*Sunil Mehta

Liquidation has been defined as a process of bringing a business to an end and distribution of the assets of the company between persons having claims over the company. Liquidation is a consequence of being insolvent and / or having no realistic prospect of a going concern. Liquidation could be compulsory or voluntary. Compulsory liquidation usually occurs when a company is unable to pay its dues to its obligor in part or full, not only when it is due, but also as a deferred payment in future based on the available assets as against the liabilities of corporate entity. This liquidation is generally forced by the creditors. Voluntary liquidation usually occurs when a company has no realistic prospects to remain a going concern. The inability of payment of dues is not the case when situation of voluntary liquidation arises. Voluntary liquidation is forced by the entity itself through its board of directors. Businesses need efficient and speedy procedures for exit as much as for start-up. World over, insolvency procedures help entrepreneurs close down unviable businesses and start up new ones. This ensures that the human and economic resources of a country are continuously channelised to efficient use, thereby increasing the overall productivity of the economy. Considering the importance, many countries have reformed the insolvency processes. India is no exception to this.

LIQUIDATION UNDER THE CODE

Before the enactment of Insolvency and Bankruptcy Code, 2016 (Code), the option of liquidation was available to bankers even in the days of the Board for Industrial and Financial Reconstruction (BIER), which had been set up under the Sick Industrial Companies (Special Provisions) Act, 1985 (SICA). The route, however, involved considerable delay as promoters would often declare themselves sick and avail of a moratorium period over which recovery could not be initiated.

It was essential to provide for a sound framework for restructuring and rehabilitation of companies along with a framework for winding up and liquidation. The framework should seek to preserve the estate and maximise the value of assets; recognise inter se rights of creditors and provide equal treatment to similar creditors, while dealing with small creditors equitably. This resulted in framing of the Code .

Liquidation has gradually gained momentum since the enactment of Code which aims at preservation as well as maximisation of value of assets created by an entity by keeping an organization as a going concern and simultaneously resolving the financial stress on the entity. Under the Code, a large number of companies have been liquidated or are under liquidation.

As per quarterly newsletter of the Insolvency and Bankruptcy Board of India (IBBI), till quarter ending June 2019, 2162 cases were admitted for Corporate Insolvency Resolution Process (CIRP), out of which 475 cases have ended with commencement of liquidation. In addition, 452 cases of voluntary liquidation were also admitted, of which, 56 firms have so far been dissolved, final reports have been submitted in 114 cases and 338 are at different stages of the process.

The liquidation process, especially voluntarily liquidation, has become the thrust area for the financial creditors (FCs), other stakeholders, investors and professionals.

LEGAL FRAMEWORK

The provisions regarding liquidation contained in Chapter III (section 33-54) of the Code came into effect from December 15, 2016 and provisions regarding voluntary liquidation contained in Chapter V (section 59) of the Code came into effect from April 1, 2017. The legal framework is mainly covered by separate regulations issued by the IBBI as per power conferred by section 196 of the Code.

In pre-Code regime, the winding up was governed by the Companies Act, 1956. However, new provisions of winding up were provided in the Companies Act, 2013 (the Act of 2013) under Chapter XX, but the same were not notified till effective date of the Code. The Code has amended Companies Act, 2013 by virtue of section 255, as per schedule XI of the Act. Accordingly, winding up was defined under the Act of 2013 as ‘Winding up under this Act or liquidation under Insolvency and Bankruptcy Code, 2016, as applicable’. Further, at the same time the provision regarding voluntary winding up was omitted from the Act of 2013. Accordingly, it could be interpreted that while the winding up will be governed by both Companies Act and the Code, liquidation and voluntary liquidation will be governed by the Code.

FINE LINES BETWEEN WINDING UP, LIQUIDATION, VOLUNTARY LIQUIDATION

In general understanding, winding up, liquidation and voluntary liquidation are the same thing. All these processes end up with the dissolution of the corporate entity. However, in legal arena all three differ in terms of applicability, procedure & processes.

Winding Up

‘Winding up’ in terms of the Act of 2013 is to be decided by the National Company Law Tribunal (NCLT), where:

- Company has decided the same by virtue of special resolution; or

- Company has acted against the interests of the sovereignty and integrity of India, the security of the State, friendly relations with foreign States, public order, decency or morality; or

- Affairs of the company have been conducted in a fraudulent manner or the company was formed for fraudulent and unlawful purpose or the persons concerned in the formation or management of its affairs have been guilty of fraud or misconduct in connection therewith; or

- Company has defaulted in filing of its financial statements / annual returns with registrar for the immediately preceding consecutive five financial years; or

- It is just and equitable that the company should be wound up.

