Dr. Sanjiv Agarwal

Anti Profiteering is a check against profiteering – something which ought to be ethical but is now a legal issue in Goods and Service Tax.

While every business would like to earn more and more profits from business, given an opportunity, it is a fact that GST is a new concept being introduced in India for first time and claimed as a major tax reform and that experience suggests that GST may bring in general inflation in the introductory phase. The Government wants that GST should not lead to general inflation and for this, it becomes necessary to ensure that benefits arising out of GST implementation be transferred to customers so that it may not lead to inflation. For this, anti profiteering measures will help check price rise and also put a legal obligation on businesses to pass on the benefit. This will also help in instilling confidence in citizens.

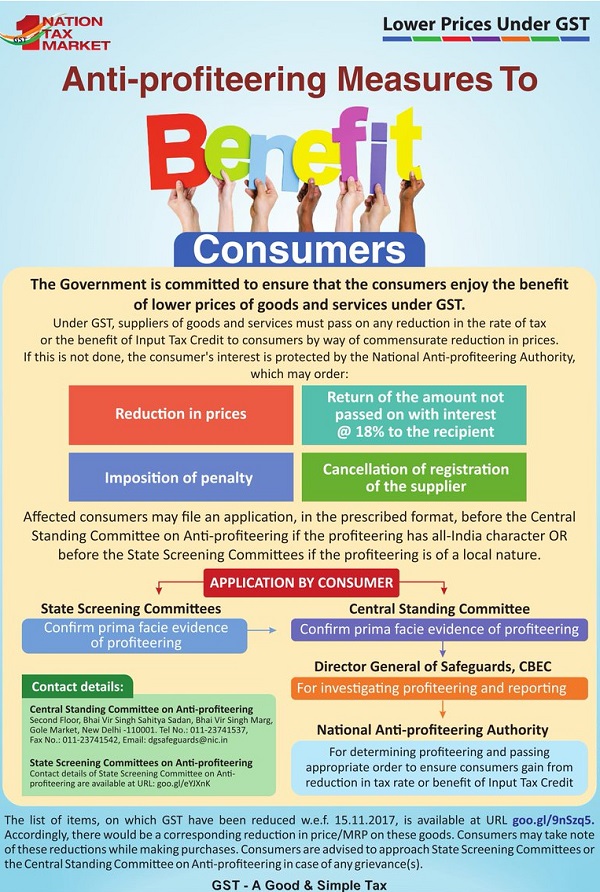

As per section 171 of the CGST/SGST Act, any reduction in rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices. An authority may be constituted by the government to examine whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him.

Objectives

The GST law contains a provision on anti-profiteering measure as a deterrent for trade and industry to enjoy unjust enrichment in terms of profit arising out of implementation of Goods and Services Tax in India, i.e., anti-profiteering measure would obligate the businesses to pass on the cost benefit arising out of GST implementation to their customers.

Section 171 provides that it is mandatory to pass on the benefit due to reduction in rate of tax or from input tax credit to the consumer by way of commensurate reduction in prices.

Anti-profiteering Authority

The power has been given to Central Government to constitute an authority to oversee whether the commensurate benefit of allowance of input tax credit or reduction in the tax rates have been passed on to the final customer. Section 171(2) of the GST Act provides for establishment of an authority for an anti-profiteering clause in order to ensure that business passes on the benefit of reduced tax incidence on goods or services or both to the consumers.

The National Anti-profiteering Authority shall be responsible for applying anti-profiteering measures in the event of a reduction in rate of GST on supply of goods or services or, if the benefit of input tax credit is not passed on to the recipients by way of commensurate reduction in prices. The National Anti-profiteering Authority shall be headed by a senior officer of the level of a Secretary to the Government of India and shall have four technical members from the Centre and/or the States.

The National Anti-profiteering Authority shall be responsible for applying anti-profiteering measures in the event of a reduction in rate of GST on supply of goods or services or, if the benefit of input tax credit is not passed on to the recipients by way of commensurate reduction in prices. The National Anti-profiteering Authority shall be headed by a senior officer of the level of a Secretary to the Government of India and shall have four technical members from the Center and/or the States.

