Preamble

Indians are amongst the second-largest buyers of physical gold in the world. In the last few years, the boom in the digital revolution expanded to the gold market too, and it introduced a new form of investment – digital gold. Digital gold as a concept is quite new in India.

Further, bottlenecks in physically holding gold has been also removed in Digital Gold. One has to buy physical gold in multiples of 1gm (equivalent to approximately ₹4,500) compared with multiple of Re 1 when buying digital gold. In addition, jewellery and ornaments will come with high making costs and there is always the risk of theft. Selling physical gold involves a trip to a jeweller where digital gold can be sold anytime with money instantly credited to your bank account.

Not to say, gold investment has significant emotional and social value is worth it, as it is a safe hedge against inflation. In the long term, the returns on investment in gold are in line with the rate of inflation. In last one year Gold has given 26.85% return to the investors.

A highly secure online investment instrument, digital gold allows investors to purchase certified 24-Karat pure gold in a hassle-free manner. Every time digital gold is bought online, the seller stores an equivalent amount of physical gold in a secure vault. Investors can start making small investments, as low as Re1 and accumulate gold in their portfolio, across many transactions.

Popular payment wallets such as PayTM, GPay and PhonePe allow digitally buy and store gold from several providers within your existing payment application. The apps come with a secure Gold Locker where gold be stored all the gold purchased through the app where digital sell of the gold can be done.

Customers can invest in digital gold with multiple providers. When digital gold is purchased from MMTC-PAMP, one of the leading providers of digital gold and India’s largest and only London Bullion Market Association accredited gold refinery, investors will be buying 24k 999.9 purest physical gold. The fully secured and insured gold is then stored in certified vaults with MMTC-PAMP. This gold value is then captured in the investor’s preferred app/intermediary’s online platform.

Investors also have the option of retaining their purchase within the secure digital vault or redeeming from a wide range of 24k 999.9 pure gold bars or coins. In case the physical option is chosen, this is then delivered directly to the investor’s doorstep.

Maximum buying limit is Rs 2 lakh per day without a PAN card for digital to a single transaction or multiple cumulative transactions in a day. Likewise, the sale of physical gold, it attracts 3% taxes in the form of GST.

Page Contents

What is digital gold?

It is a mode of investing / buy or sell 24 karat Hallmark gold for as low as ₹1 in physical gold like the regular gold, can be bought online and is stored in insured vaults by the seller on behalf of the customer.

The pandemic has accelerated the rising preference among users to transact and invest digitally, making digital gold one of the most popular investments.

The largest digital platforms in the country, including e-commerce portals, wealth management channels, banking and payment apps, are offering digital gold as part of their offerings.

How digital gold works?

You can invest in digital gold from several mobile e-wallets such as Paytm, Google Pay and PhonePe. Brokers such as HDFC Securities and Motilal Oswal also have an option for digital gold investing. Currently, there are three first companies that offer digital gold in India-

1. Augmont Gold Ltd.

2. MMTC-PAMP India Pvt. Ltd. a joint venture between state-run MMTC Ltd. and Swiss firm MKS PAMP.

3. Digital Gold India Pvt/ Ltd with its SafeGold brand.

Apps and websites like Paytm, G-Pay etc only provide a platform for metal trading companies SafeGold and MMTC PAMP. Once you invest in digital gold, these trading companies purchase an equivalent amount of physical gold and store it under your name in secured vaults.

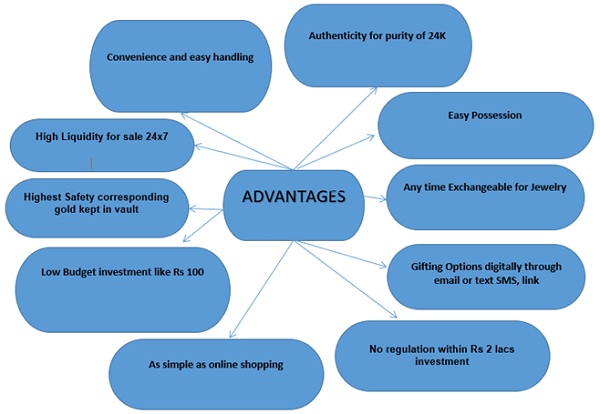

What are the Advantages of buying digital gold?

