NFRA Inspection Report, numbered 132.2-2022-05 and dated December 29, 2023, scrutinizes the audit practices of Walker Chandiok & Co. LLP (WCCL). Mandated by Section 132 of the Companies Act 2013, the National Financial Reporting Authority (NFRA) initiated an audit quality inspection in December 2022, encompassing a review of firm-wide controls and selected Audit Documentation. The report identifies three significant audit areas—Revenue, Trade Receivables, and Investments—for in-depth examination due to their higher risk of material misstatement. Through detailed observations, it sheds light on critical issues such as dual audit documentation formats, potential non-compliance with independence-related requirements, prohibited non-audit services, and deficiencies in client acceptance and continuance procedures. The report aims to provide a comprehensive analysis of the inspection findings, urging attention to rectify shortcomings and enhance audit quality.

INSPECTION REPORT 2022

Audit Firm: M/s Walker Chandiok & Co. LLP

Firm Registration No. 001076N / N500013

Inspection Report No. 132.2-2022-05

December 29, 2023

Part A

Executive Summary

Section 132 of the Companies Act 2013 mandates the National Financial Reporting Authority (henceforth, NFRA) to inter alia monitor compliance with Auditing Standards, to oversee the quality of service of the professions associated with ensuring compliance with such standards, and to suggest measures required for improvement in quality of their services. Under this mandate, NFRA initiated audit quality inspection of the audit firm Walker Chandiok & Co LLP (henceforth, ‘the Firm’ or ‘WCCL’) in December 2022. The scope of the inspection included a review of firm-wide quality controls to evaluate Audit Firm’s adherence to SQC-1 and review of selected Audit Documentation of the annual statutory audit of financial statements for the year ending 31.03.2021. Three significant audit areas were identified in respect of each audit engagement viz., Revenue, Trade Receivables and Investments, due to their inherent higher risk of material misstatement. The on-site inspection was carried out during the month of December 2022.

The Inspection Team held discussions with the Audit Firm personnel, reviewed policies and procedures and examined documents. The observations were conveyed to the Audit Firm and after examining the replies, a draft inspection report was issued to the Audit Firm. The replies and documents submitted by the Audit Firm have been examined in finalising this report. The key observations in this report are summarised as follows:

a. Audit Documentation of the Firm comprises electronic audit documentation and physical files. This duality of audit documentation and the lack of integration between electronic and paper files poses risks of non-compliance with SQC 11 and other Standards on Auditing (SAs) and raises concerns about the reliability of audit documentation.

(Para 12 to 14)

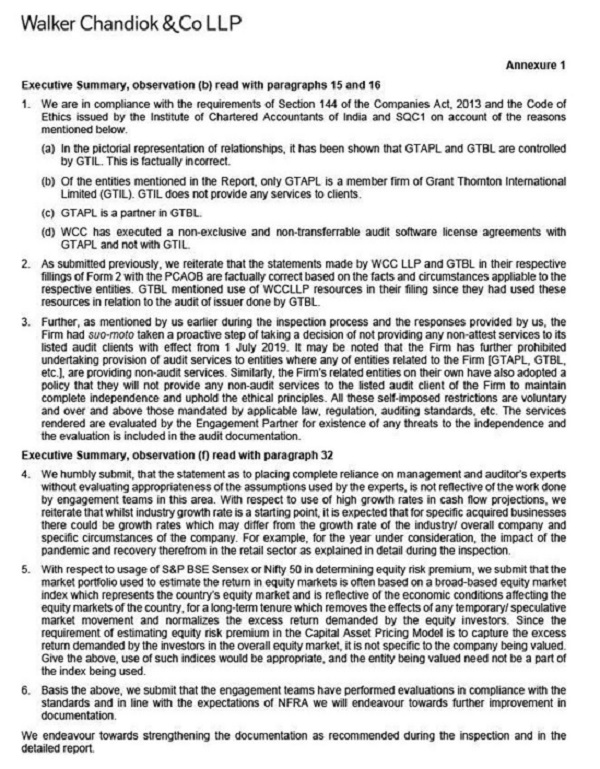

b. Grant Thornton Bharat LLP (GTBL), Grant Thornton Advisory Private Limited (GTAPL) and Grant Thornton International Limited (GTIL) are ‘directly or indirectly’ related entities as per Explanation (ii) to Section 144 of the CA These entities are also part of a large global ‘GTIL Network’ as per SQC 1. However, the Firm denied the existence of direct or indirect relationship and Network.

