Summary: The Budget 2025 aims to accelerate economic growth while promoting inclusive development. A major focus is on “GYAN”—Garib (poor), Youth, Annadata (farmers), and Nari (women). Key initiatives include enhanced credit for farmers and micro-enterprises, a Cotton Productivity Mission, and a High-Yielding Seeds program. Infrastructure investments feature a ₹1.5 lakh crore interest-free loan to states and extended support for Jal Jeevan Mission. The financial sector sees reforms such as a Grameen Credit Score framework and increased FDI limits for insurance. In taxation, new income tax slabs have been introduced, with a higher exemption limit for salaried individuals and extended benefits for startups. Indirect tax changes include amendments in GST regulations, rationalization of TDS thresholds, and an extended timeline for updated tax returns. Other reforms include asset monetization, urban development, and a Nuclear Energy Mission. The budget also introduces BharatTradeNet for digital trade infrastructure and enhances research funding with a ₹20,000 crore allocation.

BACKGROUND

♦ Aspiration for Viksit Bharat

- Accelerate Growth

- Secure Inclusive Development

- Enhance Spending Power Of India’s Rising Middle Class

- Invigorate Private Sector Investments

- Uplift Household Sentiments

♦ MAJOR FOCUS ON GYAN (Garib, Youth, Annadata and Nari)

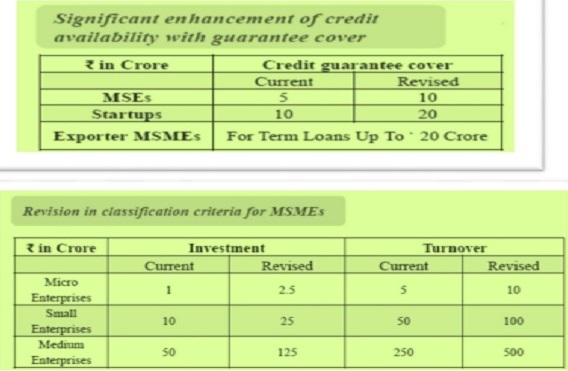

- Enhanced Credit through KCC (Facilitate short term loans for 7.7 crore farmers, fishermen, and dairy farmers with enhanced loan of ₹5 lakh.

- Mission for Cotton Productivity (5-year mission to facilitate improvements in productivity and sustainability of cotton farming)

- National Mission on High Yielding Seeds (Targeted development and propagation of seeds with high yield, pest resistance and climate resilience.

- Makhana Board in Bihar (To be set up to improve production, processing, value addition, and marketing and organisation of FPOs.

- Aatmanirbharta in Pulses

- India Post as a Catalyst for the Rural Economy

- Credit Cards for Micro Enterprises: Customised Credit Cards with a ₹ 5 lakh limit for micro enterprises registered on Udyam portal. In the first year, 10 lakh such cards will be issued.

- Scheme for first time Entrepreneurs: For 5 lakh first-time entrepreneurs, including women, Scheduled Castes and Scheduled Tribes, a new scheme, to be launched, to provide term loans up to ₹ 2 crore during the next 5 years.

- Investing in people, economy and innovation

- Investing in people, economy and innovation (Support to States for Infrastructure: With an outlay of 1.5 lakh crore, 50-year interest free loans to states for capital expenditure and incentives for reforms.

- Jal Jeevan Mission: To achieve 100 % coverage, the mission extended till 2028 with an enhanced total outlay.

- Power Sector Reforms: Incentivize distribution reforms and augmentation of intra-state transmission. Additional borrowing of 0.5 % of GSDP to states, contingent on these reforms.

- Asset Monetization Plan 2025-30: launched to plough back capital of ₹ 10 lakh crore in new projects.

- Urban Challenge Fund ₹ 1 lakh crore to implement the proposals for ‘Cities as Growth Hubs’, ‘Creative Redevelopment of Cities’ and ‘Water &Sanitation’.

- Maritime Development Fund with a corpus of ₹25,000 crore for long-term financing with up to 49 % contribution by the government.

- Nuclear Energy Mission for Viksit Bharat: Amendments to the Atomic Energy Act and the Civil Liability for Nuclear Damage Act will be taken up for active partnership with the private sector.

- UDAN: Regional connectivity to 120 new destinations and carry 4 crore passengers in the next 10 years.

- PM Research Fellowship- To provide ten thousand fellowships for technological research in IITs and IISc.

- Research, Development & Innovation- Allocating ₹ 20,000 crore to implement private sector driven Research, Development and Innovation initiative.

- Export Promotion Mission: With sectoral and ministerial targets to facilitate easy access to export credit, cross-border factoring support, and support to MSMEs to tackle non tariff measures in overseas markets.

