Impact of Ind AS on Non-Banking Financial Companies (NBFCs)

1. Applicability of Ind AS to NBFCs:

Coverage:

As per the Companies Ind AS Rules, “Non-Banking Financial Company” means a Non-Banking Financial Company as defined in clause (f) of section 45-I of the Reserve Bank of India Act, 1934 and includes:

– Housing Finance Companies,

– Merchant Banking companies,

– Micro Finance Companies,

– Mutual Benefit Companies,

– Venture Capital Fund Companies,

– Stock-Broker or Sub-Broker Companies,

– Nidhi Companies,

– Chit Companies,

– Securitisation and Reconstruction Companies, Mortgage Guarantee Companies, Pension Fund Companies, Asset Management Companies and Core Investment Companies.

Roadmap:

Ministry of Corporate Affairs (MCA) in its press release dated 18th January 2016 has prescribed the roadmap for implementation of Indian Accounting Standards (Ind AS) for Non-Banking Financial Companies (NBFCs) as under:

Phase I:

| Sr. No. | Criteria | Applicable from |

| 1. | All NBFCs having net worth of Rs. 500 crores or more | Accounting period beginning from April 1, 2018 |

| 2. | Holding, Subsidiary, Joint Venture or Associate Companies of Companies covered under Sr. No. 1 above | Accounting period beginning from April 1, 2018 |

Phase II:

| Sr. No. | Criteria | Applicable from |

| 1. | All NBFCs whose equity or debt securities are listed or are in the process of listing on any stock exchange in India or Outside India and having net worth less than Rs. 500 crores | Accounting period beginning from April 1, 2019 |

| 2. | NBFCs other than those covered in Sr. No. 1 above, that are unlisted companies having net worth of Rs. 250 crores or more but less than Rs. 500 crores | Accounting period beginning from April 1, 2019 |

| 3. | Holding, Subsidiary, Joint Venture or Associate Companies of Companies covered under Sr. No. 1 and 2 above | Accounting period beginning from April 1, 2019 |

Clarification:

- The criteria to be evaluated based on the standalone financial statement of the Company.

- On satisfying above mentioned criteria, Ind AS would be applicable to both Standalone as well as Consolidated Financial Statements of the Company / Group.

- On applicability, Company need to restate comparative figures also as if Ind AS was applicable from the first day of preceding accounting period.

Voluntary Adoption:

- NBFC shall apply Ind AS only if it satisfies the above-mentioned criteria and they shall not be allowed to voluntarily adopt Ind AS.

- However, NBFCs can provide Ind AS compliant financial statement just for the purpose of incorporating it in the consolidated financial statements of Group.

- NBFCs which are not fulfilling above mentioned criteria are required to follow Accounting Standards as specified in Annexure to the Companies (Accounting Standards) Rules, 2006.

Examples:

1. ABC Company Limited is an unlisted NBFC having net-worth of INR 80 Crores as at March 31, 2017. ABC Company Limited is a subsidiary company of XYZ Company Limited (Which is not an NBFC Company) to which Ind ASs are applicable w.e.f April 1, 2018.

Q: Whether Ind ASs are applicable to ABC Company Limited w.e.f 1st April, 2018 or not?

NO, Not even Voluntarily.

Q: If Not, How XYZ Company Limited will consolidate financials of ABC Company Limited while preparing Consolidated Financials for the FY 2018-19?

Two Sets of FS are required to be prepared by ABC. One for Regular Reporting (IGAAP) and one for Group Consolidation (Ind AS)

2. PQR Limited has applied for its registration as NBFC to RBI which is not yet granted. PQR Limited has issued Debentures in the Month of July, 2019 which are listed on an Exchange. Company is into the Business of NBFC and having Net-worth of 380 Crores as at March 31, 2019.

Q: Whether Company needs to Publish its half yearly results as per Part III or Part II of Schedule III to the Companies Act, 2013.

As per Part III of Schedule III. As the company which is carrying on the activity of NBFC but not registered with RBI will also be subject to the roadmap for the applicability of Ind AS as applicable to any other NBFC (ITFG Bulletin 13).

3. SB Limited is a registered stock-broker and has applied for termination of its licence which is not approved even as at balance sheet date.

Q: Whether SB Limited shall follow the road map prescribed for NBFC or not?

No. It is the Activity and not mere the Licence or Registration which decides whether Company is an NBFC or not.

