1. Introduction: Transportation of goods from one place (of production or origin) to other places for further process or for consumption is normal economic activity. It facilitates trade and industry. The services offered by way of transportation of goods by road are important component of GDP and thus attracted attention of tax gathering arms of the Government. The levy was initially met with lot of objections and countrywide protest by transporters in the erstwhile service tax regime. Government had to device ways to mitigate hardships pointed out by largely un organised sector transport industry and convince the importance of levy of tax in the value added chain. Several exemptions were carved out to heal the wounds of the transport sector. The major breakthrough was achieved by introduction of reverse charge mechanism (RCM) where by GTA were merely to provide details of freight charges and the consignor consignee details. The tax burden was shifted to consignor/ consignee and relief to the transporters as such from payment of tax.

2. GTA meaning: Transportation of goods by road takes place in different facets. Factories may own transport vehicles and use for their transportation. This type of transaction is not covered under GTA. This is a kind of self service. (Some of the self services are covered under GST for levy like HO to branch services etc.,) The issue of Goods Consignment Note (GC note for short) is the main document where in the liability under RCM is fastened. Important to note that nomenclature is not decisive. Any other document may partake the character of GC note ( .. by whatever name called). The nature of transaction in substance will be looked into to fasten the liability. The forward charge of levy with ITC is available to GTA. However most of the GTA service providers opt for RCM method as better and simpler option available to them. Under RCM method the GTA is liable to furnish details of transport services including name of persons liable to pay GST under RCM if such GTA is registered person.

3. Features of GTA services: Although GST Act does not provide definition of GTA, notification 12/2017 dt.28-07-2017 CT(Rate) under para 2(ze) states GTA as follows:

“goods transport agency” means any person who provides service in relation to transport of goods by road and issues consignment note, by whatever name called”

The Consignment note is prescribed under rule 54(3), as Tax Invoice under special circumstances. Section 31 read with rule 46 specify the contents of Tax Invoice that has to be issued by registered service provider. Considering the practical difficulties faced by transport industry special mention is made and some relaxation is provided for compliance to GTA in issue of Tax Invoices under rule 54(3).

4. Importance of GC note: Issue if GC note fastens liability on the GTA service provider. He is considered as Bailee of the goods handed over to him for transport by consignor. It also provides right of lien on goods to recover the freight charges. Normally GTA cover the liability by taking insurance on the goods under general cover.If a consignment note has been issued by the transporter, it implies that the lien (i.e. the right to keep possession of property) of the goods has been handed over to the transporter and that the transporter has now become accountable for the safe delivery of the consignment to the consignee.

COMMISSIONER CENTRAL EXCISE VERSUS M/S KISAN SAHKARI CHINI MILLS LTD. AND ANOTHER-2017 (3) TMI 1786 – ALLAHABAD HIGH COURT held that The term “consignment note” has no magical or technical meaning looking to the very purpose and intent of legislature in the matter.- SLP filed by KISAN was dismissed as reported in 2017 (3) TMI 1786.Hence any document similar to GC note will hold the transporter as GTA service provider unless proved otherwise on facts.

As per Section 161 of Indian Contract Act, 1872 –

“Bailee’s responsibility when goods are not duly returned— if, by the default of the bailee, the goods are not returned, delivered or tendered at the proper time, he is responsible to the bailor for any loss, destruction or deterioration of the goods from that time.”

The Carriers Act, 1865 may also aid in looking at the civil liability of the carriers apart from the contract Act, 1872.

Thus the GC note or look like document distinguishes the GTA services for RCM liability under GST law. The other types of transportation of goods by road services are not covered under GTA, for example full load transport of Coffee beans by planters, Wooden logs out of from forest auction etc., The facts of each case are important to claim exemption as transport of goods otherwise than GTA.

5. Contents of GC note:As per Rule 54(3) of CGST Rule,2017

A consignment note is serially numbered and contains –

a. Name of consignor

b. Name of consignee

c. Registration number of the goods carriage in which the goods are transported

d. Details of the goods, description, quantity, volume.

e. Place of origin

f. Place of destination.

g. GSTIN of person liable to pay GST – consignor, consignee, or the GTA.

h. Other information as mentioned in rule 46 like date of issue, Value of goods, serial number etc.

6. Liability to register under GST:

a. GTA service provider are liable to register in the state under GST if aggregate turnover in a financial year exceed Rs. 20 lakhs.