Liquidation

By virtue of Schedule XI of the Code, reason ‘if the company is unable to pay its debts’ was removed from the above list. Accordingly, it is clear that in case of default of payment of dues, the creditors cannot directly refer the company for liquidation / winding up but has to undergo CIRP first. Liquidation will be the last resort if resolution under CIRP fails. Liquidation under the Code is to be initiated by Adjudicating Authority (AA) if:

- No resolution plan is received or approved by the Committee of Creditors(CoC)and submitted by the Resolution Professional (RP) to AA within the timeline applicable to CIRP / Fast Track Insolvency Process; or

- Resolution plan submitted by RP is rejected by AA due to non-compliance; or

- CoC decides to liquidate the Corporate Debtor(CD) even before confirmation of resolution plan (even before preparation of information memoranda).

- Contravention by CD after approval of resolution plan by AA.

Since, CIRP could be initiated by any operational creditor (OC), CD or financial creditor (FC), the liquidation is effectively initiated by the company itself or its creditors in cases where any default was committed by the CD, obviously after assessing the possibility of resolution.

Voluntary Liquidation

‘Voluntary liquidation’ as the name suggests, means liquidation at own will. However, a corporate entity which is incorporated by a law subject to certain permissions & process could not be liquidated suo motu without safeguarding the interest of its stakeholders. Voluntary liquidation is to be initiated by the CD, when there is no default. As per Section 59(6) of the Code, the provisions of section 35 to 53 (applicable in case of liquidation) shall also apply to voluntary liquidation proceedings. Accordingly, for entering into voluntary liquidation the following compliances are required to be done:

- Declaration by majority of the designated partners of Limited Liability Partnership (LLP) / individual consisting of a governing body by an affidavit that (i) Either the corporate has no debt or that it will be able to pay its debt in full from the proceeds of assets to be sold under liquidation; (ii) the corporate person is not being liquidated to defraud any person. Such declaration is to be supported by audited financial statements and record of business operations of two years and a report of valuation of the assets;

- Passing of resolution within 4 weeks of declaration, by special majority of LLP Partners or contributories, appointing the liquidator or to voluntarily liquidate the company due to expiry of its duration as fixed by constitution documents;

- In case the company owes any debt, the resolution is to be approved by the creditors representing two-third of the debt value within 7 days;

- The resolution to be notified to IBBI and Registrar of Companies (ROC) within 7 days of passing resolution or approval, as the case maybe.

Thus, the major difference between liquidation and voluntary liquidation is applicability and the party eligible to initiate.

ROLE OF LIQUIDATOR

The entire process of liquidation/voluntary liquidation relies on the liquidator and accordingly, the liquidator has been given significant powers. As powers and responsibilities go side by side, the liquidator carries legal as well as moral responsibilities.

The major powers and duties of the liquidator which are to be performed along with compliance of the Act, Rules and Regulations include the following:

- invite, verify and settle the claim of all the creditors;

- to take the custody / control of all assets including actionable claims;

- to measure the assets and prepare the reports;

- protection and preservation of assets;

- carry the business of the CD for its beneficial liquidation;

- sale of assets, realisation of actionable claims;

- power to transfer the assets to other person and giving lawful right to person acquiring the assets;

- to become signatory for all valid purposes;

- to institute or defend any suit or other legal proceedings;

- to take out, in its official name, letter of administration of any deceased contributory;

- to engage professionals to assist him/her in the discharge of his duties;

- to submit the Preliminary Report, Progress Report, Asset Sale Report and Final Report to AA.

The liquidator carries all the powers of the board of directors / key managerial personnel of the CD. For performance of the duties, the liquidator has to charge the fees as may be decided by the CoC. However, IBBI (Liquidation Process) Regulations, 2016 also define the schedule of fees. The schedule of fees is designed in such a way that clearly links the liquidators compensation with its timely and effective performance. The more effectively and efficiently the liquidator performs its duties, more the payable fees.

Since, the liquidator is entrusted with significant duties and powers, it is expected that liquidator will perform its duties with morals and ethics along with compliance of law. Accordingly, any related party of the CD, auditors or legal or consulting firm (including its employees, partners / directors) are not eligible for becoming the liquidator subject to certain conditions given in the regulations.

