Imports to India jumped 33.09 percent year-on-year to USD 37.86 billion in May of 2017, boosted by a 236.69 percent increase in gold imports and a 29.54 percent rise in oil. Imports in India averaged 7090.77 USD Million from 1957 until 2017, reaching an all-time high of 45281.90 USD Million in May of 2011 and a record low of 117.40 USD Million in August of 1958.

Having such huge volume of trade, it may be most interesting to analyze the impact of GST on Imports. Let us now study how Imports are effected by implementation of GST.

Imports under Customs Act, 1962

Sec (23) of Customs Act 1962 : “import”, with its grammatical variations and cognate expressions, means bringing into India from a place outside India;

Sec (27) “India” includes the territorial waters of India;

THE TERRITORIAL WATERS, CONTINENTAL SHELF, EXCLUSIVE ECONOMIC ZONE AND OTHER MARITIME ZONES ACT, 1976

5. (1) The contiguous zone of India (hereinafter referred to as the contiguous zone) is and area beyond and adjacent to the territorial waters and the limit of the contiguous zone is the line every point of which is at a distance of twenty-four nautical miles from the nearest point of the baseline.

Section 2 (56) of CGST Act, 2017 defines “ nd a“, which means the territory of India as referred to in article 1 of the Constitution, its territorial waters, seabed and sub-soil underlying such waters, continental shelf, exclusive economic zone or any other maritime zone as referred to in the Territorial Waters, Continental Shelf, Exclusive Economic Zone and other Maritime Zones Act, 1976 (80 of 1976), and the air space above its territory and territorial waters.

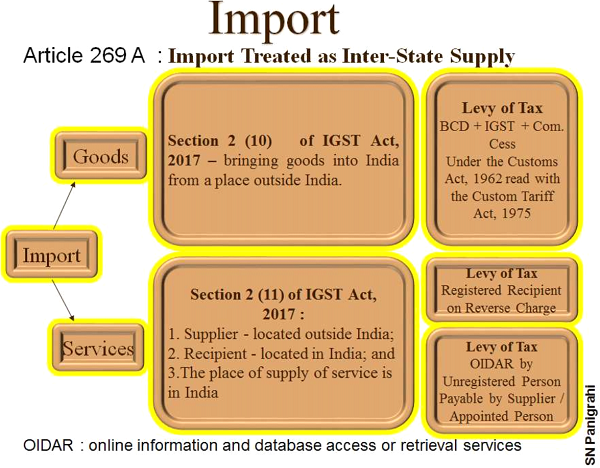

Import Treated as Inter-State Supply:

Section 2 (10) of IGST Act, 2017 defines ± 3LPSRrtIofI RIL Js” with its grammatical variations and cognate expressions, means bringing goods into India from a place outside India.

Under the GST regime, Article 269 A constitutionally mandates that the supply of goods, or of services, or both in the course of import into the territory of India shall be deemed to be supply of goods, or of services, or both in the course of inter-State trade or commerce for levy of integrated tax. So import of goods or services will be treated as deemed inter-State supplies and would be subject to Integrated tax (IGST).

We shall discuss Import of Goods and Import of Services separately as treatment for determining place of supply, time of supply and levy of tax different for goods and services. In this article we shall confine the discussions to Import of Goods only.

Import of Goods :

As per Sec (25) of Customs act, 1962 : “imported goods” means any goods brought into India from a place outside India but does not include goods which have been cleared for home consumption.

