional month’s time to such assessees to prepare their accounts and file their return by 31st August to make compliance easier and reduce taxpayer grievances. |

–

| Extending the period of filing revised return

[Section 139(5) r.w. newly inserted Section 234-I] |

– Section 139 of the Act relates to filing of income tax returns and includes original, belated, revised, and updated returns. Under section 139(5), a taxpayer who has already filed an original or belated return can file a revised return if any mistake or omission is found in the earlier return.

– Earlier, a revised return had to be filed within nine months from the end of the relevant financial year or before completion of assessment, whichever was earlier. – It is now proposed to amend section 139(5) to extend the time limit for filing a revised return from nine months to twelve months from the end of the relevant financial year. – In addition, a fee is proposed to be charged under section 234-I for revised returns filed after nine months from the end of the assessment year. – These changes will apply from 1st March 2026 and will be effective for the assessment year 2026–27. |

| Fee for furnishing revised return of income

New section [Section 234-I] |

Without prejudice to the provisions of this Act, where, –

any person furnishes a return of income under sub-section (5) of section 139, beyond nine months but before twelve months from the end of the relevant assessment year, he shall pay by way of a fee (a) a sum of one thousand rupees, if the total income of such person does not exceed five lakh rupees. (b) a sum of five thousand rupees, in any other case.”. |

–

| VTPA Comment | – This is a welcome provision for the assessees to get additional three months’ time to file the revised return on payment of fees under section 234-I.

– The combined effect of this amendment and s. 234F as it stands, is that if the assessee fails to furnish a return of income within the time prescribed under section 139(1) i.e., original return by due date, then he has an option to file a belated return under section 139(4) by 31st December on payment of fee of Rs. 1000/ 5000 as the case may be, under 234F. – Further, if he wishes to file a revised return under section 139(5), he gets an additional time of three months till 31st of March of the assessment year, but again on payment of fees of Rs. 1000/ 5000 as the case may be, under section 234I. – The intention of the Department is to provide an additional opportunity to the assessees on payment of a fixed fee structure for compounding delays and minor non-compliances, instead of levying interest which is calculated on a month-to-month basis. |

| Scope of filing of updated return in the case of reduction of losses

[Section 139(8A)] |

– Sub-section (8A) of section 139 provides for updated return of income. It allows a taxpayer, whether or not a return was furnished earlier, to file an updated return within forty-eight months from the end of the financial year succeeding the relevant tax year.

– At present, updated return cannot be filed if it is a return of loss. – It is now proposed to amend the sixth proviso under sub-section (8A) to provide for filing updated return which has the effect of reducing the loss, where taxpayer reduces the amount of loss in comparison to the amount of loss claimed in the return of loss furnished within the due date specified under sub-section (1). – The amendment in the Income-tax Act, 1961 shall come into force from 1st March, 2026. |

| VTPA Comment | – The provision of updated return is meant to promote voluntary compliance on the part of the taxpayer to offer the income for taxation. However, till now it did not allow the assessee who has furnished a return of loss to update his return. Now, after the proposed amendment he cannot still increase his loss in the return already furnished (by the due date) but can reduce his loss on coming to know if there is a discrepancy.

– Since it is a return of loss, no additional tax computation would be leviable under section 140B of the Act which otherwise would be applicable if the return of loss is updated into a return of income. |

ASSESSMENTS

| Allowing the filing of updated return after issuance of notice of reassessment under section 148

[Section 139(8A)]

|

– This is a proposed amendment that updated return under sub-section (8A) of section 139 may be furnished by a person for the relevant assessment year in pursuance of a notice under section 148 within such period as specified in the said notice and in such case, the assessee is precluded from filing return in pursuance of the said notice in any other manner.

– Section 140B(3) of the Act provides that additional income-tax amounting to 25%, 50%, 60% and 70% of the aggregate of tax and interest payable, shall be paid along with original tax and interest payable, for filing the updated return in first, second, third and fourth year, respectively from the end of the financial year succeeding the relevant tax year. – It is further proposed to insert sub-section (3A) in section 140B of the Act so as to prescribe that where an updated return is filed in pursuance of a notice issued under section 148 within the period specified in the said notice, the additional income-tax payable under section 140B(3) shall be increased by a further sum of 10 % of the aggregate of tax and interest payable on account of furnishing the updated return. – The amendment in the Income-tax Act, 1961 shall come into force from 1st March, 2026. |

| VTPA Comment | – This proposed amendment would reduce litigation arising out of impugned assessment and penalty notices under section 148 as the assessee can now voluntarily deposit the additional tax on the updated return under section 140B. |

