1st of February, 2018, notified as the date of coming into force of E-Way Bill Rules vide Notification No. 74/2017-Central Tax dated 29.12.2017

The E-Way Bill Rules 138 & 138A notified, vide Notfn No. 27/2017-Central Tax dated 30.08.2017, will now come into force with effect from 01.02.2018 (Notification No. 74/2017- Central Tax dated 29.12.2017)

E-Way Bill Mechanism

- The rules for implementation of nationwide e-way Bill system for inter-State movement of goods on a compulsory basis notified with effect from 1st February, 2018. This will bring uniformity across the States for seamless inter-State movement of goods.

- While the system for both inter-State and intra- State e-way Bill generation will be ready by 16th January, 2018, the States may choose their own timings for implementation of e-way Bill for intra- State movement of goods on any date before 1st June, 2018.

- In any case, uniform system of e-way Bill for inter-State as well as intra- State movement will be implemented across the country by 1st June, 2018.

- Four States- Karnataka, Uttarakhand, Rajasthan and Kerala have already introduced E-way Bill

Features of E-way Bill Mechanism

- Common Portal for E-Way Bill is http://ewaybill.nic.in

- E-Way bill is complete only when Part-B is entered. Part-B is a must for the Eway bill for movement purpose. Otherwise printout of EWB says it is invalid for movement of goods

- The validity of the e-way bill starts when first entry is made in Part-B. That is, vehicle entry is made first time in case of road transportation or first transport document number entry in case of rail/air/ship transportation, whichever is the first entry.

- It may be noted that validity is not re-calculated for subsequent entries in Part-B.

- One e-way bill can go through multiple modes of transportation before reaching the destination. As per the mode of transportation, the EWB can be updated with new mode of transportation by using ‘Update Vehicle Number’.

- There is a chance that consignee or recipient may reject to take the delivery of consignment due to various reasons. Under such circumstance, the transporter can get one more- way bill generated with the help of supplier or recipient by indicating supply as ‘Sales Return’ and with relevant document details and return the goods to supplier as per his agreement with him.

- “Bill to” and “Ship to” Cases

> Two E-way Bills to be issued

- TRANSIN or Transporter ID?

> TRANSIN is 15 digits unique number generated by EWB system for unregistered transporter once he enrolls on the system. TRANSIN is 15 digits number on similar lines with GSTIN and it is based on state code, PAN and Check digit. This can be shared by transporter to his clients to enter this number while generating e-waybills.

E-Way Bill Format

PART A

- GSTIN of Recipient – GSTIN or URP

- Place of Delivery – PIN Code of Place

- Invoice/Challan No – Number

- Invoice/Challan Date – Date

- Value of Goods –

- HSN Code – At least 2 digit of HSN Code

- Reason for Transport – Supply/Exp/Imp/Job Work/…

- Transporter Doc. No – Document No provided by trans.

PART B

- Vehicle Number – Vehicle Number

Modes of generation of E-way bill

- Mobile (Android and ios) based app is developed for e-way bill operations

- All the activities of e-way bill can be done on this app

- IMEI of the mobile number needs to be registered on the EWB system to use the app