While the WCCL (controlled by Mr. Vinod Chandiok, father) declared in its filings with PCAOB2 that it had no ‘audit related memberships, affiliations or similar arrangements’ with any other entity, GTBL which is controlled by Mr. Vishesh Chandiok (son), declared in its filings with PCAOB that it had ‘audit related memberships, affiliations or similar arrangements’ with WCCL and the global network namely GTIL.

The Firm did not provide, during this inspection, details of GTIL Network entities, and non- audit services provided by those entities to audit clients of the Firm. Consequently, the Inspection team was unable to evaluate whether the Firm is in full compliance with the independence-related requirements of the Code of Ethics and SQC 1.

(Para 15 & 16)

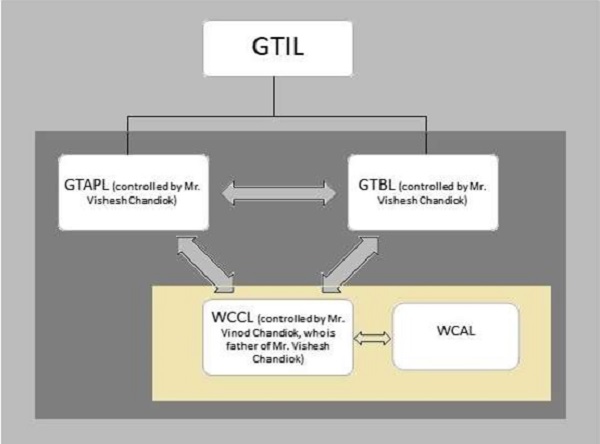

c. In two instances, it was observed that the Firm had provided non-audit services prohibited under section 144 of the Companies Act, 2013 to the auditee companies. In one case, the firm provided ‘consolidated procedures for certain related entities’ of an auditee company for which it was the statutory auditor, including of the consolidated financial In another case, assurance on related party transactions was provided to the Board of Directors, and later on such transactions were audited by the Firm, leading to self-review threat.

(Para 21 to 24)

d. The Firm failed to adhere to some of the prescribed ‘client acceptance and continuance’ prerequisites, including verifying the client’s integrity and recording the resolution of concerns.

(Para 25 to 27)

e. The engagement quality control reviews conducted by the Firm’s Engagement Quality Control Review (EQCR) partners exhibited significant deficiencies in documentation and did not conform to the Firm’s own engagement quality control policies, as well as to the requirements of SQC1 and SA 220.

(Para 28 to 30)

f. The Firm placed complete reliance on the management experts’ and the auditor’s experts’ without evaluating the appropriateness of the assumptions used by those experts. For example, for determining the ‘recoverable amount’ of investments for assessing impairment, the valuation experts used inflated growth rates ranging from 20% to 105%, deviating significantly from industry averages and historical growth rates of the The equity risk premiums for discount rate estimations were based on overall stock market indices, even though the auditee companies’ shares were not part of these indices.

(Para 32)

g. In the case of audit of some companies, we observed the following deficiencies:

i. In one case, the ET did not properly evaluate the non-compliance with the limit on the number (two) of layers of companies prescribed under Section 186 of the Companies Act 2013. The Firm also issued qualified audit opinion (instead of ‘Adverse’ or ‘Disclaimer of Opinion’) disregarding the pervasive nature of the material misstatement.

(Para 36 to 40)

ii. In another case, the ET did not obtain sufficient appropriate audit evidence for non- provision of impairment losses on investment in subsidiaries that had serious issues of going concern. The ET relied on outdated and unsigned documents regarding financial support assistance purported to be issued by overseas parent.

(Para 41 to 44)

Inspection Overview

1. Section 132 of the Companies Act 2013, inter alia, mandates NFRA to monitor compliance with Auditing Standards, to oversee the quality of service of the professions associated with ensuring compliance with such standards, and to suggest measures required for improvement in quality of their The relevant provisions of NFRA Rules prescribe control system of the auditor and the manner of documentation of the system by the Auditors. Under this mandate, NFRA initiated audit quality inspections in December 2022. The overall objective of audit quality inspections is to evaluate compliance of the Audit Firm / Auditor with auditing standards and other regulatory and professional requirements, and the sufficiency and effectiveness of the quality control system of the Audit Firm / Auditor, including:

(a) adequacy of the governance framework and its functioning;

(b) effectiveness of the firm’s internal control over audit quality; and

(c) system of assessment and identification of audit risks and mitigating measures

2. Inspections involve a review of the quality control policy, review of certain focus areas, test check of the quality control processes, and test check of audit engagements performed by the Audit Firm during the year.