–

| Jurisdiction to initiate reassessment proceedings by issuing notice under section 148 and completing the preliminary steps under section 148A

[Section 148 and Section 148A] |

– The Income-tax Act, 1961 provides a process for reassessment under section 147 in two steps. In the first step, before issuing a notice under section 148, the Assessing Officer follows the procedure laid down in section 148A. This allows the Assessing Officer to make preliminary enquiries and decide whether the case is fit for reassessment. If satisfied, the Assessing Officer issues a notice under section 148 along with a reasoned order under section 148A(d).

– Once the notice under section 148 is issued, the case is transferred to the National Faceless Assessment Centre (NaFAC) for faceless assessment under section 144B. At this stage, all communication with the taxpayer is carried out by NaFAC, and the assessment units function as Assessing Officers as empowered under section 144B. – The scheme of the Act clearly separates the pre-assessment enquiry from the actual assessment. The pre-assessment enquiry, including the decision to issue notice under section 148, is carried out only by the Assessing Officer. After the notice is issued, the reassessment proceedings are conducted in a faceless manner by NaFAC. – However, different High Courts have taken differing views on this issue, and the matter is currently pending before the Supreme Court. To remove uncertainty and reduce litigation, a clarification is proposed. – Accordingly, it is proposed to clarify by inserting a new section 147A in the Income-tax Act, 1961 that, notwithstanding any court ruling, the Assessing Officer for the purposes of sections 148 and 148A shall mean an Assessing Officer other than NaFAC or its assessment units as referred to in section 144B. – The clarification in Income-tax Act, 1961 shall come into force with retrospective effect from 1st April, 2021. |

| VTPA Comment | – The explanatory memorandum with the Finance Bill explains that it was never the intention of the legislature that NaFAC or its assessment units should be involved in the pre-assessment stage, including issuing notices under sections 148A or 148.

– Hence this clarifying amendment is to ensure litigation is minimized and certainty is achieved. |

| Dispute resolution committee

[Section 245MA]

|

In section 245MA of the Income-tax Act, in sub-section (2), the dispute resolution committee subject to such conditions as may be prescribed shall have the powers to reduce or waive any penalty imposable under this Act or grant immunity from prosecution for any offence punishable under this Act in case of a person whose disputes is resolved under this Chapter XIX-AA.

It is proposed for the words “waive any penalty imposable”, the words “waive any penalty imposed or imposable” shall be substituted and shall be deemed to have been substituted with effect from the 1st March, 2026. |

–

| Assessments not to be invalid on certain grounds

[Section 292BA] |

– A new section 292BA has been introduced in this Bill.

– “Notwithstanding anything contained in any judgment, order or decree of any court, for the removal of doubts, it is hereby clarified for the purposes of section 292B that no assessment under any of the provisions of this Act shall be invalid or shall be deemed to have been invalid on the ground of any mistake, defect or omission in respect of quoting of a computer generated Document Identification Number, if the assessment order is referenced by such number in any manner.” |

| VTPA Comments | – CBDT Circular 19/2019 required quoting a DIN on departmental communications. However, certain High Court rulings have invalidated assessments on technical grounds, such as the DIN not appearing on every page, etc. in cases where the DIN was though generated and referenced. This led to annulments of various proceedings.

– To avoid such interpretational disputes, they have inserted a clarificatory section to clarify that an assessment shall not be invalid merely due to any mistake or omission in quoting the DIN, provided the order is referenced by that DIN in any manner. Minor defects in related notices or summons will also not affect validity. Parallel amendments will be made in the 2025 Act. – The clarification in Income-tax Act, 1961 shall come into force with retrospective effect from 1st October, 2019. |