- BharatTradeNet: A digital public infrastructure, ‘BharatTradeNet’ (BTN) for international trade will be set-up as a unified platform for trade documentation and financing solutions. Support for integration with Global Supply Chains.

- Financial Sector Reforms-

– ‘Grameen Credit Score’ framework to serve the credit needs of SHG members and people in rural areas.

– NaBFID to set up a ‘Partial Credit Enhancement Facility’ for corporate bonds for infrastructure.

– Revamped Central KYC registry to be rolled out in 2025.

– Rationalisation of requirements and procedures for speedy approval of company mergers.

– FDI limit for the insurance sector will be raised from 74 to 100 per cent.

SECTION-I

DIRECT TAXES

> RATES OF INCOME TAX FOR A.Y. 2026-27

Tax rates under section-115BAC- New regime

| Total income (Rs) | Tax rate |

| Upto 4,00,000/- | Nil |

| From 4,00,001 to 8,00,000/- | 5% |

| From 8,00,001 to 12,00,000/- | 10% |

| From 12,00,001 to 16,00,000/- | 15% |

| From 16,00,001 to 20,00,000/- | 20% |

| From 20,00,001 to 24,00,000/- | 25% |

| Above 24,00,000/- | 30% |

> TAX BENEFIT FOR SALARIED CLASS

Under the new tax regime, in respect of salaried class, Salaried income upto Rs 12,75,000/- is tax free (Rs 12 lac tax exempted income plus Rs 75,000/- standard deduction)

> REBATE UNDER SECTION-87A

√ Existing limit of Rs 25,000/- is proposed to increase to Rs 60,000/-.

√ Rebate not available in case of special income i.e. capital gains u/s 111A, 112 etc.).

> Amendment of Section 10 related to Exempt income of Non-Residents

> In order to incentivize operations from the IFSC, it is proposed to amend clause (4E) of section 10 to provide that the income of a non-resident on account of transfer of non-deliverable forward contracts or offshore derivative instruments or over the-counter derivatives, or distribution of income on offshore derivative instruments, entered into with Foreign Portfolio Investors being an IFSC unit shall also not be included in the total income subject to certain conditions as may be prescribed.

> Effective date-1st day of April, 2026.

> Scheme of presumptive taxation extended for non-resident providing services for electronics manufacturing facility

> It is proposed to provide a presumptive taxation regime for non-residents engaged in the business of providing services or technology, to a resident company which are establishing or operating electronics manufacturing facility or a connected facility for manufacturing or producing electronic goods, article or thing in India, under a scheme notified by the Central Government in the Ministry of Electronics and Information Technology and satisfies such conditions as prescribed in the rules.

> New Section-44BBD to be inserted.

> Taxation-Twenty-five per cent of the aggregate amount received/ receivable by, or paid/ payable to, the non-resident, on account of providing services or technology, as profits and gains of such non-resident from this business.

> Effective date-1st April, 2026

> Period of registration of smaller trusts or institutions

> Background- Section 12AB provides registration of trust or institution for a period of 5 years or provisional registration (where activities have not commenced at the time of filing application for registration) for a period of 3 years. At the expiry of such registration or provisional registration, or in case of provisional registration, if the activities of the trust or institution have commenced, the trust or institution is required to make application for further registration.

> Proposed Amendment- it is proposed to increase the period of validity of registration of trust or institution from 5 years to 10 years, in cases where the trust or institution made an application under sub-clause (i) to (v) of the clause (ac) of sub-section (1) of section 12A, and the total income of such trust or institution, without giving effect to the provisions of sections 11 and 12, does not exceed Rs. 5 crores during each of the two previous year, preceding to the previous year in which such application is made.

> Effective date-1st April, 2025.

> Income on redemption of Unit Linked Insurance Policy

> BACKGROUND- Clause (10D) of section 10 provides for income-tax exemption on the sum received under a life insurance policy, including bonus on such policy. There is a condition that the premium payable for any of the years during the terms of the policy should not exceed ten per cent of the actual capital sum assured.

Further amended by Finance Act, 2021- the exemption under this clause shall not apply with respect to any unit linked insurance policy or policies issued on or after the 01.02.2021, if the amount of premium or aggregate amount of premium payable during the term of such policy or policies exceeds Rs. 2,50,000.

> Proposed Amendment

– ULIPs to which exemption under clause (10D) of section 10 does not apply, is a capital asset [clause (14) of section 2]

– The profit and gains from the redemption of ULIPs to which exemption under clause (10D) of section 10 does not apply, shall be charged to tax as capital gains [sub-section (1B) of section-45].