“Aggregate turnover” shall include all supplies made by the taxable person, whether on his own account or made on behalf of all his principals. Section 2(6) specify aggregate turnover to be computed on all India basic for same Permanent Account Number(PAN). Further Section 24 mandates (i) person making any interstate taxable supply shall obtain compulsory registration (without looking at turnover limits). Registration is required in a state from where supply is made and not where supply is made.

b. Persons who are ONLY engaged in making supplies of taxable services where total tax is payable by recipient of services(RCM) are exempt from registration. Notification no. 5/2017 CT dt:19-06-2017. Please note that this is not applicable for interstate transactions since section 24(i) mandates compulsory registration in case of interstate transactions irrespective of threshold limit. GTA services are largely covered by RCM but they are only to specified persons as per NN 13/2017 CT ( Rate) dt: 28-07-2017 persons under (a)…to..(g). For other persons, RCM is not applicable and GTA has to discharge the tax on forward basis. In such cases exemption from registration is not available. GTA services provided to an individual being not covered under (a)—(g) is a case on hand tagging the liability on the GTA.

c. Turnover u/s Section 2(112) of CGST Act, –

“turnover in State” or “turnover in Union territory” means the aggregate value of all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis) and exempt supplies made within a State or Union territory by a taxable person, exports of goods or services or both and inter-State supplies of goods or services or both made from the State or Union territory by the said taxable person but excludes central tax, State tax, Union territory tax, integrated tax and cess.

d. Practically GTA having interstate transportation are compulsorily registrable u/s 24(i). GTA if only provides services liable to tax under RCM (not liable to pay any GST on its own) is exempt from registration vide Notification No. .5/2017 – Central Tax dt 19-06-2017. This notification is issued under section 23(2) of CGST and exemption is U/S 9(3) of CGST. However, in case of interstate transactions liable for RCM u/s 5(3) of IGST, such notification of exemption from registration is not issued. Hence compulsory registration U/S 24(i) is mandated. Interesting to note that under IGST exemption from registration is granted based of threshold aggregate turnover of Rs.20 Lakhs ( Rs 10 Lakhs for special states) is granted vide notification no. 10/2017 – Integrated Tax dated 13-10-2017.Not referring section 24(i) in this IGST exemption notification is quite surprising.

e. Notification No. 12/2017- Central Tax (Rate) New Delhi, the 28th June, 2017 prescribed NIL rate U/S 11(1) vide entry # 18 read as follows:

TABLE

| Sl. No | Chapter, Section, Heading, Group or Service Code (Tariff) | Description of Services | (per cent.) | Condition |

| (1) | (2) | (3) | (4) | (5) |

| 18 | Heading 9965- | Services by way of transportation of goods-

(a) by road except the services of— (i) a goods transportation agency; (ii) a courier agency; (b) by inland waterways |

NIL | NIL |

Hence transportation of goods by road except GTA and courier are NIL rated i.e EXEMPT supply u/s 2 (47). There is no liability of registration for such service providers.

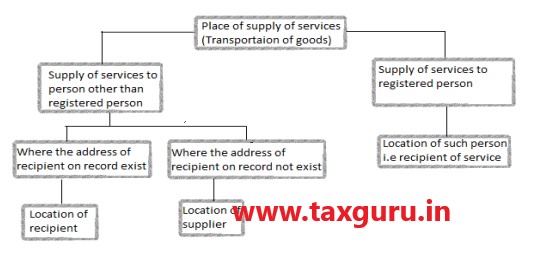

7. Place Of Supply (POS): This aspect has divergent views in certain type of transactions. Consideration and person liable to pay the consideration must be the focal point to decide POS. Transactions with consignor may be in the form of CIF. FOB, ex- factory basis. Further the freight payment may be of To-Pay basis, Paid basis, Periodical billing basis. The consignor and consignee may be same person having separate registrations in different states having branches, factories etc., The deciding factors for determination of POS are summarised as follows:

a. Supplier location–Tamil Nadu

b. Customer location – Karnataka

| Nature | Place of Supply | Consideration | Inter-State/ Intra State | Tax Applicable | |

| Case 1 | On To-Pay basis to customer registered in Bangalore | Supply of service to registered person – POS – is location of such person.

POS – Bangalore |

Paid by Bangalore customer | Inter State | · IGST

|

| Case 2 | On To-Pay basis to a unregistered customer in Bangalore | Supply of service to unregistered person – POS – where goods are handed over

POS – Chennai |

Paid by Bangalore customer | Intra State | · CGST

· TN-SGST |

| Case 3 | On Paid basis to a registered customer in Bangalore | Supply of service to registered person – POS – is location of such person.

POS – Chennai |

Paid by Tamil Nadu customer | Intra State | · CGST

· TN-SGST |

| Case 4 | On paid basis to a unregistered customer in Bangalore | Supply of service to unregistered person– POS – where goods are handed over

POS – Chennai |

Paid by Tamil Nadu customer | Intra State | · CGST

· TN-SGST |

b. *Place of supply determined as per section 12(8) of IGST Act ,2017.