PENALTIES

| Penalty for under-reporting and misreporting of income within Assessment Order

[Section 270A] Procedure for imposing of penalty [Section 274] Tax payable against notice of Demand issued under section 156 [Section 220]

|

In section 270A

After sub-section (11), the following sub-section shall be inserted and shall be deemed to have been inserted “(11A) Where additional income-tax is paid in accordance with sub-section (3A) of section 140B (tax on updated return), the income on which such additional income-tax is paid shall not form the basis of imposition of penalty under this section.”. These provisions should be read with the amendments made to section 139 and 140B with reference to an updated return of income filed in pursuance of a notice issued under section 148, in respect of reopening proceedings under the Act. In section 274, (a) in sub-section (1), after the words “a reasonable opportunity of being heard”, the words “by way of a show cause notice to that effect” shall be inserted and shall be deemed to have been inserted. (b) after sub-section (3), the following sub-sections shall be inserted and shall be deemed to have been inserted, namely: “(4) Notwithstanding anything contained in any other provision of this Act, where any draft of the proposed order of assessment under section 144C or assessment under section 143 or reassessment under section 147 is made on or after 1April 2027 in respect of the assessment year 2026-27 or any earlier assessment year (a) the penalty under section 270A, if any, shall constitute part of such draft assessment or shall be imposed as a part of such order of assessment or reassessment, as the case may be and (b) the reference to the assessment order or the penalty order under section 270A in any of the provisions of this Act shall take reference to such order of assessment or reassessment, as the case may be. (5) Where the approval of the Joint Commissioner is taken for passing of an order of assessment or reassessment on or after the 1 April 2027, such approval shall also be deemed to be the approval for the imposition of penalty under section 270A, if any, constituting part of such order of assessment or reassessment.” In Section 220 Sub-section (1) provides amount payable in notice of demand under section 156 shall be paid within thirty days of service of the notice at the place and to the person mentioned in the notice. Sub-section 220(2) If the amount specified in the said notice of demand is not paid within the period limited under sub-section (1), the assessee shall be liable to pay simple interest at one percent for every month or part of a month commencing from the day immediately following the end of the period mentioned in sub-section (1) and ending with the day on which the amount is paid. After the third proviso to sub-section 2, the following proviso shall be inserted “Provided also that no interest shall be charged under this sub-section in respect of any demand raised on account of penalty levied under section 270A (a) up to the date of passing of the order under section 250. (b) up to the date of passing of the order under section 254, where the assessment or reassessment has been made in pursuance to directions issued by the Dispute Resolution Panel under section 144C.”. The above amendment will take effect from 1 March 2026 and will apply from AY 2026-2027. |

–

| VTPA Comments | The avowed objective of introducing the new methodology of passing a common order for both assessment and penalty for under-reporting and misreporting of income is that it will ensure avoiding multiplicity of proceedings which in turn would reduce the compliance of the taxpayers apart from providing consistency in levying of penalty.

However, the jurisprudence on levy of penalty for concealment of income, etc., and in the present case for under reporting, misreporting of income, states that such penalty only arises on the passing of an assessment order. The Hon’ble Supreme Court (SC) in the case of Varkey Chacko vs CIT in 203 ITR 885 held as under: It would therefore to be seen how this provision will get implemented in law. |

–

|

Immunity from imposition of penalty, etc. [Section 270AA] |

In section 270AA of the Income-tax Act, for sub-sections (1) to (3), the following sub-sections shall be substituted and shall be deemed to have been substituted with effect from the 1 March, 2026:

“(1) An assessee may make an application to the Assessing Officer to grant immunity from imposition or, as the case may be, waiver of penalty under section 270A and immunity from initiation of proceedings under section 276C or section 276CC, if he fulfils the following conditions, namely: (a) the tax and interest payable as per the order of assessment under sub-section (3) of section 143 or reassessment under section 147 has been paid within the period specified in the notice of demand; (b) where penalty has been levied or, as the case may be, leviable under the circumstances referred to in sub-section (9) of section 270A, additional income tax amounting to one hundred per cent. of the amount of tax payable on under-reported income has been paid within the period specified in the notice of demand, in lieu of such penalty; and (c) no appeal has been filed against the order referred to in clauses (a) and (b). (2) An application referred to in sub-section (1) shall be made within one month from the end of the month in which the order referred to in clause (a) and clause (b) of the said sub-section has been received by the assessee, in such form and verified in such manner, as may be prescribed. (3) The Assessing Officer shall, on fulfilment of the conditions specified in sub-section (1) and after the expiry of the period of filing the appeal as specified in clause (b) of sub-section (2) of section 249, grant immunity from imposition or, as the case may be, waiver of penalty under section 270A and initiation of proceedings under section 276C or section 276CC. (3A) No immunity or, as the case may be, waiver under sub-section (3) shall be granted where any proceedings has been initiated under Chapter XXII (offences and prosecutions).” The above amendment will take effect from 1 March 2026 and will apply from AY 2026-2027. |

–

| VTPA Comments | Presently in law immunity under section 270AA can only be granted in the cases of underreporting of income and not in the case of under-reporting of income in consequence of misreporting.

