The August 2023 edition of the GST Council Newsletter offers a comprehensive overview of India’s Goods and Services Tax (GST) landscape. Chaired by Hon’ble Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman, the 51st GST Council Meeting yielded crucial amendments to the CGST Act, IGST Act, and Schedule III of CGST Act, 2017, bringing clarity to the taxation of supplies in sectors like casinos, horse racing, and online gaming. Additionally, it unveils remarkable insights into August’s GST revenue collection, boasting an impressive 11% year-on-year growth, with a specific focus on domestic and international transactions. The newsletter also delves into significant notifications, encompassing special procedures for electronic commerce operators (ECOs), CGST Rules amendments, and extensions of due dates for GST returns. Informative circulars clarify GST rates, goods classification, and the applicability of GST on specific services, while portal updates introduce electronic credit reversal and reclaimed statements. Alongside this, it provides insights into best practices at the state level, in-house activities at the GST Council Secretariat, and legal principles shaping the judicial system, making it your indispensable guide to the ever-evolving world of GST.

Recommendations of 51st GST Council Meeting

GST Council recommended certain amendments in CGST Act, 2017 and IGST, Act 2017, including amendment in Schedule III of CGST Act, 2017, to provide clarity on taxation of supplies in casinos, horse racing and online gaming

The 51st GST Council met under the Chairpersonship of Hon’ble Union Minister for Finance & Corporate Affairs Smt. Nirmala Sitharaman via video conferencing in New Delhi on 02.08.2023. The meeting was also attended by Union Minister of State for Finance Shri Pankaj Chaudhary besides Finance Ministers of States & UTs (with legislature) and senior officers of the Ministry of Finance & States/ UTs.

The GST Council in the 50th meeting held on 11.07.2023 had deliberated on the Second Report of the Group of Ministers (GoM) on Casinos, Race Courses and Online Gaming and had recommended that the actionable claims supplied in Casinos, Horse racing and Online gaming may be taxed at the rate of 28% on full face value, irrespective of whether the activities are a game of skill or chance. The Council had also recommended that the law may be amended to provide clarity in the matter.

Accordingly, the GST Council in its 51st meeting recommended certain amendments in the CGST Act, 2017 and IGST Act, 2017, including amendment in Schedule III of CGST Act, 2017, to provide clarity on the taxation of supplies in casinos, horse racing and online gaming. The Council also recommended to insert a specific provision in IGST Act, 2017 to provide for liability to pay GST on the supply of online money gaming by a supplier located outside India to a person in India, for single registration in India for the said supplier through a simplified registration scheme and also for blocking of access by the public to any information generated, transmitted, received or hosted in any computer resource used for supply of online money gaming by such supplier in case of failure to comply with provisions of registration and payment of tax.

The Council also recommended that valuation of supply of online gaming and actionable claims in casinos may be done based on the amount paid or payable to or deposited with the supplier, by or on behalf of the player (excluding the amount entered into games/ bets out of winnings of previous games/ bets) and not on the total value of each bet placed. The Council recommended that CGST Rules, 2017 may be amended to insert specific provisions for valuation of supply of online gaming and supply of actionable claims in casino accordingly. The Council also recommended issuance of certain notifications/ amendment in notification related to the issue.

It was also decided by the Council that effort will be made to complete the process of making amendments in the Act at the earliest and bring the amendments into effect from 01.10.2023.

Source: PIB Press Release dated 02.08.2023

GST Revenue Collection

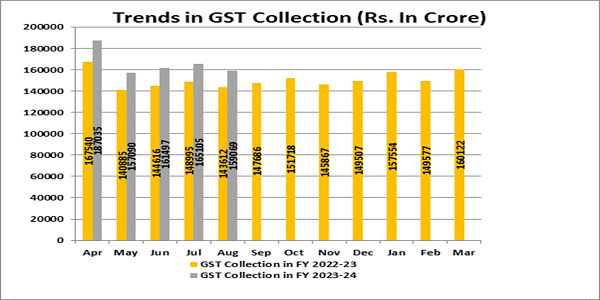

₹1,59,069 crore gross GST revenue collected during August 2023; records 11% Year-on-Year growth. GST Revenues from domestic transactions (including import of services) are 14% higher Year-on-Year

The gross GST revenue collected in the month of August, 2023 is ₹1,59,069 crore of which CGST is ₹28,328 crore, SGST is ₹35,794 crore, IGST is ₹83,251 crore (including ₹43,550 crore collected on import of goods) and Cess is ₹11,695 crore (including ₹1,016 crore collected on import of goods).