Liquidation Estate

During the process of liquidation, the liquidator shall form an estate of assets, which is termed as the liquidation estate of the CD. The assets to be included and not to be included in liquidation estates are as under:

| Included Assets | Excluded Assets |

| Assets on which the CD has the ownership rights, including assets not under possession or encumbered assets | Assets held in trust for any third party which are in possession of CD |

| Tangible assets, whether movable or immovable | Collateral held by financial services providers which are subject to netting and set-off in multilateral trading or clearing transactions |

| Intangible assets including shares held in subsidiaries of CD | Provident Fund, Pension Fund or Gratuity fund to the extent it is due |

| Assets subject to determination of ownership by the court | Contractual arrangement for use of asset which does not transfer the title |

| Any assets recovered through proceeding of avoidance of transactions | Personal assets of shareholders / partners |

| Any other assets as on liquidation commencement date | Bailment contracts |

| The assets on which secured creditors relinquished security interest | The assets on which secured creditors opted to realize their charge under section 52 |

When it comes to liquidation estate, one of the important terms is ‘Contributory’ which means a person liable to contribute towards the assets of the company in the event of it being wound up. In common terms, the shareholder / member is the contributory. However, the holder of partly paid share is the contributory with liability as holder of fully paid up share does not carry any liability. The contributory not only includes the present members but also includes any member who was the holder of unpaid share, within one year from the liquidation commencement date, for the liabilities incurred till it was the member of the company. The role of contributory is not only practical but also very important especially when there is a company with partly paid up share or limited by guarantee as it may be a source of significant funds.

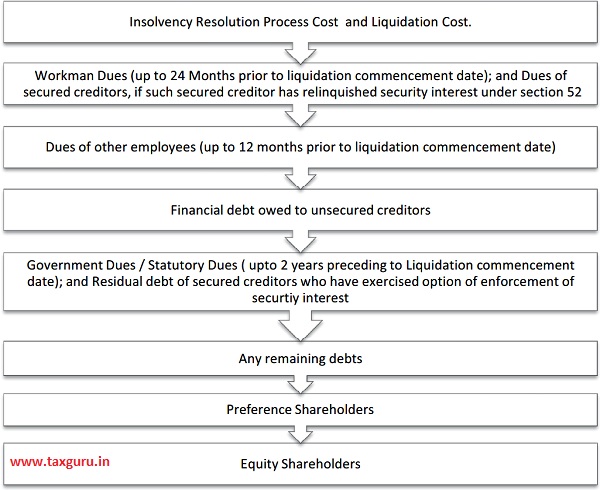

WATERFALL MECHANISM UNDER THE CODE

Secured creditors are given option either to stand outside the liquidation process by realising their dues from sale of assets charged to it or to relinquish their security interest in favour of the liquidator’s estate. It may be stated that it is the secured creditor’s commercial call to select any option which may be based on certain factors such as possibility of realisation of security, ease of control and possession, sharing of security or possible demarcation.

Subject to the option considered by the secured creditors, the distribution of the amount realised from liquidation estates will be done in the figure below:

LIQUIDATION PROCESS AND TIMELINES

Liquidation process is described in IBBI (Voluntary Liquidation Process) Regulations, 2017 and IBBI (Liquidation Process) Regulations, 2016. The regulations prescribe the indicative timelines for timely completion of liquidation process. Liquidation process includes the following steps:

- Commencement of liquidation along with appointment of liquidator. The liquidation commencement date is the deciding factor of further timelines and position of assets and liabilities;

- Public announcement calling stakeholders to submit their claims, to be published in one English and one regional newspaper, website of CD and IBBI;

- The claim of all the stakeholders will be received and verified and correct classification of the same will be done for the purpose of distribution of proceeds from realisation of assets;

- A Stakeholders’ consultation committee shall be constituted within 60 days from liquidation commencement date which will include members from secured FCs, unsecured FCs, workmen and employees, Government, OCs, shareholders as per weightage and maximum members defined in regulations subject to a minimum of one member representing each class of stakeholders. The meeting of stakeholders’ consultation committee shall be convened as and when necessary or when request is received from at least 51 per cent of the representatives. However, the advice of stakeholders’ consultation committee will be non-binding on liquidator;

- The early dissolution of the company may be requested to AA if it is felt that the cost of liquidation will exceed the estimated realizable value of assets;

- The liquidator shall prepare list of contributories for unpaid capital and realise the contribution to the extent of unpaid value of shares by sending a notice to make the payment within 15 days;

- Preliminary report is to be submitted by liquidator to AA within 75 days from liquidation commencement date which shall include capital structure, estimates of asset and liabilities based on books of CDs or reliable records, as may be available, decision regarding desired inquiry on any matter of CD and proposed plan of liquidation process;