The amendment also now provides immunity to the taxpayer in respect of under-reporting of income in consequence of misreporting, provided that the taxpayer pays an additional income-tax to the extent of 100% of the amount of tax payable on such income in lieu of the penalty. |

–

| Dispute resolution committee

[Section 245MA] |

In section 245MA of the Income-tax Act, in sub-section (2), the dispute resolution committee subject to such conditions as may be prescribed shall have the powers to reduce or waive any penalty imposable under this Act or grant immunity from prosecution for any offence punishable under this Act in case of a person whose disputes is resolved under this Chapter XIX-AA.

It is proposed for the words “waive any penalty imposable”, the words “waive any penalty imposed or imposable” shall be substituted and shall be deemed to have been substituted with effect from the 1st day of March, 2026. |

OFFENCES & PROSECUTION

| Contravention of order made under sub-section (3) of section 132

[Section 275A] |

– Section 275A of the Act applies when a person violates an order passed during search and seizure under section 132(3)

– It is proposed to amend the marginal heading of this section as below: “Contravention of order made during search action.” – The words ‘rigorous imprisonment’ have been substituted with the words ‘simple imprisonment’ – This amendment will take effect from the 1st day of March, 2026 |

–

| Failure to comply with the provisions of clause (iib) of sub-section (1) of section 132

[Section 275B] |

– Section 275B of the Act applies when a person fails to afford necessary facility during search and seizure under section 132(3)

– It is proposed to amend the marginal heading of this section as below: “Failure to afford facility for inspection of books of account during search.” – The words ‘rigorous imprisonment for a term which may extend to two years….’ have been substituted with the words ‘simple imprisonment for a term up to six months….’ – This amendment will take effect from the 1st day of March, 2026 |

–

| Removal, concealment, transfer or delivery of property to thwart tax recovery

[Section 276] |

– This section pertains to transfer of assets to evade recovery of tax

– For the words “rigorous imprisonment for a term which may extend to two years and shall also be liable to fine”, the words “simple imprisonment for a term up to two years and with fine” have been substituted – This amendment will take effect from the 1st day of March, 2026 |

–

| Substitution of new sections for sections 276B, 276BB, 276C, 276CC, 276CCC and 276D

Decriminalisation of offences |

– Section 276B

Failure to pay tax to the credit of Central Government under Chapter XII-D or XVII-B. The offences under section 276B are proposed to be fully decriminalized, as below: (i) with simple imprisonment for a term which may extend to two years, or with fine, or with both, in a case where amount of such tax exceeds fifty lakh rupees; (ii) with simple imprisonment for a term which may extend to six months, or with fine, or with both, in a case where amount of such tax exceeds ten lakh rupees but does not exceed fifty lakh rupees; (iii) with fine, in any other case. – Section 276BB Failure to pay tax collected at source. Section 276BB states that if a person fails to pay to the credit of the Central Government, the tax collected by him as required under the provisions of section 206C, he shall be punishable with rigorous imprisonment for a term which shall not be less than three months but which may extend to seven years and with fine It is now proposed to amend the section to include the following punishment: (i)with simple imprisonment for a term which may extend to two years, or with fine, or with both, in a case where amount of such tax exceeds fifty lakh rupees; (ii) with simple imprisonment for a term which may extend to six months or with fine, or with both, in a case where amount of such tax exceeds ten lakh rupees but does not exceed fifty lakh rupees; (iii) with fine, in any other case |

| – 276C

Wilful attempt to evade tax, etc 276C(1) – This sub-section provides that any wilful attempt to evade tax, penalty or interest, or to under-report income under the Act, is punishable, without prejudice to any other applicable penalties as below: (i) in a case where the amount sought to be evaded or tax on under-reported income exceeds twenty-five hundred thousand rupees, with rigorous imprisonment for a term which shall not be less than six months but which may extend to seven years and with fine; (ii) in any other case, with rigorous imprisonment for a term which shall not be less than three months but which may extend to two years and with fine. 276C(2) – This sub-section provides for wilful evasion of payment of tax If a person wilfully attempts in any manner whatsoever to evade the payment of any tax, penalty or interest under this Act, he shall, without prejudice to any penalty that may be imposable on him under any other provision of this Act, be punishable with: Rigorous imprisonment for a term which shall not be less than three months but which may extend to two years and shall, in the discretion of the court, also be liable to fine The above punishments have been amended for both sub-section (1) and (2) as : (a) with simple imprisonment for a term which may extend to two years, or with fine, or with both, in a case where the amount sought to be evaded or tax on under-reported income exceeds fifty lakh rupees; (b) with simple imprisonment for a term which may extend to six months, or with fine, or with both, in a case where the amount sought to be evaded or tax on under-reported income exceeds ten lakh rupees but does not exceed fifty lakh rupees; (c) with fine, in any other case. |