– ULIPs to which exemption under clause (10D) of section 10 does not apply, shall be included in the definition of equity oriented fund [clause (a) of Explanation to section 112A].

> Effective date-1st April, 2026.

> Extension of timeline for tax benefits to start-ups

- BACKGROUND- Section 80-IAC- deduction of an amount equal to hundred percent of the profits and gains derived from an eligible business by an eligible start-up for three consecutive assessment years out of ten years, beginning from the year of incorporation, at the option of the assessee. Conditions-

– the total turnover of its business does not exceed one hundred crore rupees,

– it is holding a certificate of eligible business from the Inter-Ministerial Board of Certification.

– it is incorporated on or after the 1st day of April, 2016 but before the 1st day of April, 2025.

> Proposed Amendment- to extend the benefit for another period of five years, i.e. the benefit will be available to eligible start-ups incorporated before 01.04.2030.

> Effective date-1st April, 2025.

> PROVISIONS RELATED TO TDS

– Rationalisation in TDS threshold limits

| Section | Current threshold | Proposed threshold | Effective date |

| 193 – Interest on securities | NIL | Rs 10,000/- | 01.04.2025 |

| 194A – Interest other than Interest on securities | – Rs 50,000 for senior citizens

– Rs 40,000 for others When payer is bank, co-operative society & post office – Rs 5,000 for other cases |

– Rs 1,00,000 for senior citizens

– Rs 50,000 for others When payer is bank, co-operative society & post office – Rs 10,000 for other cases |

01.04.2025 |

| 194 – Dividend for an individual shareholder | Rs 5,000/- | Rs 10,000/- | 01.04.2025 |

| 194K – Income in respect of units of a mutual fund or specified company or undertaking | Rs 5,000/- | Rs 10,000/- | 01.04.2025 |

| 194B – Winnings from lottery, crossword puzzle, etc. | Aggregate of amounts exceeding Rs. 10,000/- during the financial year | Rs. 10,000/- in respect of a single transaction | 01.04.2025 |

| 194BB – Winnings from horse race | 01.04.2025 | ||

| 194D – Insurance commission | 01.04.2025 | ||

| 194G – Income by way of commission, prize etc. on lottery tickets |

Rs 15,000/- |

Rs 20,000/- |

|

| 194H – Commission or brokerage | |||

| 194-I Rent | Rs 2,40,000/- during the F.Y. | Rs 50,000/- per month or part of the month | 01.04.2025 |

| 194J – Fee for professional or technical services | Rs 30,000/- | Rs 50,000/- | 01.04.2025 |

| 194LA – Income by way of enhanced compensation | Rs 2,50,000/- | Rs 5,00,000/- | 01.04.2025 |

> Reduction in compliance burden by omission of TCS on sale of specified goods

- BACKGROUND- Sub-section (1H) of section 206C of the Act, requires any person being a seller who receives consideration for sale of any goods of the value or aggregate of value exceeding Rs 50 lakhs in any previous year, to collect tax from the buyer at the rate of 0.1% of the sale consideration exceeding Rs 50 lakhs, subject to certain conditions.

- Section 194Q of the Act, requires any person being a buyer, to deduct tax at the rate of 0.1%, on payment made to a resident seller, for the purchase of any goods of the value or aggregate of value exceeding fifty lakh rupees in any previous year.

- ISSUE- Sub-section (1H) of section 206C mandates tax collection at source (TCS) by a seller while Section 194Q provides for tax deduction at source (TDS) by a buyer on the same transaction.

- Proposed Amendment- It is proposed that provisions of sub-section (1H) of section 206C of the Act will not be applicable from the 1st day of April, 2025. Meaning thereby that it the buyers primary responsibility to deduct TDS under section-194Q.

> Removal of higher TDS/TCS for non-filers of return of income

BACKGROUND- Section 206AB of the Act, requires deduction of tax at higher rate when the deductee specified therein is a non-filer of income-tax return. Section 206CCA of the Act, requires for collection of tax at higher rate when the collectee specified therein is a non-filer of income-tax return. This is subject to other conditions specified in the two sections.

> Proposed Amendment-To address this issue and reduce compliance burden for the deductor/collector, it is proposed to omit section 206AB of the Act and section 206CCA of the Act.

> Extending the time-limit to file the updated return

> BACKGROUND- Sub-section (8A) of section 139 of the Act, relates to furnishing of updated return. As per the present provisions, an updated return can be filed upto 24 months from the end of the relevant assessment year.

> Proposed Amendment

– To extend the time-limit to file the updated return from existing 24 months to 48 months from the end of relevant assessment year.

