CA Renu Singhal

WHAT IS INCOME FROM HOUSE PROPERTY?

Income that arises by owner from any building or land attached with building is chargeable under the head House Property..

Preconditions

1. There must be a Building or Land appurtenant thereto. Means if there is only a piece of open pl0t of land i.e. on which there is no building, will not be taxable under this head But if land is attached with a building forming part of building shall be taxable under this head. For example: If there is swimming pool in a building, playground, backyard, kitchen garden or garage, then all these shall be chargeable under this head.

Meaning of Building: Any structure having walls and roof thereof is Building. Building constructed of wood, brick or stone may be considered as building and it is not always necessary to have roof on top of it.

House property includes all type of house properties, i.e., residential houses, godowns, cinema building, workshop building, hotel building, office, shop etc.

Example: Mr. A has one big farm house. It includes vast open area within its boundaries. The farm house has been let out at a rent of Rs. 5,00,000 p.m., out of which rent of Rs. 1,25,000 p.m. is attributable to the open land. In this case, entire rental income that is 5,00,000 p.m. is taxable under the head house property.

Building under this head includes self occupied property or let out property. Let out of property may be for residential, factory, godown or office purposes.

Building used for own business or profession will not be covered under this head.

2. Person must be owner of property. Owner may be individual or a Company incorporated for the purposes of buying and development of land. Property will be taxable under this head even if property is his stock in trade or letting out of property is the business of assessee.

But it is not always necessary that only the owner of property shall be chargeable to tax under this head.

Example: Under leasehold agreement, if a superstructure is built on a leasehold land, then the lessee shall be taxable under this head irrespective of the fact that he has to handover the possession of superstructure after the expiry of lease period. Ownership includes both free-hold and lease-hold rights and also includes deemed ownership

WHAT ARE THE INCOMES FROM HOUSE PROPERTY?

1. RENTAL INCOME: It means the rental income in the hands of the owner by letting out the house property. Rental income of a person other than the owner cannot be charged to tax under the head “Income from house property”. Hence, rental income received by a tenant from sub-letting cannot be charged to tax under the head “Income from house property”. Such income is taxable under the head “Income from other sources”.

2. DEEMED RENTALS: Where Rental income is not received by the registered owner of the property then such rental income is not charged to tax under the head “Income from house property”.

However, in certain cases a person may not be the registered owner of the property even though he is treated as owner (i.e. deemed owner) of the property and rental income to be considered as DEEMED RENT and such rental income shall be charged to tax under the head house property. Few such cases are given hereunder:

(i) Transfer of property to a Minor Child or Spouse without adequate consideration. In this case, transferor shall be considered as deemed owner.

Note:

a. Where transfer is made to minor married daughter then such minor daughter shall be treated as owner for the purposes of this head.

b. Where transfer of property is made to spouse under an agreement to live apart, then such spouse shall be treated as owner for the purposes of this head.

(ii) Holder of impartible estate is deemed as the owner of the property comprised in the estate. Example: Impartible estate means property which is not legally divisible i.e. partition of which cannot be done under the prevalent conditions, then holder of such estate shall be treated as owner for the purposes of chargeability under this head.

(iii) A member of co-operative society, company or other association of persons to whom a building/Flat is allotted or leased under house building scheme of the society, company or association, such member are deemed owner of the property. This is irrespective of the fact that ownership of such flat lies with Co-operative society, company or other association of persons.

(iv) A person acquiring property by “power of attorney transaction” by satisfying the conditions of section 53A of the Transfer of Property Act, will be treated as deemed owner (although he may not be the registered owner). Section 53A of said Act prescribes following conditions:

(a) There must be an agreement in writing.

(b) The purchase consideration is paid or the purchaser is willing to pay it.

(c) Purchaser has taken the possession of the property in pursuance of the agreement.