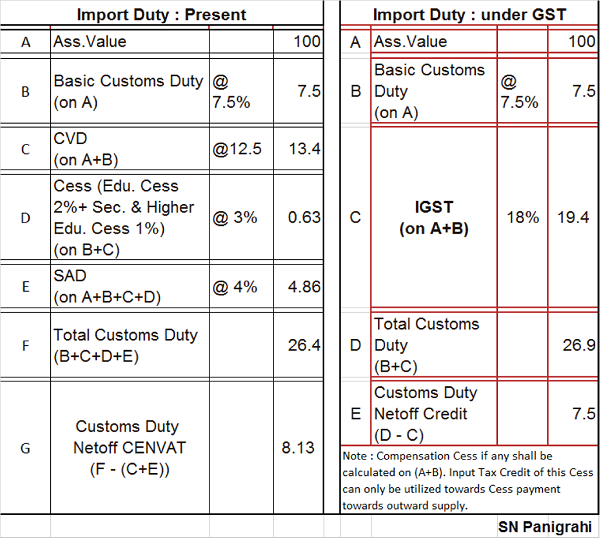

The import of goods has been defined in the IGST Act, 2017 as bringing goods into India from a place outside India. All imports shall be deemed as inter-State supplies and accordingly integrated tax shall be levied in addition to the applicable Custom duties. The IGST Act, 2017 provides that the integrated tax on goods imported into India shall be levied and collected in accordance with the provisions of the Customs Tariff Act, 1975 on the value as determined under the said Act at the point when duties of customs are levied on the said goods under the Customs Act, 1962.

The integrated tax on goods shall be in addition to the applicable Basic Customs Duty (BCD) which is levied as per the Customs Tariff Act. In addition, GST compensation cess, may also be leviable on certain luxury and demerit goods under the Goods and Services Tax (Compensation to States) Cess Act, 2017.

The Customs Tariff Act, 1975 has accordingly been amended to provide for levy of integrated tax and the compensation cess on imported goods. Accordingly, goods which are imported into India shall, in addition to the Basic Customs duty, be liable to integrated tax at such rate as is leviable under the IGST Act, 2017 on a similar article on its supply in India. Further, the value of the goods for the purpose of levying integrated tax shall be, assessable value plus Customs Duty levied under the Act, and any other duty chargeable on the said goods under any law for the time being in force as an addition to, and in the same manner as, a duty of customs.

The value of the imported article for the purpose of levying cess shall be, assessable value plus Basic Customs Duty levied under the Act, and any sum chargeable on the goods under any law for the time being, in force as an addition to, and in the same manner as, a duty of customs. The integrated tax paid shall not be added to the value for the purpose of calculating cess. (Sec 11(2) of the Goods and Services Tax (Compensation to States) Act, 2017

Customs Duty calculation is illustrated below:

Let us see in the below table how Import Duties are worked out.

Customs Warehouse Provisions under GST

The Customs Act, 1962 provides for removal of goods from a customs station to a warehouse without payment of duty. The said Act has been amended to include ‘warehouse’ in the definition of “customs area” (section 2 of the Customs Act, 1962) in order to ensure that an importer would not be required to pay the Integrated tax (IGST) at the time of removal of goods from a customs station to a warehouse.

That means if goods are taken to warehouse from port or customs station – no IGST is applicable

Goods cleared from warehouse, IGST and GST Compensation Cess will payable at the time of removal from warehouse

Other Customs Levies Shall Continue

Other Customs levies as per customs act shall continue. Following duties may continue to be levied as at present:

Basic Customs Duty Levied under Sec 12 of Customs Act 1962

Anti-Dumping Duty Levied under Sec 9A of Customs Tariff Act 1975

Safeguard Duty Levied under Sec 8B of Customs Tariff Act 1975

Classification of Goods:

HSN (Harmonized System Nomenclature) is a multipurpose international product nomenclature developed by the World Customs Organization (WCO).

WCO has 181 members, three-quarters of which are developing countries that are responsible for managing more than 98 percent of world trade. India, a member of WCO since 1971, has been using HSN codes since 1986 to classify commodities for Customs and Central Excise.

HSN standardizes the classification of merchandise under sections, chapters, headings, and subheadings. This results in a six-digit code for a commodity (two digits each representing the chapter, heading, and subheading).

Indian Customs and Central Excise added two more digits to make the codes more precise, resulting in an eight-digit classification.

For the purpose of Imports & Exports, HSN code at 8 digit level would continue under the GST regime.