The government has settled ₹37,581 crore to CGST and ₹31,408 crore to SGST from IGST. The total revenue of Centre and the States in the month of August, 2023 after regular settlement is ₹65,909 crore for CGST and ₹67,202 crore for the SGST.

The revenues for the month of August, 2023 are 11% higher than the GST revenues in the same month last year. During the month, revenue from import of goods was 3% higher and the revenues from domestic transactions (including import of services) are 14% higher than the revenues from these sources during the same month last year.

The chart below shows trends in monthly gross GST revenues during the current year.

Notifications

> Notification No. 36/2023 – Central Tax dated 04.08.2023, issued to notify special procedure to be followed by the electronic commerce operators (ECOs) in respect of supplies of goods through them by composition taxpayers

The Central Government vide the said Notification outlines that ECOs are now required to follow a special procedure for goods supplied through them by composition taxpayers under Section 10 of the CGST Act, 2017. Key aspects of this special procedure include barring inter-state supply of goods through ECOs, collection of tax at source by the ECOs, and mandatory furnishing of supply details through FORM GSTR-8 on the common portal. It will come into force with effect from 01.10.2023.

> Notification No. 37/2023 – Central Tax dated 04.08.2023 issued to notify special procedure to be followed by the electronic commerce operators (ECOs) in respect of supplies of goods through them by unregistered persons

The Central Government vide the said Notification outlines that ECOs are now required to follow a special procedure for goods supplied through them by the persons exempted from obtaining registration. The ECOs shall allow the supply of goods through it by unregistered persons only if enrolment number has been allotted on the common portal to them. Key aspects of this special procedure include barring inter-state supply of goods through ECOs, collection of tax at source by the ECOs, and mandatory furnishing of supply details through FORM GSTR-8 on the common portal. It will come into force with effect from 01.10.2023.

> Notification No. 38/2023 – Central Tax dated 04.08.2023 issued to make amendments (Second Amendment, 2023) to the CGST Rules, 2017

The Central Government vide the said Notification issued CGST (Second Amendment) Rules, 2023 for implementation of recommendations of GST Council. The amendments include:

1. Rule 9: Under this amendment, the phrase “in the presence of the said person” has been eliminated from Rule 9 of the CGST Rules. This change affects the procedure for verification of the registration of taxable persons under the Act, making the registration process more efficient and less reliant on physical presence.

2. Rule 10A: Rule 10A now prescribes a new deadline for submitting information related to bank account details. As per the amendment, this information must be furnished “within a period of thirty days from the date of grant of registration, or before furnishing the details of outward supplies of goods or services or both”.

3. Rule 21A: Rule 21A underwent substantial modifications primarily designed to deal with violations of the Act or the rules. Such contraventions can lead to the potential cancellation or suspension of the registration of the concerned person.

4. Rule 23: It extends the period permitted for filing an application for the revocation of the cancellation of registration to a total period of 270 days from the date of the service of the order of cancellation of registration.

5. Rule 25: The Amendment substituted Rule 25, which clearly defines the procedures and timelines for the physical verification of business premises in specific scenarios.

6. Rule 43: The value of exempt supply has been modified for the purpose of reversal of common ITC.

7. Rule 46: Rule 46 has been simplified. In the clause (f) for the words “name and address of the recipient along with its PIN code and the name of the State and the said address shall be deemed to be the address on record of the recipient”, the following words “name of the state of the recipient and the same shall be deemed to be the address on record of the recipient” has been substituted.

8. Rule 59: It contains two new clauses related to restrictions on providing the details of outward supplies under certain situations. This amendment ensures that businesses follow appropriate procedures when declaring outward supplies.

9. Rule 64: For the words “person in India other than”, the words “non-taxable online recipient referred to in section 14 of the Integrated Goods and Services Tax Act, 2017 (13 of 2017) or to” has been substituted.

10. Rule 67: Rule 67 has been amended to align it with the GSTN portal.

11. Introduction of New Rule 88D: A New Rule 88D, has been introduced to deal with the difference in input tax credit as per the auto-generated statement and that availed in the return.

12. Rule 89: The clause (k) to sub-rule (2) has been amended to include interest, if any, or any other amount paid in addition to details of the amount of claim on account of excess payment of tax while submitting the statement along with refund application.

