The government introduced the Taxation Laws (Amendment) Bill, 2021, which seeks to withdraw tax demands made under the Finance Act, 2012 retrospective legislation to tax the indirect transfer of Indian assets.

The Taxation Laws (Amendment) Bill, 2021 inserted three provisos (Fourth, Fifth, and Sixth Proviso) in Explanation 5 to Section 9(1)(i) to give relief to certain eligible entities impacted by the retrospective amendment. These amended provisions of indirect transfer of assets in India shall not apply to the assets transferred before 28- 05-2012 (i.e., the date on which the Finance Bill, 2012 received the assent of the President). Accordingly, all pending assessments shall be deemed to have been concluded without additions for such income and the demand raised in concluded assessments or rectification orders for indirect transfer of Indian assets made before 28-05- 2012 shall be nullified on the fulfillment of specified conditions.

Explanation 5 to Section 9(1)(i)

Explanation 5 to Section 9(1)(i) clarifies that an asset or a capital asset, being any share or interest in a company or entity registered or incorporated outside India, shall be deemed to be situated in India, if the share or interest derives, directly or indirectly, its value substantially from the assets located in India. In other words, an asset or capital asset shall be deemed to have been situated in India, and income arising from transfer of such asset shall be deemed to accrue or arise in India if the following conditions are satisfied:

1. The asset or capital asset is a share (or interest) in a company (or entity) registered or incorporated outside India;

2. The share or interest derives its value substantially from the assets located in India; and

3. Such value may be derived directly or indirectly from the assets located in India.

However, the share or interest shall not be deemed to derive its value substantially from the assets (whether tangible or intangible) located in India, if, on the specified date, the value of such assets:

1. Does not exceed Rs. 10 crores; and

2. Does not represent at least 50% of the value of all the assets owned by the company or entity, as the case may be.

The Fourth Proviso to Explanation 5 to Section 9(1)(i)

provides that the provisions of Explanation 5 (hereinafter referred to as ‘indirect transfer of Indian assets’) shall not apply, in respect of income accruing or arising through or from the indirect transfer of Indian asset made before 28-05-2012, to:

a. an assessment or reassessment to be made under Section 143, Section 144, Section 147 or Section 153A or Section 153C;

b. an order to be passed enhancing the assessment or reducing a refund already made or otherwise increasing the liability of the assessee under Section 154; or

c. an order to be passed deeming a person to be an assessee in default under Section 201(1).

In other words, the retrospective impact of Explanation 5 to Section 9(1)(i) shall be ignored if assets situated in India are indirectly transferred before 28-05-2012. Thus, the income accruing or arising through or from such indirect transfer of Indian assets or capital assets shall not be taxable in India. Therefore, all assessments or rectification applications pending before the authorities, to the extent it relates to the computation of income from indirect transfer of assets, shall be deemed to be concluded without any additions.

The Fifth Proviso to Explanation 5 to Section 9(1)(i)

provides that the provisions of Explanation 5 shall not apply, in respect of income accruing or arising through or from the indirect transfer of Indian asset made before 28-05-2012, to:

a. an assessment or reassessment made under Section 143, Section 144, Section 147 or Section 153A or Section 153C;

b. an order passed enhancing the assessment or reducing a refund already made or otherwise increasing the liability of the assessee under Section 154;

c. an order passed deeming a person to be an assessee in default under Section 201(1); or

d. an order passed imposing a penalty under Chapter XXI or under Section 221.

In other words, the retrospective impact of Explanation 5 to Section 9(1)(i) shall be ignored if assets situated in India are indirectly transferred before 28-05-2012. Thus, the income accruing or arising through or from such indirect transfer of Indian assets or capital assets shall not be taxable in India. Therefore, all assessments or rectification applications concluded by the authorities, to the extent it relates to the computation of income from indirect transfer of assets, shall be deemed to never have been passed or made.

The Sixth Proviso to Explanation 5 to Section 9(1)(i) provides that where any amount becomes refundable to such person, then such amount shall be refunded to him, but no interest under section 244A shall be paid on that amount.