2. Major areas of Impact:

Following are the major areas that will be affected by introduction of Ind AS:

1. Recognition of Interest Income and Expense based on Effective Interest Rate (EIR) Method

| Sr. No. | Treatment under IGAAP | Treatment under Ind AS |

| 1. | Transaction costs* that are incurred to obtain Loans are charged to statement of P&L upfront or over a tenure of Loan. | Considering these transaction costs as finance cost, an effective interest rate (EIR) is determined and based on which these expenses are amortised over a tenure of Loan on systematically basis. |

| 2. | Transaction costs* that are charged from the customer while granting them Loans are recognised in statement of P&L upfront or over a tenure of Loan. | Considering these transaction costs as Interest income, an effective interest rate (EIR) is determined and based on which these incomes are recognised over a tenure of Loan on systematically basis. |

| 3. | Any premium payable on redemption of Debenture or preference share is charged to statement of P&L or adjusted against Security Premium. | Premium payable on redemption is also considered as finance cost and is amortised in statement of P&L over a tenure of Loan based on the Effective Interest Rate determined. |

| 4. | As per the Guidance issued by RBI, NBFCs shall not recognise the Interest Income on Non-Performing Assets (NPAs). | Ind AS 109, requires to recognised Interest based on EIR determined. If Loan is considered impaired, then Interest Income will be accounted on the Loan amount as reduced by Impairment Provision. |

* Example of Transaction costs are Processing charges, Upfront fees, Commission, etc which are paid / recovered at the time of getting / granting the loan.

Illustration:

Assumptions

Loan Amount : 10 Crores

Processing Charges (PC) : 1% of Loan sanctioned i.e. 10,00,000

Tenure of Loan : 5 Years

Rate of Interest : 10%

Repayment : Bullet Payment at the end of year 5

EIR : 10.27%

Impact on P&L

The Effective Interest Rate (EIR) of this borrowing is computed at 10.27%

| Year | As per IGAAP | As per Ind AS | Difference |

| 1 | 1,10,00,000

(Interest + PC) |

1,01,62,934 | 8,37,066 |

| 2 | 1,00,00,000 | 1,01,79,660 | (1,79,660) |

| 3 | 1,00,00,000 | 1,01,98,103 | (1,98,103) |

| 4 | 1,00,00,000 | 1,02,18,440 | (2,18,440) |

| 5 | 1,00,00,000 | 1,02,40,863 | (2,40,862) |

| Total | 5,10,00,000 | 5,10,00,000 | – |

B. Classification of Financial Instruments:

♦ Under IGAAP, there is no such concept of Financial Instruments.

♦ Ind AS 32 defines Financial Instrument as any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity.

♦ Ind AS 109 allows to classify Financial Assets under below three categories:

-

- At Amortised Cost

- At Fair Value through Profit or Loss (FVTPL)

- At Fair Value through Other Comprehensive Income (FVTOCI)

Such classification is based on:

-

- Entity’s business model for managing the financial assets and

- the contractual cash flow characteristics of the financial asset.

♦ Business model assessment based on the contractual cash flow characteristics refers to the way an entity manages its financial assets in order to generate cash flows. For e.g. whether an entity holds asset for the sole payments of Principal and Interest (SPPI) or to earn profits by selling/trading financial assets or both.

♦ Similarly, Financial liabilities can also be classified either at amortised cost or as Fair value through Profit or Loss (FVTPL).

♦ Such classification under Ind AS will affect the valuation of respective financial Instruments based upon the category under which they are classified.

Examples:

| Nature | Business Model | Cash Flow – SPPI? | Income from Trading | Classification |

| Loan Portfolio | To Retain till Maturity | Yes | No | Amortised Cost |

| Investment in Mutual Funds | Short Term Fund Parking | No | Yes | FVTPL |

| Investment in Redeemable Debentures | To Retain till Maturity unless Selling results into higher Profit | Yes | Yes | FVTOCI |

| Derivative Assets – Currency Forward | Hedging | No | Yes | FVTPL / FVTOCI |

| Fixed Deposits with Banks | To Retain till Maturity | Yes | N.A. | Amortised Cost |

| Security Deposits | Will be received back at the end of Contract | Yes | N.A. | Amortised Cost |

| Investment in Subsidiary / Associates |

Separately Covered |

|||

C. Concept of an Equity Instruments and Compound Financial Liability:

♦ Ind AS 32 defines Equity Instruments as any contract that evidences a residual interest in the assets of an entity after deducting all its liabilities.