SMS based E-way bill

Operations

- Generate the E-Way Bill

- Update the Vehicle details

- Cancel the E-Way Bill

Pre- requisite

- Registering the mobile number with the GSTIN on the EWB system

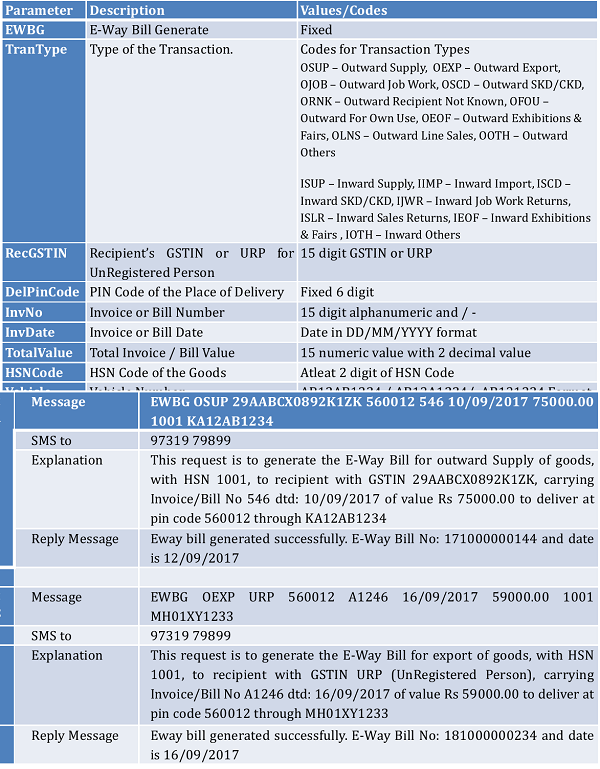

EWBG Tran Type Rec GSTIN DelPinCode Inv No Inv Date Total Value HSN Code Vehicle

Explanation of Parameters

- EWBG – E-WayBill Generate Key Word – It is fixed for generation

- Tran Type – Transaction Type – Refer to the Code list

- RecGSTIN – Recipient’s GSTIN. If it not there, then URP for ‘UnRegistered Person’

- DelPinCode- PIN Code of Place of Delivery of Goods

- Inv No – Invoice or Bill Number of the document of supplier of goods

- Inv Date – Invoice or Bill Date of the document of supplier of goods

- Total Value- Total Value of goods as per Invoice/Bill document in Rs.

- HSN Code – HSN Code of the first Commodity

- Vehicle – Vehicle Number in which the goods is being moved

Message Format

EWBV EWB_NO Vehicle Reas Code

Explanation of Parameters

- EWBV – E-Way Bill Vehicle Updating Key Word – It is fixed for vehicle updation

- EWB No – 12 digits E-Way Bill for which the new vehicle has to be added

- Vehicle – New Vehicle number for the movement of goods

- Reas Code- Reason Code to indicate why the vehicle number is being added.

Example

- EWBV 120023450123 KA12BA1234 BRK

Message Format

EWBG EWB_NO

Explanation of Parameters

- EWBC – E-Way Bill Cancellation Key Word – It is fixed for Cancellation

- EWBNo- 12 digits E-Way Bill Number, which has to be cancelled

Example

- EWBC 120023450123

Every day the following message is sent to all the tax payers who using EWB system

GSTIN: 29AAWPR3924N1ZM: Your E-waybill statistics for : 06/12/2017-GENERATED BY YOU as Outward: 7 (Value Rs. 3584882) ;Rejected by you:1 (Value Rs 28000) ;GENERATED BY OTHER PARTY as outward: 3 (Value Rs. 1872500)

API based EWB Generation

This is site-to-site integration of Tax payer system with EWB system

All the activities of e-way bill can be done on the API system

This can be used by tax payers who generates more than 200- 300 EWB/day

APIs are RESTful Web service based with JSON format

The pre- requisite is Tax Payer systems should have SSL and Static IP

Tax Payer should test on the sandbox before going for production

Same APIs can be used by Suvidha Provider, if the Tax Payer has authorized him.

Benefits of API Interface

No need of double or duplicate entry – one for Invoice generation and other for E-Way Bill

Mistakes are avoided

No need of one more print – Invoice can have EWB No

EWB No can be updated in Tax payer system with related invoice

E-way Bill data to GST System for GSTR-1

Readiness for Form INV – 1 (Invoice Reference Number)

Same API interface can be used in other states with requesting for those GSTIN

- Tax payer enters invoice details in his system

- Tax payer generated Invoice from his system

- Tax payer system calls EWB system through API with relevant information

- EWB system after authentication and verification of information, generates EWB and returns EWB No.

- Tax payer system gets this EWB No. and writes to his database along with EWB No. on the Invoice Copy and moves the goods.

Example – API Interface for Transporter system

- On hourly basis, TRANS system pulls all the ewaybills assigned to him from EWB system

- Before movement of goods, transporter enters vehicle no. for his LR and saves in his system

- Now, TRANS system calls EWB system with EWB No. and other details requesting to update Part B.

- EWB system after authentication and verification of details , updates vehicle details and gives ACK.

- TRANS system updates this ACK and prints the Trip sheet.

- Now, transporter moves the goods.

List of APIs

Officer Activities

Data Exchange with GSTN and States

In Case of Billed to – Shipped to Transaction what is the procedure and who is responsible for generating E-way bill?

Dear Sir,

If I dispatch the goods below 50000/- for Job Work. There will applicable EWAY Bill ?

Kindly describe the Job Work condition

Dear Sir

Need some clarity on the EWay Bill for export . As all export Invoice is made in $ and to calculate the value of threshold limit i.e. Rs.50000.00 How exporter will proceed. Secondly , at the time of generation of E way bill $ may not be accepted since Transportation purpose is only upto the port level.

So there is no detailed clarity on the Eway Bill for export or Import.

Please give detailed guideline.