|

|

|

– 276CC

Failure to furnish returns of income This section pertains to a person wilfully failing to furnish returns of income under section 115WD(1) or (2) or section 115WH, 139(1), 142(1)(i), section 148 or 153A, This section has been amended to reduce harsh punishment for non-filing and limiting to only fines in low-value cases as below: (a) with simple imprisonment for a term up to two years, or with fine, or with both, where the amount of tax, which would have been evaded if the failure had not been discovered, exceeds fifty lakh rupees; or (b) with simple imprisonment for a term up to six months, or with fine, or with both, where the amount of tax, which would have been evaded if the failure had not been discovered, exceeds ten lakh rupees but does not exceed fifty lakh rupees; or (c) with fine, in any other case: |

| – 276CCC

Failure to furnish return of income in search cases This section pertains to a person wilfully failing to furnish returns of income which he is required to furnish by notice given under 158BC(1)(a) This section is amended so as to reduce the punishment as below: (a) with simple imprisonment for a term which may extend to two years, or with fine, or with both, in a case where the amount of tax exceeds fifty lakh rupees; (b) with simple imprisonment which may extend to six months, or with fine, or with both, in a case where the amount of tax, exceeds ten lakh rupees but does not exceed fifty lakh rupees; (c) with fine, in any other case. |

|

|

|

– 276D

Failure to produce accounts and documents Section 276D provides that if a person wilfully fails to produce such accounts and documents as are referred to in the notice under section 142(1) or wilfully fails to comply with a direction issued to him under 142(2A) It is proposed to amend section 276D of the Act so as to change the punishment as below: (a) in the case where a person wilfully fails to produce, or cause to be produced, on or before the date specified in any notice served on him under sub-section (1) of section 142, such accounts and documents as are referred to in the notice. This offence is proposed to be decriminalised. (b) in the case where a person wilfully fails to comply with a direction issued to him under sub-section (2A) of section 142, he shall be punishable with rigorous imprisonment for a term which may extend to one year and with fine. This punishment is proposed to be changed to “simple imprisonment for a term which may extend to six months or with fine These amendments will take effect retrospectively from 1st March, 2026. |

–

| VTPA Comments | – The 2026 Budget has aimed to decriminalize most offences and replace “rigorous” with “simple” imprisonment for many offences and in cases of low value offences, only fines have been prescribed.

– Most prosecution and offences have been linked to the amount of tax sought to be evaded, with higher amounts facing longer, but simple, imprisonment terms. – Before this amendment, relatively small tax evasion cases could trigger mandatory jail terms, offering courts little scope for flexibility. The new law replaces this with a graded punishment system that scales punishment based on the quantum of tax and the nature of non-compliance. |

–

| False statement in verification, etc.

[Section 277] |

– As per the existing provision, if a person makes a statement in any verification under the Act or under any rule made thereunder, or delivers an account or statement which is false, and which he either knows or believes to be false, or does not believe to be true, he is punishable with:

– (i) Rigorous imprisonment for a minimum term of six months, which may extend up to seven years and fine for cases where tax evasion would have been more than 25,00,000; and – (ii) Rigorous imprisonment for a minimum period of three years upto two years and fine. – It is proposed to amend and for clauses (i) and (ii), the following clauses shall be substituted namely:–– – “(a) with simple imprisonment for a term up to two years, or with fine, or with both, where the amount of tax, which would have been evaded, exceeds fifty lakh rupees; or – (b) with simple imprisonment for a term up to six months, or with fine, or with both, where the amount of tax, which would have been evaded, exceeds ten lakh rupees but does not exceed fifty lakh rupees; or – With fine, in any other case. – This amendment will take effect from the 1st March 2026. |

| Falsification of books of account or document, etc.