♦ Compound Financial Liabilities refers to the Instruments which satisfies the criteria of both Financial Liabilities as well as Equity Instruments.

♦ An entity recognises separately the components of a financial instrument that creates a financial liability of the entity and grants an option to the holder of the instrument to convert it into an equity instrument of the entity. For example, a bond or similar instrument convertible by the holder into a fixed number of ordinary shares of the entity is a compound financial instrument.

♦ The issuer of a non-derivative financial instrument shall evaluate the terms of the financial instrument to determine whether it contains both a liability and an equity component. Such components shall be classified separately as financial liabilities and equity instruments based upon the mechanism devised under Ind AS subject to satisfaction of conditions laid down by Ind AS 109.

Examples:

1. ABC Limited has issued 1,00,000 cumulative compulsorily convertible preference shares of Rs. 10 each. The Preference shares will be converted into Equity shares in the ratio of 1:1 at the end of three years from its issuance. Dividend, if declared by company then these shares will have a preference over other equity shares and will be paid at 12% p.a.

Q: What will be the classification of above-mentioned financial instrument? Whether the same will be classified fully as Financial Liability, Equity Instrument or Compound Financial Instrument?

– Equity Instrument (Since Fixed for Fixed Criteria is satisfied for conversion into Equity and Dividend is payable at the discretion of Company)

– Dividend paid on these shares will be reduced from Retained Earnings.

2. ABC Limited has issued 1,00,000 redeemable cumulative preference shares of Rs. 10 each. The Preference shares will be redeemed at the end of three years from its issuance at a premium of Rs 2 per share. Rate of Dividend is 8% p.a.

Q: What will be the classification of above-mentioned financial instrument? Whether the same will be classified fully as Financial Liability, Equity Instrument or Compound Financial Instrument?

– Financial Liability (Since there is no Conversion Option Available)

– The Instrument will be recorded at Amortised Cost using Effective Interest Rate Method

– Dividend Paid on Such Preference share will be considered as Finance Cost and will be debited to Statement of P&L.

3. ABC Limited has issued 1,00,000 cumulative optionally convertible preference shares of Rs. 10 each. The Preference shares will be either converted into Equity shares in the ratio of 1:1 or redeemed in full at the end of three years from its issuance at the discretion of the Holder. Dividend, if declared by company then these shares will have a preference over other equity shares and will be paid at 6% p.a.

Q: What will be the classification of above-mentioned financial instrument? Whether the same will be classified fully as Financial Liability, Equity Instrument or Compound Financial Instrument?

– Compound Financial Instrument (Since it is at the discretion of the holder whether to convert such shares or to get it redeemed on maturity)

Q: What will be Accounting treatment in case company determines that the fair value of like preference shares without the conversion option is Rs. 8 per share (which is derived by discounting Rs. 10 @ Effective Interest Rate of 7.72% p.a.)

Accounting Entries:

