New Notifications in GST (Notification No. 81/2020 to Notification No. 88/2020-Central Taxes)

TABLE OF CONTENTS:

| Notification No. | Content |

| 81/2020 | Regarding Amendment in Sec. 39 |

| 82/2020 | Regarding New Rules |

| 83/2020 | Due Dates of GSTR -1 |

| 84/2020 | Options for GSTR – 1 |

| 85/2020 | Procedure for GSTR – 3B |

| 86/2020 | Regarding an earlier notification |

| 87/2020 | Regarding Form ITC -04 |

| 88/2020 | Regarding E- Invoicing |

Hello Everyone,

Let us start our discussion on the latest notifications issued by the CBIC on 10th of November 2020 Regarding New Schemes of GST Returns effective from 1st January 2021

To Understand all these notifications, first of all we need to understand section 39 of CGST Act…

SECTION 39 : FURNISHING OF RETURNS UNDER GST LAW

Section – 39 Describes the form and Manner of furnishing of Returns under GST Law. For Simplifi-cation of GST and Compliances, govt. has come up with New scheme of GST Returns and issued certain Notifications for that purpose Let us discuss one by one each and every Notification and develop our understanding……..

NOTIFICATION NO. 81/2020 – CENTRAL TAX :

This Notification Simply Says that All the New provisions (i.e. Amended) of section – 39 (i.e. Furnishing of returns) has been appointed from 10th of November 2020.

Note : – The New provisions which was inserted by Govt. will be discussed in next notifica-tions.

Conclusively we can say that this notification is just related to the date of applicability of Section – 39.

NOTIFICATION NO. 82/2020 – CENTRAL TAX :-

Through this notification govt. has inserted certain rules for implementing New and Simplified GST Compliance Procedure.

Before Discussing these Rules we have to know one important aspect about new and simplified GST Return Procedure. In the New Scheme of GST Returns, GSTR – 3B Return will be auto – populated from the data of GSTR – 1 (Output Details) and GSTR – 2B(Input Details) effective from 1st January 2021 hence, if there is no any change in the data of GSTR-1 filed by us and also filed by our supplier then there is no need to change the auto – populated data of GSTR-3B and if there is any change then we may edit GSTR- 3B. From this procedure the chances of error got reduced.

Now, Let us Discuss the Rule No. 59

RULE NO. 59 :-

Now, we will discuss this rule with the help of certain points.

1. If you have adopted quarterly return filing option, then govt. has given you an facility that you may furnish your January 2021 month GSTR-1 data till 13th February 2021 and also Febru-ary 2021 data till 13th march 2021 through IFF (i.e. Invoice furnishing facility) if your cumu-lative turnover for these two months is up to 50 lakh rs.

2. At the time of march month return you only need to furnish the details of march month , need not to furnish previous months details and you can file your quarterly return.

3. Now next question is that what is the benefit of this facility??

The Answer is that from January 2021, GSTR – 3B data will be auto – populated from your GSTR-1 and if taxpayer has adopted quarterly Return Filing Option then he may furnish his GSTR-1 monthly through IFF facility So, his outward supply will got auto populated in his GSTR-3B and if his supplier is also an quarterly return filer then he may furnish his GSTR-1 through IFF facility and the same has been auto Populated in your GSTR – 2B and GSTR – 3B.

RULE NO. 60 :

This Rule simply talks about the form and manner of ascertaining details of inward supply As per this rule, the details which was submitted by your supplier in his GSTR-1 will be auto – populated in your GSTR-2B From your GSTR – 2B , the same has been auto – populated in your GSTR- 3B.

RULE NO. 61 :

This rule talks about furnishing of GSTR- 3B Return Every Registered taxable person other then a person referred to in section 14 of IGST Act, ISD , Non Resident taxable person or a person paying tax under section 10 or 51 or 52 shall furnish his GSTR – 3B Return in following Manner :-

STATE – I : Chhattisgarh, Madhya Pradesh, Gujarat, Maha-rashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshad-weep.

STATE – II :Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi.