Input Tax Credit of Integrated Tax:

The definition of “input tax”in relation to a registered person also includes the integrated tax charged on import of goods. Thus, input tax credit of the integrated tax paid at the time of import shall be available to the importer and the same can be utilized by him as Input Tax credit for payment of taxes on his outward supplies. The integrated tax shall, in essence, be a pass-through to that extent. The Basic Customs Duty (BCD), shall however, not be available as input tax credit.

The Input Tax Credit in respect of Compensation Cess on supply of goods and services leviable under Sec 8 shall be utilized only towards payments of said cess on supply and services leviable under the said section (Sec 11(2) of the Goods and Services Tax (Compensation to States) Act, 2017.

As per section 11 of the IGST Act, 2017 the place of supply of goods, imported into India shall be the location of the importer. Thus, if an importer, say is located in Rajasthan, the state tax component of the integrated tax shall accrue to the State of Rajasthan.

At present traders (not registered with Excise) who sells imported goods in India are not eligible to take credit of CVD & SAD (if paid), which is being absorbed as cost. Similarly output service providers importing goods are eligible to take credit of CVD only and not SAD.

However under GST regime, traders will also be able to claim input tax credit of IGST, reducing costs for them further. Output service providers are also can take IGST credit.

GSTIN Replacing IEC

As per Trade Notice No : 9 dated 1 2th June’20 17, of DGFTImporters and Exporters need to declare only GSTIN wherever registered with GSTN (Instead of IEC). This is to facilitate Credit flow of IGST, on imports and refund or rebate of IGST related to Exports. However, those who are not registered with GSTN (Turnover is less than threshold limit of Rs 20 Lakhs (Rs 10 Lakhs for Special Category States) and not falling under compulsory registration under Sec 24 of CGST Act. 2017), PAN of the entity shall be used. Further, for the existing IEC holders, necessary changes in the system are being carried out in the DGFT so that their PAN becomes their IEC. DGFT System will undertake this migration, and the existing IEC holders are not required to undertake any additional exercise in this regard.

IEC holders are required to quote their PAN (in place of existing IEC) in all their future documentation w.e.f. the notified date. The legacy data which is based on IEC would be converted into PAN based in due course of time.

Declaration of valid GSTIN in Customs Documents (BE/SB)

Declaration of valid GSTIN in Customs documents (BE/SB) would be mandatory w.e.f. 0000 hrs of 01-07-2017, the likely implementation date of GST, to avail IGST credit on Imports or GST refund on exports. The declared GSTIN would be validated for correct IEC/ PAN linkage.

Accordingly, during GSTIN registration, please ensure declaration of correct IEC and the same PAN [earlier registered with DGFT for getting IEC]. In case of any difference in PAN declared for GSTIN vis-à-vis the PAN declared for IEC registration, amendment of PAN in IEC may be undertaken immediately.

Author Bio

I am exporter of jute bags,exports with payment of tax but not paying anything it adjusting from my credit ledger,and i am getting refund from ICEGATE, my question is

1.Every exporter must take LUT ?

2.What i am filling my return is correct procedure ?

Please explain Clarify my doubts any one

Dear Sir,

Our all import Gst is not appearing in form 2A in the GST portal to avail GST input credit.

As per the govt new rules, we can only claim GST 2A appearing GST input credit only so this is a very important activity for us otherwise we are going to lose heavily un claimable.

We are not aware of this procedure also. Therefore please check and let me know.

Sir,

In GSTR3B Where we have to show exempted import of supplies.

valuable information Thank you

Hello Sir,

I am Importer, now i am pay additional duty on import with charge GST, so i take credit this.

its not mention on BOE. ye duty goods relief krte time lagai thi. or uske uper GST bhi charge kiya h. to mujhe uska credit milega ?

Our company import services from foreign party and paid after filling Form 15CA Rs 120/- , treated as our Import purchase value. Rs 120/-. We sale this services @ IGST 18% (150+27)=Rs 177.Output IGST is Rs 27/-. How I calculate or claim ITC of this Import Purchase?

Dear Mr Panigrahy,

Please clarify whether ARE 3 form has been discontinued post GST.

we have paid our employee education fee to outside of india, this is will under GST. or what is % or this is taken RCM method how much % IGST paid, and tis will be eligible for ITC, please advice.