3. Inspections are, however, not designed to review all aspects and identify all weaknesses in the governance framework or system of internal control or audit risk assessment framework and are also not designed to provide absolute assurance about the Audit Firm’s quality of audit In respect of selected audit assignments, inspections are not designed to identify all weaknesses in the audit work performed by the Auditors in the audit of the financial statements.

4. Inspections are intended to identify areas and opportunities for improvement in the Audit Firm’s system of quality control. Inspection reports are also not intended to be either a rating or a marketing tool for Audit Firms.

Audit Quality Inspection Approach

5. Selection of Audit Firms for the 2022 inspections was based upon the extent of public interest involved, as evidenced by the size of the firm, its composition and nature, the number of audit engagements completed in the year under review, complexity and diversity of preparer’s financial statements (henceforth, Companies) audited by the firm and other such risk indicators. M/s Walker Chandiok & Co. LLP was one of the audit firms selected as per the above parameters.

6. The selection of individual audit engagements of the Audit Firm was largely risk-based, based on financial and non-financial risk indicators identified by Accordingly, the Audit Files in respect of five (5) Audit Engagements relating to the statutory audit of financial statements for the year ending 31.03.2021 were reviewed during the inspection.

7. The scope of the inspection was as follows:

a. Review of Firm-wide quality controls to evaluate the Audit Firm’s adherence to SQC 1, Code of Ethics and the applicable laws and rules. Focus areas for the year 2022 inspection related to critical elements of the Firm’s quality control system , auditor independence, acceptance and continuation of audit clients, engagement quality control and the Audit Firm’s internal quality inspection program.

b. Review of individual Audit Engagement Files – A sample of five (5) individual audit engagement files pertaining to the annual statutory audit of financial statements for the year ending 31.03.2021 was selected. Three significant audit areas were identified in respect of each audit engagement viz., revenue, trade receivables and investments, due to their inherent higher risk of material misstatement.

The selected sample of five individual audit engagements is not representative of the Firm’s total population of the audit engagements completed by the Firm for the year under review.

Inspection Methodology

8. An entry meeting was held with M/s Walker Chandiok & LLP on 28.11.2022 at NFRA office. The Firm presented an overview of the Governance and Management Structure, Firm-wide System of Quality Control, and their audit approach and methodologies, including IT Systems. The on-site inspection was carried out in December 2022. The inspection methodology comprised meetings, walkthroughs, presentations and interviews with some members of the leadership team as well as the Engagement Teams of the selected audit engagements.

9. The areas of weaknesses or deficiencies on the part of the Audit Firm, included in the inspection report, should be understood as areas of potential improvement and not as negative assessment of the work of the Audit Firm unless specifically indicated otherwise.

Audit Firm’s Profile

10. M/s Walker Chandiok & Co. LLP, a Limited Liability Partnership, is a member of M/s Walker Chandiok & Affiliates, which is registered with The Institute of Chartered Accountants of India (ICAI). As per the submissions of the Firm, it is a network of two audit The Firm has fifteen offices in India and has more than 60 partners. The Firm was statutory auditor of 212 entities in FY 2020-21, which were under NFRA purview. Five of these company audits were selected for review.

Acknowledgement

11. NFRA acknowledges the general co-operation extended by M/s Walker Chandiok & Co. LLP during the inspection.

PART B

Review of Firm-Wide Audit Quality Control System

A. Audit Documentation

12. The Audit Firm maintains audit documentation both electronically and in physical form (hard files). The audit documentation up to the time of its archival (within the 60-day timeframe stipulated in SQC 1) lacks integrity as required under Paras 77, 79 and 80 of SQC The physical files are neither scanned and incorporated in the electronic files, nor cross-referenced to the electronic files, making it difficult to demonstrate completeness of the audit file and whether it was compiled within the 60-day timeframe stipulated in SQC 1.

13. The Audit Work Papers (henceforth, AWP) contain documents and information obtained from the clients as well as those prepared by the ET. It is important to identify the source of the document and information used as audit evidence to ensure their reliability and integrity. However, we observed instances where adequate details such as whether it was obtained from the clients, and from whom and when it was obtained were missing. This could have potential risks of non-compliance with SA 500, SA 540 and SA 550.

14. In response to the draft inspection report, the Firm stated that the hard copy files are submitted to designated file managers within the documentation assembly period, and after completion, access is restricted, requiring central approval for retrieval. The Firm acknowledged the observations regarding the absence of cross-referencing of physical working papers to the electronic files and has since issued internal guidance to reinforce indexation and cross-referencing The Firm cited Para 15.25 of its Audit and Assurance Service Manual (AASM), which provides the guideline to indicate if workpapers were prepared by the client’s personnel and stated that the engagement teams had inadvertently missed to include such identification in some working papers.