[Section 277A] |

– Section 277A provides that if any person wilfully and knowingly makes a false entry, or omits or alters any entry in books of account or other documents with the intent to evade tax such person is punishable with rigorous imprisonment and fine.

– In section 277A, the punishment of rigorous imprisonment for a term not be less than three months up to two years with fine, is now changed to simple imprisonment for a term up to two years with fine. – This amendment will take effect from the 1st March 2026. |

–

| Abetment of False return, etc.

[Section 278] |

– Section 278 provides for prosecution of any person who abets or induces another person to make or deliver a false return, statement, account, declaration, or other document under the Income-tax Act.

– If a person knowingly and willfully encourages or assists another in committing such an act, thereby facilitating concealment of income or tax evasion and they can be punished with imprisonment and fine. – Section 278 has been revised to change the punishment structure for offences involving false statements or attempts to evade tax. The earlier clauses (i) and (ii) are replaced with a graded penalty framework based on the quantum of tax, penalty, or interest sought to be evaded: – If the amount involved exceeds INR 50 lakh, the offence is punishable with simple imprisonment up to 2 years, or fine, or both. – If the amount involved is more than INR 10 lakh but up to ₹50 lakh, the offence is punishable with simple imprisonment up to 6 months, or fine, or both. – For any amount up to INR 10 lakh, the punishment is limited to a fine only. – This amendment will take effect from the 1st March 2026. |

–

| Punishment for second and subsequent offences

[Section 278A] |

– Section 278A provides for enhanced punishment where a person, after having been convicted under specified prosecution provisions of the Income-tax Act, commits the same offence again.

– In cases of second or subsequent convictions under sections such as 276B, 267BB 276C, 276CC, 276DD 277, 278, or other related prosecution provisions, the punishment becomes more stringent, generally involving rigorous imprisonment for a longer minimum term, along with fine. – Section 278A has been amended to the effect that: – The nature of imprisonment has been downgraded from rigorous imprisonment to simple imprisonment. – The earlier minimum term of seven years has been reduced to three years. – This amendment will take effect from the 1st March 2026. |

| VTPA Comments | These sections are being amended to ease the severity of punishment for offences under prosecution-related provisions of the Act. The key change in most of these sections are that the nature of imprisonment has been downgraded from rigorous imprisonment to simple imprisonment. |

–

| Disclosure of particulars by public servants

[Section 280] |

– Section 280 restricts public servants from disclosing any particulars contained in statements, returns, documents, accounts, or records obtained under the Income-tax Act.

– The punishment under this section was that the public servant who contravened the provision was liable to be punished with an imprisonment up to six months with a fine. – Section 280 is now amended, to say that the punishment for divulging confidential taxpayer information with a simple imprisonment up to one month, or with fine, or with both. – This amendment will take effect from 1st March, 2026. |

RATES OF TAX

1.1 For Individuals, Hindu Undivided Families, Association of Persons, Body of Individuals and Artificial judicial person – No changes under old regime

| Existing Tax Rates* | |

| Total Income (INR) | Rate (%) @ |

| 0 – 2,50,000# | Nil |

| 2,50,001 – 5,00,000# | 5 |

| 5,00,001 – 10,00,000 | 20 |

| 10,00,001 and above | 30 |

@ Health and Education cess of 4% is leviable on the amount of income-tax and surcharge.

# The basic exemption limit is INR 2,50,000 in case of every individual below the age of 60 years, INR 3,00,000 in case of resident individuals of the age of 60 to 80 years, and INR 5,00,000 for ‘very senior citizen’ in case of resident individuals of age 80 years and above.

* Where total income does not exceed INR 5,00,000, the assessee shall be entitled to a credit on the income-tax payable by way of Rebate under section 87A corresponding section 156(1) of IT Act 2025, of an amount equal to hundred percent of the Income-tax payable or INR 12,500, whichever is less.