Dear sir,

We are importer, we have received goods from outside india. And we have pay our IGST @ 5% on that value. And we have taken ITC claim on our GST3B on july. But still am not received my ITC claim under GSTR2A(auto). How to claim this ITC, and please give us solution. Am awaiting for your favorable reply

IMPORT PURCHASE IN JUN-2017 BUT MATERIAL RECEIVED IN JUL-2017 NOW HOW TAKE DUTY IN TRANS-1

Hello sir my doubt is,

If i import goods for value of 100 + 10% custom duty, + gst 28 %=100+10+ 31 gst= 141₹.total.

If i sell to wholesaler should only add my profit as 10 rs =151₹. Or i again have to add gst 28%=

151+28%=193. Pls clear me this. Is every i i port i pay tax than again while selling i have to add tax. Or 151 is is inclusive gst and final invoice total 151 ok.

Sir, please share

IMPORT DUTY EXCEL CALCULATOR FOR MACHINE TOOLS & ACCESSORIES

the imported material received in july after roll out of GST but the firm filed er1 return showed trasferable ITC into GST scheme . how they taken credit of basic ex.duty/SAD in to gst as the b/e not showing igst/gst . can the extra credit indicated in trans-1 or credit to be taken in july in gst

If Manufacture is self-importer, Manufacture imports the raw material. Whether he can take ITC of customs duty.

And manufacture purchase the raw material from the importer. In this case, also he can take ITC.

Kindly reply.

Good Information Ji & I request for Hotel Industry:

1. Whether we can take input credit on import under EPCG Scheme- Room Furniture, Hotel supplies, furnitures, stationery etc.,

2. Whether we can take input credit on import – Room Furniture, Hotel supplies, furnitures, stationery etc.,

Hello,

As there was no CVD on toys imported from China in India?

Kindly let us know whether a toy trader can take deemed credit u/s 140(3)?

i bought goods from USA and reached to Indian Custom department in 28 june 2017, due to documentation of custom department i received goods in 4 July . now my question is that i pay custom duty and cvd on goods. now i sales that goods in july then can i take benefit of cvd as IGST ?

Very detailed and informative article. Thanks.

We are a distributor of foreign co. for indian territory.

On June 30 we have imported stock. Please advise the portion of paid customs duty available for ITC. Is it CVD+ SAD ?

What will be the custom duty rate on importing Protein supplements as before GST implementation it was 42%.

Whether credit of igst will be claim if goods sale from port after filing of bill of entry if importer is reg in other state

Dear Sir,

First of all, your above article is very good and useful one.

What are the changes in High Sea Sale under GST ?

It is understood that IGST has to be raised in High sea sale invoice by the supplier and the buyer has to be pay IGST along with BCD. In such case, it will become double taxation.

Kindly clarify.

Regards,

T G SARAVANAN

Does import duty is going to come down on textile fabric. Before GST regime import duty was 29.5% constituting 10 % as BCD apart from CVD and other cess. Now polyester fabric can be imported at 10 % BCD and 5 % IGST. This way important will be cheaper by 14%.

Local textile industry is going to be hit or shut down.What will happen to MAKE IN INDIA.china polyester fabric will be cheaper.

Please clarify

I have an import consignment for which I have filed Bill of entry and also paid the required custom duty, ten days back ( when the IGM was filed). However, the container is still in transit and has not reached its destination port. As it is clear, that the container will reach the port only after 1st July 2017 ( in the GST regime), I will have to charge the GST rate on the Tax invoice of the material. Can I claim the input credit for the paid custom duty, as the delay is not from my side, but the transit delay. Please advice on the same.

Valuable information

Dear Sir,

We are the Importer and Want to know same HSN code used further as same in Bill of entry used by Custom Officers at Port , at the time of goods clearance…………

Please advice ………

Best Regards

Prakash

How IGST on import will be paid….is it on RCM basis???

Best Article so far seen.

Very informative!!!

Good information. Thanks SN Panigrahi sir