B. Deviations from Independence norms

15. We observe that WCCL, GTBL, GTAPL and GTIL are ‘directly or indirectly’ related entities as per Explanation (ii) to Section 144 of the Companies Act, 2013 (henceforth, Act) and ‘Network’ as per Para 6(k) of SQC 1. We note that WCCL, in its filings with PCAOB declared that it had no ‘audit related memberships, affiliations or similar arrangements’ with any other entity. On the contrary, GTBL declared in its filings to PCAOB that it had ‘audit related memberships, affiliations or similar arrangements’ with GTIL and WCCL. The Firm denied any ‘direct or indirect’ relationship or any membership with GTIL and denied existence of any ‘Network’ with GTBL, GTAPL and GTIL, and stated as follows:

i) WCCL and Walker Chandiok & Associates LLP comprise the ‘Network’ “Walker Chandiok & Affiliates”.

ii) WCCL, GTAPL and GTBL are separate legal entities and are related parties as per the Companies Act.

iii) WCCL and GTAPL, including GTBL and other related entities, have agreements executed on arm’s length basis for resource sharing, hiring of professional staff, providing infrastructure/ specialist services, including information technology support and maintenance services.

iv) WCCL had executed a non-exclusive and non-transferable software license agreement with GTAPL for use of e-audit software.

v) Due to close relationship between Mr. Vinod Chandiok (father) and Mr. Vishesh Chandiok (son), WCCL shares the audit client details with GTBL through restricted lists to ensure that neither WCCL nor GTBL or any of their related entities, provide prohibited non-audit services to the audit clients.

vi) The reason for GTBL’s declarations to PCAOB regarding ‘audit related memberships, affiliations or similar arrangements’ with WCCL was because of the existence of supplier arrangements to hire staff on arm’s length However, since WCCL did not provide any audit services to any issuer, their declarations to PCAOB for ‘audit related memberships, affiliations or similar arrangements’ was marked as ‘No’.

vii) The Firm denied existence of ‘Network’ as per Para 6(k) of SQC 1 as there is no cooperation and profit or cost-sharing, common ownership, control / management, any common quality control policies, procedures and/ or common business strategy, the use of a common brand name or any significant part of professional resources with GTIL/GTBL/GTAPL.

16. The relationship between the different network entities, including the Firm is shown in Figure We observe that there is ‘direct or indirect’ relationship amongst WCCL, GTBL, GTAPL and GTIL, as per Explanation (ii) to Section 144 and that these entities are also part of a ‘Network’ as per Para 6(k) of SQC 1 because of the following reasons:

i) Vinod Chandiok controls WCCL. Mr. Vishesh Chandiok (son of Mr. Vinod Chandiok) has majority control in GTAPL. GTAPL is a member firm of global network of GTIL. GTAPL along with Mr. Vishesh Chandiok and others have significant influence on GTBL. There are multiple references of the brand ‘GT’ traceable from the quality control policies and the e-audit software etc.

ii) The Engagement Quality Control Manual (EQCM) of the Firm contains multiple references to The EQCM refers to use of GTIL policies, procedures, software, including sharing of the audit client details; direct influence of WCCL’s audit processes while working on the audit software; reliance on GTIL processes for confidentiality, working in foreign jurisdiction, independence checks, client acceptance & continuance, archival of audit files, and assessment of cyber security plan; and sharing of manpower resources between WCCL and GTIL network firms etc. This clearly establishes the sharing of significant professional resources, policies, and procedures.

iii) The Firm’s contentions that there is no cooperation amongst the parties, i.e. WCCL, GTBL, GTAPL, GTIL cannot be accepted because by sharing the client details and through other means, one party is able to restrict the other party from providing certain services to the auditee companies, signifying cooperation. The cooperation may not necessarily be in writing amongst them.

iv) There is a documented policy and practice through which client details are shared by WCCL with GTIL to ensure compliance with section 144 of the Companies Act, However, its implementation could not be ascertained, as the inspection team did not have access to data of GTIL. Therefore, compliance of the Firm with the provisions of section 144 of the Companies Act, 2013 could not be verified.

Figure 1: Pictorial depiction of relationship of the Indian entities with the global network of GTIL

Legend –

- This indicates sharing of resources at arm’s length basis as conveyed by the

- Entities in this box are ‘Network’ as per WCCL, registered with

- Entities in this box are ‘Related Parties’ as per

- As per our observations, entities in this box are part of a ‘Network’ as defined in SQC

The Quality Control Policy of the Firm, EQCM, does not cover the mandatory requirements of the Companies Act, 2013.