– Rate of additional income-tax payable for updated return filed after expiry of 24 months and upto 36 months from the end of the relevant assessment year shall be 60% of aggregate of tax and interest payable.

– The additional income-tax payable for updated return filed after expiry of 36 months and upto 48 months from the end of the relevant assessment year shall be 70% of aggregate of tax and interest payable.

– Effective date-1st April, 2025.

SECTION-II

INDIRECT TAXES

> GST RELATED CHANGES

√ Clause (61) of section 2 of the Central Goods and Services Tax Act is being amended to explicitly provide for distribution of input tax credit by the Input Service Distributor in respect of inter-state supplies on which tax has to be paid on reverse charge basis, by inserting reference to sub-section (3) and sub-section (4) of section 5 of Integrated Goods and Services Tax Act. This amendment will be effective from 1st April 2025.

√ Sub-clause (c) of clause (69) of section 2 is being amended to replace “municipal or local fund” with “municipal fund or local fund” and to insert an Explanation after the said sub-clause, to provide for definitions of the terms ‘Local Fund’ and ‘Municipal Fund’ used in the definition of “local authority” under the said clause so as to clarify the scope of the said terms.

√ A new clause (116A) is being inserted in section 2 to provide definition of Unique Identification Marking for implementation of Track and Trace Mechanism.

√ Sub-section (4) of Section 12 relating to time of supply in respect of Vouchers is being deleted. (ii) Sub-section (4) of Section 13 relating to time of supply in respect of Vouchers is being deleted.

√ Clause (d) of sub-section (5) of section 17 is being amended to substitute the words “plant or machinery” with words “plant and machinery”. This amendment will be effective retrospectively from 1st July 2017, notwithstanding anything to the contrary contained in any judgment, decree or order of any court or any other authority.

√ Section 20(1) and Section 20(2) are being amended to explicitly provide for distribution of input tax credit by the Input Service Distributor in respect of inter-state supplies, on which tax has to be paid on reverse charge basis, by inserting reference to sub-section (3) and sub-section (4) of section 5 of Integrated Goods and Services Tax Act in said sub-sections of section 20 of Central Goods and Services Tax Act. The amendment will be effective from 1st April 2025.

√ Proviso to sub-section (2) of section 34 is being amended to explicitly provide for requirement of reversal of corresponding input tax credit in respect of a credit-note, if availed, by the registered recipient, for the purpose of reduction of tax liability of the supplier in respect of the said credit note.

√ Section 38(1) is being amended to omit the expression “auto generated” with respect to statement of input tax credit in the said subsection.

√ Section 38(2) is being amended by omitting the expression “auto generated” with respect to statement of input tax credit in said subsection and also to insert the expression “including” after the words “by the recipient” in clause (b) of said sub-section to make the said clause more inclusive.

√ Section 38(2) is being amended by inserting a new clause (c) in the said sub-section to provide for an enabling clause to prescribe other details to be made available in statement of input tax credit.

√ Section 39(1) is being amended so as to provide for an enabling clause to prescribe conditions and restriction for filing of return under the said sub-section.

√ Section 107(6) is being amended to provide for 10% mandatory predeposit of penalty amount for appeals before Appellate Authority in cases involving only demand of penalty without any demand for tax.

√ Section 112(8) is being amended to provide for 10% mandatory predeposit of penalty amount for appeals before Appellate Tribunal in cases involving only demand of penalty without any demand for tax.

√ New section 122B is being inserted to provide penalty for contraventions of provisions related to the Track and Trace Mechanism provided under section 148A.

√ New section 148A is being inserted to provide for an enabling mechanism for Track and Trace Mechanism for specified commodities.

√ Schedule III of CGST Act is being amended, w.e.f. 01.7.2017 by inserting a new clause (aa) in paragraph 8 of Schedule III of the Central Goods and Services Tax Act, to provide that the supply of goods warehoused in a Special Economic Zone or in a Free Trade Warehousing Zone to any person before clearance for exports or to the Domestic Tariff Area shall be treated neither as supply of goods nor as supply of services.

√ It further seeks to amend Explanation 2 of Schedule III of the Central Goods and Services Tax Act, w.e.f. 01.07.2017 to clarify that the said explanation would be applicable in respect of clause (a) of paragraph 8 of the said Schedule.

√ It further seeks to amend Schedule III of CGST Act, w.e.f. 01.07.2017 by inserting Explanation 3 to define the terms ‘Special Economic Zone’, ‘Free Trade Warehousing Zone’ and ‘Domestic Tariff Area’, for the purpose of the proposed clause (aa) in paragraph 8 of said Schedule.

√ No refund of tax already paid will be available for the aforesaid activities or transactions referred to in clause 128.

(Source- Finance Bill 2025)