13. Rule 96: In sub-rule (2) to Rule 96 of the CGST Rules, 2017, both the provisos has been omitted, to align the refund of IGST paid on export with the GSTN portal mechanism.

14. Rule 108: Rule 108 has been amended to include proviso regarding the manual filing of appeal to the Appellate Authority in FORM GST APL-01, along with the relevant documents only in exceptional situation as mentioned in the Rule.

15. Rule 109: Rule 109 has been amended to include proviso regarding the manual filing of appeal to the Appellate Authority in FORM GST APL-03, along with the relevant documents only in exceptional situation as mentioned in the Rule.

16. Introduction of New Rule 138F: A new rule, 138F, has been introduced for information to be furnished in case of intra-State movement of gold, precious stones, etc. and generation of e-way bills thereof.

17. Introduction of New Rule 142B: A New Rule 142B, has been introduced regarding intimation of certain amounts liable to be recovered under Section 79 of the Act.

18. Rule 162: A sub-rule 3A has been inserted specifying the compounding amount specific to each of the offences under Section 132 as per the table provided in the said sub-rule 3A, which shall come in effect from 01.10.2023.

19: Introduction of New Rule 163: A New Rule 163, has been introduced regarding Consent based sharing of information, which shall come in effect from 01.10.2023.

Additionally, new forms, FORM GST DRC-01C and FORM GST DRC-01D have been introduced. Several existing forms, FORM GSTR-3A, GSTR-5A, GSTR-8, GSTR-9, GSTR-9C, and GST RFD-01, have also been changed notably.

> Notification No. 39/2023 – Central Tax dated 17.08.2023 issued to amend Notification No. 02/2017-Central Tax dated 19.06.2017

The Central Government vide the said Notification has made amendments to the earlier Notification No. 02/2017-Central Tax dated 19.06.2017. The amendments primarily affect the territorial jurisdiction and tax implications in specific regions. These alterations take effect from 04.04.2022.

> Notification No. 40/2023 – Central Tax dated 17.08.2023 issued to appoint common adjudicating authority in respect of show cause notice issued in favour of M/s United Spirits Ltd

The Central Government vide the said Notification appointed a common adjudicating authority for a specific case involving M/s United Spirits Ltd.

> Notification No. 41/2023 – Central Tax, Notification No. 42/2023 – Central Tax and Notification No. 44/2023 – Central Tax dated 25.08.2023 issued to extend the due date for furnishing FORM GSTR-1, FORM GSTR-3B and FORM GSTR-7 for April, May, June and July, 2023 for registered persons whose principal place of business is in the State of Manipur

The Central Government vide the said Notifications has extended the due date for furnishing FORM GSTR-1, FORM GSTR-3B and FORM GSTR-7 for registered persons whose principal place of business is in the State of Manipur for the tax periods April, May, June and July, 2023 till twenty fifth day of August, 2023.

> Notification No. 43/2023 – Central Tax dated 25.08.2023 issued to extend the due date for furnishing FORM GSTR-3B for quarter ending June, 2023 for registered persons whose principal place of business is in the State of Manipur

The Central Government vide the said Notifications has extended the due date for furnishing FORM GSTR-3B for quarter ending June, 2023 for registered persons whose principal place of business is in the State of Manipur for the said tax period till twenty fifth day of August, 2023.

Circulars

Circular No. 200/12/2023-GST dated 01.08.2023 issued clarification regarding GST rates and classification of certain goods based on the recommendations of the GST Council in its 50th meeting held on 11.07.2023

The Central Government vide the said Circular, based on the recommendations of the GST Council in its 50th meeting held on 11.07.2023, clarified with reference to GST levy related to the following items:

i Un-fried or un-cooked snack pellets, by whatever name called, manufactured through process of extrusion : Supply of un-cooked/un-fried extruded snack pellets, by whatever name called, falling under CTH 1905 will attract GST rate of 5% vide S. No. 99B of Schedule I of Notification No. 1/2017-Central Tax (Rate), dated the 28.06.2017 with effect from 27.07.2023. Extruded snack pellets in ready-to-eat form will continue to attract 18% GST under S. No. 16 of Schedule III of Notification No. 1/2017-Central Tax (Rate), dated the 28.06.2017. Also, GST rate on the un-fried or un-cooked snack pellets, by whatever name called, manufactured through process of extrusion, the issue for past period up to 27.07.2023 is hereby regularized on “as is” basis.