17. The Policy of the Firm does not prohibit all the prohibited non-audit services as listed in Section 144 of the Companies Act, For instance, the EQCM policy of the Firm does not prohibit the following non-audit services:

i. Investment advisory services

ii. Investment banking services

iii. Outsourced financial services

iv. Management services

18. The Firm pointed to para 26 of EQCM, stating the requirement for all personnel to adhere to ethical and independence requirements as per the Act and other Indian laws. However, in view of the incomplete list of prohibited non-audit services in EQCM, there is scope for confusion and the Firm is advised to include, at a minimum, the services in the list as prescribed by the Act.

Sign- offs regarding Independence Confirmation were not obtained from the ET members

19. It is noted that, there were no signoffs from some of the ET members / the EP / the EQCR partner, pertaining to the independence declaration in the e-audit files of the selected audit engagements.

20. The Firm acknowledged the absence of independence declarations in e-audit files and stated that they are working to ensure completeness of required declarations.

Prohibited Non-Audit Services provided by the Firm

21. In one case, where the Firm was appointed to audit a group’s consolidated financial statements, the Firm also provided prohibited non-audit service of “consolidation procedures for certain related entities,” which was in violation of the provisions of Section 144 of the Companies Act, 2013. The Firm charged separate fees for this service which was 66% of the statutory audit The Firm submitted that the company, its subsidiaries, and associates had adopted Ind AS 1153 as a new accounting standard from April 1, 2018, a process deemed complex, necessitating careful evaluation of judgments and estimates. Additionally, the company implemented hedge accounting in one subsidiary and other intricate financial instruments, requiring additional resources. As a result, a separate fee agreement was reached with the Company.

22. The inspection team noted that at the time of signing of the Engagement Letter (EL), the auditor was aware of the scope of work. Thus, charging a separate fee for “consolidation procedures for certain related entities” and for “review of Ind AS 115 or hedge accounting” was not in compliance with the provisions of Section 144 of the Act and also created a self-review threat.

23. In another case, it is noted that the Firm provided non-audit services in the form of reviewing the related party transactions and giving assurance on the same to the Board of Directors. By rendering such prohibited non-audit services under section 144, the Audit Firm was not eligible to continue as statutory auditors under section 141 (3) (i) of the Companies Act, 2013.

24. The Firm stated that the said assurance service was performed as per the requirements of Section 92E of the Income-tax Act, 1961 and was a sub-set of the overall Form 3CEB certification, therefore it did not create any self-review or any other threat to the independence. These assertions of the Firm are in contradiction to those documented by the ET in the Audit Work Papers (AWP), where the ET had recorded that the Board of Directors sought a quarterly statement of related party transactions from the Management, along with an analysis of whether these transactions were conducted at arm’s length. The scope of work was “to undertake discussion(s) with the management to understand ‘as is’, related party transactions and current policies for monitoring and documenting the related party transactions”. Review of the arm’s length price (ALP) included “analysis maintained by the company including review of the supporting documents / reports, benchmarking search maintained by the company to support the said ALP analysis”. The ET had noted that the nature of certification by WCCL will be very similar to the certification of Form 3CEB, except that the proposed certificate will be addressed to the Board of Directors and not the Income Tax authorities. Such services could cause a self- review threat, apart from being prohibited non-audit services, as the output from these services would also be audited during the statutory audit of the company.

C. Client Acceptance and Continuance Policies

25. On perusal of some of the cases and their audit files, it was observed that the Firm has a practice of requesting background checks on the auditee companies from database of GTIL for integrity testing. In some cases, background check responses from GTIL were not positive, however, the Firm did not perform any alternative procedures to assess the prospective/existing client’s integrity before accepting/continuing the audit engagement. The Firm’s reliance solely on a single source, GTIL, for assessing the integrity of client personnel is insufficient and does not fulfill the requirements of Para 28 of SQC 1.

26. In response, the Firm asserted that their policy is in compliance with relevant requirements of SQC 1 and requires communications with existing or previous service providers of client under consideration, discussions with third parties (for example client engaged bankers, legal counsel and industry peers), inquiry from other firm personnel, background checks conducted on the client using relevant third-party databases. The Firm also added that its EQCM prescribes assessing the competence and bandwidth to conduct the engagement, and the engagements are accepted in compliance with Para 28 of the SQC

27. We observe that the procedures followed by the Firm, other than the confirmation obtained from GTIL, are not documented. No audit documentation was found in relation to evaluation of the competence and capabilities of the audit firm to undertake the

D. Engagement Quality Control Review

28. SQC 1 and SA 220 requires the EQCR partner to document the performance of the procedures for the quality review as per the policy of the Firm, completion of review before report issuance, and awareness of unresolved matters that may impact appropriateness of conclusions. The EQCM of the Firm also requires the EQCR partner to review and sign off on, at the minimum, some AWPs viz. Audit Plan and Risk Assessment, Summary of Significant Matters, Summary of Control Deficiencies, Financial Statement Disclosure Questionnaire and Audit Adjustments etc. However, in some audit engagements, these requirements were not complied with by EQCR We therefore note that the audit documentation on the part of EQCR is not fully compliant with the requirements of para 25 of SA 220.