(v) In case of lease of a property for a period exceeding 12 years (whether originally fixed or provision for extension exists), lessee is deemed to be the owner of the property. However, any right by way of lease from month-to-month or for a period not exceeding one year is not covered by this provision. For Example, Where property given on lease for 10 years with a right to extend it for another 2 years, then lessee will be treated as deemed owner. But, where a property leased out for one month with an option to renew it for a month till next 20 years, then in such case lessee will not be treated as deemed owner as each lease period is of one month.

3. LOSS IN CASE OF SELF OCCUPIED PROPERTY: In case of Self Occupied property, GAV is to be considered as NIL and deduction of interest on borrowed capital shall be available which will result into Loss under the head House Property. Such loss in fact is beneficial (income) for owner as it can be set off against other incomes which will result into lower income and in turn low taxability.

Note:

i. Where assessee has more than one Self Occupied Property, then only one house property (of the choice of assessee) shall be treated as Self Occupied and rest of the properties shall be treated as Deemed to be let out property.

ii. Where property is not occupied due to personal convenience then House Property will be treated as deemed to be let out property. For Example: Abhishek is having a flat in Delhi whereas he is living along with his father who is also living in Delhi. Then in such case, since Abhishek is not occupying his flat due to his personal convenience therefore his own flat will be treated as deemed to be let out property.

iii. Where property is not occupied by the owner for the reasons of his employment, business or profession carried out at any other place.

Purpose for deduction on account of interest of Self Occupied Property: Deduction on account of interest on borrowed capital motivates assesses to invest in property. From such investment assessee gets income tax benefit as well as property. In nutshell, he will in a beneficial position in buying property by taking a loan rather than taking property on rent.

STEPS FOR COMPUTATION OF INCOME FROM HOUSE PROPERTY

| Computation of Income under the head House Property | |

| Gross Annual Value | xxx |

| Less: Municipal Taxes | (xxx) |

| Net Annual Value | xxx |

| Less: Deductions under section 24 | |

| Standard Deduction | (xxx) |

| Interest on borrowed capital | (xxx) |

| Income from house property | xxx |

Let’s discuss each item of computation one by one:

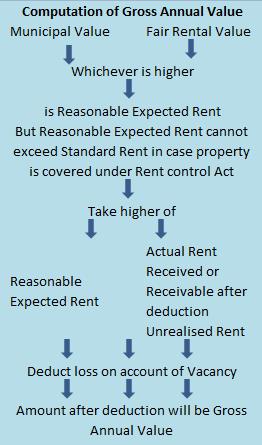

Gross Annual Value

Amount which can be earned in a year from house property is its Gross Annual Value. Four components are required for computing Gross Annual Value i.e. Municipal Value, Fair Rental Value, Standard Rent, Actual Rent and computation is shown in the form of chart hereunder:

Components of Gross Annual Value

Component 1: Municipal Value: The valuation done by Municipality of the area of property is considered as Municipal value. However, in some big cities, value is determined after deduction 10% on account of repairs, allowance for sewage and water tax etc.

Component 2: Fair Rental Value: This is the rent which can be getting from similar property in similar locality.

Component 3: Standard Rent: This is the maximum rent which can be charged from tenant under Rent Control Act.

Component 4: Actual Rent received or receivable for previous year less unrealised rent.

Note:

Meaning or Unrealised Rent: The amount of rent which a landlord is unable to recover from tenant provided i) landlord has taken reasonable steps to get the property vacated and have taken legal action for recovery of unrealised rent ii) tenant has already vacated the property iii) such tenant is not in occupation of any other property of landlord.

Example:

| Computation of Gross Annual Value | ||||||||

| Details | Rs. | Rs. | Rs. | Rs. | Rs. | Rs. | Rs. | |

| Municipal Value (MV) | 100 | 100 | 100 | 100 | 200 | 200 | 400 | |

| Fair Rental Value (FRV) | 120 | 90 | 200 | 500 | 200 | 400 | 200 | |

| Standard Rent (SR) | 140 | 80 | 150 | 400 | 200 | 500 | 100 | |

| Annual Rent | 150 | 60 | 300 | 600 | 300 | 300 | 400 | |

| Unrealised Rent | 20 | 10 | 50 | 300 | 200 | 50 | ||

| Loss due to Vacancy | – | – | – | – | – | 50 | 70 | |

| Solution | ||||||||

| Step 1 | Higher of MV and FRV | 120 | 100 | 200 | 500 | 200 | 400 | 400 |

| Step 2 | Lower of Step 1 value and SR | 120 | 80 | 150 | 400 | 200 | 400 | 100 |

