In order to ensure dealing with a GST Compliant Supplier; one should keep a check of the following details which are readily made available on the GST portal:-

1) Check Status of GST Registration

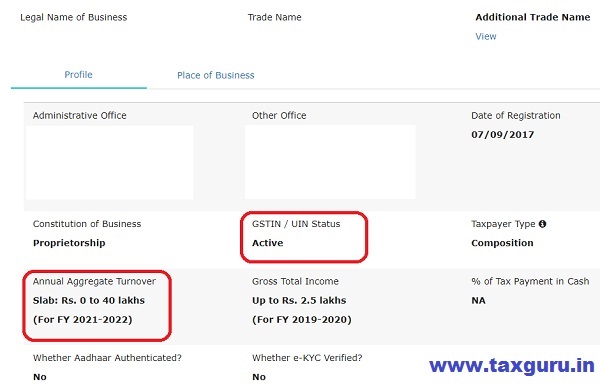

While carrying out transaction with a registered supplier, the recipient shall ensure that the said supplier is actively registered under GST. Since there have been various instances where the supplier’s GSTIN was cancelled and even though transactions were carrying out but the tax were not paid to Government treasury. Further, revenue issues notices to the bonafide recipient for recovering the said tax which was already paid by the recipient to the supplier and the supplier defaulted in making payment to the exchequer.

In order to avoid such litigations, registration status of a registered person can be verified from the GST portal under the Search Taxpayer tab.

2) Check GST Return Filing Status

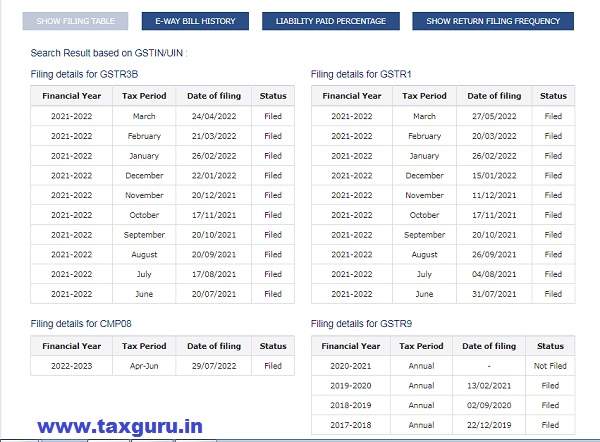

Since the reflection of Invoices pertaining to Inward supplies are automatically reported in Form GSTR 2B on the basis of statement of outward supplies in Form GSTR 1 filed by the supplier within the stipulated date and which determines the ITC availability in the hands of the recipient; it becomes of utmost importance to ensure that the supplier is filing its Form GSTR 1 within the stipulated time limit; non-compliance of which may lead to additional burden on the recipient since the ITC availability may get delayed.

Moreover, the compliance on the part of supplier is not ensured merely by reporting the invoices in Form GSTR 1; as one of the main conditions to avail ITC is that the Tax must be deposited to the Revenue; the supplier needs to discharge the appropriate GST liability pertaining to supplies reported in Form GSTR 1 through summary return in Form GSTR 3B.

There have been various instances wherein the supplier have appropriately reported invoices for outward supplies in Form GSTR 1, but have not discharged the appropriate Tax through Form GSTR 3B pertaining to such invoices. In such instances, Department is issuing notices; demanding the tax from the bonafide recipient who has already paid the tax to the supplier; who has defaulted in making payment to the exchequer.

In order to avoid all the above adverse implications, one can check the return filing status and percentage of liability reported by supplier in their GSTR 1 and corresponding liability discharged vide Form GSTR 3B. The above details can be seen after logging into GST portal in the Search Taxpayer section.

3) Whether supplier is liable to E-Invoicing ?

Any registered person who had aggregate annual turnover exceeding Rs. 10 Crore in any of the financial year from 2017-18 to 2021-22, are liable to prepare e-invoice w.e.f. 01 October 2022. This has brought various small taxpayers in the net of e-invoicing.

In case a registered supplier, who is liable for e-invoicing, fails to generate e-invoice; then the said invoice will be considered invalid and void-ab-initio owing to which the recipient would not be able to claim ITC of the taxes paid in lieu of the said invoice.

One can check its supplier’s aggregate annual turnover for the FY 2021-22 on the GST portal after logging in under the Search Taxpayer tab.

Author Bio