| Date | Particulars | Debit | Credit |

| Initial Recognition | Bank A/c (1,00,000 * 10) | 10,00,000 | |

| To Financial Liability (1,00,000 * 8) | 8,00,000 | ||

| To Equity (10,00,000 – 8,00,000) | 2,00,000 | ||

| End of Year 1 | Interest Expense (8,00,000*7.72%) | 61,774 | |

| To Financial Liability | 61,774 | ||

| End of Year 2 | Interest Expense (8,61,774*7.72%) | 66,544 | |

| To Financial Liability | 66,544 | ||

| End of Year 3 | Interest Expense (9,28,318*7.72%) | 71,682 | |

| To Financial Liability | 71,682 | ||

| On Maturity | Option A: If redeemed in Full | ||

| Financial Liability | 10,00,000 | ||

| To Bank | 10,00,000 | ||

| Option B: If Converted into Equity Shares of Rs. 1 Each | |||

| Financial Liability | 10,00,000 | ||

| To Equity Share Capital (1,00,000*1)) | 1,00,000 | ||

| To Securities Premium (1,00,000*9) | 9,00,000 | ||

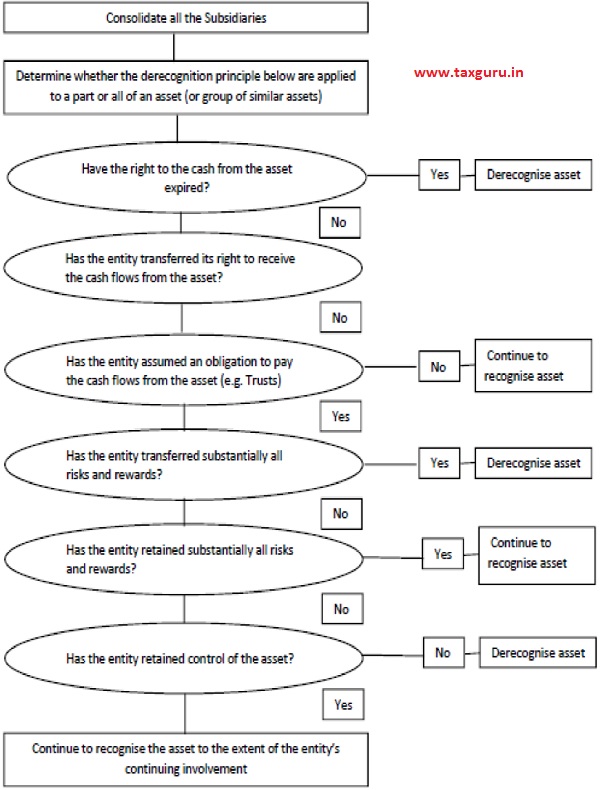

D. Derecognition of Financial Assets:

♦ Under IGAAP, assets were derecognised if it meets the criteria of ‘True Sale’ as prescribed under RBI’s guideline on transfer of Assets through Securitisation and Direct Assignment of cash flows.

♦ Under Ind AS, Asset will be derecognised only if:

-

- the contractual rights to the cash flows from the financial asset expire, or

- an entity transfers the financial asset by transferring the contractual rights to receive the cash flows of the financial asset and substantially all the risks and rewards of ownership of the financial asset.

♦ Further, derecognition criteria needs to be evaluated at Group level and hence NBFCs shall first assess whether the Special Purpose Vehicle (SPV) to which these assets are transferred are required to be consolidated in NBFC or not.

Flowchart to evaluate the Derecognition Criteria:

♦ To evaluate whether entity has transferred all risks and rewards, one need to compute and compare the entity’s exposure to variability in the present value of future cash flows before and after the transfer

♦ Whether the entity has retained the control of the transferred asset or not that depends upon the transferee’s ability to sell the asset.

♦ On derecognition of a financial asset, the difference between the carrying amount (measured at the date of derecognition) and the consideration received (including any new asset obtained less any new liability assumed) shall be recognised in profit or loss.

Illustration

Assumptions

Outstanding Amount of Portfolio Loans : Rs. 1,00,000

Rate of Interest (Coupon and EIR) : 10%

Direct Assignment of Cash flows : 90% Principal Amount at Interest Rate of 9.5%

Consideration : Rs. 91,000

Fair value of Interest Spread : Rs. 500

(on the date of derecognition)

Pending Loan Tenure : 2 Years

♦ Here, the entity retains rights to Rs.10,000 of collections of principal plus interest thereon at 10%, plus the excess spread of 0.5% on the remaining Rs. 90,000 of principal.

♦ Collections from prepayments are allocated between the entity and the transferee proportionately in the ratio of 1:9.

♦ The entity determines that it has transferred all significant risks and rewards of ownership in relation to the Portfolio which it has assigned.

♦ Consideration received includes upfront payment of Rs. 91,000 plus, present value excess interest spread of Rs. 500.

♦ Profit on derecognition will be difference between total consideration (received + receivable) less carrying value of portfolio assigned i.e. Rs. 1,500 (91,000 + 500 – 90,000).

♦ Accounting Entry on derecognition (IGAAP):

| Particulars | Debit | Credit |

| Original Loan Portfolio Asset | 90,000 | |

| Consideration Received – Bank | 91,000 | |

| Deferred Profit on Derecognition | 1,000 |

Deferred Profit will be recognised in statement of P&L over a period of remaining loan tenure. Excess Interest Spread will be recognised as an Income on accrual basis.

♦ Accounting Entry on derecognition (Ind AS):

| Particulars | Debit | Credit |

| Original Loan Portfolio Asset | 90,000 | |

| Consideration Received – Bank | 91,000 | |

| Asset for the consideration received in the form of excess spread | 500 | |

| Profit on Derecognition | 1,500 |

♦ Immediately following the transaction, the carrying amount of the asset is Rs. 10,500 comprising Rs.10,000, representing the allocated cost of the loan portfolio retained and Rs. 500, representing the receivable in form of interest spread.