| Step 3 | Annual Rent – Unrealised Rent | 130 | 50 | 250 | 300 | 100 | 300 | 350 |

| Step 4 | Higher of Step 2 and Step 3 | 130 | 80 | 150 | 400 | 200 | 400 | 350 |

| Step 5 | Loss due to Vacancy | – | – | – | – | – | 50 | 70 |

| Step 6 | Gross Annual Value (Step 4 – Step 5) | 130 | 80 | 150 | 400 | 200 | 350 | 280 |

WHAT ARE THE ELIGIBLE DEDUCTIONS?

Deduction for the payment of Municipal taxes:

Municipal taxes levied by the local authority are allowed as a deduction from the Gross Annual Value to arrive at the Net Annual Value. The deduction shall be allowed only if the following conditions are met:

-The municipal taxes are actually paid during the financial year

-The municipal taxes are actually borne by the owner

Note: The Municipal taxes are allowed as a deduction only in the financial year in which they are actually paid. If the taxes are due but not paid are not allowed as a deduction. However, municipal taxes etc paid during a financial year are allowed even if they relate to past or future years. Similarly, Municipal Taxes paid in foreign country for a House Property situated outside India shall be allowed as deduction but amount paid to municipal authorities for authorisation or regularisation of property shall not be allowed as deduction.

Statutory deduction @ 30% of Net Annual Value

A deduction at a flat rate of 30% of Net Annual Value is allowed to everyone irrespective of actual expenditure made on account of repairs, maintenance, ground rent, insurance etc. For the purpose of statutory deduction Net Annual Value is Gross Annual Value less taxes paid.

INTEREST ON HOME LOAN

Whenever any home loan is taken for purchase, construction, repair, renewal or reconstruction of house property – the interest is allowed as a deduction from the Net Annual Value on accrual basis (accrual basis means interest is allowed as a deduction even though the interest is not actually paid). It is pertinent to note that

a.Interest on Loan taken for purchase of land is also deductible under this head as in statute the word Property is mentioned and not house property.

b. no deduction is allowed for any brokerage or commission for arranging the loan. In case of a self occupied house property, this deduction is allowed to be claimed and therefore in such a case, an assessee may have a loss under the head House Property. The total amount allowed towards this deduction for a self occupied house property is Rs 2,00,000 for the assessment year 2015-16. In case of a let out or a deemed to be let out property, the entire interest is allowed as deduction under section 24. This interest can be claimed when the construction of the property is complete

Pre Acquisition Period Interest

Pre Acquisition Period Interest is the Interest on loan taken for acquisition or construction of property for the period

Starting : From the date of borrowing

Ending: March 31st immediately preceding the date of acquisition or construction of property

Deduction of Pre Acquisition Period Interest is allowed in five equal instalments commencing from the year in which construction or acquisition of property takes place.

| Computation of Interest | ||

| Loan Amount | 1,00,000 | |

| Loan Taken on | 01.05.2012 | |

| Date of completion of construction | 01.07.2015 | |

| Interest rate | 12% p.a. | |

| Solution | ||

| Pre Acquisition Period | ||

| Starts from Date of Borrowing | 01.05.2012 | |

| Ends on March 31st immediately preceeding the date of construction | 31.03.2015 | |

| Interest for Pre Acquisition Period | ||

| 2012-13 (01.05.2012 to 31.03.2013) | 11000 | 1,00,000×12%x 11/12 |

| 2013-14 (01.05.2013 to 31.03.2014) | 12000 | |

| 2014-15 (01.05.2014 to 31.03.2015) | 12000 | |

| Total Pre Acquisition Interest | 35000 | |

| Deduction will start from expiry of Pre Acquistion period i.e. 1/5th of Pre Acquisition Interest + Current Year Interest | 17000 | 35000/5 + 12000 |