The Authority under section 171 of the GST Act shall have the following monitoring functions:

(a) Input tax credit availed by taxpayer have actually resulted in commensurate reduction in price of goods/services.

(b) The reduction in prices on account of reduction in tax rates have actually resulted in a commensurate reduction in price of goods/services.

The Government has notified anti-profiteering authority (APA) which will check any undue increase in prices of products of companies under GST. The APA will work to check any undue increase in prices of products by taxpayer companies under the GST regime.

Various authorities under GST law for anti-profiteering shall, thus comprise of the following:

- National Anti-Profiteering Authority,

- Standing Committee on Anti-Profiteering, and

- State level Screening Committee.

The powers to take action are also listed as duties whereby it can order price reduction, refund of profit, recovery, penalty or even cancellation of GST registration. The authority constituted by Central Government will have powers to impose a penalty in case it finds that the price being charged has not been reduced consequent to reduction in rate of tax or allowance of input tax credit.

During the two years of initial transition into GST regime, Anti-Profiteering Authority (APA) will step in and may ask businesses that have not passed on full benefits of reduced tax burden to consumers to make up for such benefit, with interest.

Anti-Profiteering Authority (APA) shall act as a monitoring and regulatory authority to curb anti-profiteering practices of tax payers under GST regime. The APA shall have powers to:

- Make company reduce the prices.

- Make company refund the money to the consumer along with interest @ 18% p.a.

- Order company to deposit the refund amount in the Consumer Welfare Fund (in case the buyer is not identifiable).

- Impose monetary penalty equivalent to amount involved in undue profiteering.

- Cancel registration of the assessee.

Orders of authority may be for any of the following:

- Reduction in prices

- Returning money to the customer along with interest

- Depositing money in customer welfare fund in case the customer does not claim it or is not identifiable

- Imposition of penalty equivalent to the amount of profiteering

- Cancellation of registration

Union Cabinet has on 16th November, 2017 cleared the setting up of GST National Anti-profiteering Authority (NAA). The post of Chairman and members of the authority have been created paving the way for authority to be functional soon. Ideally Government should have set up NAA much earlier as consumers are the ultimate sufferers of price hike, inflation and undue profiteering.

A five-member panel headed by Cabinet Secretary P K Sinha and comprising of Revenue Secretary Hasmukh Adhia, CBEC Chairman and chief secretaries from two states has been entrusted with the task of selecting the chairman and members of the authority.

Authority to benefit Consumers

The National Anti-Profiteering Authority is an assurance to consumers. If any consumer feels the benefit of tax rate cuts is not being passed on, he can complain to the authority. The body is mandated to ensure that the benefits of GST rate reduction is passed on to consumers.

The five-member anti-profiteering authority will have power to ask those not passing on the tax benefit to return the undue profit earned to consumers along with an 18% interest, reduce prices and if the consumer is not identifiable, deposit the amount in a Consumer Welfare Fund.

In yet another move, CBEC has issued an advisory to major consumer product manufacturers to ensure that price reduction should take place wherever rates have been lowered so that benefits may go to consumers. Restaurants are one of such examples where there are complaints of non-passing of the benefit to consumers. Except restaurants in big hotels, GST has been lowered from 18% to just 5% with no input tax credit benefit.

Companies will have to ensure that retailers and distribution chain pass on the GST cat benefit to consumer with immediate effect. No delay will be allowed. It is the company’s responsibility to ensure that its entire retail chain follows its directives on pricing. If a trader is not selling a good at revised MRP, then it is the responsibility of the company. It will have to respond to the Anti-profiteering. Authority on this action can only be taken against organized players as they are the ones who decide MRP.

The setting up of NAA has been expedited in view of the fact that many traders and businesses have failed to pass on the benefit to consumers. Activation of this provision in the law might have been avoided, had trade and industry passed on the eliminated cascading of taxes to consumers by way of lower prices.

How does MRP based products assessed for anti profiterring?