The relief in cases of concluded assessments shall be given to only those assessees who satisfy the following conditions:

a. where the assessee has filed an appeal before an appellate forum or any writ petition before the High Court or the Supreme Court against any order in respect of said income, he shall either withdraw or submit an undertaking to withdraw such appeal or writ petition, in such form and manner as may be prescribed;

b. where the said person has initiated any proceeding for arbitration, conciliation or mediation, or has given any notice thereof under any law for the time being in force or under any agreement entered into by India with any other country or territory outside India, whether for protection of investment or otherwise, he shall either withdraw or shall submit an undertaking to withdraw the claim, if any, in such proceedings or notice, in such form and manner as may be prescribed;

c. the said person shall furnish an undertaking, in such form and manner as may be prescribed, waiving his right, whether direct or indirect, to seek or pursue any remedy or any claim in relation to the said income which may otherwise be available to him under any law for the time being in force, in equity, under any statute or under any agreement entered into by India with any country or territory outside India, whether for protection of investment or otherwise; and

d. such other conditions as may be prescribed.

KEY HIGHLIGHTS

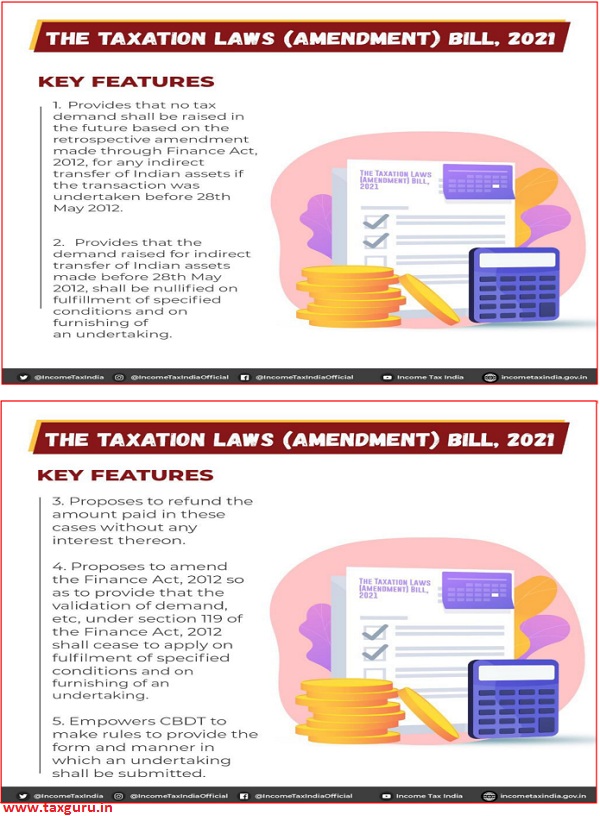

1. Taxation Laws (Amendment) Bill, 2021 seeks to withdraw tax demands made under the 2012 retrospective legislation to tax the indirect transfer of Indian assets

2. The bill proposes that any demand raised for indirect transfer of Indian assets made before May 28, 2012 shall be nullified on fulfilment of specified conditions such as withdrawal or furnishing of undertaking for withdrawal of pending litigation and furnishing of an undertaking to the effect that no claim for cost, damages, interest shall be filed.

3. The bill proposes to refund the amount paid in these cases without any interest.

4. It also proposes to amend the Finance Act, 2012 to provide that the validation of demand under section 119 of the Finance Act, 2012 shall cease to apply on fulfilment of specified conditions.

5. The Bill states that the issue of taxability of gains arising from the transfer of assets located in India through the transfer of shares of a foreign company was a subject matter of protracted litigation.

SIGNIFICANCE

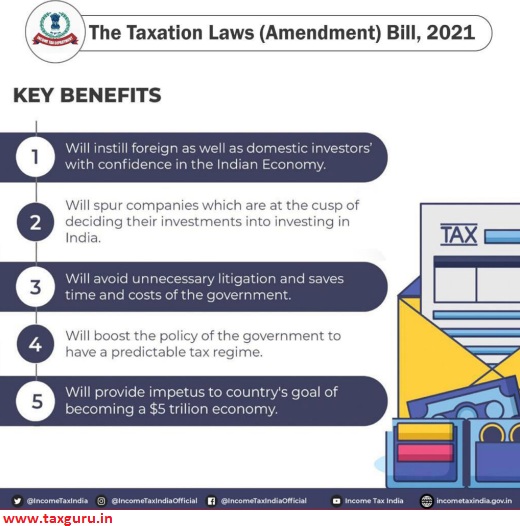

1. The bill is likely to benefit many companies including Vodafone and Cairn Energy who had to pay tax based on the retrospective tax demand provision.

2. The amendment will have a direct bearing on the long-running tax disputes

3. As per the amendment, the centre will withdraw all back tax demands on companies and will refund the money collected to enforce such levies.

4. This is crucial as the country stands at a juncture today when quick recovery of the economy after the COVID-19 pandemic is the need of the hour and foreign investment will play a significant role in promoting faster economic growth and employment.