8. Who is liable to pay GST under RCM:

Payment is by sender /consignor Payment is by recipient/consignee

9. Determining POS: ( flow chart)

10. Time of supply:

As per section 13(3) of CGST Act, 2017

In case of supplies in respect of which tax is paid or liable to be paid on reverse charge basis, the time of supply shall be the earlier of the following dates, namely:–

a) the date of payment as entered in the books of account of the recipient or the date on which the payment is debited in his bank account, whichever is earlier; or

b) the date immediately following sixty days from the date of issue of invoice or any other document, by whatever name called, in lieu thereof by the supplier:

Otherwise, the time of supply shall be the date of entry in the books of account of the recipient of supply.

11. Continuous supply of services:

As per section 2(33) of CGST Act,2017

“Continuous supply of services” means a supply of services which is provided, or agreed to be provided, continuously or on recurrent basis, under a contract, for a period exceeding three months with periodic payment obligations and includes supply of such services as the Government may, subject to such conditions, as it may, by notification, specify.”

Invoice in case of continuous supply of services

In case of continuous supply of services, where:

(a) The due date of payment is ascertainable from the contract, the invoice shall be issued on or before the due date of payment.

(b) The due date of payment is not ascertainable from the contract, the invoice shall be issued before or at the time when the supplier of service receives the payment.

(c) The payment is linked to the completion of an event, the invoice shall be issued on or before the date of completion of that event.

12. Levy and collection:

| Description of goods/services | SAC Code | Tax rate

(CGST+SGST) |

Notification No. | Schedule and Sl No. | |

| Goods transport agency | 9967 | 2.5 %+ 2.5 %

(ITC not available) |

11/2017 (CT Rate)

Dt. 28-Jun-2017 |

11 | |

| Or | |||||

| Goods transport agency | 9967 | 6%+6%

(ITC available) |

22/2017 (CT Rate)

dt. 22-08-2017 |

9 | |

13. Exemptions from GST:

As per notification no.12/2017-Central Tax (Rate) dated 28.06.2017 following GTA services are exempt from GST

- Single carriage up to one thousand five hundred rupees

- Single consignee up to rupees seven hundred and fifty

- Agricultural produce

- Milk, salt and food grain including flour, pulses and rice

- Organic manure

- Newspaper or magazines registered with the Registrar of Newspapers

- Relief materials meant for victims of natural or man-made disasters, calamities, accidents or mishap.

- Defence or military equipment

14. Exemption on (sub-contractor) hired vehicles:

As per Notification No.12/17-CT(Rate) dated 20.6.17

– Services by way of giving on hire to a goods transport agency, a means of transportation of goods attracts nill rate.

→ In case the owner of the Vehicle gives his vehicle on Hire to GTA, then the hiring charges are exempt from GST as per below:

Services by way of giving on hire –

(a) to a state transport undertaking, a motor vehicle meant to carry more than twelve passengers; or

(b) to a goods transport agency, a means of transportation of goods (Entry No 22, Heading 9966 / Heading 9973)

15. E way bills:

As per notification no 27/2017 dt 30.08.2017 read with 74 dt 29.12.2017,

E-WAY bill will be effective w.e.f 01.02.2018

As per Rule 138:- Information to be furnished prior to commencement of movement of goods and Generation of e-way bill.-

Every registered person who causes movement of goods of

consignment value exceeding fifty thousand rupees—

(i) in relation to a supply; or

(ii) for reasons other than supply; or

(iii) due to inward supply from an unregistered person shall, before commencement of such movement, furnish information relating to the said goods as specified in Part A of FORM GST EWB-01 and a unique number will be generated on the said portal.

Who can Generate E- Way Bill

- the recipient may generate the e-way bill at portal

- Transporter can also generate the e-way bill except in case of Railway, Ship OR Air

- Any transporter transferring goods from one conveyance to another in the course of transit shall, before such transfer and further movement of goods, update the details of conveyance in the e-way bill on the common portal in FORM GST EWB01(Part-A&B)

- where multiple consignments are intended to be transported in one conveyance, the transporter may indicate the serial number of e-way bills generated in respect of each such consignment electronically on the common portal and a consolidated e-way bill in FORM GST EWB-02 may be generated by him on the said common portal prior to the movement of goods.

→ Validity period of E-way bills can be extended by the generator of the e-way bills either four hours before expiry or within four hours after expiry of E-way bill.

Transactions exempted from e-way bill

E-way bill is optional for: –

1. Goods of value less than Rs. 50,000

2. If Goods are being transported by a non – motorized conveyance

3. where the goods are being transported from the port, airport, air cargo complex and land customs station to an inland container depot or a container freight station for clearance by Customs

4. If the goods are transported within the notified area

5. Goods transported are transit From/ to Nepal/ Bhutan

6. If Goods are transported to a weighbridge within 20kms and back to the place of business by being covered under a Delivery Challan

7. Where Government or local authorities transport goods by rail as a consignor

8. Goods transported are to / from the Ministry of Defence

Non-compliance with e-way bill

Not generating and carrying an e-way bill is considered as non-compliance with the provisions of the GST law and can result in both monetary as well as non-monetary losses to the taxpayer.