Additional tax benefits under section 80EE

Section 80EE has been revamped. An additional deduction of Rs 50,000 on home loan interest is allowed to be claimed starting financial year 2016-17. However to be able to claim this deduction, you must meet the following conditions

-The loan must be taken between 1st April 2016 to 31st March 2017

-As on the date of sanction of the loan the taxpayer should not own any property

-The loan must be taken from a financial institution

-The value of the house must be less than Rs 50lakhs

-The loan must be for less than Rs 35lakhs

If these conditions are met you can claim an additional deduction of Rs 50,000 for home loan interest besides Rs 2 lakh mentioned above. There is no time limit on the period for which this deduction is allowed, a person can claim this for as long as you are repaying the loan.

Extension of time limit for completion of construction – Sometimes, taxpayers take home loans for under construction property. To claim Rs 2 lakhs deduction on such home loan interest, the construction of the property must be completed within 3 years. (Period of 3 years is calculated from the end of the financial year in which loan is taken). This period of 3 years has been extended to 5 years starting 1st April 2016.

Note that interest deduction can be claimed starting the financial year in which construction of the property is complete.

Availability of deduction under different sections of the Income Tax Act in respect of Interest on Home Loan

Section 24(b): Deduction of interest on loan taken for property is allowed as deduction (on accrual basis). However, in case of self occupied property there is a limit of Rs. 2,00,000/-.

Section 80 C: Deduction of maximum of Rs. 1,50,000/- is allowed as deduction (on paid basis). It is important to note that limit of Rs. 1,50,000/- includes other expense/ investments. For example, if LIC premium paid is Rs. 50,000 and interest on loan is Rs. 1,60.000/- then total of Rs. 1,50,000/- will be available under this head. However, if such property in respect of which loan is taken is sold within 5 years then such deduction shall be treated as income of that previous year.

Section 80EE: Deduction of Rs. 50,000/- is available (subject to above conditions).

Note: Either deduction under section 24 or section 80C in respect of interest is available but deduction under section 80EE is available in addition to it.

Therefore, it is advisable to claim deduction in respect of interest under the head House Property i.e. under section 24 as amount of available deduction is more and there is no restriction on sale of house property.

Now, Let’s discuss computation of Income under the head House Property with help of examples

Example: Mr. Rahul owns a house, Municipal value of which is Rs. 80,000, Fair Rental Value is Rs. 90,000 and Standard Rent is Rs. 70,000. He has taken a home loan for constructed house property and is paying Rs. 2,50,000 as yearly interest. He is having a business income of 80,000 during previous year.

Here in this case, the Computation of his total income will be as under:

| Gross Annual Value | Nil | |

| Less | Municipal Taxes | Nil |

| Net Annual Value | Nil | |

| Less | Standard Deduction | Nil |

| Interest on borrowed Capital | (2,00,000) | |

| Loss under the head House Property | (2,00,000) | |

| Add | Income under the head Business or Profession | 80,000 |

| Gross Total Income | (1,20,000) |

Example: Mr. Rahul owns a house, Municipal value of which is Rs. 80,000, Fair Rental Value is Rs. 90,000, Standard Rent is Rs. 70,000, The property was let out for Rs. 10,000 p.m. Municipal taxes was 10%. He has taken a home loan for constructed house property and is paying Rs. 40,000 as yearly interest. He is having a business income of 80,000 during previous year.

| Gross Annual Value | 120000 | |

| Less | Municipal Taxes | 8000 |

| Net Annual Value | 112000 | |

| Less | Standard Deduction (30%) | 33600 |

| Interest on borrowed Capital | 40000 | |

| Income under the head House Property | 38400 | |

| Add | Income under the head Business or Profession | 80000 |

| Gross Total Income |

118400 |

Section 80EE does not speak about take over of loan. Is it necessary that you have to take a fresh loan for acquisition of new house or can we switch over the bank in the financial year 2016-17