ii. Fish Soluble Paste: GST on fish soluble paste, falling under CTH 2309, has been reduced to 5%. Accordingly, the rate has been notified vide S. No. 108A with effect from 27.07.2023. Also, the issue for past period up to 27.07.2023 is regularized on “as is” basis.

iii. Desiccated coconut: The issue relating to GST on the desiccated coconut, falling under CTH 0801 is regularized on “as is” basis for past period from 01.07.2017 up to and inclusive of 27.07.2017.

iv. Biomass briquettes: The issue related to GST on the Biomass briquettes, falling under any Chapter is regularized on “as is” basis for past period from 01.07.2017 up to and inclusive of 12.10.2017.

v. Imitation zari thread or yarn known by any name in trade parlance: GST on imitation zari thread or yarn known by any name in trade parlance has been reduced from 12% to 5%. Accordingly, the rate has been notified vide S. No. 218AA with effect from 27.07.2023. Also, the issue for past period up to 27.07.2023 is regularized on “as is” basis.

vi. Supply of raw cotton by agriculturist to cooperatives: It is clarified that supply of raw cotton, including kala cotton, from agriculturists to cooperatives is a taxable supply and such supply of raw cotton by agriculturist to the cooperatives (being a registered person) attracts 5% GST on reverse charge basis under Notification No. 43/2017- Central Tax (Rate) dated 14.11.2017. Also, the issue for the past periods prior to issue of this clarification is regularized on “as is basis”.

vii. Plates, cups made from areca leaves: The issues relating to GST on plates and cups made from areca leaves are regularized on “as is basis” for the period prior to 01.10. 2019.

viii. Goods falling under HSN heading 9021: It is clarified that GST rate on all such goods falling under heading 9021 would attract a GST rate of 5% and in view of prevailing genuine doubts, the issue for the past periods is regularized on “as is basis”. However, it is clarified that no refunds will be granted in cases where GST has already been paid at higher rate of 12%.

> Circular No. 201/13/2023-GST dated 01.08.2023 issued clarifications regarding applicability of GST on certain services

The Central Government vide the said Circular, based on the recommendations of the GST Council in its 50th meeting held on 11.07.2023, clarified the following :

i. Whether services supplied by director of a company in his personal capacity such as renting of immovable property to the company or body corporate are subject to Reverse Charge mechanism: It is clarified that such services are not taxable under RCM. Only those services supplied by director of company or body corporate, which are supplied by him as or in the capacity of director of that company or body corporate shall be taxable under RCM in the hands of the company or body corporate under Notification No. 13/2017-CTR (Sl. No. 6) dated 28.06.2017.

ii. Whether supply of food or beverages in cinema hall is taxable as restaurant service: It is clarified that supply of food or beverages in a cinema hall is taxable as ‘restaurant service’ as long as:

a) the food or beverages are supplied by way of or as part of a service, and

b) supplied independent of the cinema exhibition service.

It is further clarified that where the sale of cinema ticket and supply of food and beverages are clubbed together, and such bundled supply satisfies the test of composite supply, the entire supply will attract GST at the rate applicable to service of exhibition of cinema, the principal supply.

GST Portal Updates

> Advisory on e-invoice – Services Offered by the Four New IRPs

The details of the four new IRPs regarding the services offered in respect of e-invoices has been provided. To access the detailed advisory, please follow the link below:

https://tutorial.gst.gov.in/downloads/news/e_invoice_services_offered_by_the_new_irps_updated_irps_final_1Aug2023.pdf

Portal update on 02.08.2023

> Advisory: Mera Bill Mera Adhikaar Scheme

As per the direction from the Government, the GSTN has developed and launched a mobile application (available on iOS and Android platforms) and also a web portal for the “Mera Bill Mera Adhikaar” scheme. This scheme will be implemented from 01.09.2023 initially in the States of Gujarat, Assam, Haryana and UTs of Puducherry and Daman & Diu and Dadra & Nagar Haveli, as per the policy decision of the Government.

Mobile Application and Web Portal:

The mobile application is available for download on both iOS and Android platforms and links are given below.

a. Android Link: https://play.google.com/store/apps/details?id=com.gstn.msma

b. iOS Link: https://apps.apple.com/in/app/mera-bill-mera-adhikaar/id6450875616

c. The web portal can be accessed at: https://web.merabill.gst.gov.in

User Manual: For ease of use and to guide taxpayers through the process of participating in the scheme via the mobile application or web portal, a detailed user manual is available at the link below for your reference:

User Manual Download Link:

https://tutorial.gst.gov.in/downloads/news/mbma_user_manual_18_august_2023_final.pdf

Please ensure that you download the mobile application only from the Google Play store and Apple App store and access the web portal through the official link provided above to avoid any spurious application of a fraudulent entity. Please refer to the Policy Document for MBMA related policy matters with reference to broad guidelines for its implementation.