Monetary implications

In case goods are moved without generating a valid e-way bill, the authorities may impose a penalty of 10,000 INR or amount of tax sought to be evaded, whichever is higher.

Non-monetary implications

It may also lead to confiscation of goods and the vehicle conveying those goods, in case the person transporting the goods or the owner of goods/conveyance fails to pay the tax and penalty within seven days of detention or seizure.

16. Books of accounts- S 35 read with rule 56 of CGST:

a. Records to be maintained by owner or operator of godown or warehouse and transporters- the transporters, owners or operators of godown, if not already registered under the GST Act(s), shall submit the details regarding their business electronically on the Common Portal in FORM GST ENR-01.A unique enrolment number shall be generated and communicated to them. A person enrolled in any other State or Union territory shall be deemed to be enrolled in the State or Union Territory.

b. Every person engaged in the business of transporting goods shall maintain records of goods transported, delivered and goods stored in transit by him and for each of his branches. Every owner or operator of a warehouse or godown shall maintain books of accounts, with respect to the period for which particular goods remain in the warehouse, including 121 the particulars relating to dispatch, movement, receipt, and disposal of such goods. The goods shall be stored in such manner that they can be identified item wise and owner wise and shall facilitate any physical verification or inspection, if required at any time.

Author Bio

Sir,

Very good article.But one thing is missing,Registration Place of GTA.. That means

Say the case where- Supplier–Tamilnadu, Customer- Karnatak, GTA Registered office- Rajasthan., Freight is Paid by Supplier, Freight is paid by Customer. Then RCM will attract IGST or SGSt & CGST etc.

Hello sir,

Nice article but I have a querry in case of a GTA.

Whether a gta supply 100% to intra state under rcm is eligible to take refund of ITC credit available on purchases made by him in furtherance of his business. Please clarify.

Thanks

Sir,…

Very nice and detailed article.

Query- Regrading location of Service provider in the case of Multiple GST registration of GTA and from which location he should raised invoice i.e from staring location or destination location.

If you can mention any section reference for the same.

Also take both secenrerio i.e inter and intra state movement of goods and fright is paid by consignor or consignee.

Further consignor and consignee both are same entity and have gst registration in both locations.

Thanks in Advance

Rakesh Jain

Sir

Going through your Article on Analysis of GTA, I’d like to get some more clarification from you towards –

1. A Local Transporter who ferries the goods from Supplier to Customer in his own tempo will not be considered as a GTA under chapter heading 9965.

In K M Trans Logistics Private Limited (GST AAR Rajasthan) – Advance Ruling No. RAJ/AAR/2019-20/19 – Date of Judgement/Order : 29/08/2019, where the Transporter had got into an agreement to transport the vehicles from factories to showroom but w/o issuing CN or LR, it was held that the Transporter has to issue a CN or LR otherwise one will not be able to generate the EWB which is requirement at Pt. 8 of Part A.

In this case, if he issues a CN or LR, even if he has is own Transport Vehicles, will he become a GTA Automatically ?

2. You have explained POS with example of Supplier in Chennai (Regd) and Customer in Karnataka.

In case No. 2, where the goods are transported through GTA from Chennai to Banglore (customer being unregistered) and on “To Pay Basis” where the POS is Chennai you have mentioned RCM will be paid in TN under C+S GST.

Who will pay RCM in TN ? – Supplier or GTA ?

If GTA, then is he liable u/s 24(i) – If this is answered in Affirmative, then subsequent queries need not be replied.

If not GTA, then –

a. If it is on TO Pay Basis, then will not the RCM be Paid in Karnataka under C+S GST?

Also, The un-regd customer in Karnataka, if he is falling under the category of persons liable for compulsory regn as per (a) to (g) of the Notification, then he has to get himself regd and pay RCM in Karnataka?

(b) If the un-regd customer is an Individual, then the GTA will have to make payment of GST on Fwd Charge ?

Awaiting your reply in this context.

Thanking you in anticipation.

Ankit B. Shah

Hello sir,

Nice article but i have few questions in mind. Whether a gta supply 100% to intra state under rcm is required to register? Because you are telling that and this is the 1st time I came accross it. So can u give a 100% confirmation of that?.

Also here u haven’t not mentioned anything about filing of gst returns if we are registered. So my question is.

1. If we are registered do i need to charge gst even if the transaction is eligible for rcm and then file normal gst retuns?

2. If we are registered but charge no tax. Then how will we show our transaction in the Gst returns(3b &1).

Please clarify these questions as it is very important for me as i am a GTA too.

Thank you