♦ In subsequent periods, the entity recognises the consideration received on the recognised asset using the effective interest method.

E. Employee Benefit Plans:

| Sr. No. | Treatment under IGAAP | Treatment under Ind AS |

| 1. | In case of Defined Benefit Plans, Remeasurements such as Actuarial Gains and Losses on Obligations and Plan Assets are recognised in Statement of P&L as Employee benefit expense. | In case of Defined Benefit Plans, Remeasurements such as Actuarial Gains and Losses on Obligations and Plan Assets are recognised in Other Comprehensive Income which will not be reclassified to Statement of P&L at later stage. |

F. Fair Valuation of Investments:

| Sr. No. | Treatment under IGAAP | Treatment under Ind AS |

| 1. | Under AS 13, Current investments are carried at lower of cost and fair value whereas Long term investments are carried at cost less provision for diminution, other than of temporary nature, in value of such investments. | Ind AS 109, requires to value all Investments which are classified as FVTPL or FVTOCI at Fair value in accordance with Ind AS 113.

However, for Investment in Subsidiary, Associate and Joint venture companies, an option is given to value it at Cost also. |

G. Expected Credit Loss (ECL):

♦ Under current regime, Loan loss provisions are created based on the guidelines issued by Reserve Bank of India (RBI).

♦ The current provision model devised by RBI based on the historic study actual loan losses against this, Ind AS requires NBFCs to follow the ECL model, wherein the loan loss provision is calculated on the basis of the entity’s historical loan loss experience and future expected credit loss depending on credit quality assessment.

♦ The model should not be built only based on historical data but NBFCs also need to consider forward-looking information such as Loan recovery patterns, time of recovery, probability of default and recovery expected from collaterals.

♦ Expected credit loss model establishes 3 stage impairment model, based on whether there has been a significant increase in the credit risk of a financial asset since its initial recognition. These 3 stages determine the amount of impairment to be recognized as Expected Credit Loss at each reporting date.

♦ if, at the reporting date, the credit risk on a financial instrument has not increased significantly since initial recognition (stage 1), an entity shall measure the loss allowance for that financial instrument at an amount equal to 12-month expected credit losses.

♦ At each reporting date, an entity shall measure the loss allowance for a financial instrument at an amount equal to the lifetime expected credit losses if the credit risk on that financial instrument has increased significantly since initial recognition (stage 2) or is credit impaired (stage 3).

♦ Ind AS 109 talks about two type of credit loss viz. 12 Month ECL and Lifetime ECL. Lifetime expected credit losses estimates the risk of a default occurring on the financial instrument during its expected life. 12-month expected credit losses are a portion of the lifetime expected credit losses and represent the lifetime cash shortfalls that will result if a default occurs in the 12 months after the reporting date (or a shorter period if the expected life of a financial instrument is less than 12 months), weighted by the probability of that default occurring.

♦ Ind AS allows to assess credit risk on an individual or collective basis – considering all reasonable and supportable information, including that which is forward-looking.

Examples:

♦ Individual Assessment

On 1st April 2016, Company X has provided a loan of Rs. 1,00,000 to Company Y for Five years at 10% p.a. interest.

On 31st March, 2018, Company Y is expected to have some cash flow problems due to industry recession. (i.e. Risk has been significantly increased)

On 31st March, 2019, the loan is restructured and extended for another five years because Company Y does not have enough liquidity to repay the loan. (i.e. Loan is now credit Impaired)

Application of ECL will be as follows:

| Date | ECL Stage | Probability of Default | Amount of ECL | Interest Income on |

| 31/03/2017 | Stage 1 | 2% * | 2,000 | Gross carrying amount: 1,00,000 |

| 31/03/2018 | Stage 2 | 40% ** | 40,000 | Gross carrying amount: 1,00,000 |

| 31/03/2019 | Stage 3 | 65% ** | 65,000 | Amortised Cost: 35,000 |

* Probability of the loan defaulting in the next 12 months and company will not get any amount back (i.e. 100% loss)

** Probability that the loan will default over the remaining life of the loan

♦ Collective Assessment

For collective assessment, company can group its Loan portfolio in various ways such as based on the Nature of Loans granted, based on the Customer Groups, by bifurcating the outstanding portfolio into various age buckets, etc.

Company shall determine the Probability of the Default for each of the identified groups based on the past history, future payment forecasts and other relevant factors.