29. In response, the Firm acknowledged the same and stated that such sign offs could have been missed inadvertently, and therefore they have configured the audit software to require mandatory review and sign off by the EQCR partner.

30. Para 25 of SA 220 requires separate documentation for The inspection team noted that the working papers had no documentary evidence of the work done by EQCR. The Audit Firm should take necessary corrective action to ensure compliance with para 25 of SA 220 regarding documentation by EQCR.

PART C

Review of Individual Audit Engagement Files Focusing on Selected Areas of Audit

31. This section discusses deficiencies observed in a few selected audit engagements. The inspection covered five individual audit engagements, and focused on three audit areas viz. revenue, trade receivables and investments for detailed review. Certain critical audit procedures performed by the Firm’s engagement team in respect of these audit areas were reviewed viz. identification and assessment of risk of material misstatement, internal controls, design and execution of audit procedures in response to assessed risk (test of controls, test of details, sample sizes and analytical reviews etc.), accounting estimates, accounting policies, disclosures and evaluation of identified misstatements. The observations are discussed below.

Impairment of Assets: Non-evaluation of significant assumptions used by the auditee companies.

32. According to SA 5404, the ET was required to evaluate and document the reasonableness of significant assumptions used by the management in accounting estimates such as Value- in-Use, Fair Value etc., which was however missing in some AWP reviewed by the inspection team. We noted that the auditee companies had performed impairment assessment of its investments and computed the Recoverable Amount5 as required by Ind AS 366. As part of computation of Recoverable Amount, the company had calculated Value-in-Use which involves estimation or projection of future cash flows by using various significant assumptions such as business growth rate and discount rate etc. The recoverable amount for investments was derived by using inflated growth rates, ranging from 20% to 105%, but there was no independent evaluation of its reasonableness by the auditor, especially in view of the company’s own historical growth rate, which was much less, approximately 5.8% p.a. Similarly, the equity risk premium used for estimating discount rates was based on overall stock market indices (BSE Sensex or Nifty 50), though the shares of the auditee companies were not part of Sensex or Nifty The growth rates used were also not commensurate with the overall industry growth rate predicted by the Management in the ‘Management Discussion & Analysis’ section of the Annual Reports of the auditee companies and their own historical growth rates. The Firm agreed to improve the audit documentation.

Auditee Company A

Absence of Documentation in respect of assessment of accounting for investments

33. During the FY 2020-21, the auditee company reported acquisition of additional 20% ownership interest in a subsidiary wherein it had acquired controlling interest of 80% during the previous FY 2019-20 and accounted the transaction as Business Combination in that year. This acquisition of remaining shares of 20% was pursuant to a forward contract entered into with shareholders of Non-Controlling Interest (NCI) at the time of acquisition of 80% controlling interest in FY 2019-20. The auditee company had treated this forward contract as part of the Business Combination and did not present the 20% ownership as NCI in the consolidated financial statements of FY 2019-20. The consideration for the remaining 20% shares, reportedly, fulfilled the criteria for considering it as ‘Contingent Consideration’ under the applicable financial reporting framework Ind AS 1037 and Ind AS 1098. We observe that the evaluation of whether the forward contract to acquire remaining shares from NCI at a future date to be considered as part of business combination accounting at acquisition date or as separate transactions must be considered based on whether the NCI holder (sellers of the shares) have effectively lost their ownership position at the acquisition date. This assessment needs to be done based on facts such as whether NCI holder continues to participate in positive and negative changes of value in shares and continues to receive dividends on these shares. However, no such assessment was noticed from the audit file.

34. The Firm stated that the cost of investment considered by management was the total of consideration paid and payable for acquiring the subsidiary. While explaining the contingency in consideration payable for acquiring 20% shares, they conveyed that performance of the same was linked with the performance of the subsidiary company. Since the adjustments arose on account of the difference in the estimate of cost at the time of acquisition and the actual cash outflows, the same was recognized by the Company in the Statement of Profit and Loss.