The surcharge on income-tax, for Individuals, Hindu Undivided Families, Association of Persons, Body of Individuals and Artificial judicial person, are as follows:

| Total Income (INR) | Surcharge (%) |

| 50 lakh – 1 crore | 10 |

| 1 crore – 2 crores | 15 |

| 2 crores – 5 crores | 25 |

| Above 5 crores | 37 |

1.2 Changes in the new tax regime of taxation No changes under new regime

Taxability for individual or Hindu undivided family or association of persons [other than a co-operative society], or body of individuals, whether incorporated or not, or an artificial juridical person referred to in section 2(31)(vii) and under section 115BAC (1A) of IT Act 1961 for AY 2026-27/ corresponding sections respectively are section 2(77) (g) and section 202(1) of IT Act 2025 for TY 2026-27]

In the case of Individuals / HUFs, subject to foregoing of certain exemptions deductions and set off losses except the deductions below, and on satisfaction of certain conditions, unless an option is exercised as per provisions of section 115BAC (5) corresponding section 202 of IT Act 2025, the new concessional rates would be applicable as shown in the table below:

- Standard deduction to salaried taxpayers of INR 75,000

- Deduction from income in nature of family pension (1/3rd of income or INR 25,000, whichever is less) (section 57(iia) of IT Act 1961 corresponding section 93 (1)(d) of IT Act 2025

- Amount paid or deposited in Agniveer Corpus Fund under Section 80CCH of IT Act 1961 corresponding section 125 of IT Act 2025

| Total Income (INR) * | Tax Rate (%) |

| 0 to 4,00,000 | NIL |

| From 4,00,001 to 8,00,000 | 5 |

| From 8,00,001 to 12,00,000 | 10 |

| From 12,00,001 to 16,00,000 | 15 |

| From 16,00,001 to 20,00,000 | 20 |

| From 20,00,001 to 24,00,000 | 25 |

| Above 24,00,000 | 30 |

- Where total income does not exceed INR 12,00,000, the assessee shall be entitled to a credit on the income-tax payable under section 87A corresponding section 156 of IT Act 2025, of an amount equal to hundred percent of the Income-tax payable or INR 60,000, whichever is less.

- If the income of an individual exceeds Rs 12,00,000 and tax payable on such income exceeds the income amount over and above Rs.12,00,000, then the tax will be limited to the extent of such income exceeding Rs. 12 lakhs.

– The surcharge on income-tax, for Individuals, Hindu Undivided Families, Association of Persons, Body of Individuals and Artificial judicial person, under section 115BAC corresponding section 156 of IT Act 2025 are as follows:

| Total Income (INR) | Surcharge (%) |

| 50 lakh – 1 crore | 10 |

| 1 crore – 2 crores | 15 |

| Above 2 crores | 25 |

– The enhanced surcharge of 25% is not levied on income chargeable to tax under Sections 111A, 112 and 112A corresponding sections 196, 197 and 198 under IT Act 2025. Hence, the maximum rate of surcharge on tax payable on such incomes shall be 15%.

– The applicable rates of education cess (4%) would be computed on the tax amount including surcharge.

– Taxpayers having no business income will have option to opt for the old tax regime for every financial year / Tax year.

– For taxpayers having business income, the option for shifting out of new tax regime shall be exercised only once and shall be valid for that financial year and all subsequent financial years. Once the option is exercised, such person shall be able to exercise the option of opting back to new regime only once.

Section 115 BBE of the IT Act 1961, corresponding section 195 of the IT Act 2025 provides for taxation of income referred as below

| IT Act 2025 | IT Act 1961 | Nature of Income |

| 102 | 68 | Unexplained cash credits |

| 103 | 69 | Unexplained investments |

| 104 | 69A | Unexplained money/assets |

| 105 | 69B | Investment exceeding disclosed amount |

| 106 | 69C/69D | Unexplained expenditure/borrowings |

In case of above there is reduction in rates of tax as below

| Particulars | IT Act 1961 (Existing) | IT Act 2025 (Proposed) |

| Basic Tax Rate | 60% | 30% |

| Surcharge | 25% | 25% |

| Cess | 4% | 4% |

| Effective Tax Rates | Approx. 78% | Approx. 39% |

–

| Section 271AAC of the IT Act 1961 corresponding section 443 of the IT Act 2025 provides for mandatory penalty of 10% of tax on above unexplained income is proposed to be deleted. |

| Now, Penalty on unexplained income as per Section 270A(9) of the IT Act 1961 corresponding section 439(11) of IT Act 2025 is proposed to be considered as ‘Misreporting of Income’ at 200% of tax payable on such income. |

| Further, it is also proposed to extend immunity under section 270AA of the IT Act 1961corresponding section 440 of the IT Act 2025 to these cases, subject to paying an additional income-tax to the extent of 120% of the tax due on such unexplained income. |

Co-operative Societies

| Taxable Income | Tax rate |

| Upto INR 10,000 | 10% |

| INR 10,000 to 20,000 | 20% |

| Above INR 20,000 | 30% |

Surcharge

7% of tax amount if income exceeds INR 1 crore but does not exceed INR 10 crores

12% of tax amount if income exceed INR 10 crores

Education cess at 4% on tax amount including surcharge

On satisfaction of certain conditions, a resident co-operative society shall have the option to pay tax at 22% as per Section 115BAD of IT Act 1961 corresponding section 203 of IT Act 2025 plus surcharge at 10% on tax amount and education cess same as above.

