The pharmaceutical industry is an important component of health care systems throughout the world. It is comprised of many public and private organizations that discover, develop, manufacture and market medicines for human and animal health.

The pharmaceutical industry is based primarily upon the scientific research and development (R&D) of medicines that prevent or treat diseases and disorders. Drug substances exhibit a wide range of pharmacological activity and toxicological properties. Modern scientific and technological advances are accelerating the discovery and development of innovative pharmaceuticals with improved therapeutic activity and reduced side effects.

“Drugs and Medicines “basically comes under pharmaceutical sector which is the third largest in the world in terms of volume and 14th in terms of the value. Under the prior indirect tax regime, this industry was faced with a multiplicity of taxes such as excise duty, service tax as well as different state VATs in addition to CST on inter- state transactions. Pharmaceutical as an industry had always been the subject matter of litigation in the prior indirect tax regime. Given that GST is at its nascent stages and the law is yet to fully shape up, it is anticipated that there would be much litigation in the current indirect tax regime as well. In this segment, we have broadly analyzed the GST impact on Expiration of drugs

Drugs and medicines are classified as goods in GST as it involves selling of drugs and medicines from one to another in a systematic chain i.e. Manufacturer sells to Wholesaler and wholesaler to retailer on an Invoice/bill of supply. Such goods have a defined life term which is normally referred to as the date of expiry. Goods which have crossed their date of expiry are returned back to the manufacturer, on account of expiry, through the supply chain.

Expiration of Drugs

In the Pharmaceutical industry or sector, medicine has a defined term of validity and the date of validity is printed on the medicine cover. It is mandatory on part of every medicine retailer to return the expired medicine to the manufacturer. Expired medicine has no value and importance in the Indian Pharmaceutical industry. Moreover, it is prohibited to sale expired medicine in India.

Return of Time Expired Drugs – Considered as Fresh Supply

There can be three scenarios if goods are returned by the wholesaler or retailer:

> Goods are being returned by a registered person

> Goods are being returned by a composition dealer

>Goods are being returned by an unregistered person

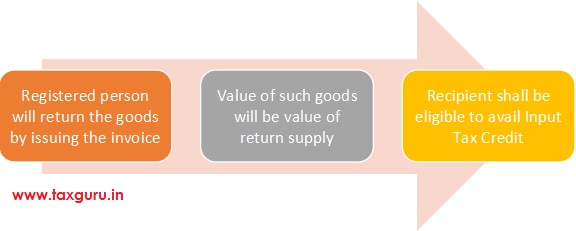

A. Registered Person

Registered person may at his option return the said goods by treating it is as a fresh supply and thereby issuing an invoice for the same. The value of the said goods as shown in the invoice on the basis of which the goods were supplied earlier may be taken as the value of such return supply. The wholesaler or manufacturer, as the case may be, who is the recipient of such return supply, shall be eligible to avail Input Tax Credit of the tax levied on the said return supply subject to the fulfilment of the conditions specified in Section 16 of the CGST Act.

B. Composition Taxpayer

Composition taxpayer may return the goods by issuing a bill of supply and pay tax at the rate applicable to a composition taxpayer. There will not be any availability of ITC to the recipient of return supply.

C. Unregistered Person

Unregistered person may return the expired goods by issuing any commercial document without charging any tax on the same.

Destruction of Expired Medicine

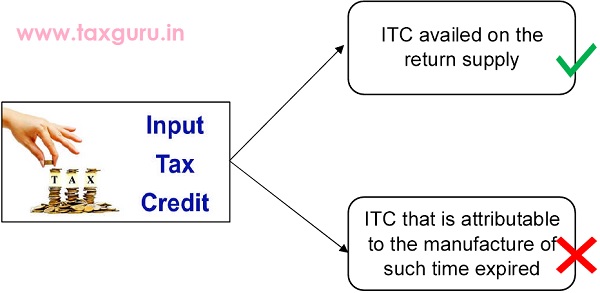

Manufacturer is required to reverse the ITC availed on the return supply as per the provisions of Section 17(5) of the CGST Act, 2017 if the time expired goods which have been returned by the retailer/wholesaler are destroyed by him. The ITC which is required to be reversed in such scenario is the ITC availed on the return supply and not the ITC that is attributable to the manufacture of such time expired goods.

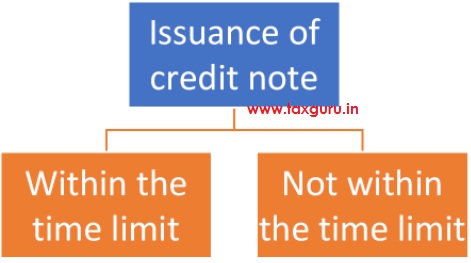

Return of time expired goods- Issuance of Credit Notes

The supplier can issue a credit note where the goods are returned back by the recipient as per Section 34(1) of CGST Act, 2017. The manufacturer or the wholesaler who has supplied the goods to the wholesaler or retailer, as the case may be, has the option to issue a credit note in relation to the time expired goods returned by the wholesaler or retailer. The retailer or wholesaler may return the time expired goods by issuing a delivery challan. The time expired goods, which have been returned by the retailer/wholesaler, are destroyed by the manufacturer, he/she is required to reverse the ITC attributable to the manufacture of such goods.

Situation I: Credit note is issued within the time limit

- Tax liability may be adjusted by the supplier

- Condition:

- The person returning the time expired goods has not availed the ITC, or

- The person has reversed the ITC, if availed

Situation II: Credit note is not issued within the time limit

- Tax liability cannot be adjusted by him

- No requirement to declare such credit note on the common portal by the supplier as tax liability cannot be adjusted

Conclusion

Under the GST regime, seamless availability of input tax credit even on inter-state transactions makes it possible for many companies to employ a hub and spoke mode. The thrust that GST gives to supply chain coincides with the move that pharmaceutical companies are making to continuous manufacturing and industrial automation. Thus, the supply chain aspects should be looked at a serious cost optimization exercise that would further enhance competitiveness of the businesses.

Time limit for credit note is six months from the end of the financial year or the date of filing the annual return, whichever is earlier. but expiry of the drug is two year from the date of manufacturing/invoice.

Please advise to settled ITC.

In the recent meeting in September month Input on return has been dealt with and now you can avail input on such returns as well!