Now, question is that how we can make the payment of taxes monthly or Quarterly ???

Note – : Rules Regarding Payment through PMT – 06 will be discussed with notification No. 85/2020 – Central Tax.

NOTIFICATION NO. 83/2020 – CENTRAL TAX

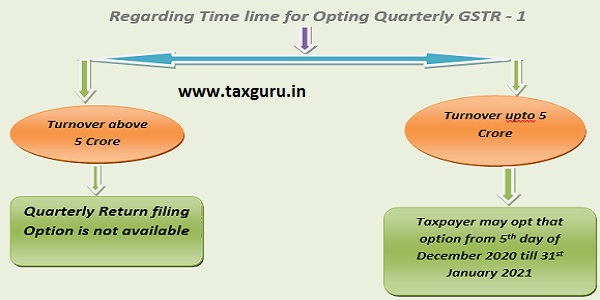

NOTIFICATION NO. 84/2020 – CENTRAL TAX :-

Deemed Option Table :-

| S.NO. | Class of registered person | Deemed option |

| 1 | Registered persons having aggregate turnover up to 1.5 crore rupees, who have furnished FORM GSTR-1 on quarterly basis in the current financial year | Quarterly return |

| 2 | Registered persons having aggregate turnover of up to 1.5 crore rupees, who have furnished FORM GSTR-1 on monthly basis in the current financial year | Monthly return |

| 3 | Registered persons having aggregate turnover more than 1.5 crore rupees and up to 5 crore rupees in the preceding financial year | Quarterly return |

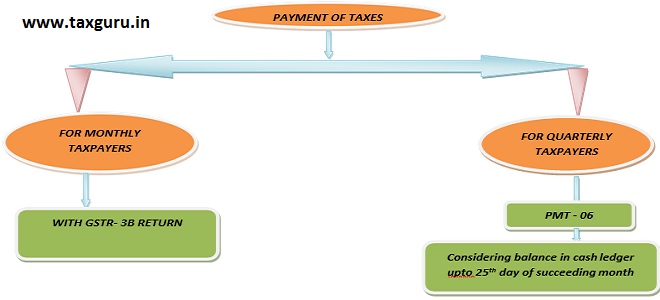

NOTIFICATION NO. 85/2020 – CENTRAL TAX :-

Regarding Manner of Payment of taxes in Case of Quarterly GSTR – 3B

Taxpayer has to pay tax equal to 35% of tax liability of such quarter in the First month or second month or both month of the quarter.

No tax payment is required in following cases:

a. for the first month of the quarter, where the balance in the electronic cash ledger or electronic credit ledger is adequate for the tax liability for the said month or where there is nil tax liability.

b. for the second month of the quarter, where the balance in the electronic cash ledger or electronic credit ledger is adequate for the cumulative tax liability for the first and the second month of the quarter or where there is nil tax liability .

Note : For opting this scheme taxpayer have to file his all pre-vious period Returns (i.e. From the date of registration till the date of opting of that option.

NOTIFICATION NO. 86/2020 – CENTRAL TAX :-

Regarding Earlier Notification No. 76/2020 – Central Tax :-

Through the Notification No. 86/2020 Govt has omitted Notification No. 76/2020 In which notifica-tion Govt. has describes the dates of GST Returns from October 2020 till March 2021.

NOTIFICATION NO. 87/2020 – CENTRAL TAX :-

Regarding Due Date of form ITC – 04

The due date for furnishing the declaration in Form ITC – 04 in respect of goods dispatched to a job worker or received from a job worker, during the period from July, 2020 to September 2020 till the 30th Day of November 2020.

NOTIFICATION NO. 88/2020 – CENTRAL TAX :-

Regarding E – Invoicing

CBIC notifies that E-invoicing is mandatory from 01.01.2021 for every taxpayer (other than SEZ unit) whose aggregate turnover (TO) in any of the Financial Year from 17-18 exceeds Rs. 100 Crores.

Author Bio

sir, we claim ITC refund behalf our company with payment of gst, after that we received a SCN from department side can you help me about this SCN reply