On satisfaction of certain conditions, a resident co-operative society manufacturing co-operative society may opt to pay tax at concessional rate of 15% as per Section 115BAE of IT Act 1961 corresponding section 204 under IT Act 2025 plus surcharge at 10% on such tax and education cess same as above.

However, for specified funds referred to in the Explanation to section 10(4D) IT Act 1961 corresponding section mentioned in Schedule VI of IT Act, 2025, no surcharge to be applied for tax calculated on the part of its income earned under section 115AD(1)(a) of IT Act 1961 corresponding section 210 of IT Act 2025.

Companies / Firms / MAT provisions

There are no changes in the Income-tax rates for others in the Budget except in case of Minimum Alternate Tax (MAT) mentioned separately.

Summary of the same is provided as below:

| Description | Existing Tax Rates (%) | ||

| Having Income up to INR 1 crore | Having Income from INR 1 crore to 10 crores | Having Income more than INR 10 crores | |

| (Including Health and Education Cess @ 4%) | |||

| Regular tax as per Para E of the 1st Schedule to the Finance Act

(Turnover up to INR 400 crores) |

26.00 | 27.82* | 29.12** |

| Regular tax as per Para E of the 1st Schedule to the Finance Act

(Turnover > INR 400 crores and not covered below) |

31.20 | 33.384* | 34.94** |

| 115BA | 26.00 | 27.82* | 29.12** |

| 115BAA | 25.17*** | 25.17*** | 25.17*** |

| 115BAB | 17.16*** | 17.16*** | 17.16*** |

| MAT@ | 15.60 | 16.69* | 17.47** |

| (of book profits) | (of book profits)* | (of book profits)** | |

| Dividend Received from Foreign subsidiary company

(section 115BBD) |

15.60 | 16.69* | 17.47** |

| Regular tax (Foreign Company) | 36.4 | 37.13$ | 38.22# |

| Regular tax (Firm) | 31.20 | 34.94** | |

| Alternate Minimum Tax (AMT) | 19.24 | 21.55** | |

| Alternate Minimum Tax (AMT) (unit in IFSC) | 9.36 | 10.48** | |

| Alternate Minimum Tax (AMT) (Co-operative societies) | 15.60 | 16.69* | 17.47** |

* Inclusive of surcharge @ of 7 %

** Inclusive of surcharge @ of 12 %

*** Inclusive of surcharge @ of 10 %

$ Inclusive of surcharge @ of 2 %

# Inclusive of surcharge @ of 5 %

@ MAT provisions would not be applicable for those who has opted for special taxation regime under Section 115BAA & 115BAB

Proposed changes to the MAT mechanism as below:

| MAT paid by a company under the old tax regime shall be treated as final tax with no new MAT credit allowed. |

| MAT rate is proposed to be reduced from 15% to 14% of book profits. |

| Existing MAT credit shall be allowed to be set off only in cases where a domestic company opts for the New Tax Regime sections 115BAA and 115BAB of the Income-tax Act, 1961 corresponding sections 200 and 201 of the Income-tax Act, 2025. |

| The set-off of such existing MAT credit shall be restricted to an amount not exceeding 25% of the tax liability computed under the said New Tax Regime for the relevant tax year. |

| Further, a new section 206(4) of IT Act 2025 is proposed to be inserted whereby a foreign company is allowed to set-off the existing MAT credit only to the extent that the tax payable under the normal provisions of the Act exceeds the MAT liability for the relevant tax year. Accordingly, MAT credit shall not be allowed to be set off beyond such excess. |

| Certain non-residents deriving income from specified businesses and opting for presumptive taxation under section 61 of the IT Act 2025 are excluded from MAT. However, certain other non-resident businesses opting for presumptive taxation were not excluded.

The Finance Bill now proposes to extend this exclusion to all non-residents opting for presumptive taxation, including: ▪ Business of operation of cruise ships (subject to fulfilment of conditions) ▪ Business of providing services/technology in India for electronics manufacturing or production for a resident company |

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Author Bio