35. We note that the assessment of the auditor regarding the forward contract to acquire remaining shares from NCI is not separately traceable from the audit file. Without confirming the correctness of the business combination accounting followed by the auditee company, we also note that the disclosures in the financial statements for FY 2020-21 and 2019-20 in respect of the forward contract to acquire additional shares at future date and the related contingent consideration arrangements are not in compliance with the requirements of Para B64(g) of Ind AS This para requires disclosure of the description of the arrangement and the basis for determining the contingent consideration recognized at the acquisition date. However, the same has not been given in Note 55(a) and 56(a) of the consolidated financial statements for FY 2020-21 and 2019-20, respectively.

Auditee Company B

Non-compliance with the requirements of Section 186 of the Companies Act, 2013 and Companies (Number of Layers) Rules, 2017

36. Auditee Company B has 92 subsidiaries and 52 associate companies; therefore, it is not in compliance with the provisions of Section 186 of the Companies Act, 2013 and Companies (Number of Layers) Rules, 2017, according to which no company, other than a company belonging to a class specified in sub-rule (2) including Non-Banking Financial Companies (NBFC), shall have more than two layers of subsidiaries. The ET replied that Companies (Number of Layers) Rules, 2017 is not applicable to the Auditee Company because its holding company is a NBFC in category of ‘Core Investment Company Non-Deposit taking- Systemically Important (CIC-ND-SI)’ with asset size above Rs 100 crore and therefore exempt from the above stated statutory provisions.

37. We note that there is no evidence in the AWP whether Company B meets all the six conditions laid down by the Reserve Bank of India that are required to be met for categorization of any NBFC as CIC-ND-SI. Therefore, the Firm’s contention that section 186 is not applicable to the Auditee Company is not supported by evidence. The Firm should have reported this non-compliance in CARO 2016, which was not done.

Failure to consider the potential ‘Material and Pervasive’ impacts of misstatements while expressing audit opinion on the Financial Statements

38. The Firm expressed a qualified opinion on the Financial Statements of the company B for FY 2020-21 due to its inability to comment upon adjustments, if any, that may be required in respect of its financial exposure to its subsidiaries, step down subsidiaries and joint ventures of subsidiaries. The Financial exposures were in the form of the loans, investments in shares and corporate guarantees for financial obligations of subsidiaries. Carrying value of investments accounted for almost 76 % of the total Balance Sheet size and the total financial exposure to certain subsidiaries and associates was amounting to ₹ 4,037.91 crores (41.40% of the total net worth of the company as of 31.03.2021). Therefore, the impact of potential adjustments was material and pervasive. However, the EP erroneously considered the impact as ‘material’ instead of considering it as ‘material and pervasive’ which would have warranted ‘Adverse’ or ‘Disclaimer of Opinion’.

39. In response, the Firm referred to a portion of the definition of ‘Pervasive’ from SA 705 and stated as ‘since the misstatement was limited to specific investments, there is no pervasive impact as per the requirements of SA 705.’ The reasons cited by the Firm are as follows:

i. The qualification was limited only to the investment of the Company in one subsidiary.

ii. It does not have an impact on the recoverability of the outstanding loans (including interest) of ₹ 709.01 crores given to the subsidiary.

iii. In respect of exposure in the form of corporate guarantee given to another related entity, it was stated that the plant remained inoperative due to non-availability of natural gas since its inception except for a brief period in FY 2014-15 and 2015-16.

iv. They did not consider the potential impact of financial exposure in certain subsidiaries and associates as ‘material and pervasive’.

40. The reasons given by the Firm are not acceptable because of the following reasons:

i. The EP failed to consider the total exposure of the company in its subsidiary (₹1,985.33 crores), while evaluating the possible effects of misstatements on the financial There is no explanation for how the ET concluded that there was no impact on the recoverability of the loans given to the subsidiary.

ii. Having noted that another related entity remained inoperative since its inception, except for a brief period of time, due to non-availability of natural gas, the Firm failed to consider the possible effects of misstatements on the financial statements of total exposure of ₹2,056.59 The contentions of the Firm were based on the assumed liquidation value of related entity’s PPE for which there is no audit evidence in the file.

The EP failed to consider the possible effects of the misstatements on the financial statements which were ‘material and pervasive’ and accordingly, required consideration of ‘Adverse opinion’ or ‘Disclaimer of opinion’, as per SA 705. From the response of the Firm, it is evident that the possible effects of misstatements were not only confined to investments but were also having impact on the other account balances like loans and advances, impairment, provision, etc., which indicate to their pervasiveness.