Portal update on 24.08.2023

> Advisory for applicants where GST Registration application marked for Biometric-based Aadhaar Authentication

Rule 8 of CGST Rules, 2017 had been amended to provide that those applicants who had opted for authentication of Aadhaar number and identified on the common portal, based on data analysis and risk parameters, shall be placed for biometric-based Aadhaar authentication and taking photograph(s) of the applicant.

Pilot for implementation of the above change is ready and the functionality is ready for roll out by GSTN portal. This functionality is being launched in Puducherry from 30.08.2023 in the pilot phase. After submission of application in Form GST REG-01 and before generation of ARN, the applicant will either get the message for visiting GST Suvidha Kendra (GSK) or a link on the declared Mobile and Email ID; as may be applicable at TRN stage, based on identification by common portal so that registration process may be completed.

Those applicants who get the link on Mobile & Email ID for Aadhaar Authentication, they can proceed for completing their application as per existing implementation.

However, those applicants who get message for visiting GSK, will be required to visit the designated GSK as conveyed on Mobile/Email and get biometric authentication for all required persons as per the GST Application Form REG-01. The applicants are requested to visit GSK before the TRN expiry date as detailed in Email for Biometric-based Aadhaar Authentication process. In this case, Application Reference Number (ARN) will be generated only after the completion of Biometric-based Aadhaar Authentication process

The days of operation of GSK would be as advised by the administration in respective states

Portal update on 28.08.2023

Introducing Electronic Credit Reversal and Reclaimed statement

Vide Notification No. 14/2022 – Central Tax dated 05.07.2022 (read with circular 170/02/2022-GST, dated 06.07.2022), the Government introduced certain changes in Table 4 of Form GSTR-3B so as to enable the taxpayers in reporting correct information regarding ITC availed, ITC reversal, ITC re-claimed and ineligible ITC. The re-claimable ITC earlier reversed in Table 4(B)2 may be subsequently claimed in Table 4(A)5 on fulfilment of necessary conditions. Such reclaimed ITC in Table 4(A)5 also needs to be explicitly reported in Table 4D(1).

In order to facilitate the taxpayers in correct and accurate reporting of ITC reversal and reclaim thereof and to avoid clerical mistakes, a new ledger namely Electronic Credit and Re-claimed Statement is being introduced on the GST portal. This statement will help the taxpayers in tracking of their ITC that has been reversed in Table 4B(2) and thereafter re-claimed in Table 4D(1) and 4A(5) for each return period, starting from August return period.

Portal update on 31.08.2023

State Best Practices

> Substantial growth in collection of goods and services tax in the current fiscal year which is 23.89% more than the national average’ – Jammu & Kashmir

The effective implementation and administration of GST in the Union Territory of Jammu and Kashmir can be credited to the State Taxes department’s innovative practices. They have established Suvidha Kendras and conducted tax awareness campaigns, seminars, and outreach programs. This proactive approach has simplified regulatory compliance, enhancing the ease of doing business. The department focuses on capacity building and adopts a promotional rather than a strictly regulatory approach.

One notable initiative is the issuance of Standard Operating Procedures (SOPs) by the Deputy Commissioner State Taxes Enforcement to assist taxpayers and transporters during adverse weather conditions that disrupt traffic. This measure allows for the extension of e-way bills for stranded vehicles, preventing unnecessary detention. The department has actively reached out to stakeholders, raising awareness through campaigns and distributing informational pamphlets. Their efforts have been applauded by the business community for facilitating smooth goods movement within the UT.

In the Picture above: Glimpses from Review Meeting conducted by Additional Commissioner State Taxes (Adm. & Enf.), Kashmir with State Tax Officers regarding revenue realization, Status of Returns Filing, DRC-03 payments, deliverables etc.

In-House Activities

> 77th Independence Day celebration at GSTCS

The Independence Day was celebrated in the office of GST Council Secretariat (GSTCS) with much patriotic zeal. The GST Council Secretariat came alive with colors and creativity as it organized various Competitions like Painting, essay writing and Poetry writing to mark the occasion. Our talented participants, from staff members to their families, poured their hearts into creating artworks that depicted the spirit of our great nation. With brush strokes that spoke of unity, diversity, and love for India, they showcased their artistic talents with boundless enthusiasm.