H. Financial Guarantee Contracts:

Ind AS 109 defines financial guarantee contracts as “A contract that requires the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due in accordance with the original or modified terms of a debt instrument.”

Under IGAAP, issuer of Financial Guarantee is required to disclose the same in financial statements as contingent liability against which Ind AS 109 requires issuer of financial guarantee to recognise associated liability in books of account as explained below:

Illustration

M/s Parent Limited (Parent) has issued a financial guarantee to the Bank in respect of Loan taken by M/s Subsidiary Limited (Subsidiary) wherein parent is responsible to make payment of amount due to Bank by subsidiary in case subsidiary fails to discharge its dues.

Assumptions

Tenure of the Loan : 10 Years

Loan Amount : Rs. 1,00,00,000

Guarantee Fees charged : Nil

Fair value of Guarantee Fees determined at Rs. 2,00,000 based on the fees charged by any unrelated entity in case guarantee is issued by them.

Accounting in Books of Parent:

Parent shall recognise liability by Rs. 2,00,000 by adding corresponding amount to the Investment in Subsidiary as this will be treated as deemed capital contribution by Parent as the guarantee was given in its capacity as a shareholder of the subsidiary.

Subsequently, guarantee fees are recognised as an income on straight line basis over a tenure of Loan by reducing the liability to that extent i.e. by Rs. 20,000 in our case.

However, in consolidated Financial statement of the group, the parent shall reverse the aforesaid accounting treatment given in its standalone financial statement.

Accounting in Books of Subsidiary:

Ind AS 109 specifies accounting treatment only for the issuer of the guarantee and doesn’t apply to the beneficiary of a financial guarantee contract.

1. Other Changes:

| Sr No. | Nature | IGAAP | Ind AS |

| 1. | Financial Statements | Includes:

Balance Sheet, Profit & Loss Account, Cash flow Statement and any explanatory note annexed to, or forming part of above. (Prescribed Format – Part I of Schedule III to the Companies Act, 2013) |

Includes:

Balance Sheet, Statement of Profit & Loss including Other Comprehensive Income, Statement of Changes in Equity, Cash Flow Statement, Notes including significant accounting Policies and other explanatory information. (Prescribed Format – Part III of Schedule III to the Companies Act, 2013) |

| 2. | Extraordinary Items | Items of Income or expense to be disclosed separately as extraordinary item if it is distinct from ordinary activities of an entity and are determined by considering the nature of event or transaction carried out by an entity. | Presentation of any item of Income or expense as extraordinary item is prohibited. |

| 3. | Deferred Tax | Deferred Taxes are computed on timing differences identified in respect of items of P&L Statement as per financial books of account and as per income tax. | Deferred Taxes are computed on temporary differences between carrying amount of an asset or liability as per financial books and its corresponding tax base. |

| 4. | Segment Identification | AS 17 requires entity to classify segments into two major categories i.e. Business segment and geographical segment using risk and reward approach where internal financial reporting to management serves only as starting point of identification. | Ind AS 108 says operating segments are identified based on the financial information that is regularly reviewed by chief operating decision maker (CODM) in deciding how to allocate resources and in assessing performance. |

| 5. | Consolidation-Joint Ventures | In the consolidated financial statements, jointly controlled entities are consolidated based on the proportionate consolidation method. | Joint operations are still consolidated as per proportionate consolidation method. However, in the consolidated financial statements, joint ventures are consolidated using equity method. |

| 6. | Non-controlling Interest (Minority Interest) | Losses are attributed to the Minority Interest only to the extent of its outstanding balance. | Losses are required to be attributed to the Non-controlling Interest to the extent of its share even if it results into deficit balance. |

| 7. | Lease | Lessee shall account for lease transactions based on the classification of lease into Operating or Finance Lease. | Lessee shall recognise Right of use (ROU) asset and corresponding lease liability in books. No such classification in operating and finance lease is required. |

Disclaimer: This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice.

Author Bio

1. ABC Company Limited is an unlisted NBFC having net-worth of INR 80 Crores as at March 31, 2017. ABC Company Limited is a subsidiary company of XYZ Company Limited (Which is not an NBFC Company) to which Ind ASs are applicable w.e.f April 1, 2018. Q: Whether Ind ASs are applicable to ABC Company Limited w.e.f 1st April, 2018 or not? NO, Not even Voluntarily.

Query: Would like to read the relevant rule/ para for above Ans. mentioned. Please revert.