In the realm of Goods and Services Tax (GST), comprehending the nuances of tax invoices and credit/debit notes is imperative for both suppliers and recipients. A tax invoice stands as a pivotal document, affirming the exchange of goods or services, while credit and debit notes rectify any discrepancies in the taxable value or tax charged.

Tax Invoice Essentials:

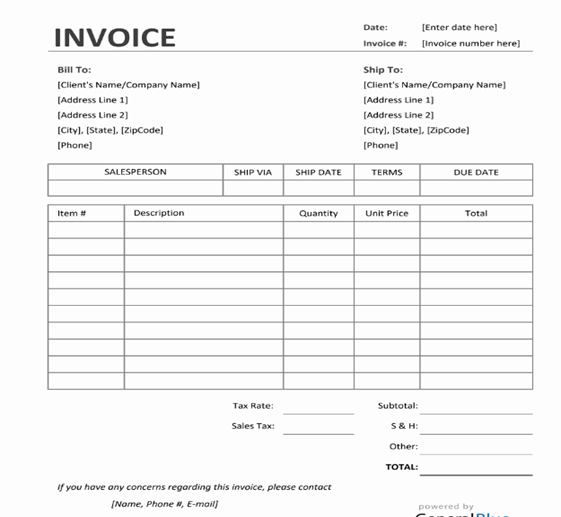

Subject to rule 5, a tax invoice referred to in section 23 shall be issued by the supplier containing the following basic details.

- Name and Address of the Registered Supplier

- Name and Address of the recipient

- GST No. of the supplier

- GST No. of the recipient (if registered under the GST)

- Taxable value

- Tax amount

- Invoice value

- Quantity of the supply

- Rate of supply

- Description of the supply with HSN/SAC code of the supply

- Invoice Number

- Invoice date

- Signature/Digital signature (applicable for E-invoice) of the supplier/authorized representative

- For article on e-invoice please click on the link below:

https://taxguru.in/service-tax/e-invoice-compliance-gst-changes-implementation.html

A sample format of Tax invoice is provided hereunder:

Tax invoice is a very important document both for the Supplier and the receiver. It is a basic document confirming the supply of goods/service. Without a valid Tax invoice registered persons are not entitled to get any benefit under GST.

Credit and Debit Note under GST

After issuing a tax invoice after the supply of goods and services taxable value and tax charged exceeds the taxable value and tax payable for such supply or where the goods supplied are returned by the recipient if any deficiency is observed in the value of supply then the supplier can raise a credit note to that extent of deficiency in supply provided the credit note to be raised within the financial year containing such particulars as may be prescribed. On the other hand After issuing a tax invoice after the supply of goods and services taxable value and tax charged falls short of the taxable value and tax payable for such supply then the supplier can raise a debit note to that extent of that particular amount of shortfall in supply provided the debit note to be raised within the financial year containing such particulars as may be prescribed.

If any registered person issues a credit note in relation to the supply of goods and services then the same has to be declared by such registered person in the return for the month during which such credit note has been issued but not later than 6 months from the end of the relevant financial year or such other date as prescribed by the Govt. or date of furnishing the relevant annual return whichever is earlier.

Conclusion

Understanding the fundamentals of tax invoices, credit notes, and debit notes under GST is paramount for ensuring compliance and facilitating seamless transactions. These documents not only validate the legality of transactions but also serve as vital tools in rectifying any discrepancies, thereby fostering transparency and efficiency in the GST regime.