Auditee Company C

Failure to consider the impairment loss on the investments and perform audit procedures to verify the appropriateness of management’s assertions

41. The auditee Company C has 286 subsidiaries of which large majority, at least 255 subsidiaries, were loss making. In respect of two subsidiaries which accounted for c.86.53% of the total investments in subsidiaries, there is no assessment of the need for impairment loss provision as required under Ind AS 36, although there were indicators of impairment. The Management provided a written There are no WPs in the audit file documenting sufficient audit procedures having been performed by the ET for assessment of impairment of investments and the Management’s assertions thereon. The Firm had merely obtained management representation letter stating that there was no impairment loss on the investments.

42. The Firm, in response to the Inspection Team’s observation, provided reasons for non- provision of impairment loss such as positive future cash flows and substantial amount of assets in the form of land parcels etc. However, the AWPs did not have any of this information except a commentary saying that the total exposure of the parent was more than the net worth of these subsidiaries.

Failure to obtain sufficient appropriate audit evidence on the Key Audit Matters reported in the Independent Auditor’s Report.

43. In the Key Audit Matter (KAM) section of the Independent Auditors Report, in respect of going concern assumption assessment the Firm documented audit procedures as follows:

i. Tested the cash flow projections prepared by the management for the period of 12 months from the date of the standalone financial statements;

ii. Obtaining financial support assistance and management agreement from the ultimate holding company.

44. However, our review of the AWP revealed that there was no documentation of the audit procedures mentioned above. In respect of financial support and management agreement with the ultimate holding company, the Firm provided a document, purportedly an extract of the Management Agreement, which was unsigned and undated, and its current validity was not known. Accordingly, there was no sufficient appropriate audit evidence of the audit procedures stated in the KAM section of the Auditor’s Report. The Firm acknowledged that their documentation could have been enhanced by more elaborate testing remarks.

PART D

Chronology of Events

|

S. No. |

Date | Particulars |

| 1. | 28.11.2022 | NFRA email requesting to provide information in continuation to the Pre-Inspection briefing |

| 2. | 29.11.2022 | WCCL email providing information in continuation to the Pre- Inspection briefing |

| 3. | 01.12.2022 to

30.12.2022 |

On-Site Inspection |

| 4. | 16.05.2023 | NFRA email for providing FTP location for uploading of documents |

| 5. | 29.05.2023 | WCCL email for providing documents via 3 emails |

| 6. | 19.10.2023 | Draft Inspection Report sent |

| 7. | 03.11.2023 | WCCL email for requesting extension of time for submitting response to Draft Inspection Report |

| 8. | 16.11.2023 | NFRA email granting extension of time for submitting response to Draft Inspection Report |

| 9. | 18.11.2023 | WCCL email requesting a meeting with the inspection team of NFRA |

| 10. | 20.11.2023 | Meeting held with the WCCL Team |

| 11. | 24.11.2023 | WCCL email for response to Draft Inspection Report (Part A and B) |

| 12. | 26.11.2023 | WCCL email for response to Draft Inspection Report (Part C) |

| 13. | 24.12.2023 | Communication of final Inspection Report to WCCL |

| 14. | 28.12.2023 | Comments on the final inspection report by WCCL |

| 15. | 29.12.2023 | Publication of Inspection Report on the website of NFRA as per Rule 8 of NFRA Rules 2018 |

Appendix A: Audit Firm’s Response to the Inspection Report

Pursuant to Section 132(2) of the Companies Act, 2013 and Rule 8 of NFRA Rules, 2018, the Authority is publishing its findings relating to non-compliances with SAs and sufficiency of the Audit Firm’s quality control system. As part of this process, the Audit Firm provided a written response to the draft Inspection Report, which is attached hereto. Based on the request of the Audit Firm, NFRA has excluded the information from this report which was considered proprietary.

–

Notes:

1 Standard on Quality Control (SQC) 1, Quality Control for Firms that Perform Audits and Reviews of Historical Financial Information, and Other Assurance and Related Services Engagements

2 PCAOB – ‘Public Company Accounting Oversight Board’ (Independent audit regulator of USA).

3 Ind AS 115 ‘Revenue from Contracts with Customers’

4 Para 15 (b) of Standard on Auditing (SA) 540, Auditing Accounting Estimates Including Fair Value Accounting Estimates, and Related Disclosures

5 Para 6 of Ind AS 36, Recoverable Amount of an asset or a cash-generating unit is the higher of its fair value less costs of disposal and its value in use.

6 Indian Accounting Standard (Ind AS) 36, Impairment of Assets

7 Indian Accounting Standard (Ind AS) 103, Business Combinations

8 Indian Accounting Standard (Ind AS) 109, Financial Instruments