- Asset Memorandum shall be prepared by liquidator within 75 days from the liquidation commencement date which shall include the assets intended to be realised along with valuation supported by registered valuer report, mode of realisation, expected realisation amount and other related information relating to assets;

- Progress reports are to be submitted by the liquidator within 15 days from the end of quarter in which he is appointed and further reports within 15 days from end of each quarter during liquidation. The report shall include all developments taken during the quarter and accounts maintained by liquidator. The reports for last quarter of the financial year also include audited accounts of receipts and payments. The progress report shall also include the asset sale report wherever in any preceding quarter any sale has taken place containing description of asset sold and facts regarding mode and value of sale;

- With respect to assets charged with secured creditors, where the secured creditors have not relinquished their security interest and not proposed to exercise their rights under the Securitization and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI), or the Recovery of Debts Due to Banks and Financial Institutions Act ,1993 (RDDBFI), the liquidator may find a possible buyer at a proposed value (or better value) indicated by secured creditor within 21 days from the days of receipt of intimation from secured creditor;

- In case, the liquidator fails to sale any asset, the same may be distributed to stakeholders with the permission of AA;

- Final Report before dissolution will be prepared with complete details of liquidation proceedings and liquidation costs and submitted to AA with necessary formalities for order of dissolution;

- Any unclaimed proceeds of liquidation or undistributed asset are to be kept into Companies Liquidation Account in the Public account of India which shall be further transferred to general revenue account of Central Government, if remains unclaimed for 15 years;

SALE OF ASSETS UNDER LIQUIDATION

The liquidator may sell the assets on standalone or collectively, slump sale/parcels or going concern basis. Further, the mode of sale may be by way of auction or private sale. Further, the auction process may be either electronic or physical depending upon the likelihood of maximising the realisation from the sale of assets. The liquidator may sell only such encumbered assets on which relinquishment of charge by secured creditors is extended in favour of liquidator’s estate.

The sale is to be ordinarily executed by way of transparent auction process. However, sale may be held on private sale basis if asset is of perishable nature or value likely to deteriorate, or price higher than the reserve price of failed auction if realised or with the approval of AA. However, prior permission of AA is to be taken in any case if the asset is proposed to be sold to related party of CD, related party of liquidator or any professional appointed by liquidator.

The sale of assets is the main pillar of the liquidation process and ‘timely and equitable realisation’ from the asset sale is the backbone of the successful resolution process. The major challenges faced by the liquidation process, presently are lack of bidding during auction, long implementation period and delayed processes. Thus, the sale of assets under liquidation is a more challenging area for the professionals i.e. liquidators as compared to the RP. The failure of CIRP lends a company to liquidation but failure of liquidation has no conclusive ending and is a time lagging process. The reason behind such liquidation process may be either inadequate marketing or deterioration in the asset.

Thus, when an asset is to be sold through auction the liquidator needs to prepare a proper marketing strategy which is not limited up to preparing asset information sheet and releasing advertisement. The liquidator carries the independent responsibility equivalent to key managerial personnel of tthe company and there is a need of proactive approach and aggressive marketing strategy for the overall interest of all stakeholders and preserving economical value of assets.

WAY FORWARD

The successful conduct of liquidation process is the primary responsibility of liquidator and efforts are required to be made by liquidator for maximum realization from the liquidation estate. However, the role of other stakeholders is equally vital for the success of liquidation process. Towards this, the Code has made a legal framework for creation of ‘Stakeholder’s Consultation Committee’. This committee can contribute significantly by way of developing marketing strategy for sale of assets as well as finding the prospective buyers.

Another practical issue observed in liquidation process is the lack of a common portal/platform for publicity of auction notices under liquidation unlike available in case of invitation of resolution plan on IBBI portal. It leads to lack of awareness among the prospective buyers as the current source of publicity of auction notices are mainly newspapers or company’s website. In case of CD which are not well known in market, the auction notices get unnoticed. Accordingly, a common portal for displaying liquidation notices is the need of the hour so that assets under liquidation may reach maximum eye balls beyond geographical boundaries.

To conclude, it is desired that the liquidation process should not result in death of the assets of the company. Therefore, there is a need of developing a secondary market which will go a long way in preserving the economic assets and their revival.

Source- https://ibbi.gov.in/uploads/whatsnew/2456194a119394217a926e595b537437.pdf

*(Mr. Sunil Mehta is the Chairman of the Indian Bank Association and the MD & CEO of Punjab National Bank.)

Discussion is excellent