♦ No making charges on buy/sell transactions.

♦ High Liquidity like Cash

♦ Investments 24×7 at real-time rates with a single click.

♦ Stored safely in secure vaults

♦ Backed by an independent trustee.

♦ No lock-in period

♦ Short-term parking of Funds

♦ Increased Digital awareness:

This growing technology has increased the availability of information among general masses. With growing information and knowledge, the investors have now become aware about various forms of investing. Like investors have now started understanding the difference between endowment policies and life insurance, and are now segregating investment from insurance products.

♦ No involvement of an intermediary.

♦ Purity :

It was a major concern with buying pysical gold, which, as we saw, is completely eliminated in the digital products.

♦ Security and locker charges:

Keeping physical gold is a very risky business and storing it in bank lockers adds an additional burden in the form of locker rents, which is not the case in digital gold as it can’t be stolen from our demat accounts and additionally is tradable.

Also with growing efficiency in our capital markets we have seen the transformation from physical shares to demat, combating all the difficulties in investing, similar is the case with gold. Investors have started understanding the difference between investment in gold and buying jewelry for various ornamental uses.

What are the Disadvantages of Investing in Digital Gold?

♦ Limit of Rs.2 lakhs for investment on most platforms.

♦ Lack of an official government-run regulating body such as RBI or SEBI.

♦ Delivery and making charges are further applied to the price of gold on conversion to physical.

♦ In some cases, companies only offer a limited storage period, after which you either have to take physical delivery or sell the gold.

♦ Cyber thefts pose a major risk that come along with any online transaction. Buying the digital form of the commodity is also prone to this.

♦ Uncertainties like registering the Nominee name exist

Currently, digital gold is not directly under the purview of any regulatory body. So there is an element of risk as rules are not yet in place yet.

How secure it is?

The entities who actually sell digital gold serve as custodian of the accumulated gold, irrespective of buying directly or via any platform. A trustee is appointed to oversee quality and operation of vaults.At no point does the ownership of the accumulated gold transfer to either the partner service provider or the custodian. The physical gold is stored in secured vaults that are fully insured for any eventualities— loss due to theft or damage caused.

A differential analysis of three means of Digital Investment in Gold:-

| Nature | Digital Gold Wallet | Sovereign Gold Bond (SGB) | Gold Electronic Trade Fund ( ETF) |

| 1. Issued by :- | It is primarily sold by MMTC PAMP, Augmont Goldtech and Digital Gold India (SafeGold) through service providers like PayTM, GooglePay , Banker, Jewellers etc. | Issued by the Reserve Bank of India (RBI) on behalf of the government. These bonds were introduced under the Gold Monetization Scheme in 2015. These bonds are issued in many tranches throughout the year by the RBI.

|

It is issued by Mutual Fund AMC like SBI, HDFC etc. and regulated by SEBI, hence reducing the safety and security worries. |

| 2. Holding cost:- | It is least expensive as various charges like asset management fees, security service fees not applicable for at least 5 years except one time 3% GST on purchase or sale. | It bears various recurring charges like asset management fees, security service fees ranging from 0.5% to 1%. | It has recurring charges like asset management fees, security service fees ranging from 0.5% to 1%. |

| 3. Denomination:- | It offers to invest in gold even Rs 100/- i.e. small fraction of 1 gram. | Each bond represents 1 gram of gold.

|

It is a way to invest in gold in small quantities like fraction of 1 gram,like digital gold .

|

| 4. Interest on Investment:- | No interest on gold deposit is applicable. Appreciation / depreciation of Gold price is applicable to the investor. | In addition to the changes in gold rates, these bonds have an attractive interest rate of 2.5% per annum, which is paid semi-annually by the RBI adding to the yield.