On this occasion, Sh. Pankaj Kumar Singh, Additional Secretary addressed the officials of GST Council Secretariat and encouraged everyone to participate effectively in the In-house events. He also appreciated the efforts of the participants. Our heartiest congratulations to all the winners and a big round of applause to every participant for making this event a grand success.

In the Pictures above: Pankaj Kumar Singh, Additional Secretary, GSTCS felicitating the winners and handing out the awards to the winners.

> Capacity Building Session on functioning of BIFA tool organised through Video Conferencing

GST Council Secretariat recently organized an insightful Capacity Building Session via Video Conferencing on 24.08.2023 in collaboration with CCT, Karnataka. The event was designed to shed light on the efficient utilization of the BIFA Tool.

Participants gained a comprehensive understanding of the BIFA Tool, its features, and practical applications. The session provided invaluable real-world insights. A Q&A session allowed participants to seek clarification and guidance on using the BIFA Tool.

In the Picture above: Officers and staff of the GSTCS attending the session conducted by CCT, Karnataka hosted by Additional Secretary and Joint Secretary of GSTCS

Legal Corner

> Ex nudo pacto non oritur action

The Latin maxim “Ex nudo pacto non oritur actio” is a fundamental principle in contract law that states that no action or right of action arises from a mere verbal or informal agreement lacking any legal consideration. In simpler terms, it means that a contract must be supported by valid consideration to be enforceable in a court of law.

For a contract to be legally binding, it must have the following elements:

- Offer and Acceptance: There must be a clear and unequivocal offer from one party, which is then accepted by the other party without any ambiguity or misunderstanding.

- Intention to Create Legal Relations: Both parties must intend to create legal obligations and be bound by the terms of the contract.

- Consideration: There must be valuable consideration exchanged between the parties. Consideration refers to something of value that each party gives or promises to give in exchange for the other’s promise. This could be money, goods, services, or even a promise not to do something that one has the legal right to do.

- Capacity: Both parties must have the legal capacity to enter into a contract. This means they must be of sound mind, of legal age, and not under any undue influence or duress.

- Lawful Object: The purpose or object of the contract must be lawful and not against public policy.

If a contract lacks any of these essential elements, it will be considered a “nudo pacto” or naked agreement, and the parties will not have any legal recourse to enforce it. In such cases, the law will not recognize the agreement as a valid contract, and no rights or remedies can be claimed for its breach.

The principle of “Ex nudo pacto non oritur actio” serves as a safeguard against unscrupulous dealings and encourages parties to be cautious in their agreements. It emphasizes the significance of having legally valid consideration to support the mutual promises made in a contract, ensuring that both parties have something at stake, and thereby promoting fairness and equity in contractual relationships.

> Actus Curiae Neminem Gravabit

The Latin maxim “Actus Curiae Neminem Gravabit” is a legal principle that underscores the idea that the actions of the court should not cause harm or prejudice to any party involved in a legal proceeding. In essence, it emphasizes that the court’s conduct and decisions should be fair, impartial, and just, ensuring that no individual is adversely affected by the court’s actions.

The principle embodies the following key concepts:

- Impartiality: The court must remain neutral and impartial in its proceedings, treating all parties equally before the law. It should not favor one side over another, ensuring a level playing field for all involved.

- Due Process: The principle is closely tied to the concept of due process, which ensures that all parties are given a fair and reasonable opportunity to present their case and defend their rights.

- Preservation of Rights: The court’s actions should not infringe upon the legal rights and privileges of any individual or entity. The court should respect and uphold the rights of all parties involved.

- Consistency and Predictability: The court’s decisions and actions should be consistent and predictable, based on established legal principles and precedents. This promotes confidence in the judicial system and ensures that parties can reasonably anticipate outcomes.

- Equity and Fairness: The principle underscores the importance of fairness and equity in the court’s dealings, aiming to protect the interests of all parties and avoid any unjust consequences.

“Actus Curiae Neminem Gravabit” serves as a guiding principle for the judiciary, reminding judges, magistrates, and court officials to conduct themselves in a manner that upholds justice, respects the rights of all parties, and fosters confidence in the legal system. By adhering to this principle, the court ensures that its actions do not unfairly harm or prejudice any individual or organization involved in the legal process.

Source of Newsletter – https://gstcouncil.gov.in/