|

Market appreciation/ depreciation through NAV is applicable. |

| 5. Lock in Period:- | No time duration / lock in period is applicable. | These bonds have a time duration of eight years and the RBI also provides a redemption option after the fifth year.

|

No time duration / lock in period is applicable, except for Income tax purposes. |

| 6. Mode of Custody:- | It can be kept in digital vault . | The bonds are also tradable on stock exchanges, giving a liquidity option, kept in Demat account.

|

Its custodian lies with Mutual Fund AMC. |

| 7. Regulation:- | No regulated by any statutory body yet. | It is regulated by RBI.

|

It is regulated by SEBI. |

| 8. Transferrable :- | It can be gifted and transferred/ sold within a minute. | It can be gifted or transferred with compliances. | It is not transferrable. |

| 9. Investment type | It is truly Digital Gold. | It is Paper Gold. | It is Paper Gold. |

| 10. Income Tax | Investments in digital are treated on par with regular gold and therefore the holding period, tax rate and exemption available are also identical to that of physical gold. | The appreciation in value of it at the time of its redemption is tax free but if to sell these bonds in open market the profits made will get taxed as capital gains ; short term or long term depending on the holding period. | In case of sale after 36 months the profits are treated as long term capital gains and taxed at the flat rate of 20% after applying the cost inflation index to the cost of acquisition. In case these are sold within 36 months, the gains are treated as short term capital gains and taxed at the slab rate applicable to you. |

Misconceptions about Digital Gold

♦ It is a paper certification of gold ownership:

One of the most common myths is that when a customer invests in digital gold he/she does not own it physically. This is not true. Gold corresponding to every purchase, irrespective of the amount, is stored in a secured and insured vault. Customers can access and take delivery of the gold bought at any time.

♦ Extensive documentation is required:

A user just needs is a phone, access to the internet and a bank account or UPI. It is as simple as shopping online for any other product. Only in cases of the transaction exceeding ₹2 lakh, PAN card information must be provided.

♦ Online gold is not pure gold:

Safe Gold offers 24 Karat gold of 9999 purity (99.99% pure). All SafeGold coins and bars assay certified to ensure the highest purity.

Digital gold, being a relatively new offering in the country, does not have regulations guiding it yet.

According to recent industry reports, the regulators are looking at framing guidelines for the sector. Such a step is welcomed and will lay the foundation for the healthy growth of the digital gold space in the country.

Conclusions

With nations worldwide resorting to unprecedented stimulus packages to counter the pandemic’s impact, this is likely to see currencies devalued in the near future. Besides hedging one’s portfolio from the impact of such devaluations, it is especially helpful in offsetting steep corrections in the stock markets.

While all are aware of physical gold such as jewellery, bars and coins, digital gold requires some elaboration.

Experts say that though physical gold used to see traction around festivals, digital gold investment has seen increasing trend round the year. The current pandemic has also made the concept of digital gold even more popular in the country and has increased digital gold purchasing by almost 70 per cent in the country.

There is little doubt that Gold as an investing class should make up a small part of our portfolios. But there are better options to invest in gold such as Sovereign Gold Bonds and Gold ETFs rather than going for Digital gold.

The key reason being that gold should be a part of a long-term portfolio. In that sense, it is better to go with gold bonds as they pay an additional 2.5% interest. But since bonds are less liquid, for short term hedges, investing in Gold ETFs is a better option as they fall under the regulatory body of SEBI.

Once the investment limit of Rs.2 Lakhs per day removed and a regulatory body is appointed, Digital Gold would make for an appealing investment for those who prefer investing in physical gold.

SEBI is expected to introduce norms for digital gold very soon. It recently barred brokerage platforms from offering digital gold.

Further, there is plan to offer digital silver by the end of 2021 by MMTC-PAMP.

Author Bio